GTE - Gran Tierra Energy's Latest Numbers Disappoint But It Remains A Buy

2023-05-06 20:42:27 ET

Summary

- Disappointing First Quarter 2023 results spark deep sell-off.

- Geopolitical and commodity price risks weighing on outlook.

- Gran Tierra is heavily undervalued due to overblown perception of risk.

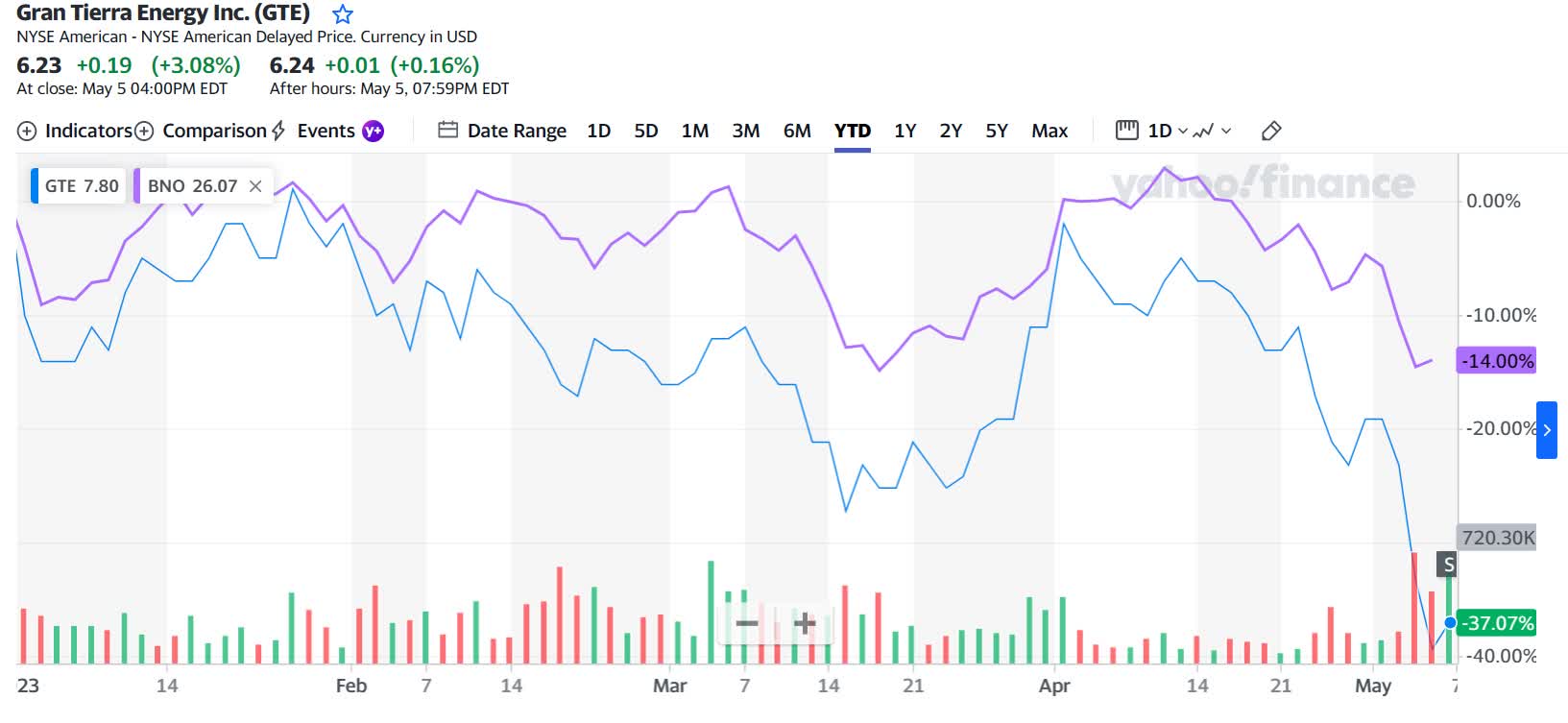

Beaten down intermediate oil producer Gran Tierra Energy ( GTE )( GTE:CA ) saw its share price plunge in the wake of reporting its first quarter 2023 results, which deeply disappointed the market. As you can see from the price chart below the sell-off now sees the driller down 37% for the year to date compared to 14% for the Brent international oil price.

