BRDCF - Goodyear Tire & Rubber: Normally Just A GDP Grower But Significant Upside With Activist's Entrance

2023-07-10 14:19:11 ET

Summary

- Goodyear shareholders have experienced abysmal returns for nearly two decades, and the current management team appears to be as entrenched as ever.

- Activist investor Elliot Management has acquired a 10% stake in Goodyear and plans to appoint five independent directors, though given the company’s annual meeting is next Spring, it is likely they settle before.

- While Elliott Management’s investment horizon is not long-term, their plan to improve margins, better monetize the company’s retail stores, and pay down debt will be beneficial for shareholders.

- Even though the business will be nothing more than a GDP grower long-term, its current dirt-cheap valuation—combined with an activist pushing for change—warrants the attention of value and event-driven investors.

Akron, Ohio-based Goodyear Tire & Rubber Company (GT) is a century-old business that ties its roots to the first Ford Model T. But, for decades now, Goodyear’s stock has been an underperformer and its business has been an under-earner. In the last five years, shareholders have lost 41% on their investment (with dividends reinvested) and the numbers aren’t much prettier 10 or 20 years out, with annualized returns of 0.13% and 4.57%, respectively. As a result, the market has low expectations for future performance and slapped a low multiple on the stock.

However, Goodyear’s business model is not fundamentally broken: while the market for OEM and replacement tires is fully matured, Goodyear’s business should closely track aggregate economic growth in the geographies it sells in. On this point, Goodyear still has the plurality (21%) of the North American tire market and consumer sentiment towards its brands skews widely recognized and well-regarded.

The stock’s current low valuation combined with non-broken, albeit under-earning, business alone makes for a compelling deep-value investment. However, the recent entrance of activist investor Elliott Management (who bought an approximate 10% stake in the company in early May) gives the company a chance to course correct. Elliott Management has zeroed in on two specific shortcomings: (1) Goodyear’s margin profile is worse than its competitors to an unjustifiable degree and (2) its retail stores have underperformed. Additionally, Goodyear is facing nearly $10 billion of financial obligations due within the next five years, and rolling-over debt will be prohibitively costly as interest rates have vaulted upwards. While it’s evident that Elliott Management is out to make money, and their time horizon is not necessarily long-term, I believe there is plenty of low-hanging fruit in Goodyear’s business.

If the ‘turnaround’ plan of introducing additional operational efficiencies and better monetizing its physical stores is realized, I believe the valuation gap between Goodyear Tire and its peers will close. As of early July, I believe there is asymmetric upside for shareholders and remain bullish.

