ARE - Government Finances Are A Mess: Focus On Quality

2023-08-02 18:00:55 ET

Summary

- Fitch Ratings downgraded the US Federal Government from AAA to AA+, causing the stock market to roil.

- Real estate investment trusts (REITs) have fared better than tech stocks in the day after the downgrade announcement, as REITs were already relatively cheap.

- While the downgrade itself is virtually meaningless, it does spur us to look at the US Government's finances.

- Uncle Sam's fiscal situation is not in great shape, with deficit spending and increasing debt, combined with falling population growth, leading to what I call a "Monetary Death Spiral."

- Amid fiscal and macroeconomic uncertainty, I make the case that quality assets and quality companies will always be valuable, so investors should focus on those.

On Tuesday, August 1, Fitch Ratings downgraded the US Federal Government from AAA to AA+. That has triggered a roiling in the markets, sending all the major indexes lower.

Interestingly, despite being generally more interest rate-sensitive than the average stock, real estate investment trusts ("REITs") as represented by the Vanguard Real Estate ETF ( VNQ ) fared better than the S&P 500 ( SPY ) or the Nasdaq's ( QQQ ) tech stocks, at least so far.

This perhaps should not be surprising since REITs have underperformed since the beginning of 2022, making them relatively cheap already.

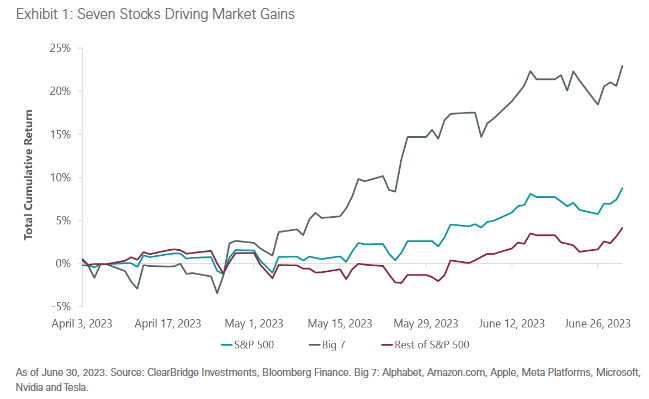

On the other end of the valuation spectrum, tech stocks have been dominant this year as they ride the wave of A.I. enthusiasm and drive most of the major indices' YTD gains.

During the second quarter, for example, seven of the top tech stocks surged over 20%, while the S&P 500 overall saw more modest, high-single-digit gains, and the index excluding those seven tech stocks saw low- to mid-single-digit gains.

{kind=link}

Astonishingly, the weight of just the top five constituents in the S&P 500 accounts for about 23% of the index's total market cap.

The question of whether mega-cap tech stocks are in a bubble is far beyond my paygrade, but it seems safe to say that many richly valued tech stocks had more air to be released than the rate-sensitive REITs that have already taken a beating over the last year and a half.

But what about that rating downgrade? Does it signify a meaningful turning point in the degradation of the US federal government's finances?

No, not at all.

That isn't to say that Uncle Sam's finances are in great shape. The opposite is true. Since the early 2000s, federal deficits as a percentage of GDP have trended lower, albeit with ups and downs.

Growth in government debt accelerated after the Great Recession of 2008-2009 and then accelerated again during COVID-19.

Of course, Modern Monetary Theorists would assert that these deficits are an unalloyed economic benefit, because it signifies that those in charge of the money printer are pushing dollars into the private economy, boosting revenue and assets. When inflation arises, the Modern Monetary Tinkerers would simply ask Congress to temporarily raise taxes to sap the excess aggregate demand until the inflation problem is resolved.

Easy peasy.

Unless, of course, you consider the difficulty of getting a deeply divided Congress to come together in a timely manner to raise taxes equitably enough that even low-income folks (whose propensity to spend is much higher) feel the pinch.

Traditional Keynesians would say government deficit spending has been necessary to offset a weak economy. Also, some of this deficit spending is for the purpose of investment into the country's future in the form of subsidies for semiconductor factories or green energy.

