BRDCY - Goodyear Tire & Rubber Company Surges On Activist Interest

2023-05-12 18:53:27 ET

Summary

- Shares of The Goodyear Tire & Rubber Company soared over the past two days following interest from activist investor Elliott Investment Management.

- The firm has taken a roughly 10% interest in Goodyear and is pushing for significant leadership and operational changes.

- This could prove to be a great catalyst for additional value creation, but even if this does not come to pass, The Goodyear Tire & Rubber Company shares have nice upside potential.

The past couple of days have been really fascinating for shareholders and market watchers of The Goodyear Tire & Rubber Company ( GT ). After news broke that the company has become a target of Elliott Investment Management , a well-known activist investment firm with around $55 billion in assets under management, shares of the tire manufacturer skyrocketed, closing up 21.4% for the day. The stock continued to rise the day after, May 12th, presumably because of enthusiasm centered around this situation.

Although activist investors have often been considered the vultures of the investment world, some of them do succeed in creating significant value for shareholders. And based on the significant amount of due diligence and openness that Elliott has brought to the table, the market seems to believe that attractive value could be the end result moving forward. Based on an overall assessment of the company, even if we assume that management at the tire manufacturer elects to take a more adversarial approach to this opportunity and ignores what Elliott says, attractive upside likely does still exist. But when you add on top of this the catalyst that is now before us, I would argue that the company is worthy of a ‘strong buy’ rating at this time.

Fascinating developments

On May 11th, shares of Goodyear Tire & Rubber skyrocketed after it became clear, through an open letter , that Elliott Investment Management had taken a 10% economic interest in the enterprise and was pushing for significant changes. With this letter, they included a very detailed presentation on what changes can be made and what the impact would be on the company as a whole. The purpose of this article is not to dig deep into every single item that they discussed. And that's because doing so would just be a complete rehash that you could get by looking at the presentation in question. Rather, I will highlight the key points of their argument and relay to you what my own thoughts are on the matter.

