GPK - Graphic Packaging: Fear Over Heavy Investments Provides Entry Point

2023-11-10 13:34:09 ET

Summary

- Graphic Packaging is a leading provider of packaging products for various industries, including food and beverage, consumer goods, and healthcare.

- The company has made significant investments in a new facility. An expensive investment, but one that appears to be necessary thanks to the potential returns.

- The valuation is at historic lows, so 6x EV/EBITDA seems like a great entry point.

Investment Thesis

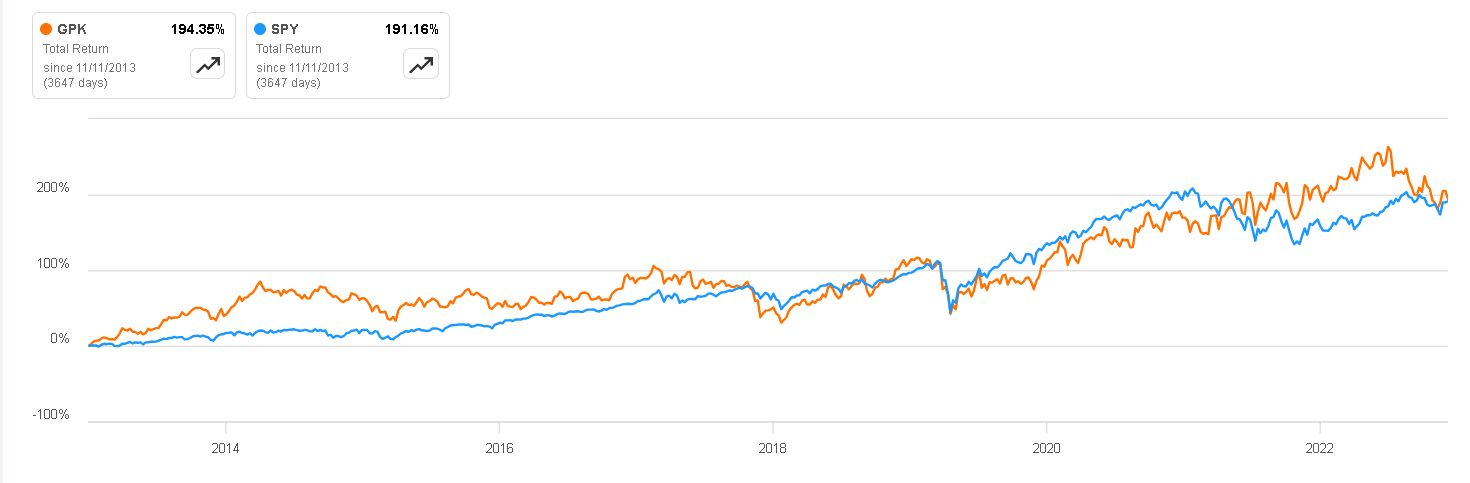

Graphic Packaging ( GPK ) is a business that is unlikely to cause problems to its shareholders. It is a solid business, resistant to crises, and its shares are also relatively less volatile, considering its beta of 0.9.

However, it has fallen 20% from its historical highs, and the current valuation is at levels that have rarely been seen in the past . This situation presents a great opportunity, considering the company's characteristics and the absence of any fundamental problems .

In this article, we will delve into the characteristics of its business model, explore the market trends in which it operates, explain the reasons for its decline, and discuss why I believe the market is overreacting to news, even when they are positive.

{kind=link}

Business Overview

Graphic Packaging is a provider of packaging products for a wide range of consumer products. The company specializes in designing and manufacturing packaging for highly stable industries , such as food and beverage, consumer goods, healthcare, and more.

Among the products manufactured by the company, we can find folding cartons, beverage packaging, paperboard packaging, and flexible packaging solutions. They work with a diverse group of more than 3,000 clients and brands to create packaging that not only protects and contains products but also serves as a means of branding and marketing. So, thanks to its reputation, scale, and vertical integration, we can consider Graphic Packaging as one of the leaders in this stable market.

A Stable and Growing Sector

In the following image, we can see the distribution of their revenues by vertical, as well as some of their clients, which reinforces the point mentioned about the stability of the business and the great reputation within the sector.

