GTE - Gran Tierra Energy Remains A Buy After Latest News

Summary

- Rising production bodes well for improved 2023 results.

- Solid oil reserve growth has lifted the after-tax NAV per share.

- Geopolitical risks associated with Colombia while a threat are overblown.

Since the 2020 pandemic it has been tough being an investor in intermediate upstream oil producer Gran Tierra Energy ( GTE )( GTE:CA ). The company was rocked by years of sharply weaker oil prices and a heavy debt load that saw the market price Gran Tierra for bankruptcy . Since then, oil prices have rallied giving most intermediate drillers a solid boost, but Gran Tierra has struggled to rally and deliver value for shareholders. Most of that stems from an overblown perception of risk associated with investing in Colombia’s hydrocarbon sector due to government plans to end contracting for oil exploration and ban hydraulic fracturing. The November 2022 tax reforms implemented by leftist president Gustavo Petro, which according to some sources nearly doubled the effective rate for oil companies in Colombia, is also weighing on Gran Tierra’s outlook. Those events, however, should not deter investors from investing in Gran Tierra which still appears particularly cheap despite disappointing 2023 guidance as discussed.

Latest developments

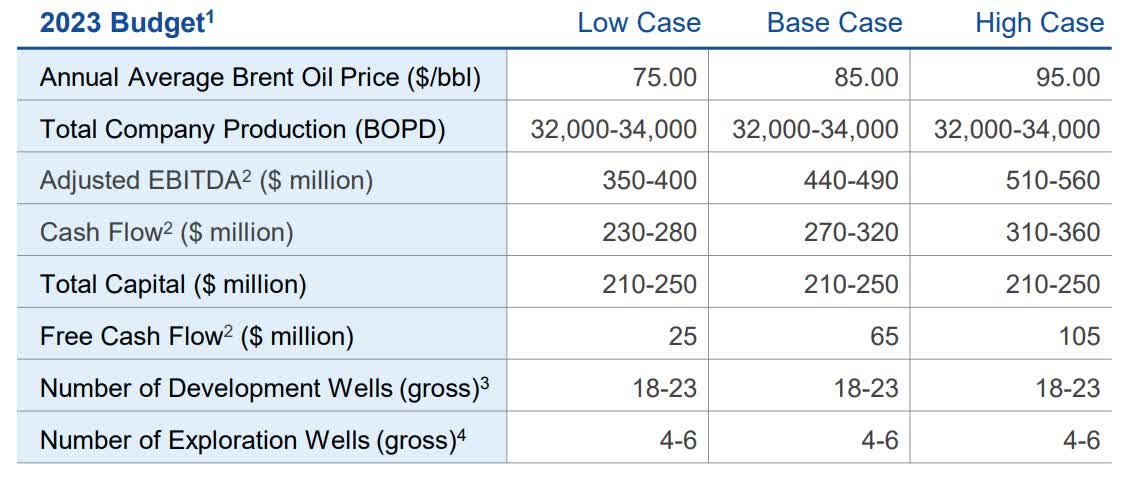

In a January 2023 operational update Gran Tierra announced that the company had achieved its 2022 annual production guidance pumping an average of 30,8000 barrels of oil per day. That is an important milestone for a driller which has repeatedly over promised and failed to deliver. Fourth quarter 2022 average exit production of 32,600 barrels per day was 10% higher than the equivalent period a year earlier. That solid production growth bodes well for Gran Tierra to achieve its 2023 budget.

{kind=link}

Source: Gran Tierra Corporate Presentation January 2023.

The driller forecast annual 2023 average production of 32,000 to 34,000 barrels per day which if achieved represents an 8%b increase over 2022. That will go a long way to boosting revenues in an operating environment where oil prices have recovered substantially since the pandemic to see Brent trading at around $85 per barrel. Gran Tierra’s base case 2023 guidance relies on Brent averaging $85 over the course of the year to generate projected annual EBITDA of $440 million to $490 million and $65 million of free cash flow if the production target is achieved.