{kind=link}

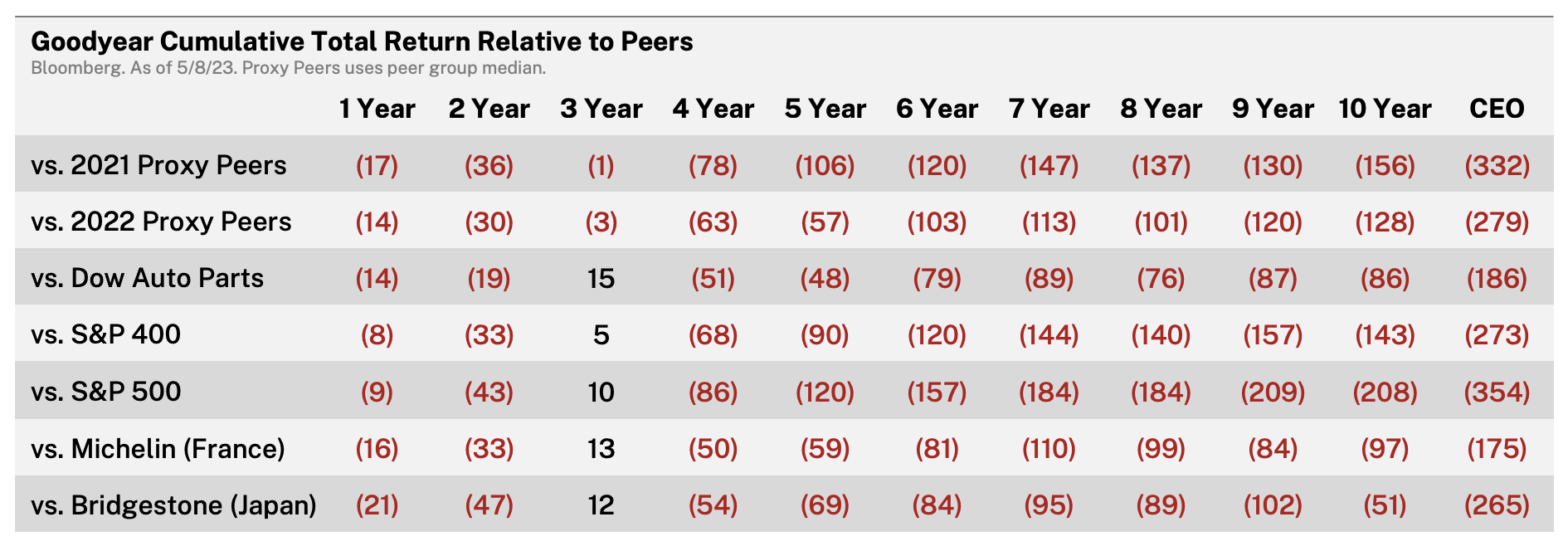

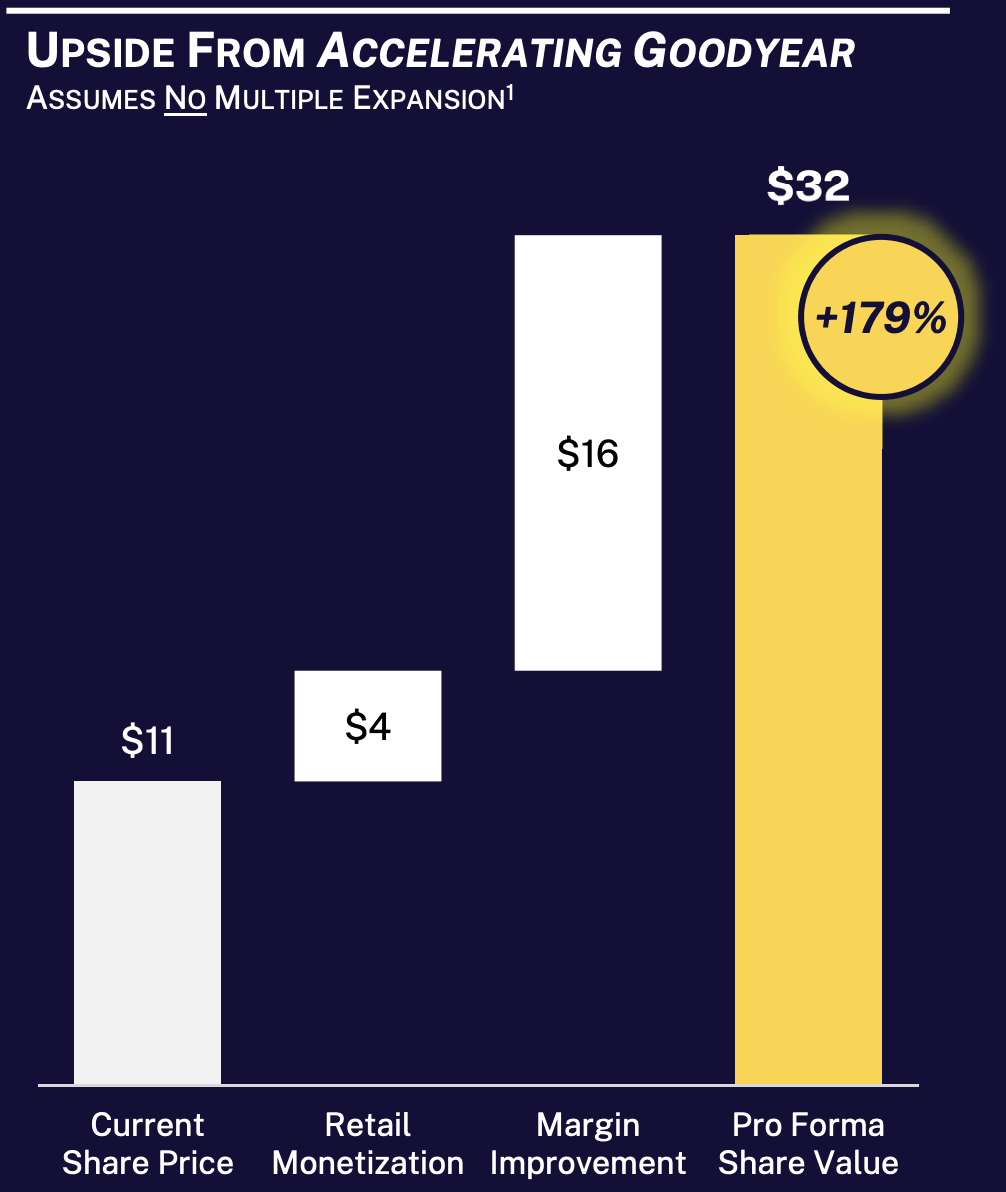

First and foremost, Elliott pointed out that, over the past several years, Goodyear Tire & Rubber has significantly underdelivered from a return perspective. For instance, relative to the S&P 400, the firm has underperformed by 90% over the past five years and by 143% over the past ten. Looking at the S&P 500 (SP500), this underperformance widens to 120% and 208%, respectively. Although many investors would see this as a reason to avoid and investment, activist investors see this as fertile ground to come in, shake things up, and create value. In addition to taking on the aforementioned 10% economic interest in the company, the company also is pushing to install 5 independent directors to the company’s Board of Directors and has laid out a detailed plan on how to significantly increase shareholder value from the roughly $11 per share that the stock was trading at previously to what they believe could be as much as $32 per share.