{kind=link}

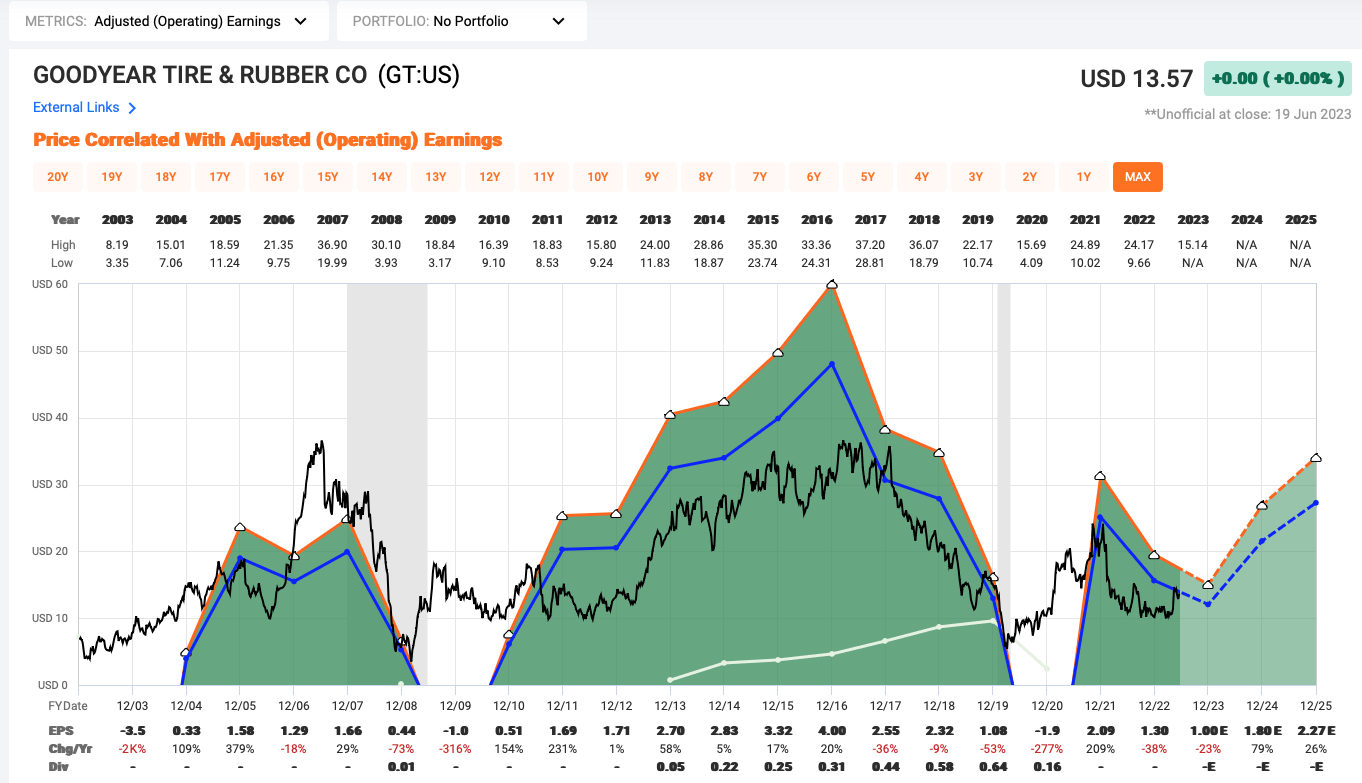

Price (black) plotted alongside operating earnings (green) since FY 2002 using the FASTgraphs analysis tool shows the cyclicality of earnings (however, as examined later, the top line holds steady through the economic cycle). (FASTgraphs)

Goodyear has underperformed relative to both its domestic and international peers (the “proxy peer” refers to companies Goodyear management has called out as peers, many of whom are domestic). (Presentation, Elliot Management)

The Business

While tire manufacturing is not a business model that carries a strong competitive advantage (or a “moat” as some call it), the barriers to entry are relatively high. As the result of industry consolidation, Globally, Goodyear has seized the number #3 title, behind Bridgestone (Japanese, is the ADR) and Michelin (French, is the ADR), neither of which counts the US as their primary market.

The Americas is Goodyear's primary segment, and Goodyear’s brands collectively have the largest share of the US replacement tires with 21% of the market, in front of Michelin (15%), Bridgestone (14%), and Continental (8%) . Fun fact: Goodyear is the only publicly traded tire manufacturer based in the US. It follows that Goodyear’s brand presence within the US is strong. The company is known for its famous “Goodyear blimp” appearances, its sponsorship of NASCAR, and other brands it operates like Cooper, Dunlop, Kelly, Mastercraft, Roadmaster, Debica, Sava, and Fulda.

Because the majority of Goodyear’s sales are replacement tires (as opposed to “OE” or original equipment sales), sales are remarkably resilient through the business cycle, given this is a capital-intensive firm (for context, net PP&E sits on the balance sheet at $7.3 billion, relative to a market cap of $3.8 billion). While the pandemic caused an abnormally large economic shock, sales only declined by 16% from FY 2019 ($14.7 billion) to FY 2020 ($12.3 billion). Pro forma FY 2022 results include approximately two-quarters of the Cooper acquisition and show a 9.0% increase in tire unit shipments (compared to 2021), a strong rebound in OE fitments, and slight gains in domestic market share.