In a mid-December 2022, I explored what Gran Tierra’s 2023 budget means for the driller’s valuation . I calculated that if the forecast 2023 EBITDA was achieved Gran Tierra has an indicative fair value of $2.53 to $2.97, which is between 164% and 209% of the company’s market value of $0.96 per share at the time of writing. While Gran Tierra’s 2023 budget accounts for the additional taxes payable after Petro’s tax reforms there is still considerable concern that heightened country risk will continue to impact the driller’s financial performance and ultimately valuation. While I believe that perception of risk to be significantly overblown the driller has taken measures to reduce risk and strengthen its financial position.

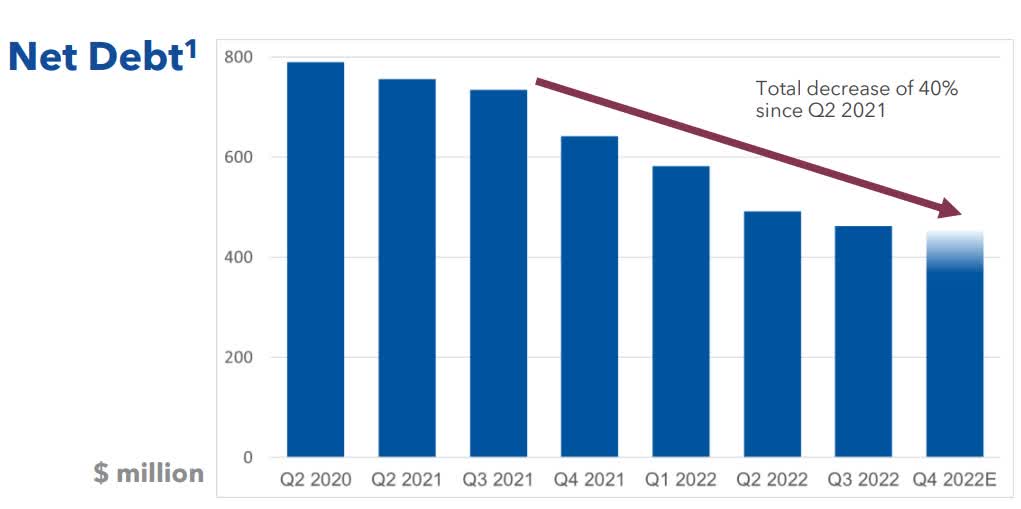

Importantly, Gran Tierra’s debt continues to fall, and the driller now has a well-laddered debt profile with no near-term maturities.

{kind=link}

Source: Gran Tierra Corporate Presentation January 2023.

Year ending 2022 Total debt is $580 million, which after deducting cash of $127 million leaves net debt of $453 million. That represents a significant decrease from 2020 when net debt was hovering at around $800 million.

