HOEGF - Gram Car Carriers: I Expect The Current 5% Yield To More Than Double This Year

2023-03-26 11:45:00 ET

Summary

- Gram Car Carriers operates and manages RoRo ships focusing on the transportation of cars and vehicles.

- Charter rates have exploded in the past year, and Gram will see the benefits in 2023.

- Five vessels have been re-chartered at substantially higher charter rates (with the lowest increase being 90%, the highest increase 300%).

- The dividend is based on 50% of the net income. As the net profit will likely increase based on the recently announced contract renewals, so will the dividend payments.

- The dividend is paid as a capital repayment.

Introduction

In a recent article I had a closer look at Hoegh Autoliners ( OTCPK:HOEGF ) which owns and operates car-carrying vessels. That side of the shipping market has been neglected for way too long resulting in a massive spike in the daily charter rates and it doesn’t look like the pressure will decrease until additional vessels will hit the water in 2024. Gram Car Carriers ( OTC:GCCRF ) is a smaller company operating a fleet which includes small distribution vessels, but the company is definitely taking advantage of the current boom in the car carrier vessels.

{kind=link}

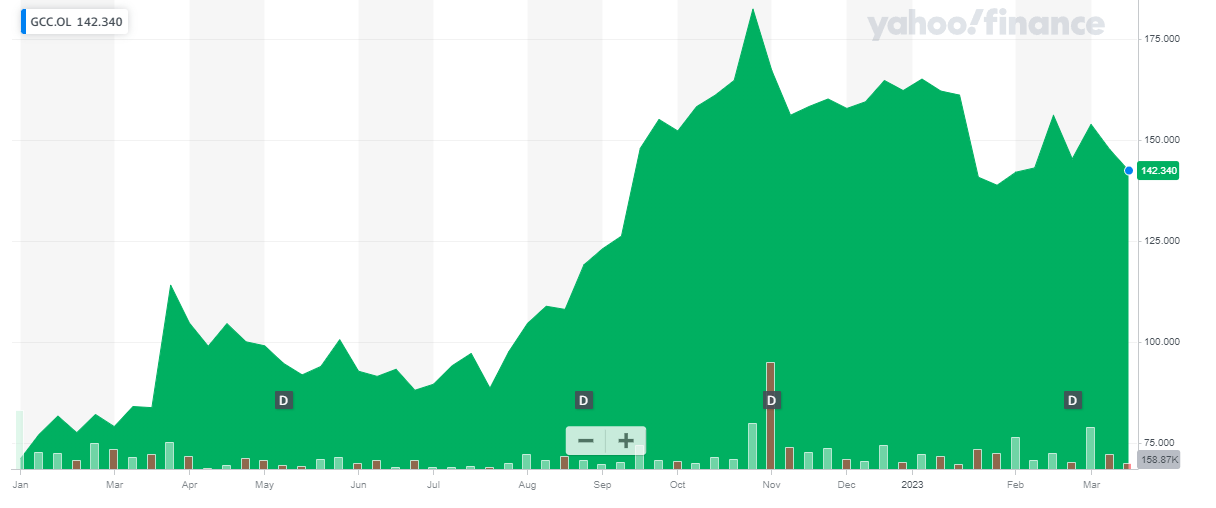

Gram Car Carriers currently has 29.3M shares outstanding . The current share price in Oslo is approximately 142 NOK/share resulting in a market capitalization of 4.2B NOK . That’s approximately $400M at the current exchange rate. The ticker symbol in Oslo is GCC, the average daily volume is almost 100,000 shares.

Strong cash flows, and they are only getting stronger

Gram Car Carriers owns 19 vessels but also manages a few more vessels for third parties. As you can see below, some of the owned vessels are ‘just’ distribution vessels, smaller ships used for the ‘last mile’ type delivery.