{kind=link}

Those recent developments coupled with Gran Tierra completing its 10-for-1 reverse split on May 4, 2023, make now an important time to determine whether the company remains deeply undervalued as I concluded in my April 17, 2023, article . In that analysis I found despite the considerable geopolitical headwinds buffeting Gran Tierra that it has an after-tax 2P NAV of $4.14 per share or 6.6 times its current share price, after accommodating the 10-for-1 reverse split.

There is no doubt that Gran Tierra is being sharply impacted by the elevated geopolitical risk associated with its operations in Colombia where most of its oil reserves and production are located, but that risk is overblown. There are clear signs that after the latest sell-off, sparked by Gran Tierra's $10 million first quarter 2023 loss, that the market has severely overreacted creating an opportunity for risk tolerant investors to acquire a deeply undervalued intermediate oil producer.

Latest results disappoint

Gran Tierra’s first quarter 2023 results , while on first appearances are extremely disappointing, are not as bad as the market believes. The key number driving the savage drop in the driller’s market value was its bottom line $10 million loss for the quarter. The main reasons for that disappointingly poor bottom-line result are myriad, key being a sharp decline in revenue from oil sales, which fell 17% year over year to $144 million.

The primary driver was a 25% decrease in the realized price per barrel sold, which for the period was $63.65 compared to $85.33 a year earlier. That occurred because the average Brent price for the first quarter 2023 was 16% lower than for the same period a year earlier. The price differentials for Colombia’s two crude oil blends Castilla and Vasconia were also significantly wider. Castilla sold for the period at an average discount of $15.17 per barrel to Brent compared to $6.38 for the first quarter 2022, while Vasconia’s discount was $7.87 a barrel against $3.60.

There was a sharp increase in first quarter 2023 operating expenses, which rose 18% year over year to $41 million. That occurred due to higher lifting costs, predominantly driven by increased oil production at Gran Tierra’s Ecuador properties being responsible for 66% of the higher lifting costs, and more expensive equipment rental in Colombia for exploration activities. Depletion, depreciation and accretion also rose 26% year over year to $51.7 million, against $40 million for the equivalent period a year earlier, due to due to increased production and higher costs in the depletable base. There was also a first quarter 2023 $1.7 million foreign exchange loss compared to a $3.7 million gain a year earlier, which further impacted earnings.

Taxes yet again are playing a prominent role in Gran Tierra’s performance and outlook. During November 2022 Colombia’s Congress approved a tax bill introduced by the country’s first leftist president Gustavo Petro. As part of the reforms aimed at raising $4 billion to contain a widening budget deficit and bolster funding for social programs taxes for oil companies operating in Colombia were hiked. This included the removal of petroleum royalties as an income tax deduction and applying a scalable levy when the international Brent price exceeds a certain level. An additional 5% tax is payable when the Brent price ranges from $67.30 to $75 per barrel, which rises to 10% at $75 to $82.20 per barrel and then an additional 15% is payable when prices exceed $82.20 a barrel.

That sparked considerable speculation as to how it will impact oil companies and their effective tax rate. Economic thinktank Fedesarollo argued it will lift the effective tax rate for energy companies from 36% to 70%, whereas the government calculated the effective tax rate will rise to around 50% if the average Brent price for the period exceeded $82.20 per barrel. Total income tax expense fell 17% year over year to $32.9 million, primarily due to lower taxable income from reduced oil sale revenue.

According to Gran Tierra’s first quarter 2023 report, its effective tax rate for the period was 142% compared to 50% for Colombia “primarily due to an increase in non-deductible foreign translation adjustments, the impact of foreign taxes, non-deductible royalty in Colombia and increase in the valuation allowance.” The considerable increase in the effective tax rate has not come from Colombia’s tax hikes but foreign taxes related to operations in other jurisdictions and Gran Tierra taking the opportunity to reduce future tax liabilities at a time when taxable income is low.

Sharply lower oil revenue and higher expenses coupled with Gran Tierra spending a substantial portion of its 2023 capital budget of $210 million to $250 million on drilling 14 development wells during the quarter saw negative free cash flow of $10 million. Those 14 wells, plus a further 4 completed during the first 5 weeks of the second quarter 2023 to give a total of 18 wells already drilled make-up a sizable portion of the 18 to 23 development wells planned for completion during 2023. The completion of those wells early in 2023 will give oil production a significant boost.

