LPI - Grab 10% Yield With Laredo Petroleum Bonds

Summary

- Laredo Petroleum has benefited from the increase in energy prices.

- The company has generated excess cash which has allowed it to invest in capital assets and reduce debt.

- If the company maintains its conservative capital management approach, bondholders should see a return of their capital plus the interest income.

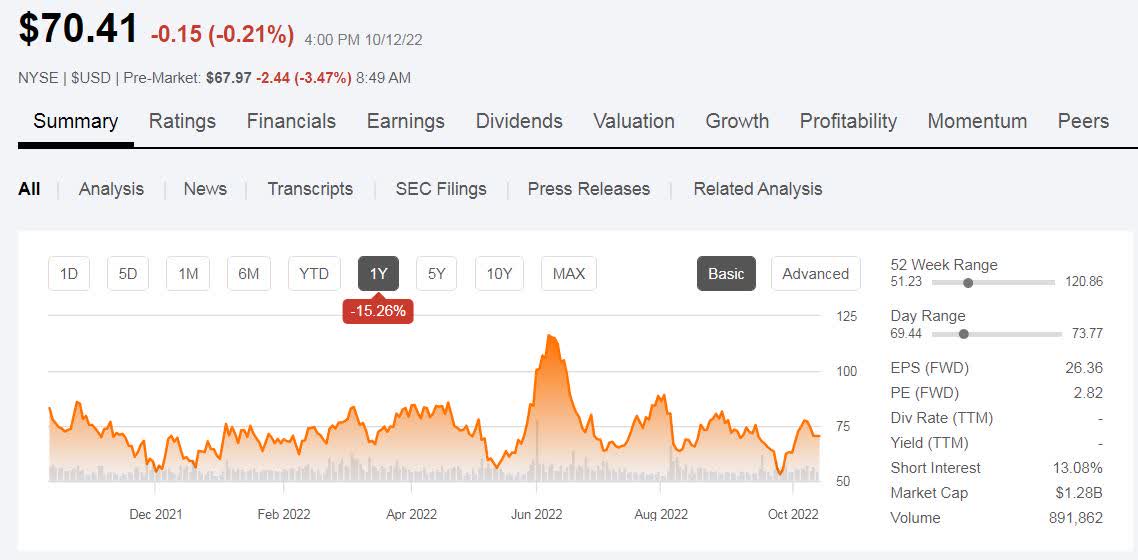

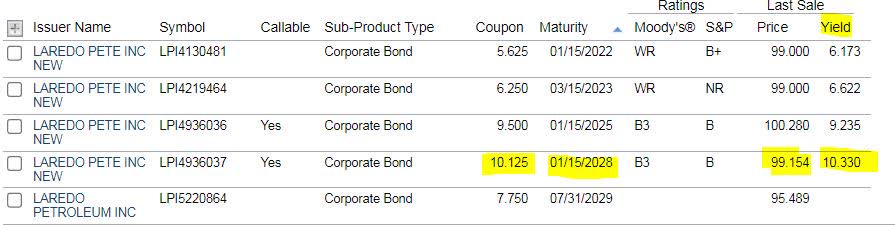