{kind=link}

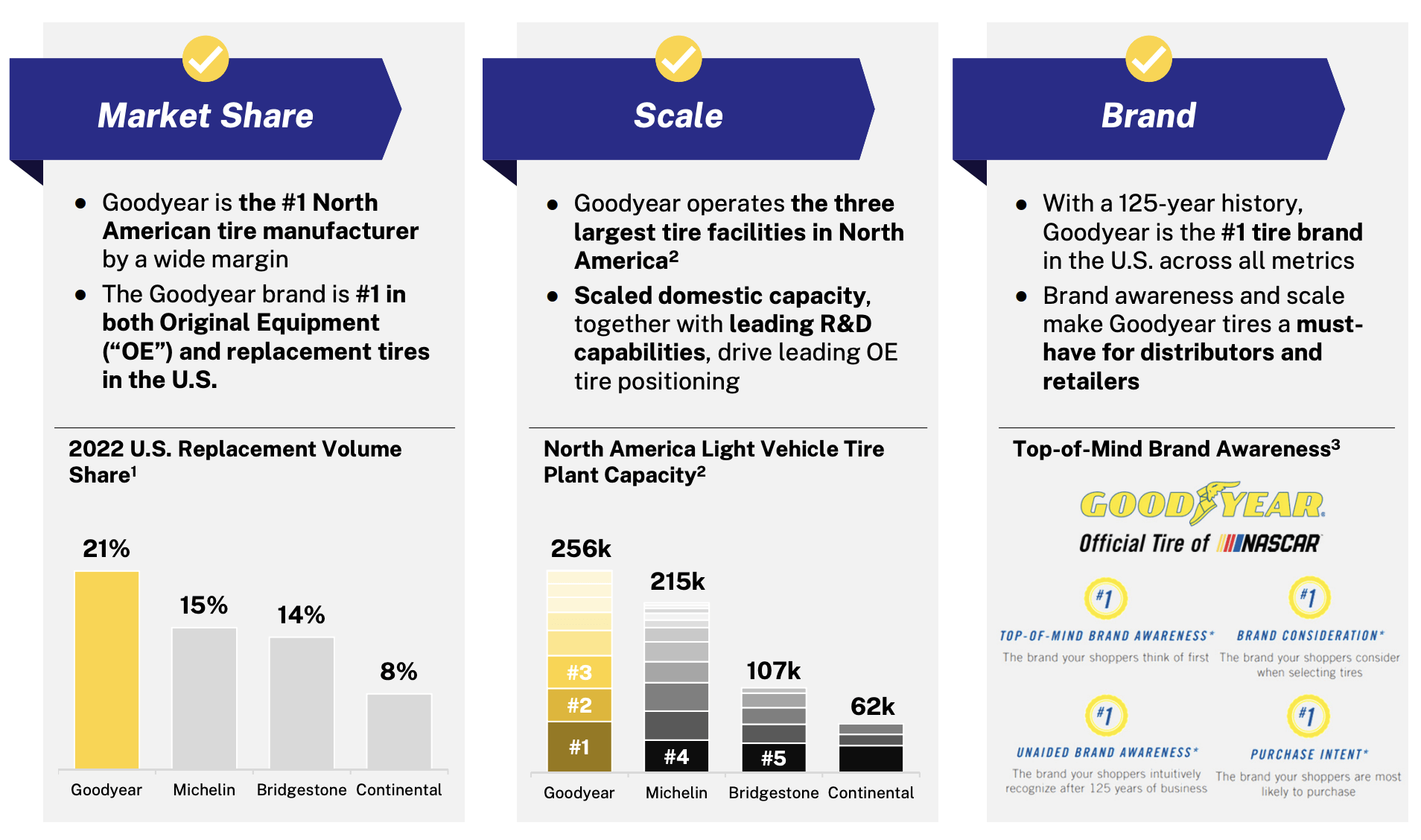

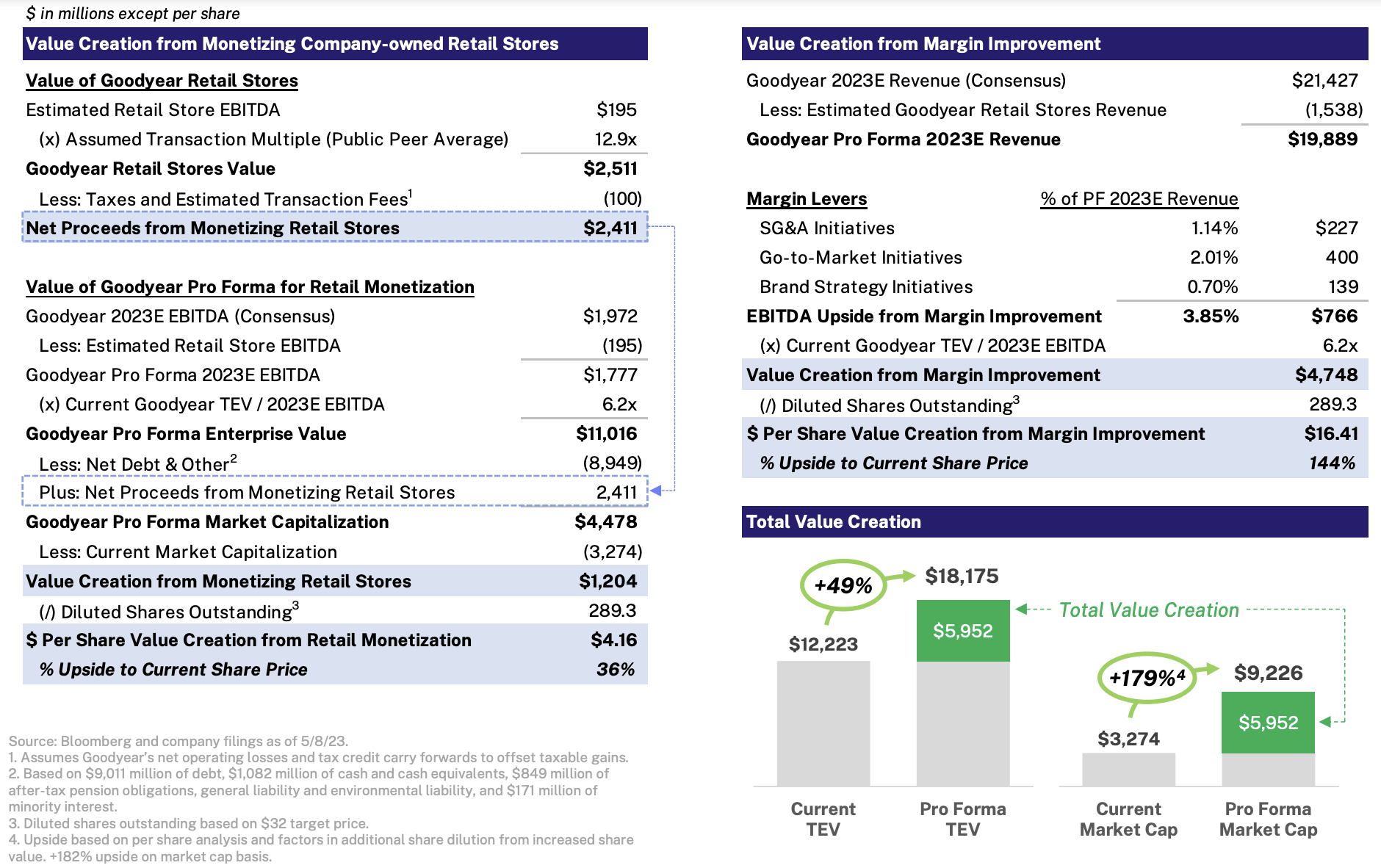

Despite the troubles that Goodyear Tire & Rubber has exhibited in recent years, Elliott pointed out that the business is, in many respects, a true market leader. In North America, for instance, it is the largest original equipment and replacement tire manufacturer and distributor. On the replacement tire side of the market in the U.S., it boasts a 21% market share, placing it 6 percentage points above the next largest rival. The company has been able to maintain this market position because of its large retail store network, as well as other assets. However, poor performance regarding those assets has prevented shares from achieving the upside that Elliott believes that they have.

On the retail side, the company boasts 715 stores, with another 310 under the commercial side. This brings its store count to 1,025 globally, with the vast majority spread throughout North America. Despite the value that's trapped in these stores, Elliott was accurate in stating that, according to J.D. Power, the aftermarket services satisfaction experienced by customers is well in excess of the segment average.

{kind=link}

The management team at Goodyear Tire & Rubber would be wise, according to Elliott, to monetize these assets. Conservatively, they believe that these units could add around $4.16 per share to the company. This is based on an EV to EBITDA multiple for the transaction of 12.9, implying gross proceeds from a sale of $2.51 billion. The transaction would have a negative impact, but only marginally so, on the company's bottom line.

