GRNNF - Grand City Properties: Strong Operating Performance And Cheap Valuation

2023-08-17 02:18:19 ET

Summary

- Grand City Properties has reported a positive operating performance in the first half of 2023.

- Despite portfolio valuations being impacted by rising interest rates, rental income growth remains solid.

- GCP's balance sheet and liquidity position are strong, allowing the company to manage the current downtrend in the real estate market.

Grand City Properties ( OTCPK:GRNNF ) has reported a good operating performance and its valuation remains quite cheap, making it a good value play in the German residential sector.

As I’ve analyzed in previous articles , Grand City Properties ((GCP)) is a good value play in the German residential sector as the company has strong fundamentals, and like most of its peers, is trading at a depressed valuation.

As the company has recently released its first half of 2023 earnings, in this article I analyze its most recent earnings and update its investment case to see if GCP remains a good value play for long-term investors.

Earnings Analysis

GCP’s investment portfolio was valued at about €9 billion at the end of last June , a decline of 5.4% YoY, as the market value of properties in Germany have been in a downtrend on recent quarters due to higher interest rates in Europe.

While this drop was considerable, it was a better outcome than its largest peer Vonovia ( OTCPK:VNNVF ), which reported a like-for-like portfolio decline of 6.6% during the same period, showing that GCP’s portfolio quality is quite good.

Lower portfolio valuations are mainly the result of higher interest rates, considering that GCP’s operating trends continued to perform well in recent quarters, which are positive for property valuations. Indeed, GCP’s in-place rent increased slightly over the past six months and its vacancy rate declined to 3.9% at the end of Q2, which are both positive developments and show that GCP’s portfolio quality continues to improve despite lower market valuations.

Operating trends (GCP)

Regarding rental income growth, the company was able to report an increase of 2.7% YoY, of which 2.4% is justified by higher in-place rent and only 0.3% by higher occupancy. This is a strong signal that the residential market in Germany remains tight, a situation that is explained by the tight supply-demand profile of the residential market, which has not changed in recent quarters as construction of new apartments has clearly slowed down.

This bodes well for players in the residential market, as demand for housing remains strong despite the economic slowdown and the inflationary environment that leads to lower affordability for households, but so far this has not impacted rental growth that much. Due to acquisitions, total rental income increased by 5% YoY to more than €200 million in the first semester, which is a strong performance considering the market background.

GCP’s total revenue was €309 million in the semester, an increase of 13.6% YoY, justified by higher operating expenses that are recoverable from tenants and increased significantly due to the inflationary environment over the last year. Its reported EBITDA was negative in H1, driven by lower property valuations (negative impact of €539 million in the period), while its adjusted EBITDA amounted to €160 million (+5% YoY).

Its net profit was negative by €401 million in H1 2023, again justified by negative property revaluations, while its operational performance adjusted for the non-cash effect was quite good in the first half of the year. Its free funds from operations ((FFO)) amounted to €94 million, a decline of 3% YoY, due to higher financing costs.

While in the past the company used an asset rotation strategy to create value, this is no longer possible as the transaction market has declined significantly. While GCP was able to sell some assets in recent months, this is mainly to strengthen its balance sheet and improve its liquidity position, rather than to seek business growth.

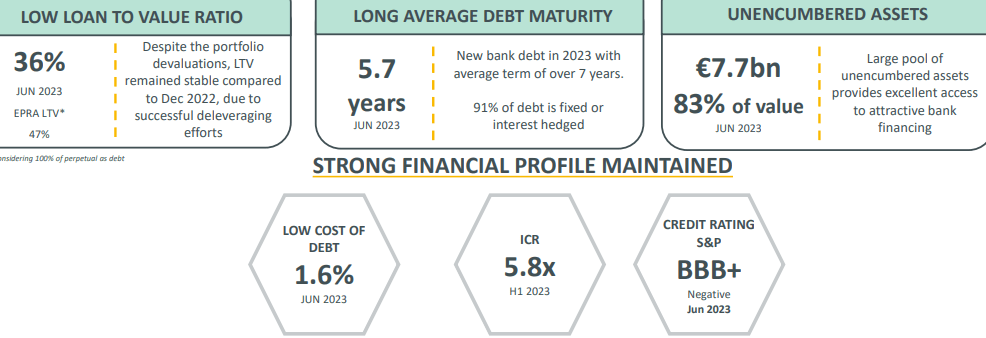

Indeed, GCP was able to close asset disposals amounting to €250 million during H1 2023, plus it has signed further disposals of about €130 million that it expects to complete in the coming months. This has improved its cash position to €714 million at the end of June, compared to €429 million at the end of 2022.

Beyond that, GCP has signed new banking financing of about €440 million during the past two quarters, of which it has drawn €190 million during H1. This is quite important to show that GCP has good access to external funding sources, enabling it to not be a forced asset seller in the near future, which would put the company in a bad negotiation position.

As the company has enough liquidity to cover debt maturities until the second quarter of 2026, it does not need to sell assets over the next couple of years to cover debt maturities, which is quite positive considering the current difficult environment to raise new debt in the capital markets. Moreover, about 83% of the company’s assets are available to be used as collateral for new debt financing, thus I don’t expect GCP to have any refinancing needs over the coming years.

Regarding its balance sheet leverage, which is measured by the loan-to-value ((LTV)) ratio, this increased slightly to 36% at the end of last June, or 47% considering perpetual debt. This was a positive outcome considering portfolio devaluations in recent quarters, as the company has made some efforts to deleverage and maintain an acceptable LTV ratio. This is key to maintain an investment grade credit rating, thus it’s quite likely that GCP will continue to prioritize balance sheet deleveraging in the coming quarters as downward pressure on property valuation is likely in the short term.

{kind=link}

Furthermore, as I’ve analyzed in my previous article on GCP, the market is currently penalizing companies with relatively high LTV ratios (including hybrid debt), thus GCP has an incentive to redeem hybrid debt when possible, to narrow its difference between its reported LTV ratio and ‘adjusted’ LTV ratio. However, as current market and credit conditions remain quite uncertain, I don’t expect GCP to buy back hybrid debt in the short term, but this is a possibility if management sees market conditions improving in the next few quarters.

Regarding capex, while new investments have been put on hold, the company continues to invest on current properties and repositioning capex increased to €37 million in H1 2023, up by 10.6% YoY. GCP’s focus is on improving asset quality, which seems to be the right approach to lead to higher portfolio valuations over the long term.

Regarding its guidance for the full year, GCP now expects FFO to be between €175-185 million, a small increase compared to its previous guidance and market expectations, and potentially to distribute next year a dividend per share between €0.76-0.80. Investors should note that GCP usually pays one dividend per year and has decided to suspend its dividend payment related to 2022 earnings, thus it’s quite uncertain if the company will decide to distribute a dividend related to 2023 earnings.

Conclusion

Grand City Properties has reported a positive operating performance during the first semester of the year, even though portfolio valuations continue to be hit by rising interest rates. Despite that, rental income growth remains solid and the company’s balance sheet and liquidity position is good, thus GCP is in good position to manage the current downtrend in the real estate market without the need to sell assets at fire-sale prices.

While its share price has recovered somewhat from its March lows, GCP’s valuation remains quite depressed trading at only 0.30x NAV, continuing to trade at a discount to both its closest peers and its own historical valuation. This valuation remains quite cheap for a company with good fundamentals like GCP, thus it remains a good value play within the German residential sector.

For further details see:

Grand City Properties: Strong Operating Performance And Cheap Valuation