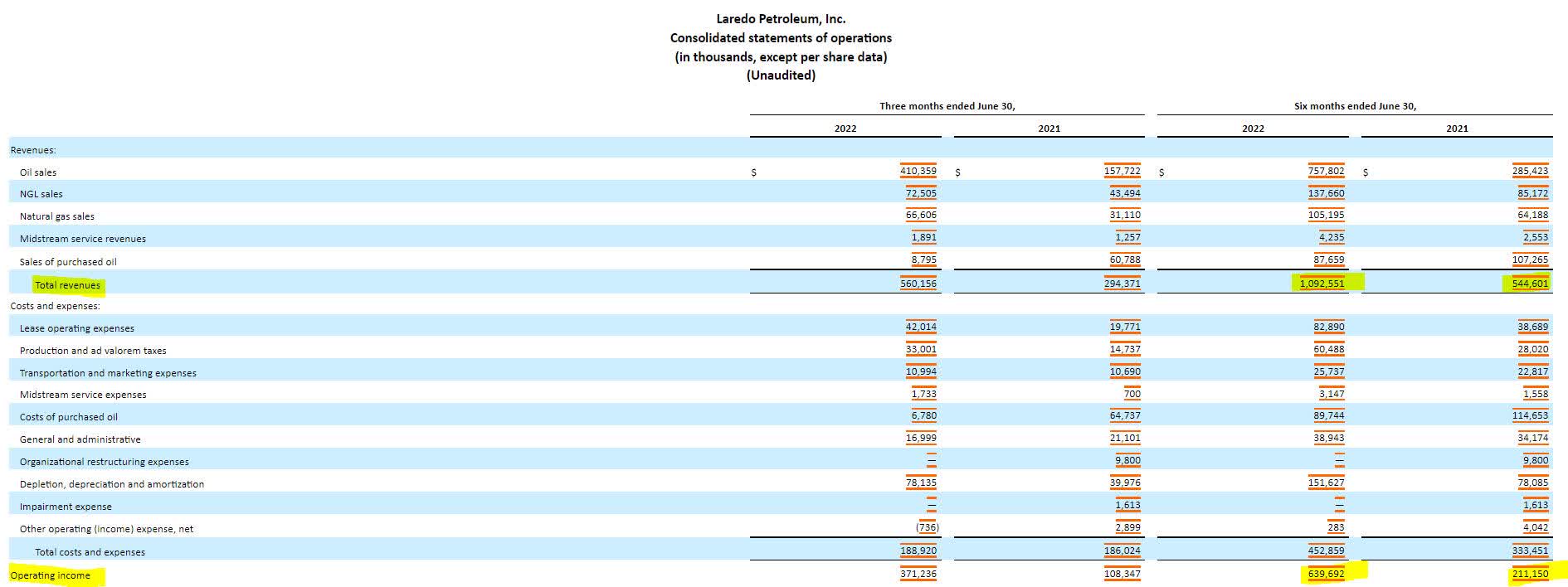

Despite the big jump in oil prices this year, Laredo Petroleum (LPI) shareholders have not seen a growth in their investment. While share prices have seesawed through the year, investors have lost 15% in the past year. Meanwhile, the company's high-yield debt has declined to slightly below par, which for its 2028 bonds, is creating coupon yields and a yield to maturity of greater than 10%.