The problem with this thinking is that the vast majority of government spending is not investments into our future. Already, slightly over half of federal spending goes to mandatory programs like Social Security, Medicare, Medicaid, veterans benefits, student loans, etc.

Over the next five years, outlays for the two largest mandatory programs, Social Security and Medicare, are projected to grow roughly three times faster than overall government spending or discretionary spending (which includes all of what might be considered "investments in the future").

And this doesn't even show the explosion in the government's interest expenses!

This, combined with continuously low population growth and aging demographics, convinces me that the "Monetary Death Spiral" remains a reality.

I originally outlined this process in a 2019 article (see HERE ) and updated it in a June 2020 article titled " The Monetary Death Spiral Is Accelerating ."

Contrary to what either the MMTers or Keynesians assert, the core thesis of the Monetary Death Spiral (and observation of history) is that high government debt and deficit spending is actually a deflationary force. It crowds out productive investment by soaking up the economy's limited physical and human capital in mostly unproductive activity.

Money may be unlimited, but real resources are limited. Shifting resources from mostly productive uses to mostly unproductive uses ultimately causes aggregate demand to be lower than it otherwise would be.

So, if the Monetary Death Spiral remains in place, how did we get all that inflation?

As I stated in my 2020 article:

The only way inflation will return in force is if/when deflation becomes sufficiently severe and economically disruptive that governments print money and distribute it directly to consumers.

While perhaps not exactly when or how I envisioned it, I'd say this is exactly what happened in 2020 and 2021.

The price of oil went negative. Prices of airline tickets plummeted. You could buy out an entire movie theater for you and your friends to have a private viewing for $99.

What did the government do in response? They printed money and distributed it directly to consumers. This caused a surge in demand at exactly the time when production and importation of goods was down and workers were sitting out of the labor market.

The result? Price hikes, i.e. inflation.

As I said in that 2020 article:

This, and only this, will cause a new uptrend in inflation. It will create a strong, new source of demand for consumer goods and services that will overwhelm supply, leading to price hikes. At first, it will seem harmless, but this will only encourage fiscal policymakers to spend more printed dollars on their programs.

My reasoning turned out to be correct.

It isn't government debt, deficit spending, or easy monetary policy that cause inflation. In fact, those tend to correlate with, if not cause, deflationary pressures. Rather, fiscal excess, especially sending printed money directly to consumers, is what triggers inflation.

If the Fed cut rates by 200 or 300 basis points tomorrow, it wouldn't lead to a resurgence in inflation as many pundits assert. Just the opposite. It would make it easier for producers to obtain financing to expand production capacity and for real estate developers to start new projects. It would cause mortgage rates to come down and unleash pent-up demand for homes, yes, but it would also free many homeowners who feel trapped by low existing mortgage rates to list their homes for sale.

So, back to government debt.

Should we worry about the US Government credit rating downgrade?

No, not really. The US dollar is and will remain the world's primary reserve currency, and Uncle Sam's money printer ensures that Treasury bondholders will be repaid in full no matter what.

Should we worry about Congressional brinksmanship during the next debt ceiling debate? Yeah, probably. But that's nothing new.

Where To Invest? Quality Will Always Be Valuable

I think the best thing to do in the face of government fiscal messiness or macroeconomic uncertainty is to focus on quality assets .

Even in the most extreme fiscal or monetary scenario, quality assets will still be valuable. A prime piece of real estate with a highly functional building on it will always be desirable. An automated factory with high-tech machinery producing necessity goods will always be economically useful. A brand with enduring consumer trust and popularity will still have value even after the fiscal apocalypse.

I've hinted at it here, but how exactly does one define "quality"? I've given that question a lot of thought this year as my own investment philosophy has honed in on quality assets.

