GGG - Graco: Future Looks Bright As Margins Expand

2023-06-11 21:57:12 ET

Summary

- Graco Inc. is a solid company with impressive and growing margins and a strong balance sheet, but its current valuation is too high for a strong buy case.

- The company's focus on the US market and share buybacks strategy should help drive a 12% earnings CAGR.

- Despite the strong financials, the risk of a correction exists if there is a slowdown in spending from companies, making Graco a hold rather than a buy.

Investment Summary

Graco Inc ( GGG ) operates in the industrial manufacturing sector, focusing on fluid handling systems and equipment. Their extensive range of products is meticulously engineered to ensure efficient and accurate fluid handling. Graco's product portfolio encompasses pumps, spray guns, meters, valves, and dispensing systems, catering to diverse industrial applications.

The company might not have seen drastic revenue growth as the market they are in isn't expected to really experience it either, just a CAGR of 4.61% between 2022 and 2028. But what did impress me with the last report was the growth in the bottom line. EPS growth of 29% YoY is helping make the current valuation make a little more sense at least. But I am not sure how much margins can climb and growth is more likely seen in the top line instead. I don’t mind paying a higher premium for growth companies like these, but 27x is just too high for me and GGG will be rated a hold from me.

Market Position Is A Tailwind

Right now Graco has above 80% of its production based in the US. Given that we are seeing a clear trend toward more companies seeking suppliers in America rather than abroad should be a tailwind for GGG. With the proximity they offer, the slightly higher cost of their products compared to foreign manufacturers is worth it. The risk of supply chain issues is lower.

Growth Plan (Investor Presentation)

Looking ahead the company is targeting a 12% earnings CAGR which should be fueled by acquisitions the company is making. Besides that I also see share buybacks being a driver of this EPS growth too. Just looking at the last report by the company the shares outstanding had a yearly decline of just over 1%. With strong cash flows and margins, I think I can confidently make an assumption that GGG will continue this strategy of buying back shares and growing the value that shareholders will get.

End Markets (Investor Presentation)

Looking at some of the growth drivers the company themselves are noting is for example an increase in infrastructure spending in the US. With growing spending and demand for residential buildings still being very high across many regional markets. Looking at a comment from the CEO Mark Sheahan he made an important note about the market circumstances, “While the operating environment remains challenging, we were able to grow in all segments as component availability improved, previous pricing actions took hold and foreign exchange headwinds moderated driving improved margin results during the quarter”. Seeing that GGG is able to efficiently raise prices even though there is a general slowdown in the economy in the US compared to previous years. For the year 2023, GGG sees the top line growing in the low single digits which makes the current valuation come into question I think. Paying around 27x forward earnings for that doesn't seem too good. You would expect consistent results in the first quarter of the year to justify the current price.

Cash Deployment (Investor Presentation)

A notable move in the last report was the decrease in the Asia Pacific market across two segments in the company, the contractor and the industrials. Some of those lower revenues are due to unfavorable currencies though, but I think it’s reasonable to expect that markets like these will be more and more challenging in the coming years. Countries are starting to favor domestic manufacturers and I think the right step for GGG would be to continue acquisitions of American companies and solidify their presence there. Looking ahead through the history of the margins for the company suggests a very optimistic outlook. They are steadily trending upwards and I don’t see them decreasing harshly given the strong market share GGG has in their niche market.

Financials

Moving over to the financials of the company they maintain a strong cash position that right now can easily pay off all the long-term debts. The cash position may be down from the high of $624 million in 2021, but $395 million covers the long-term debts of $75 million several times over. This puts GGG in a very strong position financially and I am not worried dilution will ever be necessary to raise cash for liabilities.

Comparing the total liabilities with the total assets GGG has managed to build up a large discrepancy which is great to see. The total assets outweigh the total liabilities almost 5x as much. Despite that, the company is still trading quite high on a p/b valuation, which right now sits at just under 6 on a forward basis. In most cases that would be enough for me to turn away and say the company is overvalued. But GGG seems to be a decent growth story as discussed, and higher valuations like these might have to just be accepted if you want to get in on the action.

To further highlight the financial freedom the company is finding itself in, the net debts are actually negative right now by about $247 million. I don’t think the p/b is telling the full story here, GGG is a solid company to buy into looking at just the balance sheet. The share price might be another question. But with time the valuation should become more and more realistic as growth continues and GGG is able to build out their balance sheet further.

Outstanding Shares (Macrotrends)

Looking at the shares outstanding they seem to be heading in the right direction, that is less and less outstanding. The solid cash flows the company is generating, $175 million in the last 12 months is letting them be able to continue buying shares and keep up the dividend too. All in all, I think the balance sheet of GGG is very robust and I don’t see any alarming signs on it. They have been able to grow the cash position efficiently and haven't taken on any new debt either. This leaves them in a strong position to continue acquiring companies and grow their portfolio.

Valuation & Wrap Up

GGG is an interesting play for investors who wish to get exposure to a wide range of end markets that the company serves, all from pharmaceuticals to the semiconductor industry. The latest few earnings reports by the company have been very impressive and have also helped push up the share price quite heavily.

{kind=link}

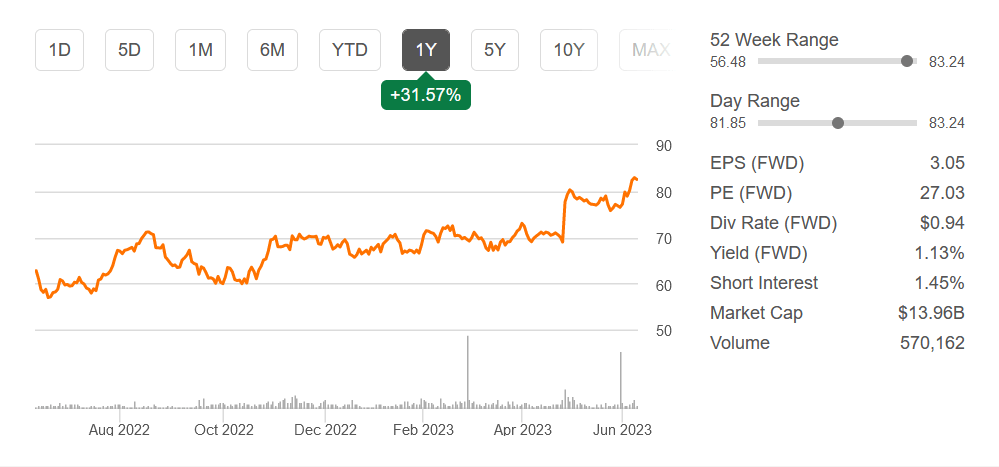

Stock Chart (Seeking Alpha)

With the forward p/e sitting around 27x currently, I don’t think there is a strong enough buy case right now. The risk of a correction is certainly there if we see a slowdown in spending from companies. But with that said, GGG is a solid company with impressive and more importantly, growing margins and a balance sheet with low debt and a high portion of the cash. I am confident that GGG will continue to grow but for now, I see them as a hold rather than a buy.

For further details see:

Graco: Future Looks Bright As Margins Expand