{kind=link}

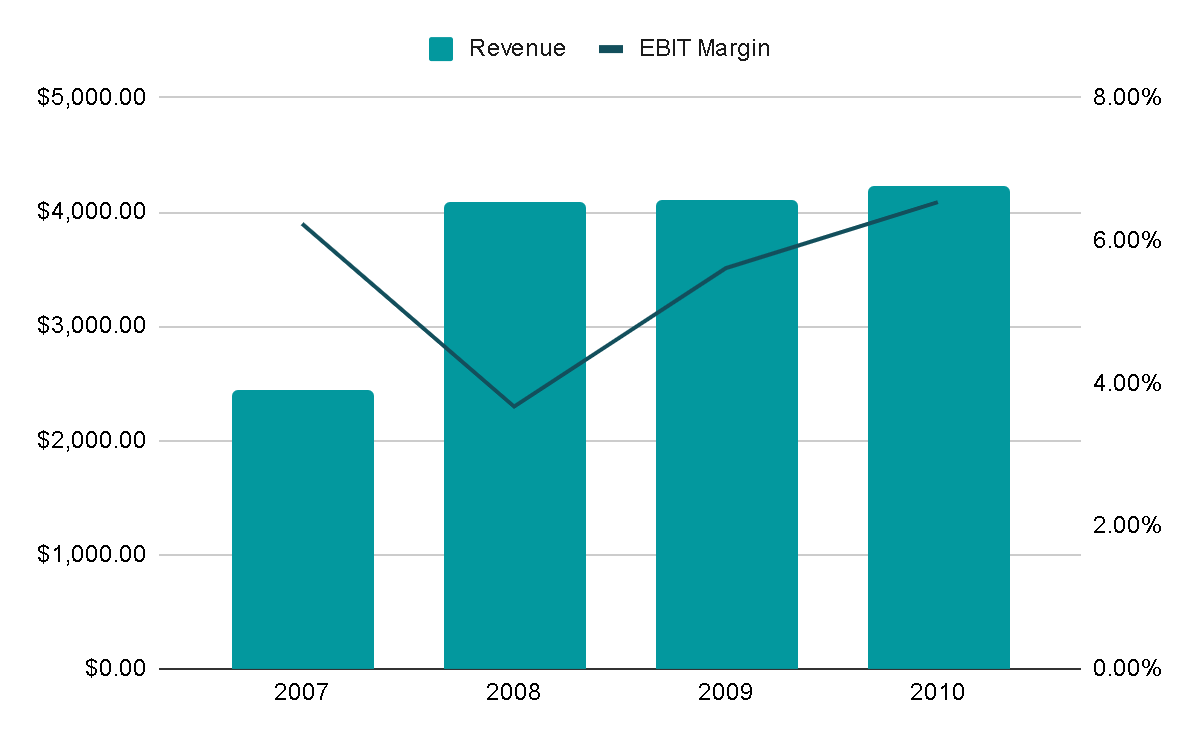

To see this represented with numbers, we can observe the performance of revenues and margins during the 2008 crisis, one of those that most affected American consumption. During FY2009, revenues remained flat, and in FY2010, they grew 2%, while the EBIT margin went from 6.2% in 2007 to 5.6% in 2009.

The explanation for this high resilience lies in two main factors. The first is that GPK's clients operate in very stable industries, such as food, beverage, and healthcare. In addition, GPK's product is also of essential basic use, such as packaging. So in a crisis, the company's customers do not suffer, and therefore, orders are not affected, and revenues are maintained. In fact, since 2007 Revenues have always grown , except in FY2014 and FY2015 when the company made some divestitures in its multi-wall bag and labels segments.

{kind=link}

Not only is the market stable, but it is also in a transition stage towards alternative packaging to plastic, which is not biodegradable and does not leave hazardous waste in the environment. This growth is driven by the concern of society as a whole, supported by governments around the world. That's why there are reports that even expect annual growth of 16% by 2027, growth from which the company could greatly benefit thanks to its Fiber-Based Packaging solutions, which is also a market from which we could expect growth .

