MNDT - Google Is One Of The Best Capital Appreciation Ideas Out There

Summary

- Alphabet is one of the best capital appreciation ideas out there.

- Through our enterprise cash flow analysis process, we assign GOOG a fair value estimate of $157 per share with room for upside.

- Alphabet has multiple powerful growth drivers at its disposal including Google Cloud, Waymo, digital advertising, and much more.

- Its fortress-like balance sheet and stellar free cash flow generating abilities enable Alphabet to repurchase "gobs" of its stock.

- We cover the process behind our enterprise cash flow analysis process in this article.

By The Valuentum Team

One of our favorite capital appreciation ideas out there is Alphabet Inc ( GOOG ) ( GOOGL ). Through our enterprise cash flow analysis process, we value Alphabet Class C ((ticker: GOOG)) at $157 per share with room for upside, well above where shares of GOOG are trading at as of this writing. We will cover how we arrived at that fair value estimate in this article. Alphabet has tremendous pricing power, dominant market positions in several lucrative areas, is a stellar cash flow generator, has a fortress-like balance sheet, and its longer term growth trajectory is underpinned by powerful secular tailwinds. We appreciate that Alphabet has multiple growth drivers at its disposal.

Alphabet's Key Investment Considerations

Image Source: Valuentum

Known for its search dominance, Alphabet is a tech company focused on a number of things: Android, ads, YouTube, Chrome, and research. We think the company will have some megahits in the years ahead (with an eye towards its rapidly growing Google Cloud division and its self-driving taxi service Waymo). It reports operating losses in its 'Other Bets' category frequently, suggesting core levels of profitability at Alphabet's digital advertising business are higher than reported. YouTube and programmatic advertising offer upside potential, too, but we're watching spending levels, which have spiked due in part to higher traffic acquisition costs.

Alphabet offers investors a compelling combination of attractive valuation, growth potential, cash-flow generation, and competitive profile. Very few firms are more attractive on a fundamental basis, in our view, and its impressive free cash flow conversion rates (consistently above 100%) speak to this. Please note we define free cash flow as net operating cash flow less capital expenditures. The company's free cash flow conversion rate is defined as free cash flow divided by net income for a given period. Alphabet's massive net cash position gives the company a substantial cushion to fall back on as it invests in high return opportunities and new concepts such as smart home features, Glass, Fiber, Waymo, Google Cloud, and other innovative ideas.

Please be aware that Alphabet has three different stock classes with two different tickers. GOOGL is Class A stock, and GOOG represents the non-voting Class C stock that was created by a stock split in 2014 in order for Google founders to maintain majority control.

Earnings Update

When Alphabet reported its second quarter of 2022 earnings update on July 26 the firm missed both consensus top- and bottom-line estimates. However, the company's underlying performance remained rock-solid and we liked what we saw as Alphabet's growth runway remains firmly intact.

Last quarter, Alphabet's GAAP revenues grew 13% year-over-year and 16% on a constant currency basis (the strong US dollar seen of late has been a material headwind for US corporates with large international footprints). Its 'Google advertising' revenues grew nicely (up 12% year-over-year) as did its 'Google Cloud' revenues (up 36% year-over-year), though its 'Google other' revenues pulled back modestly (includes YouTube subscription, Play Store, and hardware sales). Alphabet's GAAP operating income grew marginally year-over-year last quarter as operating expense growth, largely a function of the 21% year-over-year increase in its headcount, ate into its revenue growth.

Alphabet's GAAP operating margin fell ~335 basis points year-over-year to 27.9% in the second quarter of 2022, though please note that Alphabet's core digital advertising business is significantly more profitable than meets the eye. Its 'Google Services' segment generated $20.8 billion in segment-level operating income last quarter while Google Cloud lost $0.9 billion and 'Other Bets' lost $1.7 billion, and the firm also incurred $0.8 billion in unallocated corporate level costs. We expect Alphabet's Google Cloud segment will become a major earnings generator in the medium-term as it scales up this business, though for now Alphabet is focused on gaining market share in this space.

