MLI - Graco: A Concentrated Business That's Trading Just A Bit Too High

Summary

- Graco has had a nice spurt of growth in the past couple of years, with sales, profits, and cash flows climbing higher.

- The firm's balance sheet also looks solid and its long-term picture is promising.

- But shares are a bit too lofty to warrant a significant amount of enthusiasm.

There's very little that I love more than finding a company that has a very specific niche that it operates in and performs well in. You can imagine my delight, then, when I came across a firm called Graco ( GGG ). The management team at the company describes the firm as a multinational manufacturing business that provides technology and expertise regarding the management of fluids and coatings in industrial and commercial applications. A couple of years ago, the business started seeing some attractive growth on both its top and bottom lines. This, combined with the firm's cash position which is in excess of debt in the amount of $243.2 million, makes it a stable and attractive firm from an operational perspective. Unfortunately, this doesn't necessarily mean that it makes for a great investment prospect. Given how shares are priced at the moment, I do not believe that the company is any better off than being fairly valued. Because of this, I've decided to rate the firm a ‘hold’ at this time, a rating that reflects my view that shares should generate upside or downside that is more or less in line with the broader market moving forward.

A niche business

Truth be told, the initial description I gave regarding Graco is incredibly broad and vague. To really understand the company, we need to dig into precisely what it does in order to create value for its customers and its investors. The management team at the company says that the business designs, produces, and markets systems and equipment that are used to move, measure, mix, control, dispense, and spray fluid and powder materials. Although this may seem like a rather small and isolated space, the company's equipment is actually used in a variety of industries such as construction, processing, manufacturing, and more.

In particular, the business specializes in providing equipment solutions for difficult-to-handle materials. These are materials that have high levels of viscosity, that are abrasive or corrosive, or that have multiple component materials that require specific ratio control. We can dig in even deeper from here by looking at each of the firm's operating segments. The first of these is the Contractor segment. Through this, the business offers sprayers that apply paint to walls and other structures. This includes sprayers that are dedicated to do-it-yourself homeowners, all the way up to professional contractors. In addition to paint, some of its sprayers can apply texture to walls and ceilings, highly viscous coatings to roofs, markings on roads, parking lots, athletic fields, and even floors, and more. Other products under this segment include equipment that focus on proportioning materials. This can come in handy for spraying foam that's used for insulating building walls, roofs, refrigerators, and more. During the firm's 2022 fiscal year, this was the largest segment, accounting for 47% of its revenue.

The next segment is the Industrial segment. This is actually divided up into two different divisions. The first of these is the Industrial division, which produces liquid finishing and advanced fluid dispense equipment that's largely used for industrial applications. Examples can include equipment that's used to apply liquids on metals, wood, plastics, and more. It also sells applicators that use different methods of atomizing and spraying liquid materials, paint, or other coatings, depending on the viscosity of the fluid in question. The other division is the Powder division, which makes powder-finishing products and complete powder-finishing systems that coat powder on metals. These are largely used to coat window frames, metallic furniture, sheet metal, and more. During the firm's 2022 fiscal year, this segment accounted for 30% of the company's revenue.

And finally, we have the Process segment. Just like the Industrial segment, Process has two different divisions. The first of these is the Process division, which produces pumps and other technologies that help to move chemicals, water, wastewater, petroleum, food, and more. These products are offered in the food and beverage, dairy, pharmaceutical, cosmetic, and a variety of other industries. And finally, we have the Lubrication division, which mostly focuses on the production and sale of equipment for use in equipment maintenance and vehicle servicing. The firm's line of products includes pumps, hose reels, meters, valves, and more. During the company's 2022 fiscal year, this segment accounted for the remaining 23% of the company's revenue.