Plastic Alternative Forecast (The Business Research Company)

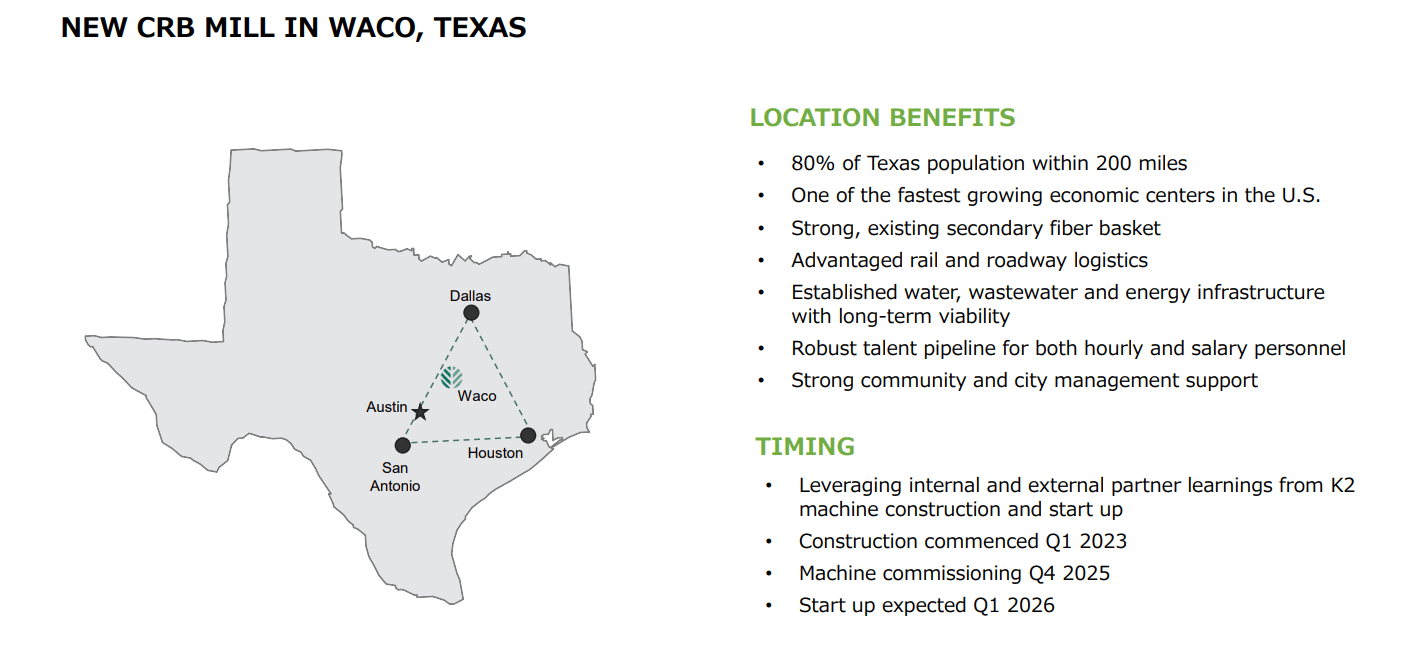

Heavy Investment in Waco

One of the concerns that the market has right now is the large investment of at least $1 billion that the company will be making in a new CRB Mill in the city of Waco, Texas, as Graphic Packaging has recognized that this area is located within the triangle that makes up 80% of the state's population, which consists of cities experiencing significant growth. Establishing a plant in that region would enable the company to supply these four important cities .

Management has already indicated that they plan to finance this investment with the Cash From Operations generated by the company. They also expect to generate returns of 11% on the investment because they will be able to reduce costs through this new strategic location, improve efficiency, and take advantage of the neglected demand in the region. However, the risk is that this is a long-term investment that, if it does not yield the expected returns, could absorb the equivalent of 2 years' worth of Free Cash Flow generated in the last year. Additionally, the plant is not expected to start operating until 2026, and we already know how impatient the market tends to be .