Alphabet's core digital advertising business is more lucrative than first glances would suggest. (Alphabet - Second Quarter of 2022 Earnings Press Release)

While Alphabet's growth rate is clearly slowing down, it's simply stunning that the company can put up double-digit revenue after growing its GAAP revenue by 62% year-over-year in the same period in 2021. Digital advertising remains the best way for most enterprises to communicate to their potential customers and should continue to grow as a percentage of total advertising spend by taking away market share from newspapers, linear TV, radio, and other mediums. Secular tailwinds, such as the proliferation of cloud computing and digital advertising, underpin Alphabet's longer term growth runway as does its foray into the nascent self-driving taxi space.

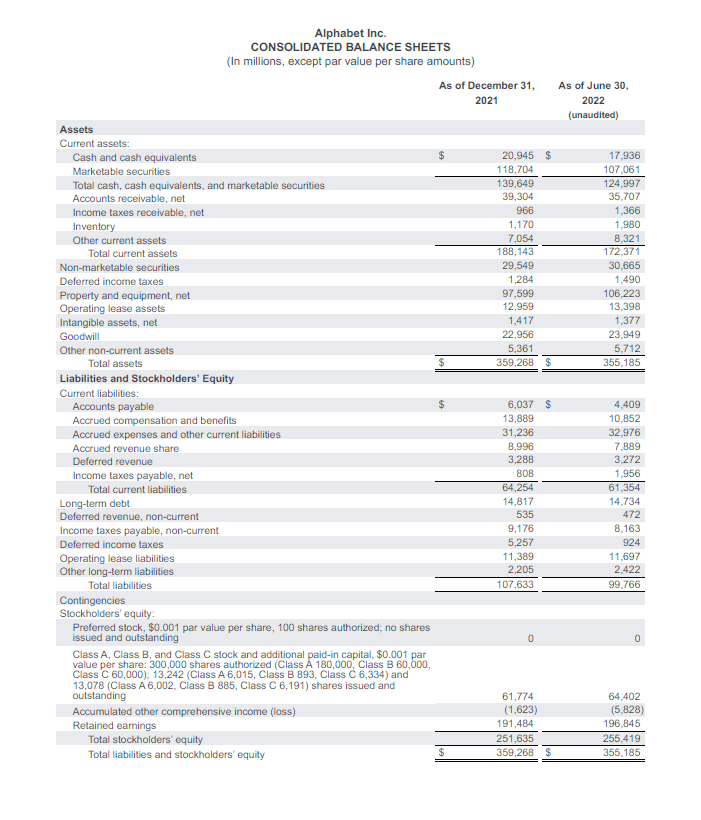

At the end of June 2022, Alphabet had $125.0 billion in cash, cash equivalents, and current marketable securities on hand along with $30.7 billion in non-current marketable securities (largely represented by strategic assets). Stacked up against $14.7 billion in long-term debt with no short-term debt on the books, Alphabet's enormous net cash position provides it with ample financial firepower.

Alphabet's fortress-like balance sheet is one of the reasons why we like the firm. (Alphabet - Second Quarter of 2022 Earnings Press Release)

{kind=link}

Please note that Alphabet is in the process of acquiring Mandiant Inc ( MNDT ) for $23.00 per share in cash through a deal with an enterprise value of ~$5.4 billion. The deal is expected to close by the end of 2022 and will hardly put a dent in Alphabet's fortress-like balance sheet. Mandiant is a cybersecurity firm that is expected to be integrated into Google Cloud and should support Alphabet's efforts to gain market share in the cloud computing and cybersecurity space. We like the deal.

