GRC - Gorman-Rupp: Good Execution Steep Price

2023-11-10 07:50:59 ET

Summary

- Gorman-Rupp completed the acquisition of Fill-Rite in 2022, fueling growth and revenue synergies.

- The company showed good growth in Q3 with strong margins as the Fill-Rite acquisition seems to have geared up operations.

- The stock currently seems moderately overpriced with my DCF model estimates but falls into a margin of safety.

The Gorman-Rupp Company (GRC) sells pump systems to multiple industries. The company has completed the acquisition of Fill-Rite in 2022, fueling the company for better margins and revenue growth through growth synergies. The company has executed well after the acquisition with good growth in Q3 along with strong margins. Still, the stock doesn't seem too good of an investment at the current price; Gorman-Rupp trades at a forward P/E of 19.2, which seems to price in a very good amount of growth from the company.

The Company & Stock

Founded in 1933, Gorman-Rupp sells pumps and pump systems. The company has multiple markets that it sells the offering to, with the largest segments being Industrials/Chemicals & HVAC Supply meant for waste streams and other applications in manufacturing, Fire Suppression for commercial structures and sprinkler systems, and Agriculture & Irrigation Supply where pumps are used for sprinklers, fuel transfer, animal waste, and other applications.

Gorman-Rupp's Markets (Gorman-Rupp November Investor Presentation)

In April of 2022, Gorman-Rupp announced that the company had entered an agreement to acquire Fill-Rite for a consideration of $525 million. The acquisition had estimated tax benefits of $80 million. As of Q1/2022, Fill-Rite had revenues of $140 million and an adjusted EBITDA of $34.5 million, making the acquisition's implied EV/EBITDA 12.9 when considering the tax benefits - when considering potential revenue synergies, the acquisition seems quite intriguing for Gorman-Rupp's shareholders. The transaction represents a large part of Gorman-Rupp's current operations, as the company has an enterprise value of around $1180 million. The acquisition was financed mostly with debt, which Gorman-Rupp has begun paying off.

Gorman-Rupp prides itself as a dividend-growing company - the company has had 51 consecutive years of dividend growth when excluding a special dividend in 2018, making the company a dividend king. Currently, Gorman-Rupp has a dividend yield of 2.39%. Besides the dividend, Gorman-Rupp's stock price hasn't yielded a very good result in the past ten years - the stock price has stayed nearly stable:

{kind=link}

Financials

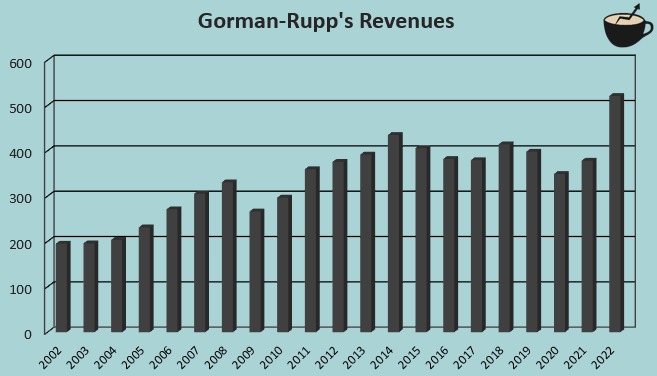

From 2002 to 2022, Gorman-Rupp has achieved a compounded annual growth rate of 5.0% in revenues. The revenue growth has been mostly stable, although from 2014 to 2020 the revenues have been somewhat turbulent:

{kind=link}

The achieved growth has mostly been organic, excluding the acquisition of Fill-Rite which has caused a massive jump in revenues in 2022 and 2023. Although Gorman-Rupp does have a strategy for acquiring businesses, other cash acquisitions have been quite insignificant in price. In Q3 , Gorman-Rupp had an organic growth of 8.9% , representing the revenue synergies and the company's overall growth capabilities.

Gorman-Rupp's margins have been mostly quite stable with an average EBIT margin of 10.1% from 2002 to 2022:

{kind=link}

After the acquisition of Fill-Rite, Gorman-Rupp's EBIT margin has increased as Fill-Rite had an impressive adjusted EBITDA margin of 24.6% when the acquisition was first announced. Currently, Gorman-Rupp's EBIT margin stands at 11.9%, well above the company's long-term average.