Even larger than this transaction would be areas of improvement that the company has pointed out elsewhere. Cost cutting initiatives when it comes to selling, general, and administrative costs, would have an estimated $227 million in EBITDA value to the company. This is not some random estimate provided by Elliott. Rather, they looked at average selling costs per tire that Goodyear Tire & Rubber pays (excluding its Cooper acquisition). This number came out substantially higher than rivals like Michelin and Bridgestone. And yet, the company operates as an outlier when it comes to consumer awareness relative to price.

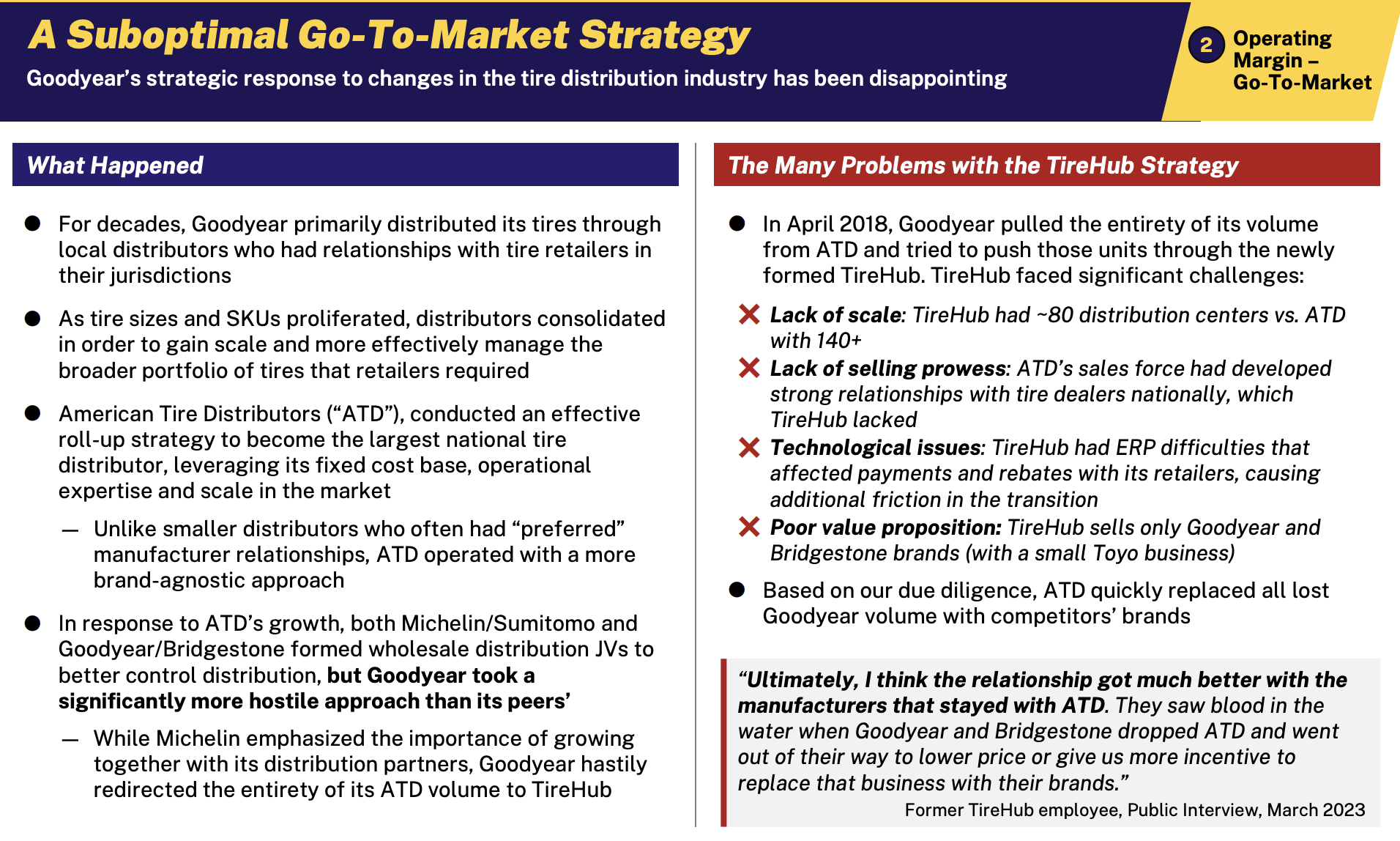

Another fertile area for improvement, according to Elliott, involves Goodyear Tire & Rubber’s go to market strategy. Significant changes in the market, such as massive consolidation aimed at creating efficiencies, resulted in a series of bad decisions by Goodyear Tire & Rubber. In the image below, you can see Elliott summarize these issues quite nicely. But the gist of it is that the company took a rather aggressive approach to American Tire Distributors. And TireHub, Goodyear Tire & Rubber’s national wholesale tire distributor in the U.S., has allegedly been poorly run, has faced technological issues, and has lacked the scale of American Tire Distributors needed to effectively compete.

