GGG - Graco: Many Reasons To Be Cautious

2024-01-17 04:38:26 ET

Summary

- Graco is still reporting solid results and while the top line declined, the company is still reporting double-digit bottom line growth.

- The company is very dependent on the construction and housing market, and while we see a slowdown in the metrics, the picture is still solid.

- I expect a recession in the coming quarters, leading to lower earnings per share and lower valuation multiples, resulting in a huge downside risk for the share price.

It was about 5 years ago when I published my first article about Graco, Inc. (GGG) in February 2019 and in almost every article since then I underlined that Graco is a great business, but I still did not add the stock to my portfolio. My last article published in May 2023 is no exception: I rated the stock once again as a "Hold" and explained once again why we are dealing with a great business but also a stock that is rather expensive.

Since my last article the stock increased about 9% and since my first article five years ago the stock increased 83% (and was performing more or less in line with the S&P 500). When looking at the performance, we can make the argument that my last ratings might have been wrong (and the stock was rather a "Buy"), but I will rate Graco as a "Hold" once again as I still see the stock price too high and more downside risk than upside potential at this point. In the following article I will look at the quarterly results which are still good and explain why Graco is a long-term hold, but not a buy at this point. And I will outline what my expectations for the coming years are.

Quarterly Results

We can start by looking at the last results Graco reported and although the results are nothing to get excited about, the business is still performing well. In the third quarter of fiscal 2023, Graco reported sales of $539.7 million. Compared to $545.6 million in the same quarter last year this is a decline of 1.1% year-over-year. But while the business is struggling to grow its top line, operating earnings increased 14.0% year-over-year from $143.1 million in the same quarter last year to $163.2 million this quarter. And diluted earnings per share increased 14.9% YoY from $0.67 in Q3/22 to $0.77 in Q3/23.

Graco Q3/23 Investor Presentation

{kind=link}

When looking at the results and bottom-line growth, especially the lower "costs of products sold" contributed to double-digit growth rates. Year-over-year these expenses declined 10.3% and resulted in a much higher gross margin (52.7% in Q3/23 compared to 47.8% in Q3/22). Operating margin improved as well an increased from 26.2% in the same quarter last year to 30.2% this quarter.

During the last earnings call , EVP Christopher Knutson stated:

The gross margin rate increased 490 basis points in the quarter. Strong price realization and lower product costs were more than enough to offset lower factory volumes.

While material costs have somewhat moderated compared to what we experienced last year, lower factory volumes and increased operational spending continue to be headwinds for the quarter and year-to-date. Total operating expenses increased $3 million or 3% in the quarter, primarily from volume and rate-related increases of $1 million and incremental share-based compensation of $2 million.

But we also must acknowledge that last year was rather the outlier (with extremely high prices and very expensive raw materials) and when looking at margins over time, Graco is reporting one of the highest operating margins ever, but gross margin seems to be rather in line with previous results. Graco is rather returning to normal again.

Growth vs. Recession

In my last article about Graco, I told two tales about the company and the stock. And one of these two tales was a business that might be heading for a recession and is hit hard in such a scenario. I already mentioned in my last article that Graco is extremely dependent on the housing market. This dependence on the housing market is also the major reason for the huge decline during the Great Financial Crisis.

Graco also declined extremely steep in the 1970s and when looking at the data we already have back then (housing permits for example), the housing market was also in big trouble. Of course, we have to look a little closer at data to know for sure if this was the major reason (but that could be the topic for another article).

{kind=link}

And when looking at net sales by end market in 2022, construction was responsible for 48% of total revenue and therefore we can expect that Graco will be hit hard again if there is another housing crisis in the United States (and other major markets for Graco).

Graco Q3/23 Investor Presentation

{kind=link}

It is not surprising that Graco's revenue (and especially earnings per share) are declining when construction is struggling. And as I already pointed out in my last article about Graco, construction is sending mixed messages. Depending on the metrics we are looking at, we can make the case for the housing market being far from perfect or we can also make the case for the housing market holding up quite well. I already mentioned housing permits above and after the numbers declined rather steep during 2022, the number was holding up quite well during 2023.

{kind=link}

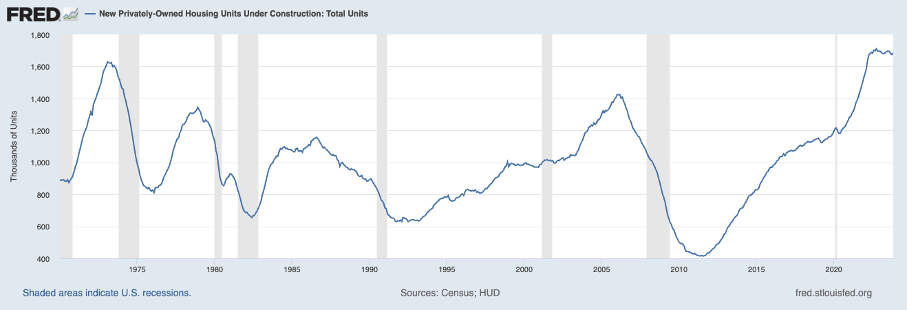

When looking at the privately-owned housing units under construction, the number is also stagnating in the last two years (after it was constantly increasing since 2011). But it is stagnating at the highest level on record (we have data since the early 1970s) and the number is even higher than before the Great Financial Crisis and slightly higher than in the early 1970s. However, I don't know how much sense it makes to compare constructed housing units in the 1970s with today's numbers as the population increased from 200 million 50 years ago to 340 million right now.