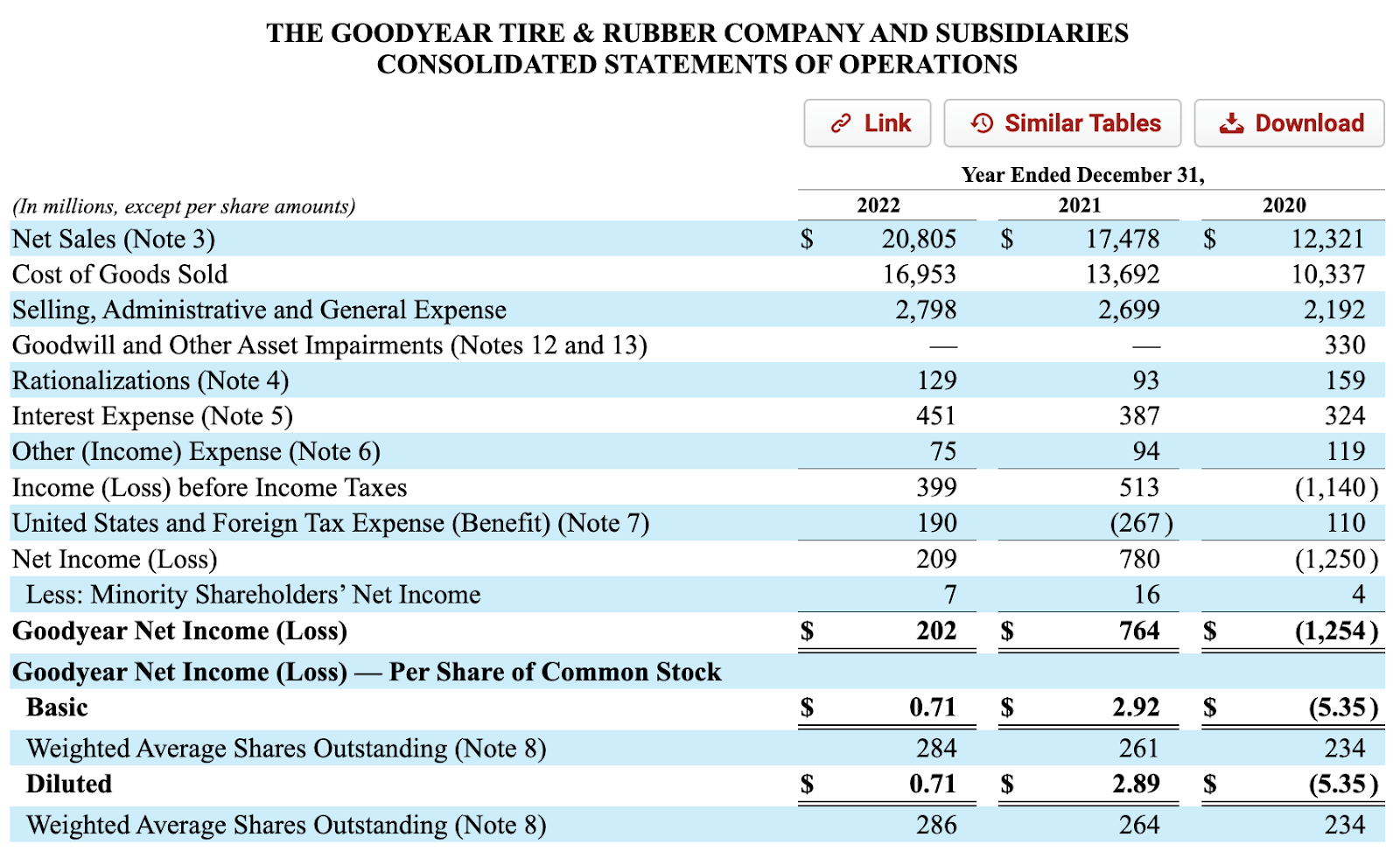

However, ballooning costs caused the bottom line tells a different story. Management Discussion and Analysis (MD&A) in the 2022 annual report cites higher raw material, energy, transportation, and labor costs causing $890 million of incremental costs relative to 2021. Despite revenue increasing by $3 billion from $17.47 billion (FY 2021) to $20.8 billion (FY 2022), these inflationary cost pressures and rising interest expense caused earnings to decline nearly 75%, from $764 million (FY 2021) to $202 million (FY 2022). It is disappointing not to see fixed-cost leveraging (i.e., incremental revenue fall to the bottom line) for a company of this size and scale.