{kind=link}

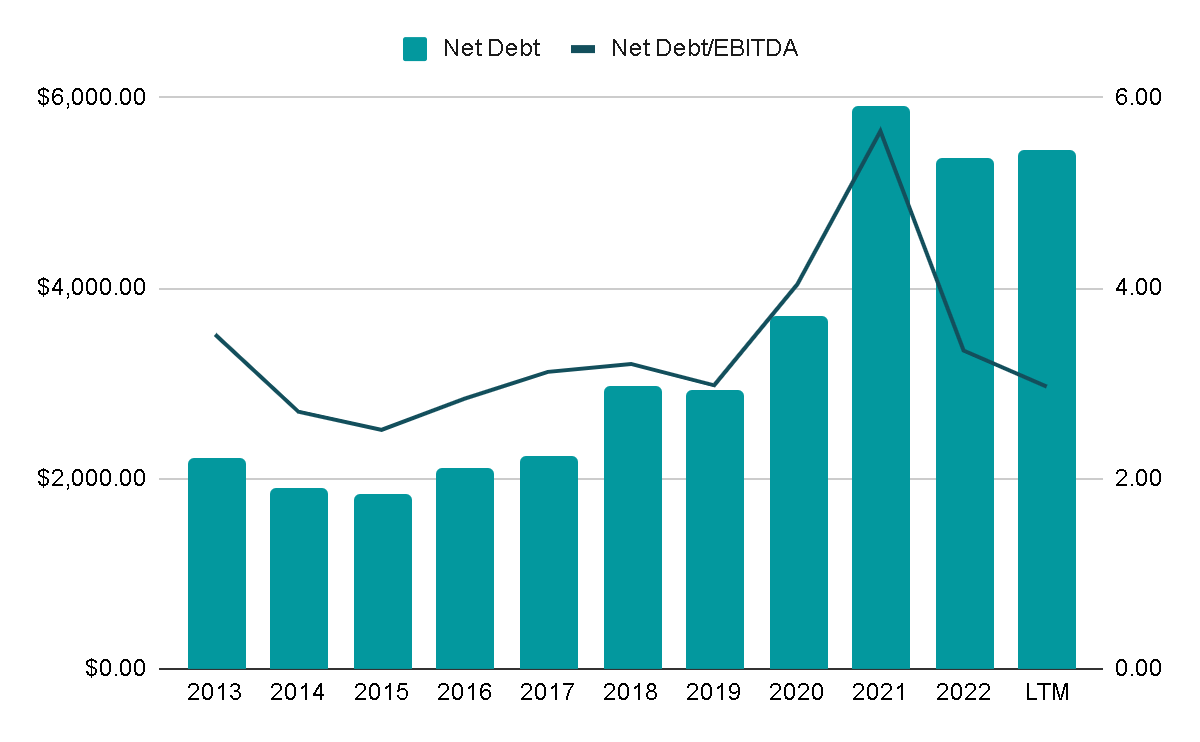

In my opinion, it seems to be a step that the company must take if it wants to capitalize on the significant trend in its business. Furthermore, the fact that this investment is going to be financed without debt is highly positive. With such high-interest rates, profitability could be significantly reduced if, to achieve an ROIC of 11%, GPK had to finance at 5% or 6% rate through debt, or 8% if they issued shares at the current P/FCF of 12. Currently, the Net Debt/EBITDA ratio is around 3x, and in recent years, they have been in a deleveraging process, so the financial position looks good .