{kind=link}

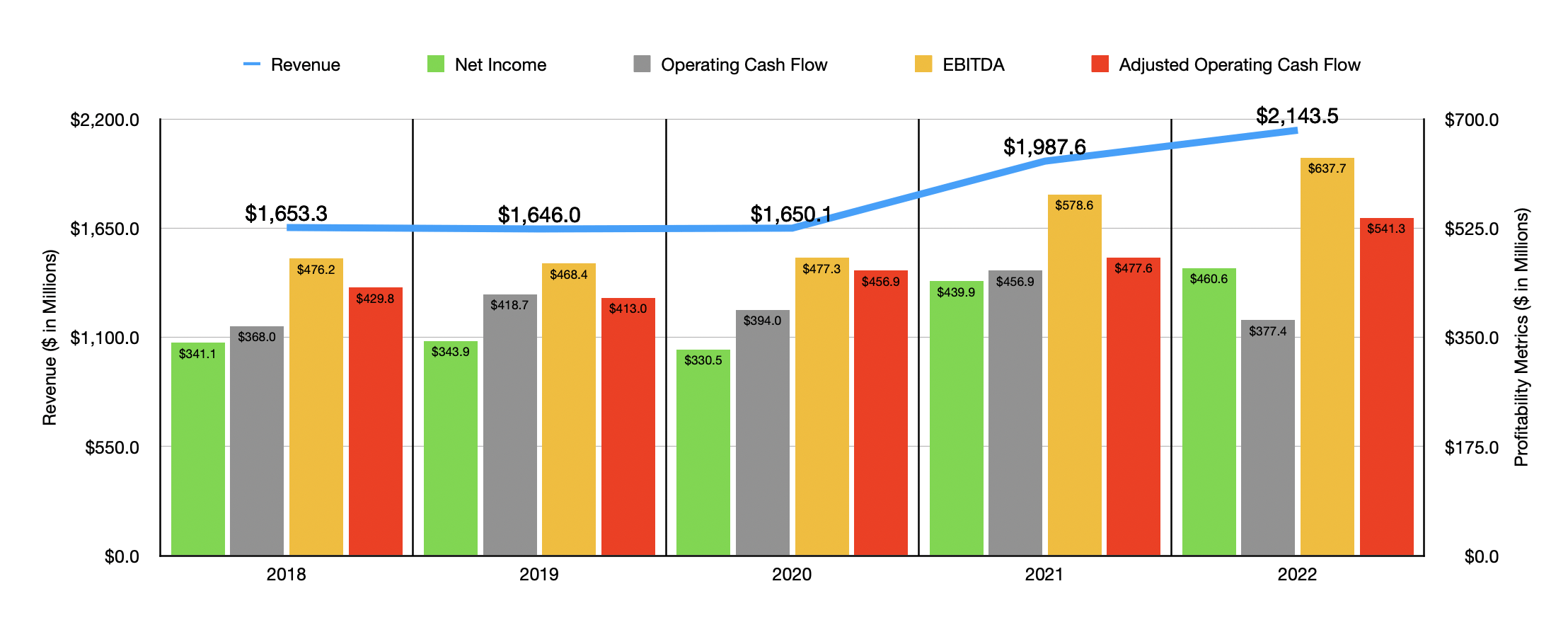

Prior to the 2021 fiscal year, the financial picture of the business looked rather mediocre. Revenue was stuck at around $1.65 billion, give or take around $6 million in any given year. But then, in 2021, sales spiked to $1.99 billion before climbing further to $2.14 billion in 2022. The 7.8% sales increase from 2021 to 2022 is rather interesting because sales would have been higher had it not been for a 4% impact associated with foreign currency fluctuations. The business also had one extra operating week in 2021 than it did in 2022. In the Americas region in which the business operates, volume and pricing changes impacted sales positively to the tune of 11% without factoring in the foreign currency component. Acquisitions added another 1% to sales. In the EMEA (Europe, Middle East, and Africa) regions, volume and pricing changes added 7% to the company's line, while in the Asia-Pacific region, the company benefited to the tune of 16% from increased volume and higher pricing.

The bottom line for the company has looked very similar to the top line in recent years. Net income remained in a fairly narrow range between 2018 and 2020, with a low point of $330.5 million and a high point of $343.9 million. In 2021, profits shot up to $439.9 million before climbing further to $460.6 million in 2022. Other profitability metrics followed a slightly different trajectory. Operating cash flow ranged between $368 million and $418.7 million in the three-year window ending in 2020. By 2022, the metric was still in this range at $377.4 million. But this was after falling from $456.9 million in 2021. If we adjust for changes in working capital, however, we would have seen a constant year-over-year improvement from 2019 through 2022, with the metric ultimately climbing from $413 million to $541.3 million. The EBITDA for the company remained in a narrow range in the three years ending in 2020 as well. But by 2022, it had risen to $637.7 million compared to a five-year low of $468.4 million.