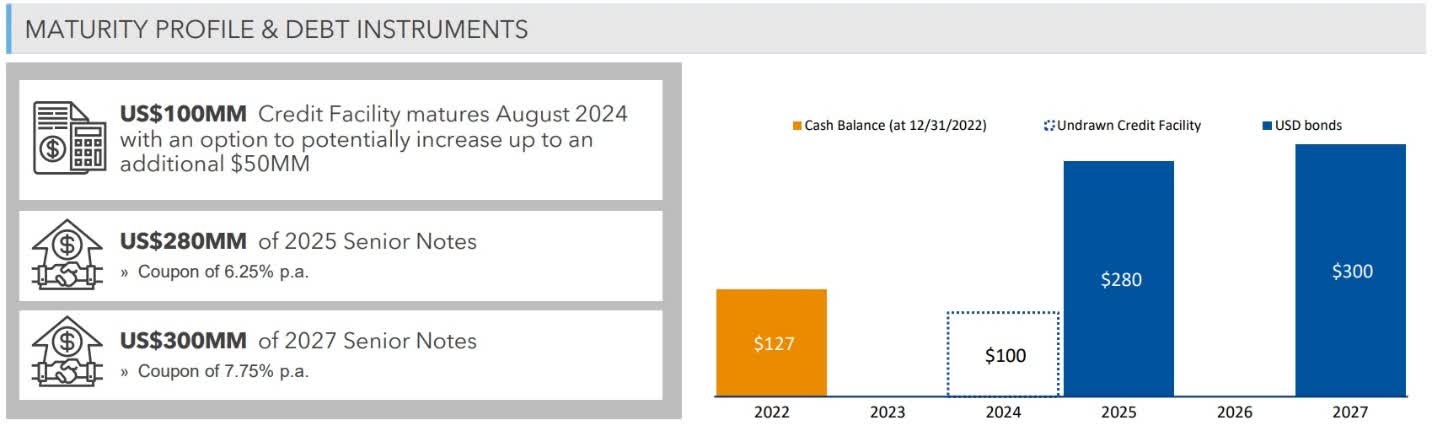

Gran Tierra has a well-laddered debt profile with no near-term maturities. The nearest maturity is $280 million of senior notes in 2025 followed by another $300 million during 2027.

{kind=link}

Source: Gran Tierra Corporate Presentation January 2023.

Gran Tierra also has an undrawn credit facility with a $100 million limit which matures during August 2024, and there is the potential to increase that facility’s limited by $50 million. This gives the driller an additional source of liquidity should it be required. The substantial debt reduction along with significant liquidity considerably reduces the risks associated with Gran Tierra and the company’s exposure to volatile commodity prices.

An important event which boosts Gran Tierra’s value is the growth of the driller’s oil reserves. During 2022 the company’s oil reserves grew while a share buyback saw it reduce the volume of common shares. Those events are responsible for boosting the net present value of Gran Tierra’s hydrocarbon reserves which are the company’s core assets that give the company value. The generally accepted industry valuation methodology for intermediate upstream drillers is to calculate their net asset value per share, which incorporates the NPV-10 of their oil reserves.

Toward the end of January 2023, Gran Tierra announced some impressive reserve replacement rates which for proven or 1P reserves was 126% then 148% for proven and possible or 2P reserves and 280% for possible otherwise known as 3P reserves. Those solid ratios show that Gran Tierra is actively expanding its oil reserves thereby boosting the company’s value. By the end of 2022 the driller’s 1P reserves had grown by 3.7% year over year to 84 million barrels while 2P reserves were 4% higher at 130 million barrels. Notably,16 million barrels were added to Gran Tierra’s 2P reserves through exploration discoveries, pointing to the considerable exploration upside held by the driller’s acreage. This reserve growth has boosted the net present value of Gran Tierra’s reserves, which has been further bolstered by higher oil prices.

Despite Brent having given back most of its 2022 gains, after soaring to over $133 per barrel after Russia’s invasion of Ukraine, it is still trading at around $81 per barrel. That amount is significantly higher than the 2021 annual average price of $70.86 a barrel. A higher average Brent price will bolster the NPV-10 for Gran Tierra’s oil reserves. The 2022 after-tax NPV-10 of Gran Tierra’s 1P oil reserves was $1.328 billion a 6% increase over 2021, while for 2P reserves the value had risen 5% year over year to $1.833 billion. Gran Tierra’s independently calculated NPV-10s were determined using an average Brent price of $80.56 which is significantly greater than the $70.37 used for the company’ 2021 NPV-10 calculations. That price, however, is still lower than the Brent price of $81 a barrel at the time of writing and the $100.93 per barrel average for 2022.

The increased value of Gran Tierra’s oil reserves has boosted the driller’s after-tax NAV per share. After deducting net debt and dividing by the volume of shares outstanding Gran Tierra has an after-tax NAV for its 1P reserves of $2.53 per share, as per the calculations below.

Gran Tierra 1P After-Tax NAV (Gran Tierra)

Source: Gran Tierra Update January 24, 2023, Gran Tierra Corporate Presentation January 2023 and author’s own work.