{kind=link}

Form 10-K for FY 2022.

{kind=link}

Form 10-K for FY 2022. Strong top-line growth has been overshadowed by weak cost controls. (Form 10-K for FY 2022.)

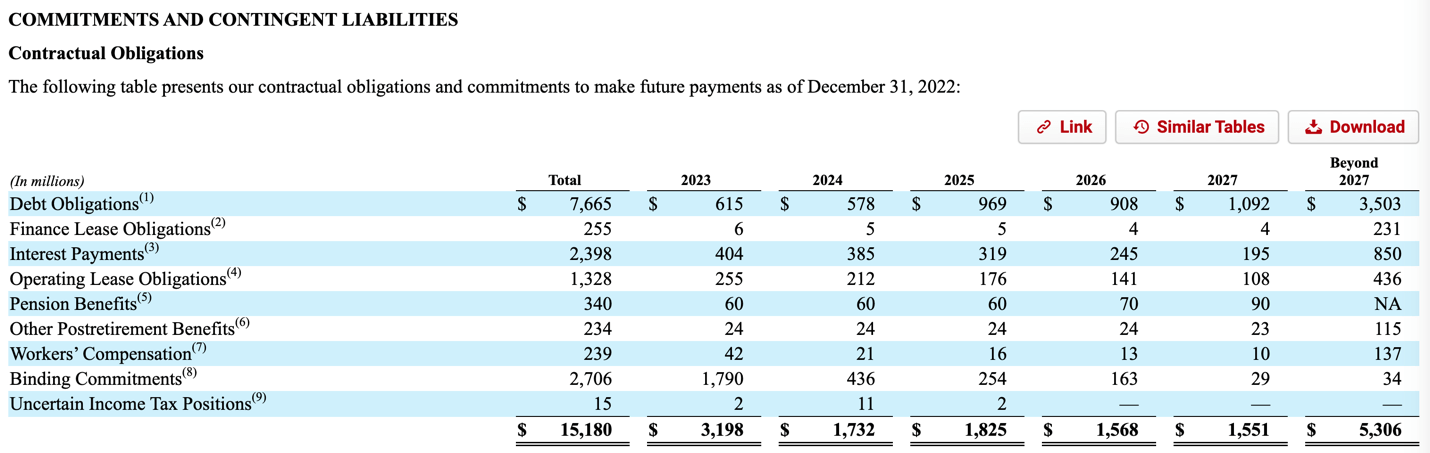

It’s also worth pointing out the significant amount of liabilities coming due over the next five years. In recent years, the company has been able to roll over its annual debt obligations (see the Cash Flows from Financing section of the S/CF). The cost of debt for a steady, GDP-tracking business like this one is quite low, especially when interest rates are near zero. But, as interest rates have sharply risen in the past year, borrowing costs on new debt will become burdensome.

{kind=link}

Statement of CFs (Seeking Alpha )