While those numbers are particularly disappointing for Gran Tierra’s hard-hit shareholders there was also good news contained in the results. Key being an 8% year over year increase in oil production to an average of 31,611 barrels per day during the first quarter 2023. That number, however, is still lower than the 32,000 to 34,000 barrels per day budgeted for 2023, although the completion of 18 development wells from a planned maximum of 23, will help to lift oil output and cover that shortfall.

The outlook for the remainder of 2023

The recent sharp decline in oil prices which sees Brent down by nearly 15% over the last month is weighing Gran Tierra’s outlook. That can be blamed on weak economic data and growing fears of a recession. Those recent losses have almost wiped out all of the gains that came with OPEC’s surprise early April 2023 production cut, which saw Saudi Arabia alone slash output by 500,000 barrels per day. There is, however, growing bullish sentiment over the outlook for oil over the remainder of 2023 with OPEC members under pressure to boost prices to balance their budgets and the onset of the summer driving season.

The U.S. EIA has forecast an average Brent price for 2023 of $85 per barrel, which is in line with Gran Tierra’s base case 2023 budget, which is reliant upon Brent averaging $85 per barrel over the course of the year. That value is slightly higher than the international benchmark’s average of $82.10 per barrel for the first quarter. There are signs Brent may not average $85 per barrel over the course of 2023 with recession fears, poor economic data from China and a supply surplus weighing on its outlook.

This means that Gran Tierra could fail to achieve its base case annual budget.

{kind=link}

Gran Tierra 2023 Budget (Gran Tierra May 2023 Corporate Presentation)

That means the driller will fail to deliver the planned financial numbers including free Cash flow of $65 million for 2023. Gran Tierra’s low case plan requires Brent to average $75 for 2023, which does appear likely, and if achieved will deliver $25 million in free cash flow. If that occurs, it has the potential to trigger a worrying problem for the company relating to its outstanding 2025 notes which are a lability totaling $272 million and fall due during February 2025.

{kind=link}

Debt Chart (Gran Tierra May 2023 Corporate Presentation)

By the end of the first quarter 2023, Gran Tierra only had cash of $105.7 million, accounts receivable of $13.6 million and $20 million of inventory, leaving a substantial shortfall if the company pays the liability due for the notes. The driller does have an undrawn $150 million cash facility which matures in 2024, and will likely be refinanced, but that will address the shortfall for the 2025 notes. For these reasons, Gran Tierra will need to obtain some form of financing for the notes which will likely be provided on onerous terms, thereby causing the company’s financing expenses to rise.

Finding the indicative fair value

While Gran Tierra’s first quarter 2023 results are certainly disappointing and underscore the considerable headwinds faced by the company and its downside exposure to weaker oil prices the valuation from my last article stands. In that analysis I calculated Gran Tierra’s after-tax 1P NAV per share was $2.62 and $4.14 for 2P. Using the same methodology applied in my April 17, 2023, update on Gran Tierra adjusted to reflect current numbers, including:

- a lower count of 333,069,000 outstanding common shares, which after the 10-for 1-reverse split changes to 33,306,900 common shares;

- reduced long-term debt of $581,391,000; and

- cash and cash equivalents of $105.7 million as per Gran Tierra’s first quarter 2023 results.

For the sake of providing a direct pre-reverse split comparison I have used the outstanding number of shares as per the March 2023 financial results. This, as per the chart below, gives an after-tax 1P NAV per share of $2.56, which is slightly lower, 2.3%, than the previous calculation of $2.62.

Financial Valuation Calculations (Gran Tierra March 2023 Financial Report and Author's own calculations)

*Note: After the 10-for-1 reverse split Gran Tierra has an after-tax 1P NAV of $25.60 per share.

That value after accounting for the reverse split is equivalent to $25.60 per share, which is four-times higher than Gran Tierra’s value of $6.33 at the time of writing.

Gran Tierra’s indicative fair value rises to $4.08 per share pre-reverse split or $40.80 post reserve split, as the chart below shows, for its after-tax 2P NAV per share. That value is 1.4% lower than the previous update where it was $4.56 per share.

Valuation Table (Gran Tierra March 2023 Financial Report and Author's own work)

*Note: After the 10-for-1 reverse split Gran Tierra has an after-tax 2P NAV of $40.80 per share.