Here are the eight most important characteristics of a high-quality company (in my humble opinion):

- Provides essential goods and/or services to its customers

- Tangible and/or intangible competitive advantages

- Pricing power and unit volume growth (or for REITs: rent growth and portfolio expansion)

- Strong market positioning in a secular growth trend

- High returns on invested capital (well in excess of cost of capital)

- A strong balance sheet that remains resilient across the full economic cycle

- A skilled and shareholder-aligned management with a solid track record

- A safe and growing dividend

I know that last point cuts out a lot of great companies like Amazon ( AMZN ) and Google ( GOOG ). I don't necessarily think high-quality companies have to have all eight of these characteristics, but the more, the merrier.

I seek to invest in:

- high-quality companies with

- a dividend that grows over time

- at a discount to fair value (and thus an attractive dividend yield )

- and wait patiently as they compound over time .

To modify Warren Buffett's phrase, my desire is to own "wonderful dividend growth companies purchased at fair prices rather than fair dividend growth companies purchased at wonderful prices."

My favorite way to accomplish my investment strategy in one click is the Schwab US Dividend Equity ETF ( SCHD ), which specifically has quality filters built into its stock-picking methodology. It seeks out companies that not only pay dividends (and have grown them for the last five years) but also have high returns on equity and relatively low leverage.

Over the last five years, SCHD's total returns have matched those of the S&P 500 almost perfectly, while notably outperforming in 2022 until mid-Spring of 2023.

But there are a number of high-quality companies outside of SCHD's investable universe, most notably in the realm of REITs.

Here are some of my favorites to buy right now:

- Alexandria Real Estate Equities ( ARE ) : I gave my pitch for ARE as a "must-own" REIT in this article as well as a rebuttal to Jonathan Litt's short report in an exclusive article for subscribers. The balance sheet, rated BBB+, is in great shape with an average debt maturity of 13+ years, and ARE's top-tier locations and state-of-the-art building designs are more of a competitive advantage than the market gives it credit for.

- Rexford Industrial Realty ( REXR ) : REXR enjoys a commanding market position in infill industrial real estate in the extremely supply-constrained Southern California market. Rents are surging. The balance sheet is ultra-strong. Investment spreads are better today than the last few years.

- Enbridge ( ENB ) : This Canadian midstream energy giant's balance sheet is not as strong as some blue-chip peers like Enterprise Products Partners ( EPD ) or Williams Companies ( WMB ), but ENB's cost of capital is good, and its diversified portfolio should continue to perform well. I like the natural gas export assets and the exposure to renewable energy.

- Mid-America Apartment Communities ( MAA ) : My favorite apartment REIT by far. Q2 results show that MAA should do fine amid elevated supply deliveries and thrive in the long run. The strong & underleveraged balance sheet gives capacity for significant portfolio expansion when opportunities arise.

- Brookfield Renewable Partners ( BEP ) : Bluest blue-chip among renewable power producers, largely because half its portfolio is in hydropower. It has a massive development pipeline and is the go-to partner for corporations to meet their decarbonization goals. (Note: BEP generates a K-1 form, but its corporate equivalent, Brookfield Renewable ( BEPC ), does not.)

- Agree Realty Corp ( ADC ) : Recession-resistant tenant base. Strong balance sheet. Best-in-class cost of capital. Skilled and shareholder-aligned management. See more in this article .

- VICI Properties ( VICI ) : Never bet against Vegas. People, especially Millennials, want experiences. They want to travel. VICI owns the real estate where people vacation. See more of my thoughts on VICI here .

- W.P. Carey ( WPC ) : Pure-play net lease REIT focused on sale-leasebacks for Class A industrial buildings in the US and big box retail in Europe. The BBB+ credit rating should help WPC attain relatively favorable rates when refinancing upcoming debt maturities. See more here .

All of these companies meet my 8-point definition of quality in spades. It's the best time to accumulate shares in them in years.

The bottom line is this: Government finances may be in shambles, or maybe things will turn out fine. In any case, quality companies and quality assets will always be valuable. So, focus on quality.

For further details see:

Government Finances Are A Mess: Focus On Quality