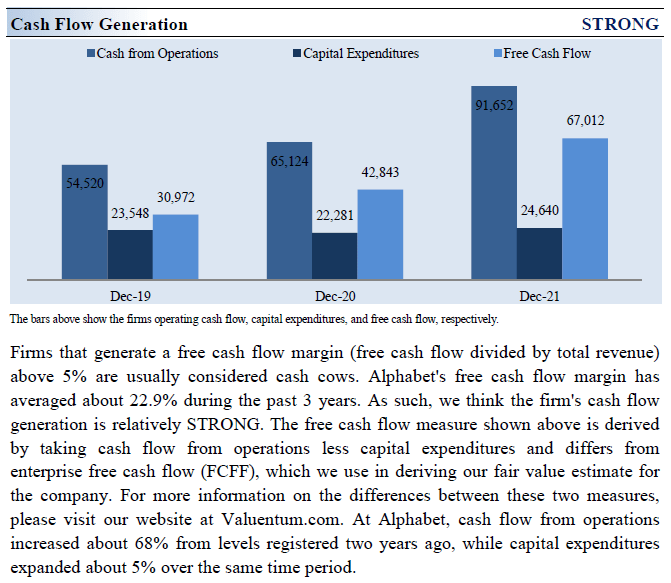

Alphabet generated a whopping $27.9 billion in free cash flow during the first half of this year while spending $28.5 billion buying back its stock via its share repurchase program. In our view, shares of Alphabet have been trading well below their intrinsic value for some time and continue to do so. For that reason, we are huge fans of its share buyback strategy.

Alphabet's free cash flow generating abilities are simply stunning. (Alphabet - Second Quarter of 2022 Earnings Press Release)

Looking ahead, we forecast that Alphabet will continue to take advantage of "panic selling" in US equity markets seen year-to-date to repurchase "gobs" of its stock, aided by its stellar free cash flow generating abilities and enormous net cash position.

Alphabet's Economic Profit Analysis

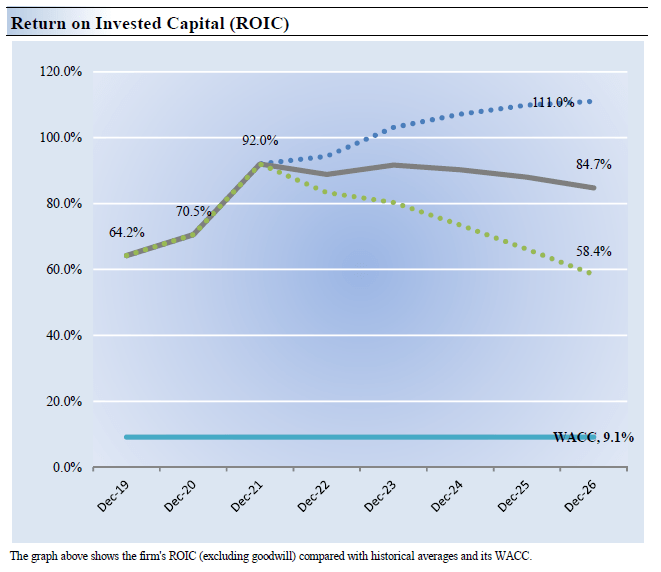

The best measure of a firm's ability to create value for shareholders is expressed by comparing its return on invested capital ['ROIC'] with its weighted average cost of capital ['WACC']. The gap or difference between ROIC and WACC is called the firm's economic profit spread. Alphabet's 3-year historical return on invested capital (without goodwill) is 75.6%, which is well above the estimate of its cost of capital of 9.1%.

In the chart down below, we show the probable path of ROIC in the years ahead based on the estimated volatility of key drivers behind the measure. The solid grey line reflects the most likely outcome, in our opinion, and represents the scenario that results in our fair value estimate. Alphabet is simply a tremendous generator of shareholder value and we forecast that will remain the case for some time.

