DTEGY - Google Should Benefit From More Telcos Moving To The Cloud

Summary

- By partnering with hyperscaler Google, telcos are benefiting from faster, cloud-based network delivery models while also benefiting from a reduction in capital expenditure.

- The Internet search company also displays an impressive number of partners for its Google Cloud Platform.

- Google Cloud's revenues have been going up while the segment operates at a loss.

- Despite its smaller size, I consider this segment as more promising going forward since it benefits from the secular trend of digital transformation.

There was a report by MTN Consulting that, by June 2022, capital expenditure by telecom operators (telcos) had risen sharply to $329.5 billion over the trailing 12 months as investments made in 5G and fiber accelerated and reached their highest in more than ten years.

This money is mainly benefiting 5G equipment suppliers in addition to tower companies as operators expand and upgrade their networks, and the objective of this thesis is to assess how telcos moving to the cloud benefits hyperscalers like Alphabet Inc. ( GOOG , GOOGL ) ("Google").

The company's share price has dipped by more than 30% since its November 2021 peak of around $150.

Now, Google's cloud segment generated less than one-sixth of its Search and advertising revenues in the second quarter of 2022 (Q2), but I consider it to be more stable in view of deteriorating economic conditions throughout the world and digital transformation becoming a secular trend. Also, telcos are expanding their partnerships with Google Cloud, and it becomes important to analyze its growth and profitability as well as the competition.

Moreover, with the big tech earnings season starting next week, this thesis will provide insights on what to specifically look for in relation to telcos.

Google Cloud

As part of the digital transformation trend, many enterprises have already migrated their IT workloads to the public clouds of the hyperscalers like Microsoft's (MSFT) Azure and Amazon's (AMZN) AWS. As for Google, revenues for its Cloud segment which includes GCP (Google Cloud Platform) were $6.3 billion for Q2, or up 36%. This growth, when viewed from the competition standpoint, was the fastest among the big public cloud providers, according to data by Canalys, right in front of Microsoft's Azure, followed by Amazon's AWS. However, the latter has the largest market share as it accounted for 31% of total cloud infrastructure spend in Q2, in front of Azure's 24%. Google was last with an 8% market share.

The deploy-as-you-need and pay-as-you-consume deployment and charging models championed by these hyperscalers bring more flexibility while being less Capex intensive compared to traditional methods of procuring IT infrastructure.

However, the CSPs (Communications Service Providers), be they fixed-line or mobile have been late to join the bandwagon, and instead, prefer to own their own on-premises corporate data centers. This has been changing since 2021 with partnerships announced for Verizon ( VZ ) working with AWS, and AT&T ( T ) entrusting its cloud to Azure, as I have covered in some of my previous theses. However, as pictured below, AT&T also has a partnership with Google for collaboration cloud while T-Mobile ( TMUS ) has opted for the Open Infrastructure Cloud, and Verizon in collaboration with Ericsson ( ERIC , ERIXF ) is involved in testing 5G Edge services with Google Distributed Cloud Edge .

Partnership with CSPs (www.google.com)

{kind=link}

Thinking aloud, these partnerships make you wonder why a CSP that has decades of experience managing IT workloads by itself and its enterprise customers would choose to pay hyperscalers for this purpose.

The Reasons why CSPs Partner with Google

The reason is that hyperscalers have "scale" and their networks span across several geographies already and they are able to provide resources more rapidly. One example is Vodafone's ( VOD ) Dynamo, for transporting huge volumes of data via Google Cloud to various access points located in different geographies. This enables more data-driven insights, enabling the U.K-based operator to garner a competitive advantage over industry peers.

Another reason for operators partnering with a hyperscaler is that 5G in contrast with network-centric 4G is more software-centric, signifying that applications purposely built for the cloud are faster compared to those which were developed for on-premises data centers.

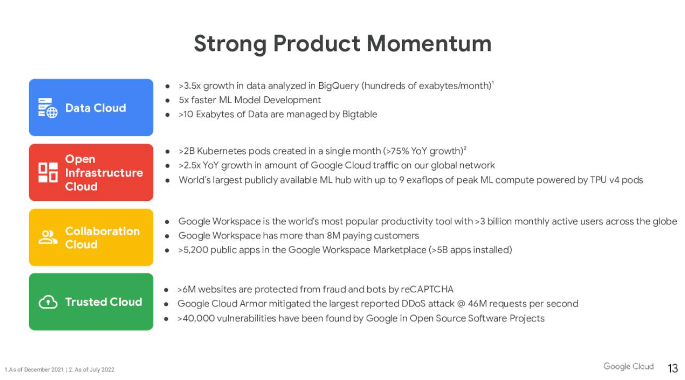

It is here that Google is advantaged compared to other hyperscalers due to its early foray into Kubernetes for building cloud-native apps while also being at the forefront of analytics. For this purpose, the company has one of the most advanced AI-powered computing centers in the world and its machine learning algorithms are 5 times faster than competitors.

Company presentation (www.seekingalpha.com)

{kind=link}

One example of AI is Deutsche Telekom ( DTEGY , DTEGF ) using it for detecting anomalies in its network, with a view to optimizing performance by rapidly analyzing complex errors through machine learning algorithms. These leverage the automated workflows of GCP's cloud-native solutions. Therefore, by using Google's cloud, these two telcos want to provide faster customer service, an area where telcos have traditionally been laggards, with Deutsche Telekom going to the extent of expanding its partnership to also focus on its core network. This represents a paradigm shift in telcos' strategy as they have kept their core or central networks within their own data centers and worked with hyperscalers more for edge (or outskirt) services.