{kind=link}

Form 10-K

Fundamental Drivers of Value

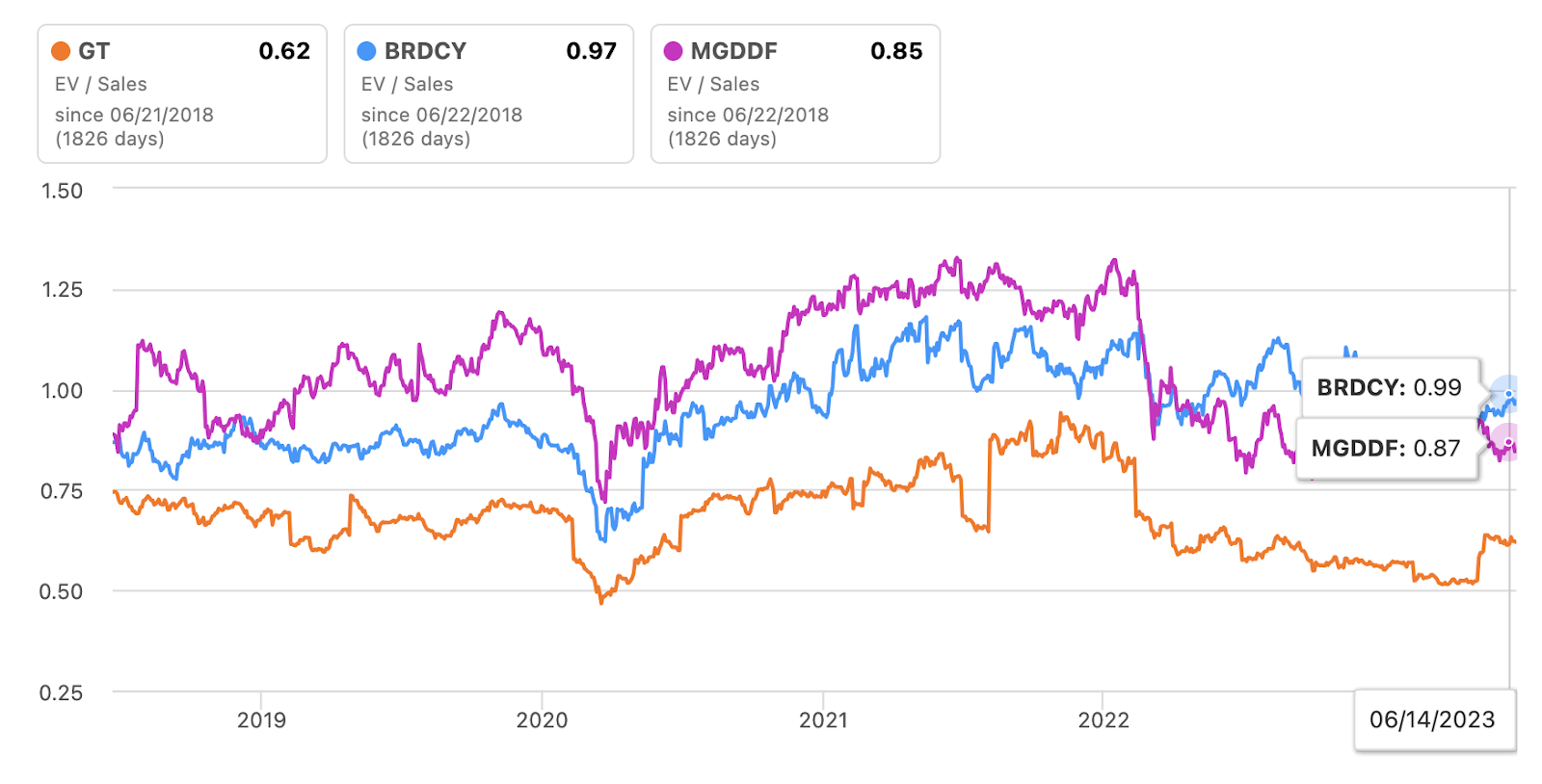

Before I dive into Elliott Management’s recent involvement, let me re-iterate how Goodyear Tire’s stock is compelling from a value POV, despite the overhangs discussed earlier. First, demand for replacement tires (and OEM tires to an extent) is inelastic through the economic cycle as evidenced by how stable the top line is. For a company in the Industrials space, it is in the top echelon of recession-resiliency. Additionally, the current valuation is not demanding. In the following chart, I used the EV to Sales metric, though other ratios tell a similar story. (The P/E ratio would not be a good metric, however, given the cyclicality of the bottom line.)