{kind=link}

Further metrics that are rather bullish for housing and construction is the still growing number of employees (although growth rates are slowing down) as well as the total construction spending in the United States. After year-over-year growth rates for construction spendings came close to zero a few quarters ago, growth is rather high again and year-over-year spending grew 11%.

What To Do?

When only looking at construction and housing data, drawing the conclusion that a recession is around the corner is rather questionable. But as I have already argued in my last article about BASF SE (BASFY) (answering the question why I think BASF is not a good investment and why I sold the stock), companies and stocks from the industrial and materials industry are probably not the best investment right now. And I also argued why it might not be the time to hold stock altogether for the next few years.

Now BASF and Graco are not operating in the same business, but the sector is somewhat similar. While we can make the argument for BASF being a chemical business, Graco is an industrial business - and both are not really recession-resilient. When looking at the sector performance in the last recessions, industrial stocks were usually hit hard - and as shown above, Graco has also declined steeply during past recessions.

And as I have argued in the article, we should be cautious about almost all stocks these days. In the article I briefly explained why it is not a good sign for the world moving towards internal and external disorder (within and between states) and the long-term debt cycle being rather close to its end:

And all three are typical signs that we are at the end of a long-term cycle, and at the end of such cycles, we usually see a "lost decade" for the stock market, many conflicts within countries, cold and hot wars between countries, the destruction of wealth and the shift of power between different groups, organizations, and countries. And all in all, this is not the best time to hold stocks. And as the stock market (the S&P 500) reached its previous all-time high again (and we see the very real potential for a double-top) now is the time to trim my positions and restructure my portfolio (now is defined here as the next few weeks or months).

Based on what I wrote about BASF and the "big picture" we could make the argument to sell Graco right now, but the situation is a little more complex. While BASF is a business that is struggling to grow (or growing only in the low single digits), Graco is able to grow in the double-digits with some consistency. On the other hand, BASF is trading for extremely low valuation multiples while Graco is mostly trading for much higher valuation multiples. Hence, the question remains: What to do about Graco?

Some Predictions

Although I see Graco as a high-quality business with a wide economic moat around the business, I would be cautious right now as Graco investors are facing two challenges - and these two challenges combined have the potential to tank the stock price once again:

- Based on the expectations of a recession (or depression) and probably a struggling housing market, we can expect lower earnings per share in the coming quarters. Graco will most likely see lower revenue and margins will also decline.

- Additionally, investors will get more cautious (or even panic) as they do in almost every recession. This usually leads to lower valuation multiples investors ascribe to most stocks. Investors expect lower growth rates as well as trouble ahead and in such a scenario almost nobody is willing to pay 25 or 30 times earnings for a stock.

Even when assuming that investors are ascribing Graco the same valuation multiples as before, the stock price will be lower when earnings contract. But in most cases, stock prices get even lower as investors are also ascribing lower valuation multiples to the stock.

Of course, investor sentiment can reverse as quickly as it got pessimistic (although panic usually sets in much quicker than confidence is restored) and a stock price can rebound quickly when earnings per share are recovering again. Nevertheless, I would not be surprised if we see another steep decline for Graco in the coming quarters (or years).

Looking At The Chart

When looking at the long-term chart, we see the picture of a stock performing great. But we also see a stock that is extremely close to the long-term trendline that has been in place since 2009 and once that trendline breaks, we can make the argument for Graco declining rather steep.

And assuming Graco is starting a bigger correction again a first potential target for the stock could be around $56. At this level we find not only the lows from 2022 as well as the highs before the COVID-19 crash, we also have the 100-months simple moving average (maybe not the most important technical indicator) as well as the 61.8% Fibonacci retracement of the last upward wave (beginning in 2009 and assuming we already saw the high).

Author's work based on TradingView

{kind=link}

In case that support level does not hold (and in case of a recession or depression I would assume a steeper correction), the next major support level is around $38. At that level we have lows from 2018 and the COVID-19 low of 2020 as well as the 200-month simple moving average and also the 38.2% Fibonacci retracement. This is not only a strong support level but also a realistic target for the stock in case of a recession. It would result in a 55% decline for the stock - which also seems reasonable during a recessions.

And although I don't think the scenario is very likely, the stock could decline even lower and a pullback to the highs set before the Great Financial Crisis is possible. This would mean the stock will decline as low as $16-$18 resulting in an about 80% decline for the stock price. This scenario seems unlikely, but we should not rule it out - especially in a deep recession or depression.

Bottom Line

The problem I have is the following. On the one hand we have a business that is performing well and has a wide economic moat around its business. And of course, the stock is not cheap, but it is also not extremely expensive. On the other hand, we have the speculation that the economy might hit a recession. Of course, I have strong arguments for my expectations, but like everybody else I don't know what will happen.

And trying to solve that contradiction seems rather difficult. But in the end, the answer is quite simple. If I don't buy Graco right now, I might miss the chance to buy a high-quality business for a price that is acceptable at best. I am certainly not missing out on any huge bargain or the deal of a lifetime. On the other hand, when buying the stock right now, I am faced with huge downside risk. This is leading to the simple conclusion: Patience!

On January 29, 2024, Graco will announce fourth quarter results and this might give us some hints what to expect in the coming quarter. Analysts got more optimistic during the last few months and are expecting earnings per share to $0.78 and compared to the same quarter last year this would be an increase of $0.05.

For further details see:

Graco: Many Reasons To Be Cautious