Gram Car Carriers Investor Relations

{kind=link}

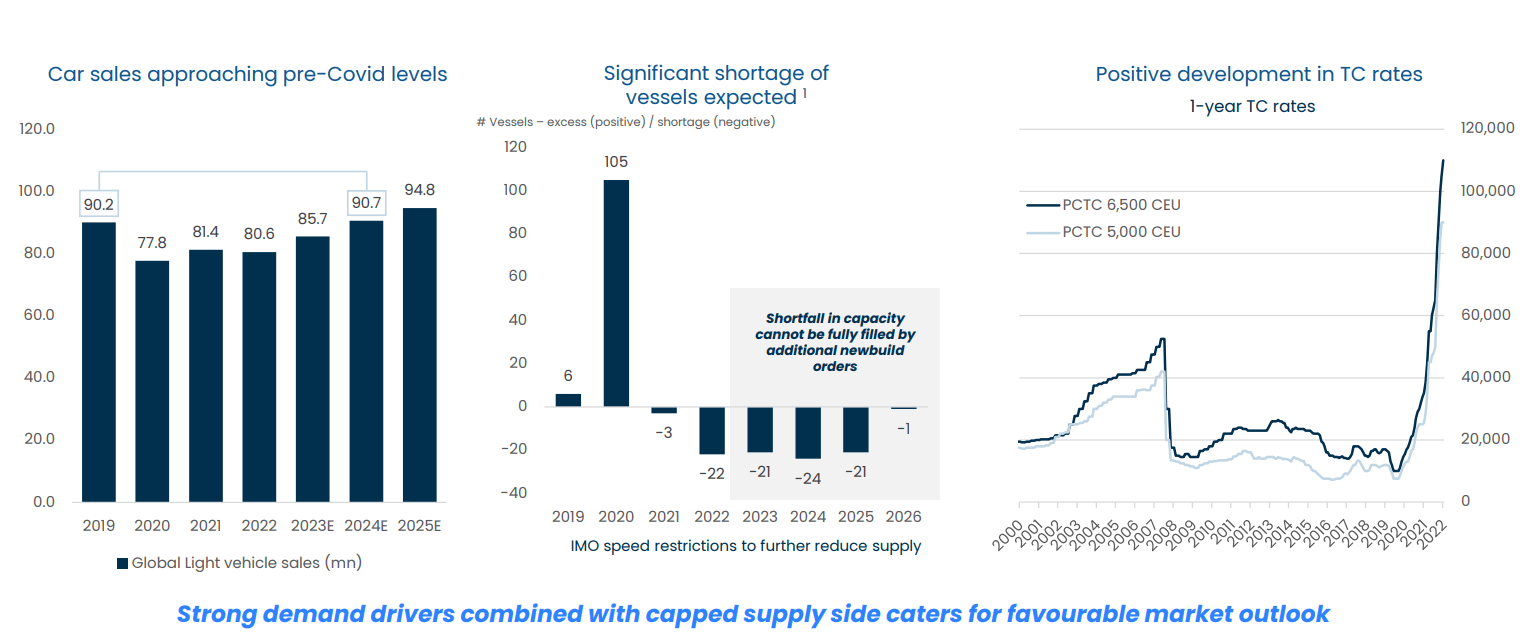

It goes without saying that smaller ships commend lower charter rates but we recently saw a similar spike in the charter rates for the ‘larger’ segment of the mid-sized vessels as charter rates throughout the sector approached $100,000/day for the large vessels and close to $100,000/day for the midsize vessels.