As discussed in previous articles the 2P after-tax NAV per share is essentially the industry accepted standard for determining an intermediate oil producer’s indicative fair value. For that reason, Gran Tierra certainly appears heavily undervalued, especially after its latest sell-off, considering the after-tax 2P NAV per share of $40.80, after the 10 for 1 reserve split, is six times greater than its market value of $6.33 at the time of writing. That demonstrates there is also a considerable margin of safety for investors.

Headwinds and risks create uncertainty

The market’s substantial undervaluation of Gran Tierra can be attributed to a heavily overblown perception of risk associated with operating in Colombia coupled with the company’s sharp sell-off after it released those poor first quarter 2023 results. I have discussed the geopolitical risks associated with operating in Colombia at length in prior articles here:

- Parex Resources: Deeply Undervalued And Remains A Buy (Rating Upgrade) ;

- Gran Tierra Energy Remains A Buy As More Positive Catalysts Emerge ;

- Frontera Remains A Buy After Strong Results And Improved Outlook ; and

- Gran Tierra Energy Remains A Buy After Latest News .

Aside from commodity price risk the main risks facing Gran Tierra arise from its operations in Colombia. Colombia’s first leftist President Gustavo Petro who was inaugurated on August 7, 2022, hike taxes which were accepted by Congress during November 2022. That reform saw royalties removed as an income tax deduction and the imposition of a scalable levy on oil sales based on the Brent price. An additional 5% tax is payable when the Brent price ranges from $67.30 to $75 per barrel, which rises to 10% at $75 to $82.20 per barrel and then an additional 15% is payable when prices exceed $82.20 a barrel. This has lifted the effective tax rate for upstream producers operating in Colombia to 50% from 36% prior to the reforms being written into law.

There are also considerable risks related to Petro’s plans to end awarding contracts for hydrocarbon exploration, which despite some signs that it may not go ahead, appears on track to be implemented. Petro is also in the process of banning hydraulic fracturing with a bill to enact this proposal being passed by Colombia’s Senate and sent to the lower house for review. While Colombia’s national government has committed to respecting existing hydrocarbon exploration and production contracts the proposals mentioned above to point to greater regulatory pressure being placed on the sector.

Civil unrest and security risks remain a constant hazard in Colombia. The South American country’s energy infrastructure is seen as a legitimate target by the last leftist guerilla groups operating in the country the National Liberation Army (ELN – Spanish initials) which regularly bombs pipelines. Oil theft from Colombia’s pipeline network using illicit taps is growing. These events, when they occur, force the shuttering of pipeline by the operator CENIT, a subsidiary of national oil company Ecopetrol ( EC ). This means drillers like Gran Tierra must use higher cost road transport to ship the oil produced to ports for shipment to international energy markets or store the petroleum produced on site until the pipelines reopen. That impacts earnings by causing transport costs to spike as well as reducing the volume of oil available for sale.

Rising civil unrest due to the petroleum industry’s disintegrating social license remains a constant hazard. Many communities, due to broken promises, oil spills and frequent polluting emissions are opposed to industry operations. That has led to community blockades and oilfield invasions forcing drillers to shutter operations, again impacting production volumes and therefore revenue.

Bottom line

Gran Tierra’s first quarter 2023 results certainly shook investors with the company’s $10 million especially disappointing. There are also a range of risks weighing on the driller’s outlook, notably the prospect of softer oil prices and the looming long-term debt liability related to the $272 million February 2025 notes. When those reasons are contemplated along with the heightened geopolitical risks in Colombia, it is understandable why Gran Tierra was heavily sold-off by the market after it released its first quarter 2023 results. What is clear is that Gran Tierra is trading at a deep discount to the after-tax 2P NAV per share of $40.80 which is six times higher than its share price at the time of writing, highlighting that there is considerable upside with a solid margin of safety on offer.

It is important to note that Gran Tierra is a high-risk investment facing considerable geopolitical risk operating in a strife-torn South American, which despite being the continents longest running democracy, is experiencing substantial political upheaval. There is also the risk posed by Gran Tierra’s dependence on oil prices, which have become particularly volatile in recent weeks due to mixed economic data and fears of an economic hard landing.

For further details see:

Gran Tierra Energy's Latest Numbers Disappoint But It Remains A Buy