{kind=link}

Seeking Alpha

Lastly, as it stands today, there is a convincing case for Goodyear Tire to be acquired by either a financial or strategic buyer. For a company with a market cap of just under $4 billion, it is within the realm of possibilities. Financial buyers would predicate their investment thesis on (1) acquiring the business for a low valuation, (2) unlocking the value of company-owned real estate, and (3) driving operational efficiencies. The case for strategic buyers is more complex but equally as compelling. Let me explain.

The industry dynamics of tire manufacturing mean participants operate with low margins, a cyclical bottom line, and largely undifferentiated products. While the industry is not necessarily ‘commoditized’, it exhibits some of the same attributes. As Warren Buffett succinctly said “how to gain an advantage in commoditized industries”, a business must become either the low-cost producer of a good or differentiate its products. Goodyear and its competitors largely function in the same way. No one company has a proprietary product that its competitors can’t replicate. That rules out selling a differentiated product. In terms of becoming the low-cost producer, the main input (rubber) is a commodity whose price can have volatile fluctuations. Goodyear and its competitors are price takers. (Goodyear, specifically, has long-term contracts with suppliers in mainly Southeast Asia.)

However, scale has a large impact on profitability. If a direct competitor purchased Goodyear Tire, they would be able to realize “synergies” by leveraging certain fixed costs like SG&A and R&D. In addition, Goodyear’s distribution channels, including the company-owned stores, provide increased exposure and cross-selling opportunities. The company-owned stores may also make Goodyear attractive to companies operating in an adjacent space as well. Considering how Michelin and Bridgestone both have little market share in the US, and no single company other than Goodyear has more than 20% of the market share in the US, there should be little anti-trust scrutiny.

These three factors alone should pique the interest of deep-value investors, but Elliott Management’s involvement is also a positive development in my opinion, and should pique the interest of event-driven investors as well.

Elliot Management’s Plan to Course Correct

Elliot Management is the infamous activist investing firm led by Paul Singer. As proclaimed on the activist campaign website , Elliot Management has made investments of $4 billion in the automotive space in “original equipment manufacturers (OEMs), suppliers, dealers and finance companies” since 2003. I found very little about the return profiles of these deals, which frankly means they were nothing to brag about. Goodyear, for its part, hasn’t had an activist trying to gain control since 1986, when Sir James Goldsmith and investment company Hanson acquired 11% of the stock .

In April 2023, Elliott launched an activist campaign to address many of the aforementioned shortfalls at Goodyear. Elliot Management suggests they will make many changes, but based on my analysis, I distilled it into three points: (1) boost gross margins by changing the company’s go-to-market strategy, (2) boost operating margins by cutting costs, and (3) find liquidity to pay off debt by selling off Goodyear’s physical stores.