Gram Car Carriers Investor Relations

{kind=link}

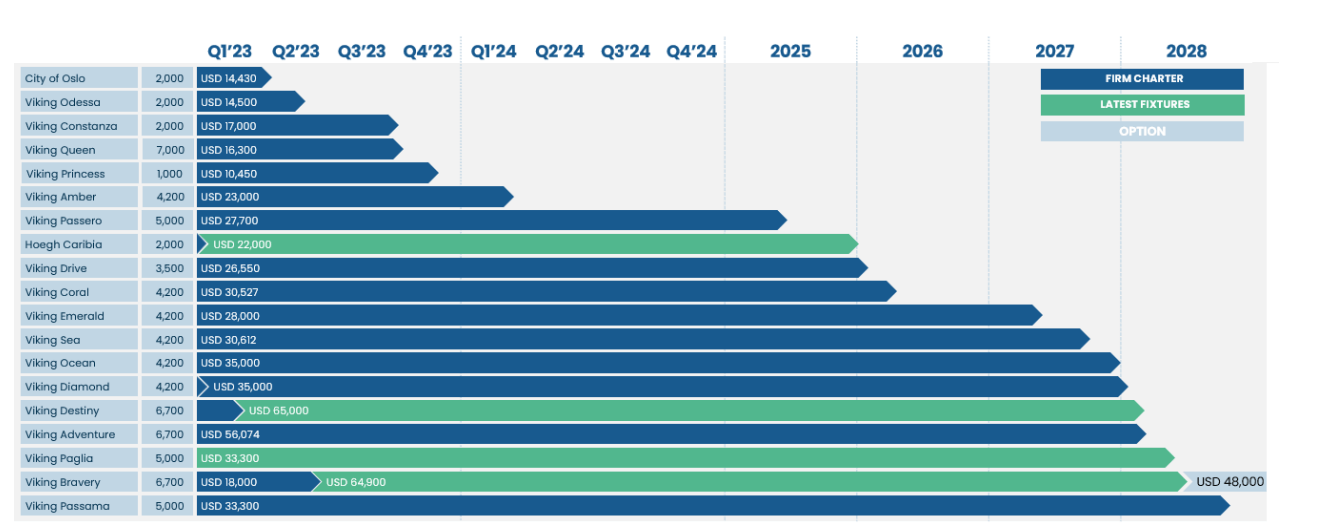

And although Gram Car Carriers has been able to post an excellent financial performance, you should realize the vast majority of its vessels were still contracted at older, lower rates. This means Gram has not fully participated in the recent violent upswing in the charter prices. Just have a look below, the Viking Queen with a capacity of 7,000 vehicles is currently still running at a rate of $16,300/day which is less than a fifth of recent 1 year charter rates (as you can see on the image above). And recent charter agreements for a five year contract were signed at an average day rate of in excess of $64,000/day , which is still four times higher than the $16,300/day the Viking Queen is currently earning. Once the vessel is up for contract renewal you should expect a substantial increase in the charter rates.

Gram Car Carriers Investor Relations

{kind=link}

We should see this happen to the Viking Destiny as well. Until the end of Q1, that vessel has a daily charter rate of $ 16,000/day . And the Viking Bravery will see a massive increase from $18,000/day to in excess of $60,000/day as well in the second half of the year. This leads me to believe the best is yet to come for Gram Car Carriers as the company is only seeing the impact from the recent charter rate increases right now. The strong charter rates will likely continue throughout the year as only 28 vessels out of the 757 vessels in this segment are available for charters this year.