{kind=link}

{kind=link}

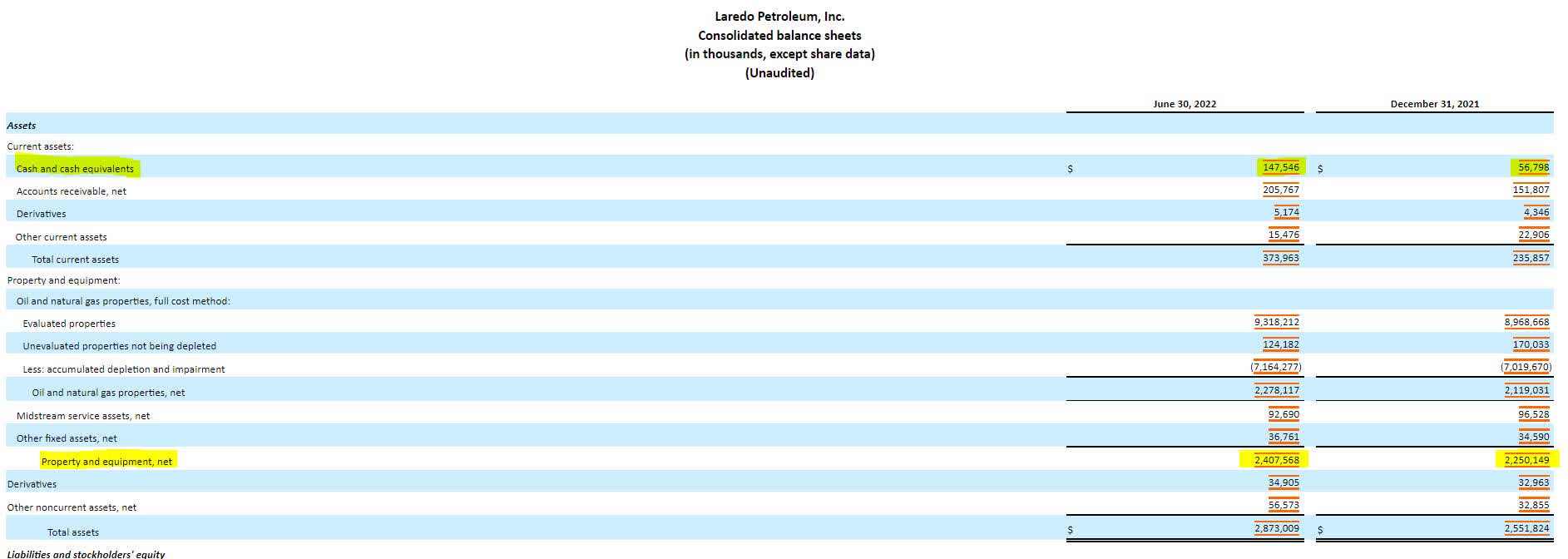

An examination of Laredo's balance sheet reveals several impressive changes during the first six months of 2022. First, the company has managed to simultaneously build its cash balance while investing in its capital assets (property, plant, and equipment). In the first six months of 2022, Laredo managed to spend $150 million more on assets than what was depreciated. These investments should help the company increase production and subsequently revenue.

{kind=link}

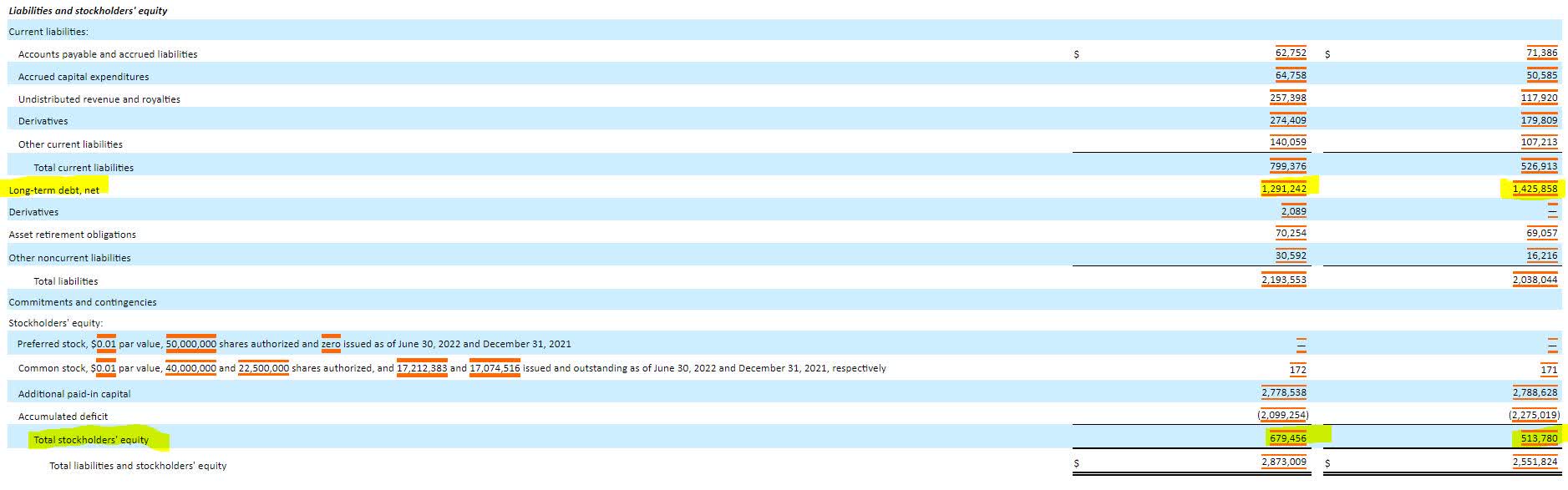

What may be more impressive is that Laredo has generated excess cash and invested in its assets while paying down long-term debt by more than $125 million, resulting in equity growth of more than $160 million. While other companies may use the increased business to take risky investments and leverage themselves further, Laredo wisely managed its resources to strengthen its balance sheet.