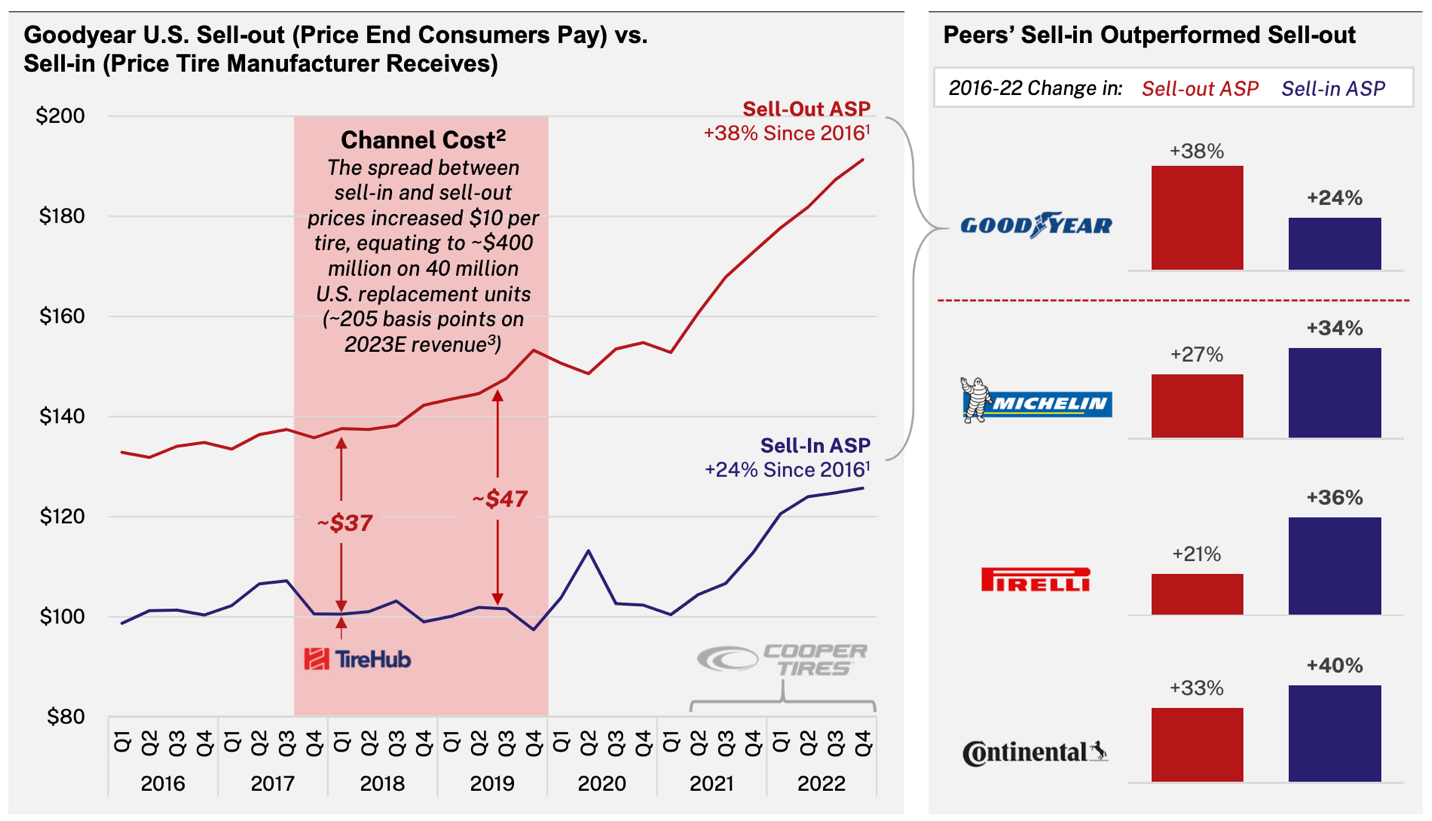

Let’s start with boosting gross margins. At the moment, the namesake Goodyear brand and Cooper (Goodyear’s two biggest brands in terms of sales) are primarily sold through independent dealers. The company’s other brands are primarily sold through company-owned stores, regional/national retailers, and TireHub. TireHub is a wholesale tire distributor, created as a joint venture between Goodyear and Bridgestone in 2018 to compete with American Tire Distributors (“ATD”), which was bought/rebranded by PE firm TPG Capital in 2010 and became the largest national tire distributor in the US after an aggressive roll-up strategy. After TireHub’s establishment, Goodyear terminated its distribution agreement with ATD.

Goodyear's gross profit margin of ~20% is worse than Michelin's (26%) and Bridgestone's (39%). Part of the disparity can be attributed to the fact that TireHub has cannibalized sales from company-owned retail stores since its inception. To maintain market share, management has prioritized market share over total revenue, leading to ~$400 million in unrealized profits according to Elliott (it’s unclear whether Elliott accounted for if higher prices would have driven less volume in their calculation).

Elliot aims to change TireHub’s pricing strategy and revamp its distribution strategy by potentially seeking out alternative partnerships. While it’s hard to discern exactly what volume vs. price mix is optimal, it is clear that the distribution at TireHub leaves much to be desired. While I believe management would eventually shifted in this direction anyway, Elliot's pressure drives an increased sense of urgency.