{kind=link}

By addressing these failures, Elliott believes that Goodyear Tire & Rubber could generate an extra $400 million per year of EBITDA. Certain brand strategy initiatives, meanwhile, could add another $139 million to the pie. Applying an EV to EBITDA multiple of only 6.2 to these extra cash flows could add another $16.41 per share on top of the aforementioned $4.16 per share that the retail asset sale could.

{kind=link}

Goodyear Tire & Rubber makes sense anyways

In response to the letter issued by Elliott, the management team at Goodyear Tire & Rubber released their own letter on May 11th wherein they stated that they value shareholder input and planned to meet with Elliott to discuss matters further. Truthfully, this is just a blanket statement that does not give us any real information of value. In the event that they take the advice offered by Elliott and work closely with them, tremendous upside could still exist for shares. But even if they don't, I would argue that the company offers attractive upside from where it's at today.

Back in early May of 2022, I found myself taking a bullish stance on the tire manufacturer. Although I acknowledged that the company had a rather lumpy operating history, I believed that shares offered attractive upside. This caused me to rate the business a "buy" to reflect my view that it should outperform the broader market for the foreseeable future. Since then, thanks to the recent move higher at least, the stock has done just that. Shares are up 6.3% compared to the 1.8% decline experienced by the S&P 500 over the same window of time.