{kind=link}

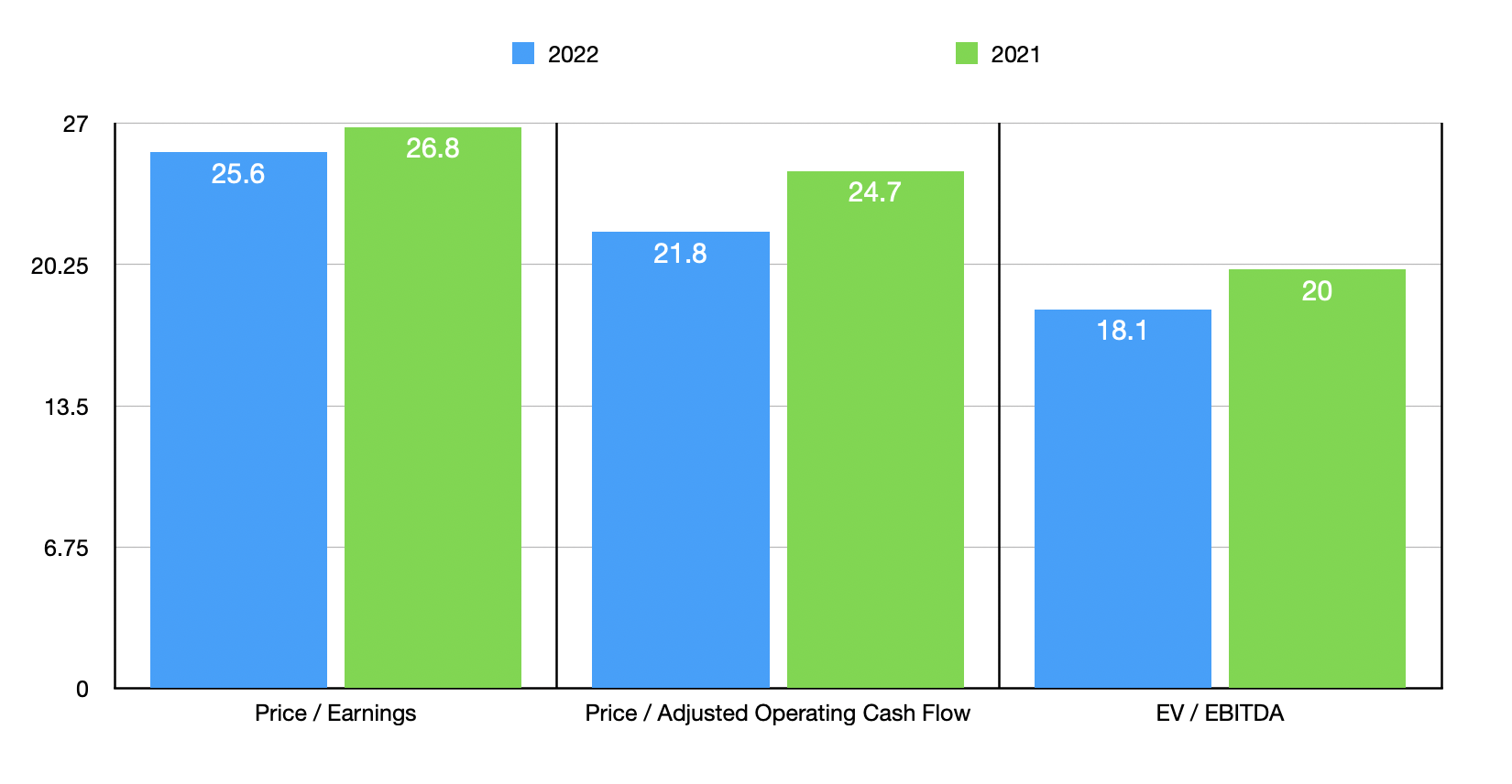

Management has not provided any guidance for the 2023 fiscal year. But using the data from 2022, we can easily value the firm. On a price-to-earnings basis, the company is trading at a multiple of 25.6. This is down slightly from the 26.8 reading that we get using data from 2021. Year over year, the price to adjusted operating cash flow multiple fell from 24.7 to 21.8, while the EBITDA multiple dropped from 20 to 18.1. In addition to being expensive on an absolute basis, the stock is also pricey relative to similar firms. Five companies that I looked at that could be considered comparables to Graco had price-to-earnings multiples ranging between 6.3 and 25. Our prospect was the most expensive of the group. Using the price to operating cash flow approach, the range was between 5.7 and 35.6. Two of the five companies were cheaper than our target in this respect. And finally, using the EV to EBITDA approach, we get a range of between 3.8 and 21.7. Four of the five companies looked at were cheaper than Graco.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Graco |

| 25.6 |

| 21.8 |

| 18.1 |

| Nordson Corp ( NDSN ) |

| 25.0 |

| 25.0 |

| 17.2 |

| Stanley Black & Decker ( SWK ) |

| 12.5 |

| 35.6 |

| 21.7 |

| Snap-on Inc. ( SNA ) |

| 14.7 |

| 19.8 |

| 10.0 |

| Lincoln Electric Holdings ( LECO ) |

| 22.3 |

| 25.7 |

| 16.1 |

| Mueller Industries ( MLI ) |

| 6.3 |

| 5.7 |

| 3.8 |

Takeaway

Operationally, Graco is a fascinating company to me and its recent financial performance is encouraging. The stability of the company over the years suggests to me that the long-term picture for the business should be solid. But this doesn't mean that investors would be wise to buy in. Yes, this is a high-quality company that should fare well in the long run. But given how shares are priced, I do not think upside is all that great from here. Because of that, I have decided to rate the business a ‘hold’ at this time.

For further details see:

Graco: A Concentrated Business That's Trading Just A Bit Too High