Partnering with Google to Save on Costs

Consequently, looking ahead, Google is likely to benefit more from telcos moving their IT workloads to the cloud. In addition to the reasons I mentioned above, there is also the financial perspective. In this case, there has been an unprecedented demand for cloud-based apps which has propped up the traffic flowing on telcos networks, while not necessarily translating into higher revenues. This has been exacerbated by the higher expenses needed to fund 5G and fiber projects in turn resulting in higher Capex spent as a percentage of revenue generated as shown below. By comparison, Google itself spends less than half the capital expenses made by telcos to generate the same level of revenues.

Thus, when viewed from this angle, telcos do not have much option than to leverage hyperscalers' vast networks and, in this respect, Google Distributed Cloud Edge constitutes an alternative to telcos having to build individual private networks for their enterprise clients. As a fully managed service, it is easy to install and administer, and it brings telcos' services closer to where data is generated and consumed.

In order to have an idea of cost savings, I make a parallel with SD-WAN (Software Defined WAN) which is about applying a higher dose of software to the physical network. In this case, SD-WAN permits savings of 30% to 40% when compared to traditional ways of building networks, which is considerable.

This signifies that there are real opportunities for Google.

Valuing Telco Opportunities

To value these opportunities, I make use of MTN Consulting's calculation that the collective revenue benefits to hyperscalers' from the entire telco industry amounted to $3.4 billion from July 2021 to June 2022, or roughly 10% of their total capital spend. Moreover, this represents a rise of nearly 80% over the course of a year.

Assuming that Google just captures one-third of this $3.4 billion opportunity, and this grows by 80% on a yearly basis, this would constitute $2.04 billion (3.4/3 x 1.8) of opportunities from CSPs for fiscal 2023, which is in addition to other enterprise customers. This could increase the revenue forecast for 2023 to $324.8 billion compared to analysts' expectations of $322.76 billion . This constitutes a rise of 0.63%, which is not sufficient enough to skew the forward Price to Sales ratio of 4.07x enough to shift it from overvalued to the undervalued territory. This is the reason I have a hold position on Google.

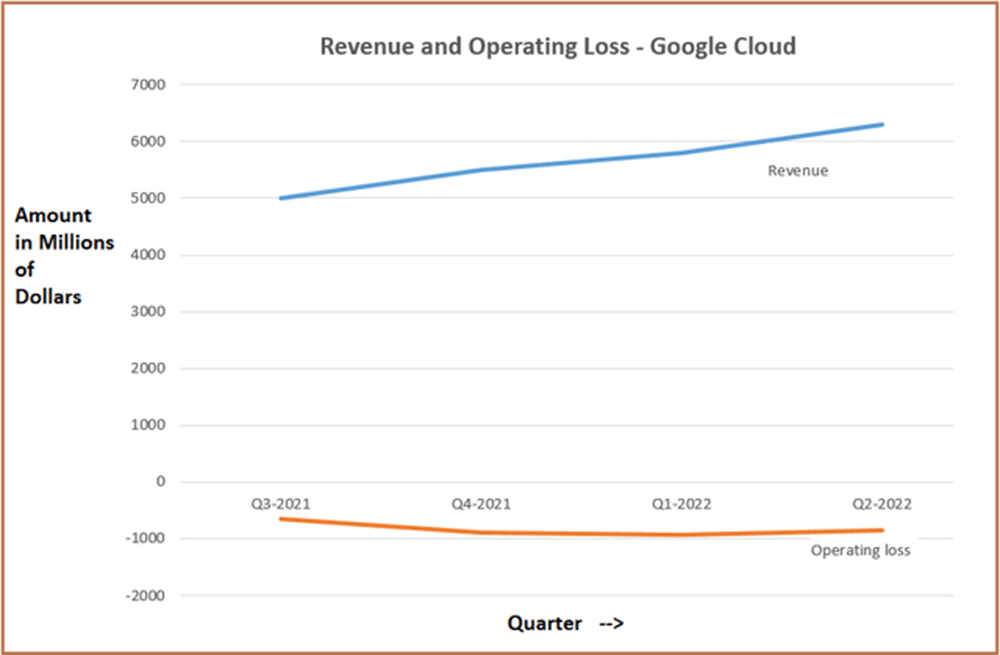

Now, the internet search company expanded its partnership with Deutsche Telekom only on July 12 , which means that any additional revenue pertaining to the deal should be accounted for Q3's financial results. Also, it is important to watch out for the rate at which revenue increases for the Google Cloud segment. For this purpose, revenues are already on an uptrend as shown in the blue chart below, after having surpassed the $6 billion mark and only further progression will show whether the company augments its market share.

{kind=link}

Moreover, as shown by the red chart above, the segment operates at a loss, and it is important to look for any sign of improvement. Now, Alphabet exhibits very high margins , and given the relatively small size of its cloud segment, it should not impact profitability, but, still, with the Federal Reserve hiking rates while shrinking its balance sheet, liquidity is being squeezed out of the system and hence, every source of operating loss starts to matter to value investors.

Concluding with the Telecom Industry Roadmap

Therefore, it is important for Google Cloud to generate revenues more rapidly than the 36% it achieved in Q2 on a year-on-year basis. The value achieved up to now does not deserve a buy, but more is to come, as the partnerships forged with Vodafone and Deutsche Telekom represent more of a roadmap for the entire telecommunications industry in its attempt to harness the power of the cloud to bring services nearer to the customer base equipped with a multitude of devices.

For CSPs, it is also about improving customer experience through cloud-based delivery models without having to develop costly new infrastructures, while also relying on Google's high level of cybersecurity threat protection achieved through acquisitions of high-profile IT security companies.

For further details see:

Google Should Benefit From More Telcos Moving To The Cloud