Gram Car Carriers Investor Relations

{kind=link}

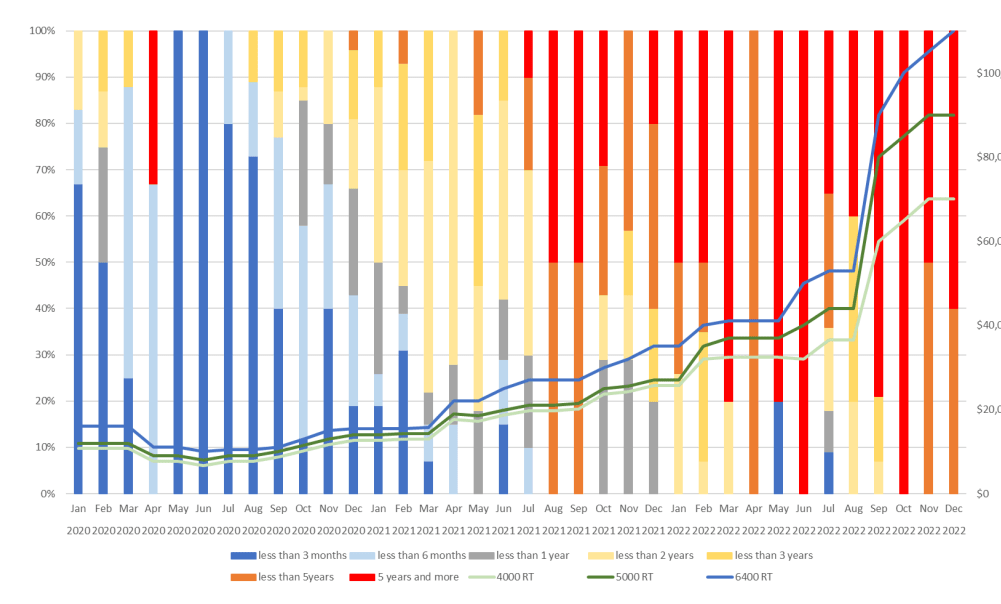

The tightening of the market is not coming as a complete surprise. In the past few years we saw a shift from short-term contracts to almost solely long-term contracts. End-users obviously want to lock in capacity in the post-COVID era to ensure all manufactured vehicles can be shipped to the clients.

Gram Car Carriers Investor Relations

{kind=link}

As we saw in the charter updates, the best is yet to come for Gram Car Carriers. But notwithstanding that element, the company’s Q4 performance already showed an important improvement compared to the performance earlier in the year as some of the higher charter rates are already trickling through.

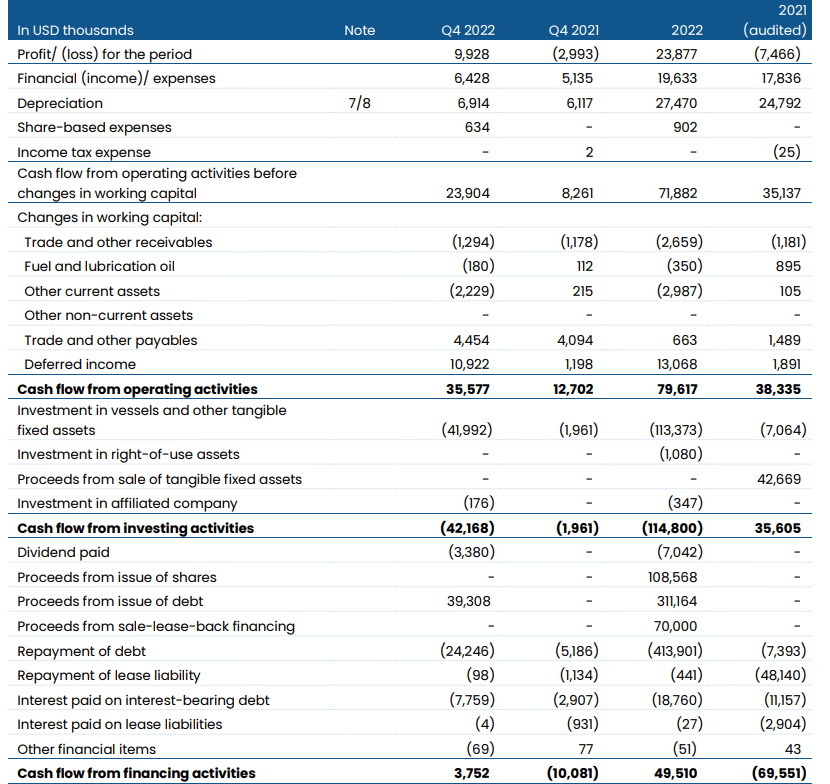

The total revenue in the fourth quarter came in at $38.3M resulting in an EBITDA of almost $23M. That’s an increase of almost 200% compared to the Q4 2021 results while the EBIT seven-folded. And despite the ‘weaker’ performance in the first few quarters of 2022, the full-year EBIT more than quadrupled to in excess of $43M.

Gram Car Carriers Investor Relations

{kind=link}

While the full-year net income came in at $23.9M for an EPS of $0.83, it’s the final quarter of the year that really sets the tone for 2023. The bottom line showed a net income of $9.9M or $0.34 per share despite seeing a substantial increase in the interest and financial expenses. That’s very encouraging and as the cash flow statement below shows, it wasn’t just a paper profit generated by Gram.

We see the total operating cash flow before changes in the working capital position came in at $23.9M. We obviously still need to deduct the $7.8M in interest expenses as well as the $0.1M in lease payments. The adjusted operating cash flow was $16M.