{kind=link}

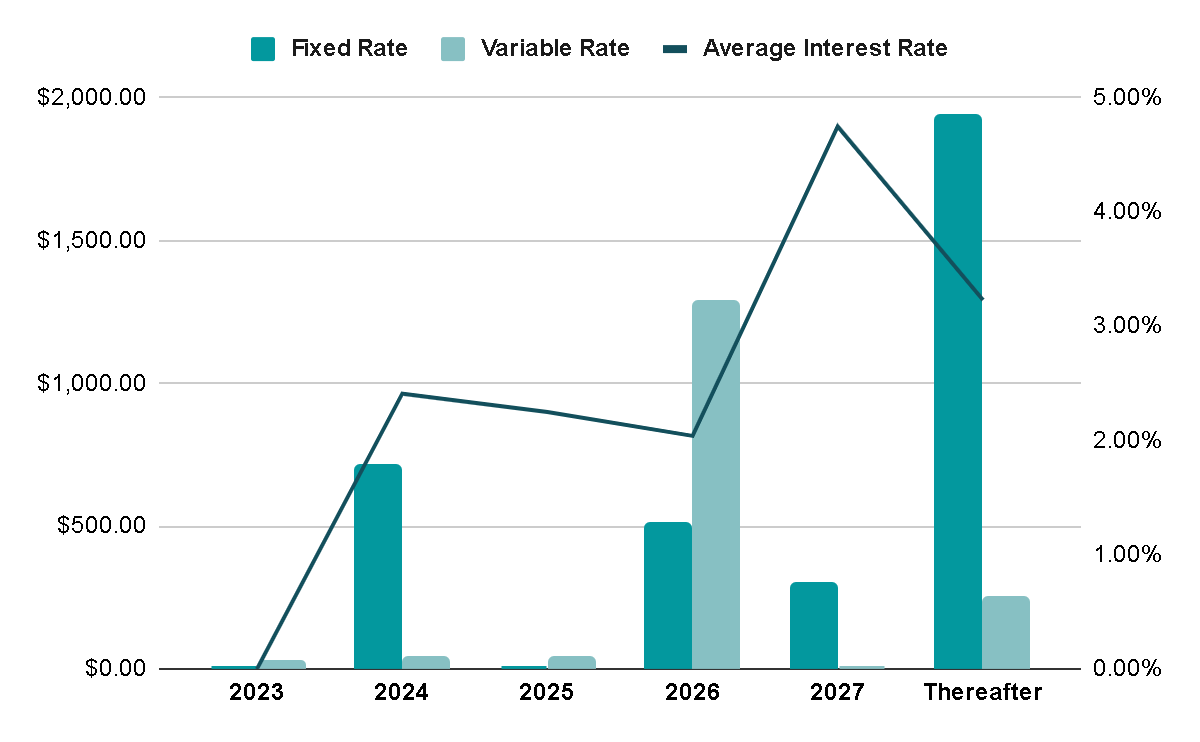

If we delve deeper into the structure of debt , we can observe two things that seem somewhat concerning to me, although not excessively so:

- 15% of the debt matures in 2024, which means they will have to renegotiate at high interest rates that do not seem to be decreasing considerably this or the following year.

- 32% of the debt is at a variable rate, although it could be argued that the highest interest rates have already passed, and during 2024, these should begin to decline. Given its solid business, it should have no problem weathering this until next year.

On the other hand, the average interest rate on fixed-rate debt is 2.45%, which is extremely positive. Additionally, 42% of the debt has maturities exceeding 5 years, which is another favorable aspect.

Although it could be improved, the debt structure is not a problem in the short term, although special attention will have to be paid to what happens in 2024.