{kind=link}

Alphabet's Cash Flow Valuation Analysis

{kind=link}

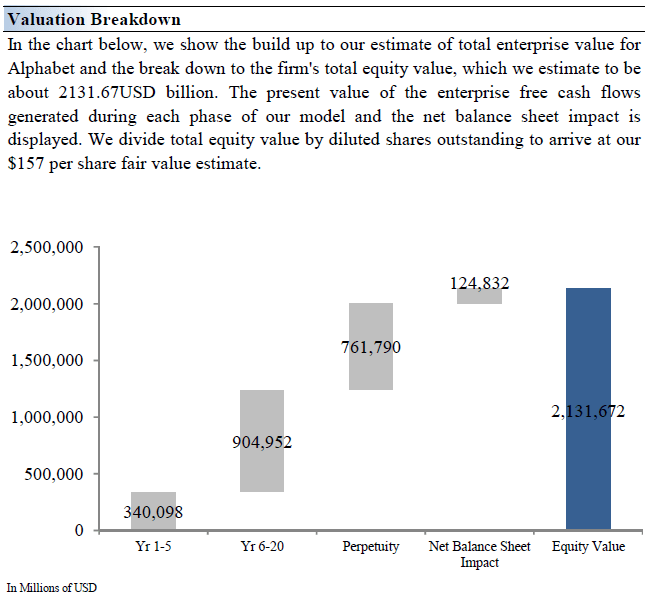

Our discounted cash flow process values each firm on the basis of the present value of all future free cash flows, net of its balance sheet considerations (in this instance, Alphabet's huge net cash position on the books positively enhances its fair value estimate). We think Alphabet is worth $157 per share with a fair value range of $126.00-$188.00.

The near-term operating forecasts used in our enterprise cash flow model covering Alphabet, including revenue and earnings, do not differ much from consensus estimates or management guidance. Our cash flow model reflects a compound annual revenue growth rate of 13.5% during the next five years, a pace that is lower than the firm's 3-year historical compound annual growth rate of 23.5%.

Additionally, our cash flow model reflects a 5-year projected average operating margin of 29.7%, which is above Alphabet's trailing 3-year average. Beyond Year 5, we assume free cash flow will grow at an annual rate of 6.2% for the next 15 years and 3% in perpetuity. For Alphabet, we use a 9.1% weighted average cost of capital to discount future free cash flows.

Image Source: Valuentum Image Source: Valuentum

{kind=link}

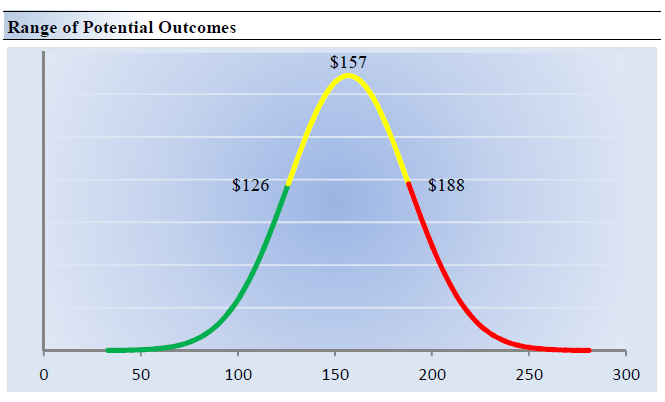

Alphabet's Margin of Safety Analysis

{kind=link}

Although we estimate Alphabet's fair value at about $157 per share, every company has a range of probable fair values that's created by the uncertainty of key valuation drivers (like future revenue or earnings, for example). After all, if the future were known with certainty, we wouldn't see much volatility in the markets as stocks would trade precisely at their known fair values.

In the graph up above, we show this probable range of fair values for Alphabet. We think the firm is attractive below $126 per share (the green line), but quite expensive above $188 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the firm, in our opinion. As of this writing, shares of GOOG are trading below the low end of this fair value estimate range, indicating Alphabet is quite undervalued currently.

Concluding Thoughts

There is not much that can get in the way of Alphabet's bright growth story, in our view, aided by its dominant market position and fortress-like financials. We are in awe of Alphabet's free cash flow generating abilities. Alphabet represents one of the best capital appreciation ideas out there, in our view.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

For further details see:

Google Is One Of The Best Capital Appreciation Ideas Out There