I also favor Elliott’s plan to deleverage Goodyear’s balance sheet by selling off company-owned stores and using the proceeds to pay down debt obligations. At a 13x EBITDA multiple (public peer average), the retail stores would be worth nearly $2.4 billion. This would go far in covering the solvency needs pointed out earlier. I believe that Goodyear management has given special attention to its retail footprint; the real estate and local presence of the stores make it a target for a financial buyer like PE or a strategic buyer.

{kind=link}

Management’s focus on maintaining volume at TireHub led to lethargic performance at company-owned stores. (Presentation, Elliot Management )

{kind=link}

Admittedly, this graphic is confusing, but it illustrates how favorable pricing for consumers (“Sell-out ASP”) has come at the expense of Goodyear (“Sell-in ASP”). (Presentation, Elliot Management )

Elliot Management also hopes to increase operating margins by cutting out non-core segments, such as Goodyear Ventures and the online merchandising website. While the company’s current cost-cutting plan is already in place (e.g., in January 2023, the company cut corporate headcount by 5% and closed a tire manufacturing facility in Melksham, United Kingdom , that came from the Cooper Tire acquisition), Elliot Management singles out Goodyear Ventures and the online merchandising website as additional places to dispose.

Overall, Elliot Management believes its plan can boost operating margins by 385 basis points. While a nearly 4% OPM improvement is bold in my opinion, it would still leave Goodyear well behind (not even in-line) with Bridgestone and Michelin. (Yes, Goodyear has a small chemicals business, but the business segment mix between these three tire manufacturers is close.)

Elliot Management believes its plan can boost operating margins by 385 basis points. (Presentation, Elliot Management )

Timeline and Logistics of a Possible Showdown

In the past three years, the company’s annual meeting has been held in early April, so Elliott may have to wait another year until it can nominate its own candidates for election to the board. Goodyear and Elliot Management will have ample time to resolve their differences and come to a settlement. However, if a proxy fight does ensue, I believe that Elliot Management would have a good chance at making inroads, given the glaring issues the company has failed to address.

Goodyear’s Board of Directors is composed of 13 members, all with one-year terms (i.e., not a staggered board) and Elliot Management plans to nominate five independent directors, which won’t be quite enough to seize complete control, although it would be enough to exert significant influence (particularly if Elliott were to decisively win a potential proxy contest).

Considering that Elliot Management owns 10% of the company’s stock, and insiders own just 1.6% as of February 2023, it will largely be up to institutional shareholders (as well as their proxy advisors like ISS and Glass Lewis) to decide the outcome. Considering Goodyear’s blatant underperformance relative to peers, Elliot Management would be in a strong position to convince Blackrock, Vanguard, and other institutional shareholders to vote in its favor.

{kind=link}

2022 Proxy Statement

{kind=link}

2022 Proxy Statement

Conclusion

Don't get me wrong, Goodyear is a century-old business that’ll largely track GDP growth over time. The domestic market is completely saturated and competition abroad is fierce. But a steady business that's also remarkably recession-resistant can still lead to phenomenal shareholder returns, especially if management is astute about capital allocation (e.g., and come to mind). Unfortunately, capital allocation has not been a strong suit for management in living memory; this is apparent from the prices of previous ill-timed share buybacks and the inconsistency of dividend payments, which were cut during the pandemic.

Elliott Management has a lot to say, and while activist investors aren’t typically aligned with the company long-term, (mis)management at Goodyear could likely use a shakeup. The current CEO, Richard J. Kramer, joined the company in 2000 and held various senior roles before assuming the CEO title in 2010. In spite of weak shareholder returns, management has nonetheless rewarded themselves with incentive payouts set at 115% in the last three years, even when the company turned a loss in 2020 and made the Cooper acquisition. If even part of Elliott Management’s plan is realized (either by successfully appointing its nominees to Goodyear’s board of directors, or by settling with management without a proxy battle), I believe there is significant potential to realize shareholder value and asymmetric upside for those who buy into Elliott Management's narrative.

For further details see:

Goodyear Tire & Rubber: Normally Just A GDP Grower, But Significant Upside With Activist's Entrance