NB: All debt is as per disclosed in Gran Tierra’s Corporate Presentation January 2023 and the share count is as per the January 2023 Reserves Update.

This gives Gran Tiera an indicative fair value of $2.53 per share which is 181% higher than its price of $0.90 at the time of writing, indicating there is considerable upside available for investors with a large margin of safety. If we turn to the after-tax NAV of Gran Tierra’s 2P reserves, which is the widely recognized industry valuation methodology, that indicative fair value rises to $3.99 per share, as the table below shows.

Gran Tierra 2P After-Tax NAV (Gran Tierra)

Source: Gran Tierra Update January 24, 2023, Gran Tierra Corporate Presentation January 2023 and author’s own work.

NB: All debt is as per disclosed in Gran Tierra’s Corporate Presentation January 2023 and the share count is as per the January 2023 Reserves Update.

That 2P after-tax NAV per share is 343% or 4.4 times greater than Gran Tierra’s market price at the time of writing. That demonstrates that there is considerable upside available to investors with a wide margin of safety.

Risks not as severe as initially thought

A key reason for Gran Tierra to be trading at such a steep discount to the after-tax NAV of its 1P and 2P reserves is the increased risk associated with operating in Colombia. In November 2022, the Andean country’s first leftist president hiked taxes for oil companies . This saw the implementation of a price-based surcharge when the Brent price exceeded certain levels and removed royalty payments as a tax deduction. Essentially the surcharge which increases as the Brent price rises will be applied as follows:

- A 5% levy is applied when Brent is selling for $67.30 to $75 per barrel;

- the surcharge rises to 10% when the price is at $75 to $82.20 a barrel;

- then reaches 15% if Brent is selling at over $82.20 per barrel.

This it was feared would almost double the effective tax rate for oil companies operating in Colombia from 36% to 70% and create a tremendous financial burden that will erode profitability. That does not appear to be occurring with most of Gran Tierra’s peers operating in Colombia, such as Parex Resources ( OTCPK:PARXF )( PXT:CA ), calculating the impact will not be so extreme. According to Parex the effective tax rate rises to around 39% with the tax reforms.

There is also the threat posed by Petro’s plans to ban contracting for hydrocarbon exploration, which was reaffirmed by the Minister of Mines and Energy at the Davos World Economic Forum. That occurred despite signs that the Petro administration was easing its plans to end oil exploration in Colombia with the hydrocarbon sector being a key economic driver responsible for a third of exports by value and around a fifth of fiscal revenues.

Colombia’s petroleum industry is crucial to ensuring that Andean country’s energy security, particularly with natural gas now an important part of the energy mix. It is important to note, Petro’s administration has repeatedly stated it will respect existing contracts and a date has yet to be set for when licensing of new hydrocarbon exploration will end. For these reasons the risks posed by the controversial plan to end contracting for hydrocarbon exploration are not as severe as initially believed.

Final thoughts

Gran Tierra’s ongoing success associated with growing its proven and probable reserves along with higher exit production for 2022 bodes well for the driller’s performance during 2023. Increased 1P and 2P reserves indicate that Gran Tierra remains heavily undervalued by the market with an overblown perception of risk, primarily due to the focus of the company’s operations in Colombia, weighing heavily on its value. Based on the higher 1P and 2P reserves at the end of 2022 Gran Tierra has an indicative fair value of $2.53 to $3.99 per share. Those new numbers are 8% and 15% greater than the indicative fair value using the after-tax NAV of Gran Tierra’s 1P and 2P reserves in my November 2022 article . They are also 181% and 343% higher than Gran Tierra’s market price of $0.97 at the time of writing indicating that not only is there tremendous potential upside ahead but also a soldi margin of safety. Higher oil prices, Gran Tierra’s ongoing share buyback and an easing of the heightened geopolitical risks in Colombia will all acts as key catalyst to drive Gran Tierra’s share price higher.

For further details see:

Gran Tierra Energy Remains A Buy After Latest News