{kind=link}

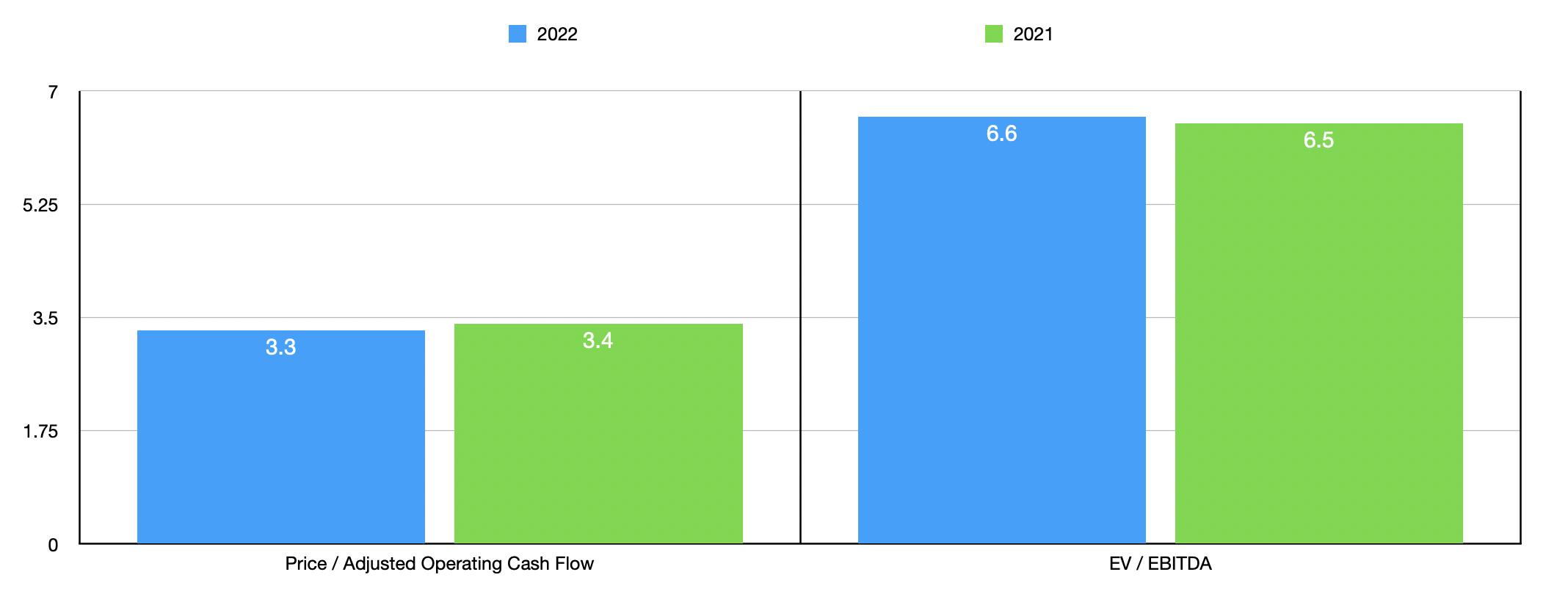

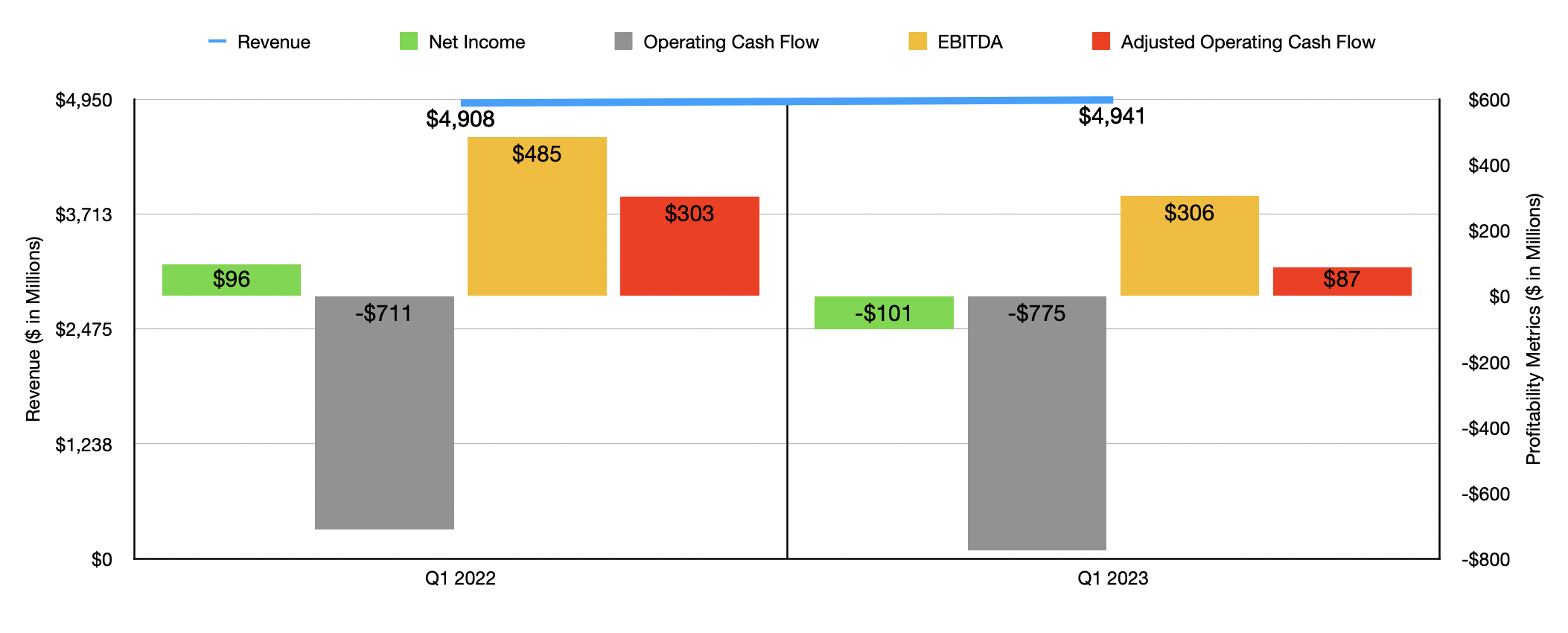

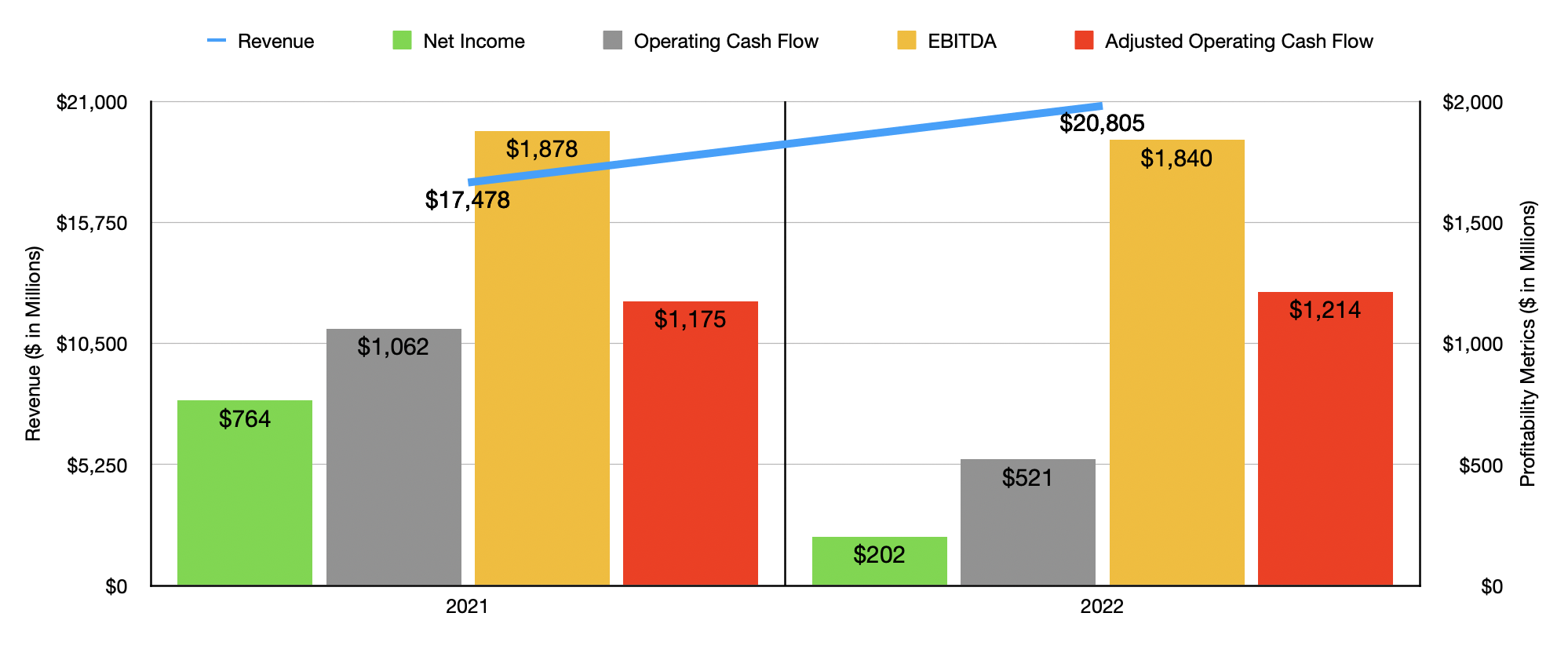

Financial performance since then has been mixed. However, I do still believe that the company offers a good opportunity for long term, value-oriented investors, even if they don't take the advice offered by Elliott. Using data from 2021 and 2022, I was able to value the company. On a price to adjusted operating cash flow basis, the company is trading at a multiple of 3.3. The EV to EBITDA multiple is a bit higher at 6.6 because of the $7.93 billion of net debt on its books. Using the results from 2021, the pricing of the company is similar. It is true that the firm has had a rather rough start to the 2023 fiscal year. Although revenue in the first quarter was 0.7% higher than it was one year earlier, profitability sank, with net profits plunging from $96 million into a negative $101 million.

{kind=link}

A big part of this involved a surge in the cost of sales thanks to higher raw material costs, increased conversion costs driven by inflation, and a reduction in tire production. Restructuring costs also increased during this time, coming in at $32 million compared to the $11 million that they were one year earlier. For the year as a whole, management is forecasting around $100 million of restructuring costs, so that pain isn't over yet. But much of this is centered around streamlining its EMEA distribution network and staff reductions. In fact, in January of this year, management announced that it was cutting their salaried workforce by 5% in a bid aimed at cutting annual expenses by $60 million. So even management acknowledges that things at the business need to change.