{kind=link}

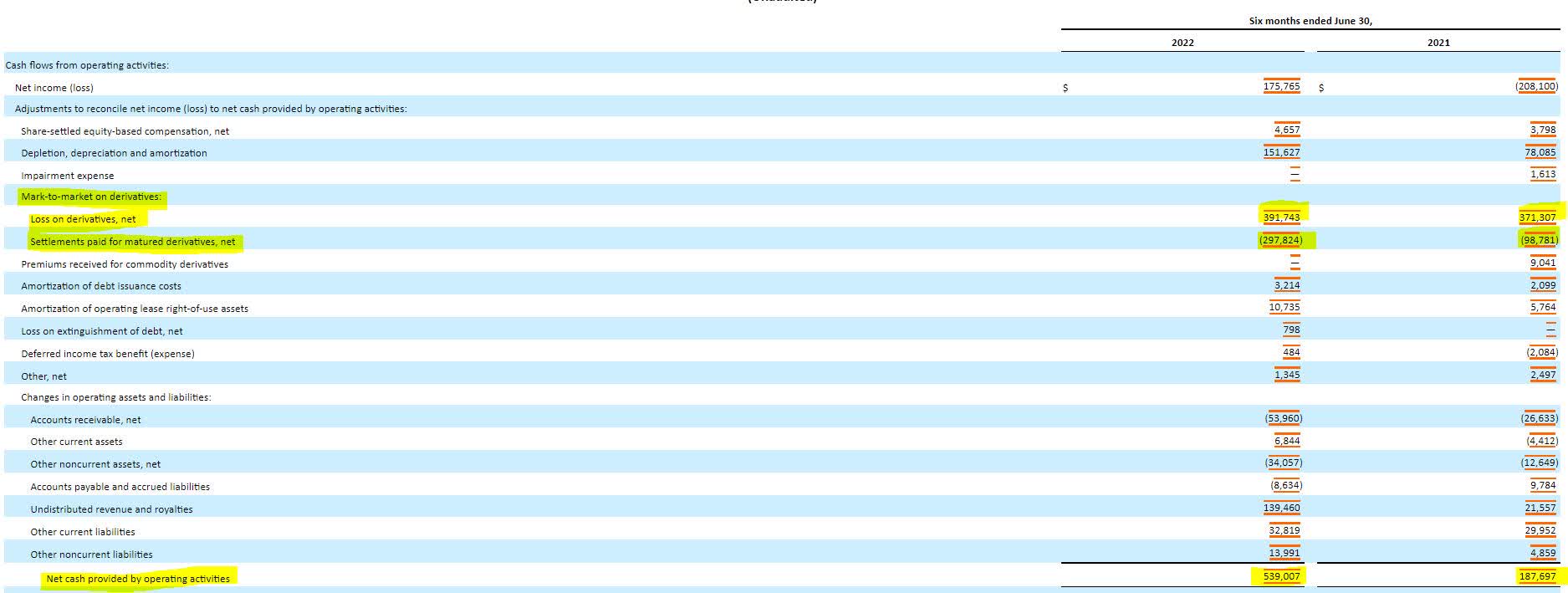

From a profitability standpoint, Laredo seized the opportunity afforded by higher commodity prices and in its investments in assets to double its revenue and triple its operating income. These improvements translated to an explosion of operating cash flow by $350 million in the first six months of 2022 vs the same time period of 2021. It's important to recognize that derivative activity helped buoy the company's cash flow in 2021 but did not adversely impact Laredo's cash flow in 2022.