{kind=link}

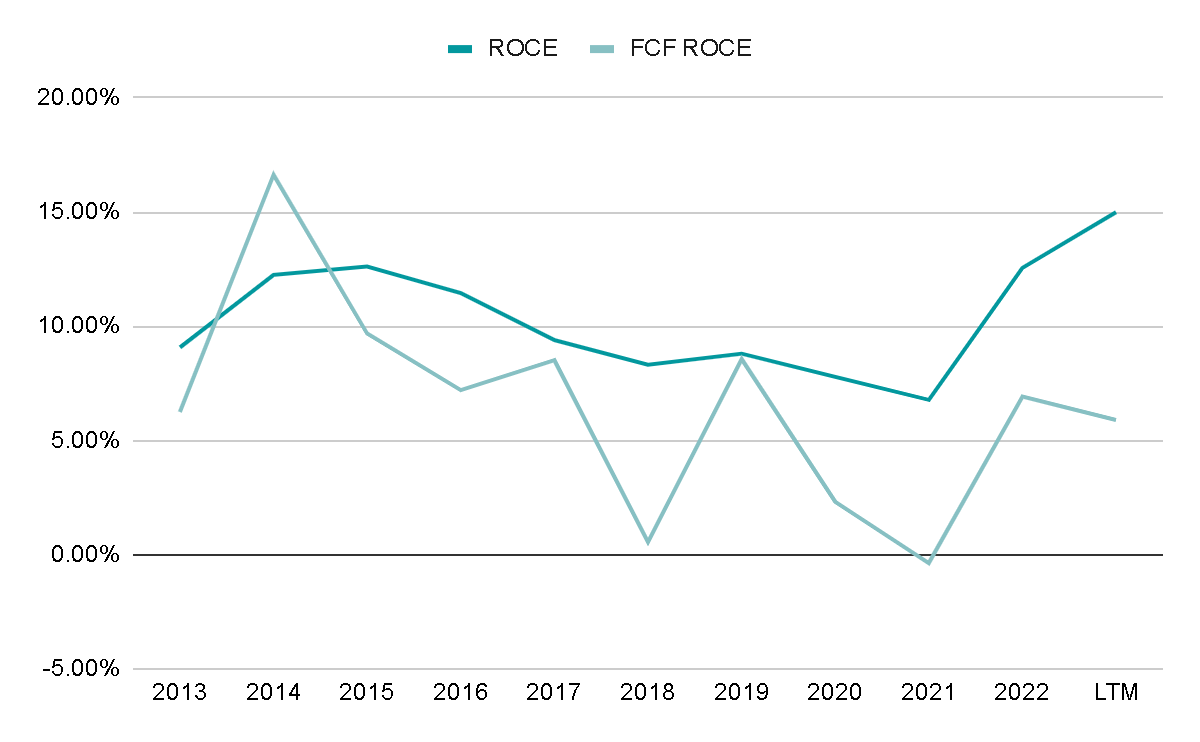

Another aspect is that the company's ROCE is usually around 9% , so if we assume that this investment generates the 11% returns that the management team expects, then it would be an investment that would generate value to shareholders and that is worth taking the risk to do it

{kind=link}

Valuation

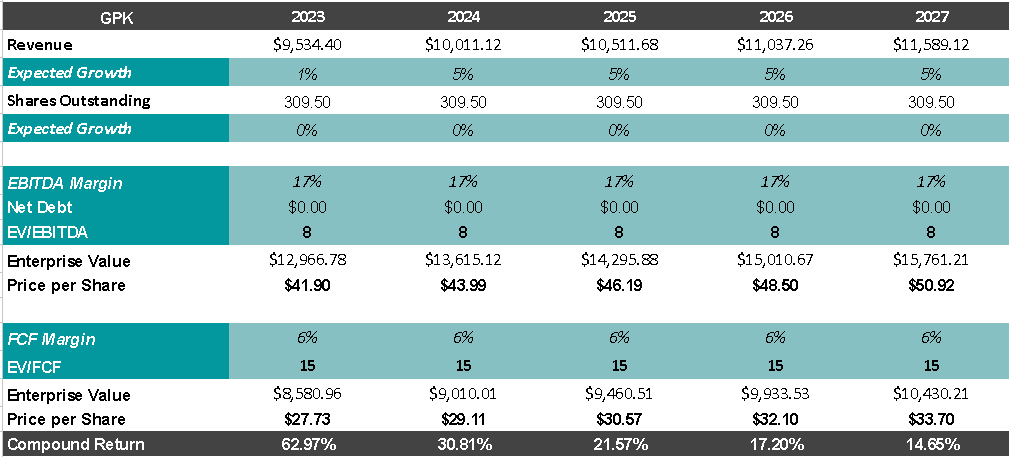

The company has grown its revenues by 32% in the last year, thanks to the benefits obtained from an extremely atypical environment where consumer prices continued to rise, while raw materials were in deflation. Therefore, a 1% growth for FY2023 seems even healthy because it represents an 11.5% CAGR over the last 5 years.

From there, I estimate that the company will be able to grow at the 5% rate it has historically achieved, partly due to volume and partly due to its great capacity to raise prices at a rate equal to or greater than inflation. Additionally, it will maintain average margins of 17% EBITDA and 6% FCF.

If we apply exit multiples of EV/EBITDA of 8x and EV/FCF of 15x, we could expect an annualized return of 14.5% from the current price, which would be even higher than 16% if we assume that the current dividend yield of 1.85% remains.

{kind=link}

Final Thoughts

The business model seems stable, and, above all, it has tailwinds to continue growing sustainably for many years. Hence, the importance of the company taking the lead and deciding to invest in strategic areas, which I applaud and believe will add value to its shareholders in the long term.

Furthermore, if we look at the valuation from an EV/EBITDA point of view, the company seems to present a historic opportunity . Since 2003, it has only once reached valuations as low as the current ones, and not even in 2008 or 2020 did it reach the current EV/EBITDA ratio of 6.6x.

Considering the quality of the business and the attractive valuation, I believe it deserves a ' buy ' rating.

{kind=link}

For further details see:

Graphic Packaging: Fear Over Heavy Investments Provides Entry Point