Valuation

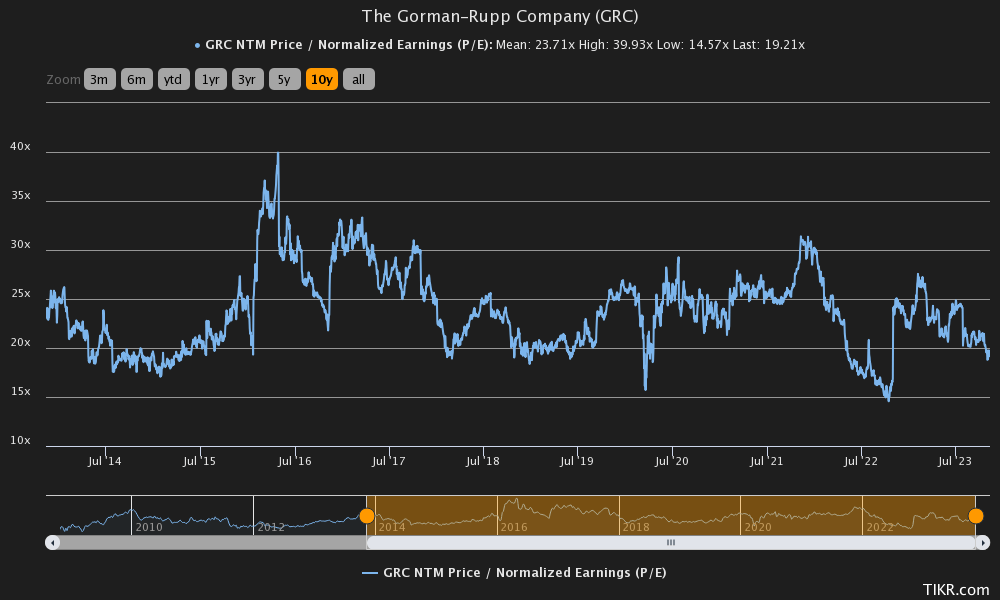

Currently, Gorman-Rupp trades at a forward P/E of 19.2, below the company's ten-year average of 23.7:

{kind=link}

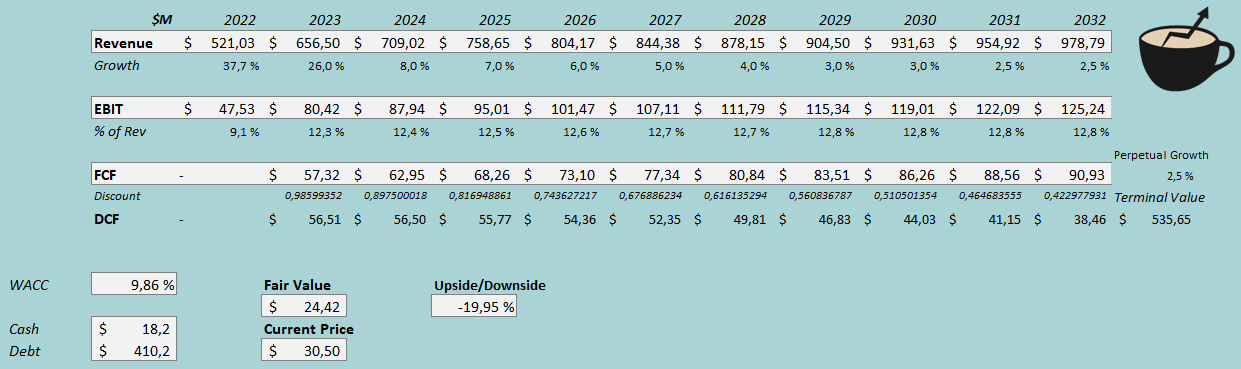

For a small-cap company, the P/E of 19.2 still seems quite high at first glance. To further demonstrate the steep valuation of Gorman-Rupp, I constructed a discounted cash flow model as usual. In the model, I estimate the company's growth to be quite good going forward - for 2023, I estimate a growth of 26%, estimating an organic growth of 7.9% in Q4. After the year, I estimate the growth to stay at a similar level with an estimated 8% growth for 2024. The growth slows down into an eventual perpetual growth rate of 2.5% from 2031 forward. Altogether, the estimated organic revenue growth represents a CAGR of 4.5% from 2023 to 2032.

I believe that Gorman-Rupp's current EBIT margin is mostly sustainable. I believe that the company can still achieve some synergies from the acquisition of Fill-Rite going forward; I estimate a margin of 12.3% for the current year, well above the 2022 figure of 9.1%. After the year, I still estimate some margin expansion with an eventual EBIT margin of 12.8%, half a percentage point above the 2023 estimate. The mentioned estimates along with a weighted average cost of capital of 9.86% craft the following DCF model with a fair value estimate of $24.42, representing a value that's 20% below the stock price at the time of writing:

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Gorman-Rupp had $10.5 million in interest expenses. With the company's current amount of interest-bearing debt , the company's annualized interest rate comes up to a figure of 10.22%. The interest rate seems very high for a company such as Gorman-Rupp. As the debt was drawn to finance the acquisition of Fill-Rite, I believe that a good portion of the debt will be paid off within a reasonable period of time. The company has already started to lower its debt. For the company's long-term debt-to-equity ratio, I believe that an estimate of 5% is reasonable as Gorman-Rupp hasn't historically leveraged debt very much.

On the cost of equity side, I use the United States' 10-year bond yield of 4.55% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Gorman-Rupp's beta at a figure of 0.85 . Finally, I add a small liquidity premium of 0.4% into the cost of equity, crafting the figure at 9.97% and the WACC at 9.86%.

Takeaway

Unfortunately, the dividend king of Gorman-Rupp doesn't seem too good of an investment at the current price if my financial assumptions actualize. The company has had a good and long history of growing dividends and earnings modestly, and I estimate the company to have remaining growth and margin synergies from the Fill-Rite acquisitions, but the price seems to be more than the price in these factors. My DCF model estimates a downside of 20% for the stock. Still, I believe that the downside falls into a margin of safety when estimating the valuation; the valuation is a combination of numerous factors, and further acquisitions or better-than-expected growth could make the stock a worthy investment. As it stands, I have a hold rating for the stock.

For further details see:

Gorman-Rupp: Good Execution, Steep Price