{kind=link}

Relative to similar players, Goodyear Tire & Rubber is fairly cheap as well. I compared the company to five similar firms, though only one of these is a pure-play tire manufacturer. On a price to operating cash flow basis, these companies ranged from a low of 1.3 to a high of 60.3. And only one of the five was cheaper than our prospect. Meanwhile, using the EV to EBITDA approach, I found that two of the five were cheaper than it.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Goodyear Tire & Rubber Company |

| 3.3 |

| 6.6 |

| Bridgestone Corporation ( BRDCY ) |

| 13.8 |

| 4.8 |

| Fox Factory Holding Corp ( FOXF ) |

| 15.4 |

| 14.6 |

| Modine Manufacturing ( MOD ) |

| 14.9 |

| 8.0 |

| Dorman Products ( DORM ) |

| 60.3 |

| 17.8 |

| Garrett Motion ( GTX ) |

| 1.3 |

| 2.1 |

Takeaway

Right now, I believe that investors should be very excited when it comes to The Goodyear Tire & Rubber Company and the potential upside it offers. There is a chance that management may take an aggressive, adversarial stance against these proposed changes. But I would hope that they would greet this overture with enthusiasm and explore the value creating initiatives in greater detail.

Even if this move by Elliott does not work, I believe that The Goodyear Tire & Rubber Company offers significant upside. And as such, I have no problem rating The Goodyear Tire & Rubber Company a "strong buy" right now.

For further details see:

Goodyear Tire & Rubber Company Surges On Activist Interest