{kind=link}

{kind=link}

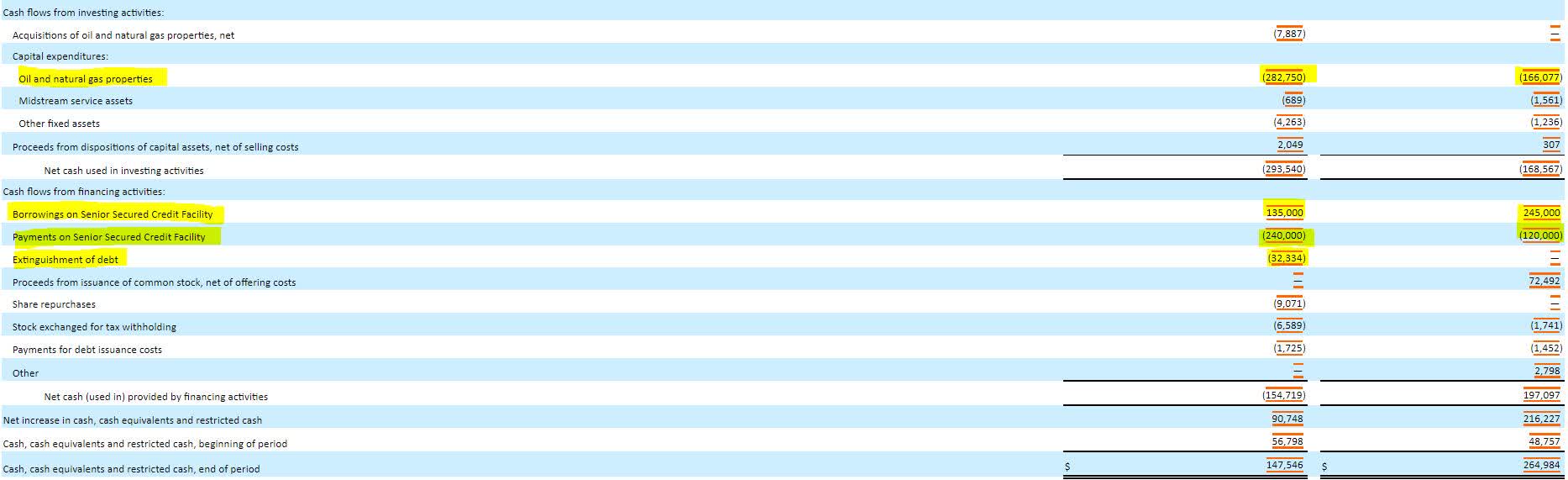

Laredo was able to use its excess operating cash flow to increase its capital expenditures (hence the increase in net property, plant, and equipment) and still generate positive free cash flow of $250 million in the first six months of 2022. The increased free cash flow allowed Laredo to pay off its senior secured credit facility (a $105 million reduction in debt) and to pay off an additional $32 million in debt. Bondholders can be assured of their investment if the company continues to generate robust cash flow.

{kind=link}

In addition to Laredo's paying off its senior secured credit facility, the company is not facing a new debt maturity until January 2025 when nearly half of its $1.3 billion debt load comes due. Even if the credit markets are inaccessible to Laredo, the company's senior secured facility can be drawn up to $2 billion, proving the company with enough liquidity to cover its long-term debt obligations.

{kind=link}

{kind=link}

While one obvious risk to the company is energy prices, another is M&A. Should Laredo undertake a risky merger or acquisition involving further leverage, it could compromise the ability of the company to service its debt. The energy sector is littered with recent bankruptcies on the back end of a merger. Such an action by Laredo would have me seriously reconsidering my investment.

Due to Laredo already paying back some of its debt this year, investors should not expect significant price declines in its bonds as the company is expected to continue paying back debt.

CUSIP: 516806AG1

Price: $98.72

Coupon: 10.125%

Yield to Maturity: 10.44%

Maturity Date: 1/15/2028

Credit Rating (Moody's/S&P): B3/B

You can get an updated price of this bond by checking out its page on FINRA .

For further details see:

Grab 10% Yield With Laredo Petroleum Bonds