Gram Car Carriers Investor Relations

{kind=link}

The company also spent $42M on buying new vessels but keep in mind these acquisitions are expansion-focused as the depreciation expenses are just $7M per quarter. An example of an acquisition is the 5,000 car-equivalent unit carrier Paglia for $49M. That vessel is currently chartered out at a rate of $33,300/day all the way until 2028. Knowing the pure operating cost per vessel (excluding depreciation and interest expenses) is $7,000/day, this vessel will generate a cash margin of in excess of $25,000/day. That’s in excess of $9M per year or approximately $45M during the five year charter period.

So yes, acquisitions like this one indicate Gram Carriers had a negative free cash flow, but that’s not an issue as those acquisitions will contribute to the bottom line and that one specific purchase will pay for itself within the next 5-6 years.

Gram Car Carriers has a dividend policy which states it is paying 50% of the quarterly profit . And as the financial performance of the company improved throughout the year, and the Q4 dividend was established at $0.169/share. This brings the full-year dividend to $0.408/share. Using the current exchange rate where you get about 10.5 NOK per USD, the NOK-equivalent dividend is approximately 1.78 NOK (based on the exchange rate when the dividend was declared, the official quart erly dividend came in at 1.75 NOK ).

Gram Car Carriers Investor Relations

This means that on an annualized basis, the full-year dividend will come in at approximately 7.1 NOK per share, which is exactly 5% based on the current share price of approximately 142 NOK. As I expect the net profit to increase this year, the dividend will increase at the same pace given the fixed payout ratio of 50%. As I will explain at the end of this article, recently signed charter agreements will result in an increased revenue which will boost the net income as well as pretty much all operating expenses are fixed. The net income will likely more than double by the end of this year which means the dividend payments will increase by a similar percentage towards, or perhaps even exceeding a 10% yield based on the current share price.

As of the end of last year, Gram had about $30M in cash and just under $340M in gross debt for a net debt position of approximately $310M. As I’m not expecting any more vessel purchases this year and considering some of the new charter rates will start contributing from this year on, I am anticipating the company to generate north of $110-120M in operating cash flow. Capex could be minimal which means the underlying free cash flow could very well be $100M and rapidly and substantially reduce the net debt ahead of a capacity increase in 2024-2025. Reducing the gross debt will also help Gram to keep the interest expenses very manageable.

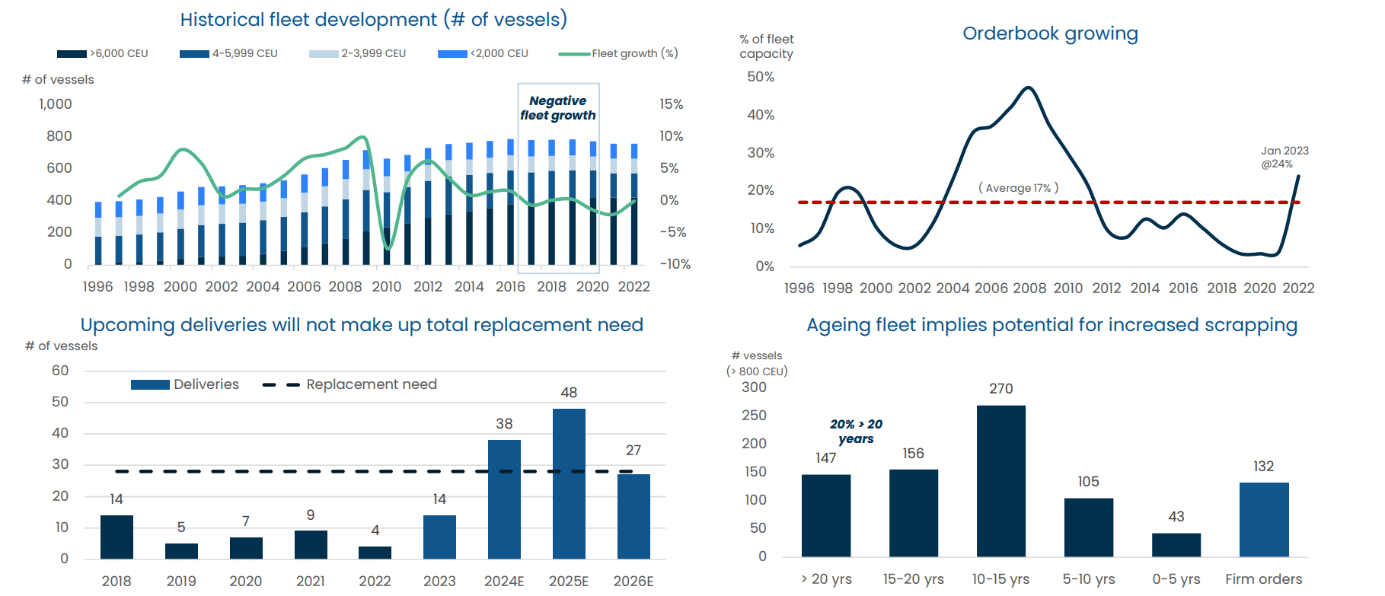

As you can see below, Gram isn’t too worried about the capacity increase as the newly delivered vessels will barely take care of the replacement need. I’m a bit more conservative as that ‘replacement need’ is just a theoretical need. As long as charter rates stay high, operators will continue to use the vessels rather than retiring them.

Gram Car Carriers Investor Relations

{kind=link}

That being said, it goes without saying that the 127 vessels that will be delivered between now and the end of 2026 will barely be sufficient to replace the fleet that’s currently over 20 years old. And by the time 2026 comes around a bunch of vessels in the age category of 15-20 years will also already exceed the 20 years.

Potential risks to the investment thesis

Investing in shipping always exposes investors to risks as well. In Gram’s case, I believe the near-term risks to be very minimal. The company has no exposure to spot shipping rates and has locked in the vast majority of its fleet on multi-year contracts providing excellent visibility for the years to come.

The main near-term risk are the contract renewals for the Viking Constanza (Q3) and the Viking Queen and Princess in Q4 2023. But as we saw how the recent charter rate for the 2,000 CEU vessels Oslo and Odessa was fixed at in excess of $25,000/day for three year contracts and as we know the recent agreements for five year deals on 7,000 CEU vessels (the Viking Queen which is up for renewal in Q4) exceeds $60,000/day, I am convinced the performance of Gram Car Carriers will get better before it gets worse.

The main risk is the expanded world fleet which will start hitting the water from 2024 on. Right now, it looks like the capacity addition may be absorbed by the increased demand to ship vehicles and the fact that a substantial portion of the ‘older’ vessels may leave the world fleet. The main longer-term risk would be to see a substantial decrease in the demand for deep sea vehicle transportation from 2025 on as charter rates may very well decrease again. And that’s why I think Gram made the right decision to lock in new charter agreements for multiple years.

{kind=link}

Of the 19 vessels shown in the image above, only four vessels are up for renewal within the next 24 months (note the City of Oslo and Viking Odessa were renewed for 3 year terms subsequent to the publication date of the charter overview. I have highlighted the vessels up for renewal between now and the end of Q1 2025.

While the risk is never zero, I think the near-term risks (with a 12-18 month time line in mind) are very limited. Upcoming contract renewals should provide excellent visibility for years to come

Investment thesis

I’m bullish on Gram Car Carriers’ performance today. Even if you only look at the increased contribution from the Viking Destiny (up $49,000/day from Q2 on) and the Viking Bravery (up by $46,000/day from Q3 on) while also taking the $10,000/day rate hike on the Hoegh Caribia into account, these three vessels alone will increase Gram’s revenue by $36M per year. That’s a 25% increase in annualized revenue (based on the Q4 revenue) caused by just these three ships and this completely ignores the charter rate potential for other vessels that will have to be rechartered this year. The Viking Odessa was rechartered subsequent to Gram publishing its report and the daily charter rate increased from $14,500 to $27,750/day for a period of three years. That’s an additional $5M in annual net revenue without seeing a material increase in operating expenses, and the City of Oslo was extended at a similar rate. So the total of five vessels with confirmed increased charter rates will add in excess of $45M in annual cash flow.

I think the market is too focused on A) near-term performance and B) the near-term expansion of the world fleet. But I expect Gram to lock in a few more long-term contracts in 2023 which will mitigate the impact from increasing volatility in the charter rates.

For further details see:

Gram Car Carriers: I Expect The Current 5% Yield To More Than Double This Year