GPK - Graphic Packaging: Strong Free Cash Flow With A Low P/E But Bearish Momentum (Rating Downgrade)

2023-09-06 17:26:29 ET

Summary

- Materials sector faces headwinds from a stronger US dollar, increasing oil prices, and higher interest rates.

- Graphic Packaging downgraded from buy to hold due to macro forces and technical weaknesses.

- GPK has a compelling valuation but faces challenges in the food and beverage category and volatility in raw material prices.

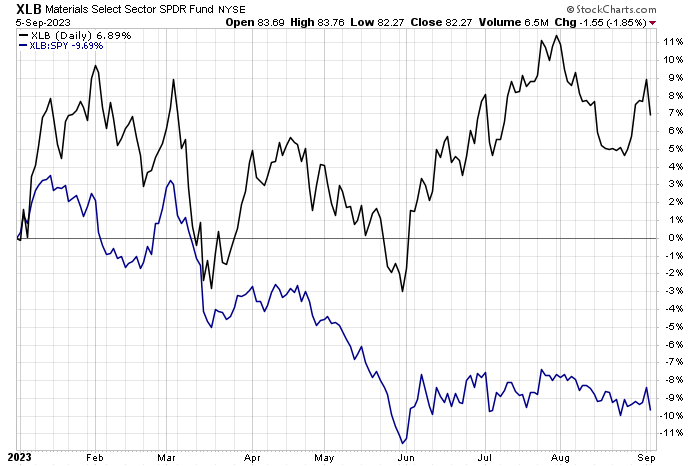

There are many headwinds facing the cyclical Materials sector right now. While economic growth continues to hold up well, a stronger US dollar, increasing oil prices, and higher interest rates all cast clouds on firms conducting business around the world. The Materials Select Sector SPDR Fund ( XLB ) endured one of its worst days of the year this past Tuesday due to those macro factors. Bigger picture, XLB is underperforming SPY by nearly 10 percentage points in 2023.

I am downgrading shares of Graphic Packaging ( GPK ) from a buy to a hold, though I still see the valuation as attractive. Macro forces and technical weakness are too much to overcome in this case.

Material Weakness in Materials Sector Relative Price Action

{kind=link}

According to the company, Graphic Packaging Holding Company is a leading provider of sustainable fiber-based packaging solutions to the world's most widely recognized food, beverage, food service, and other consumer products companies and brands. The Company operates on a global basis, is one of the largest producers of folding cartons and fiber-based food service products in the United States and Europe, and holds leading market positions in coated recycled paperboard, coated unbleached kraft paperboard, and solid bleached sulfate paperboard.

The Atlanta-based $6.7 billion market cap Containers & Packaging industry company within the Materials sector trades at a low 9.6 trailing 12-month GAAP price-to-earnings ratio and pays a near-market 1.8% dividend yield. Ahead of earnings next month, the stock has a modest 20% implied volatility percentage, and its short interest is material at 4.1%.

Back in early August, GPK reported somewhat weaker-than-expected Q2 results. Operating earnings per share verified at $0.66, below the consensus estimate, while top-line results also fell short of what analysts were anticipating. Adjusted EBITDA came in at $453 million, slightly below the Street's estimate of $482 million. A 4% year-on-year drop in organic sales was a sore spot, though it was offset somewhat by increased pricing.

On the positive side, the firm’s net debt decreased by $25 million for Q2, resulting in a net leverage ratio of 3.0. The company also announced an additional $500 million in share repurchase authorization. The management team reiterated its full-year 2023 adjusted EBITDA of $1.8 billion to $2 billion and adjusted EPS in the range of $2.70 to $3.10, though organic sales growth is seen in the 0% to –2% range.

Key risks include challenges related to the acquisition of Bell Incorporated, unease in the food and beverage category among other end markets, and volatility in raw materials prices like fiber and energy. At a higher level, trade tensions between nations could adversely affect the company’s international footprint.

On valuation , analysts see earnings surging by more than 20% this year before dipping into the single digits over the out years. Dividends are steady at $0.40 per share annually and the stock trades at attractive earnings multiples today after a shaky profitability history from 2020 through much of last year. With an EV/EBITDA ratio that is significantly under the average of the broader market, GPK features solid free cash flow, summing to $1.69 over the past 12 months – a 7.7% FCF yield.

Graphic Packaging: Earnings, Valuation, Growth Outlooks

Seeking Alpha

GPK has historically traded with a low-teens forward non-GAAP price-to-earnings ratio. If we assign this P/E and assume next-12-month EPS of $2.90, then the stock would be in the high $30s. Unfortunately, the growth outlook asserts a slightly more modest earnings multiple given the below-market EPS growth rate. Let’s tone down the P/E to 11 – we still have a very undervalued stock with an intrinsic value in the low $30s. That is up from my high-$20s estimate from earlier this year as profitability has been solid in 2023 so far.

GPK: Very Compelling Valuation Metrics

Seeking Alpha

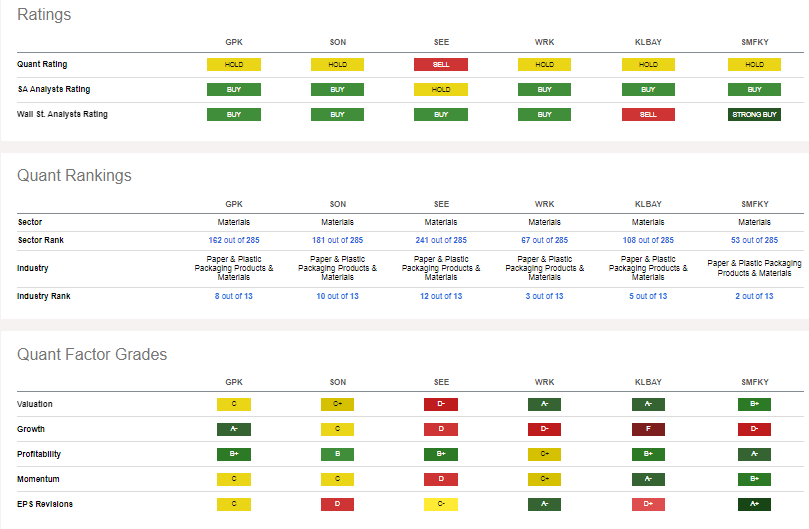

Compared to its peers , GPK features a middle-of-the-road valuation, but it actually sports a healthier growth projection, though that is likely due to robust near-term trends, rather than impressive terminal growth rates. But there’s little doubt that this Materials sector name has strong profitability even as EPS revisions waver.

Competitor Analysis

{kind=link}

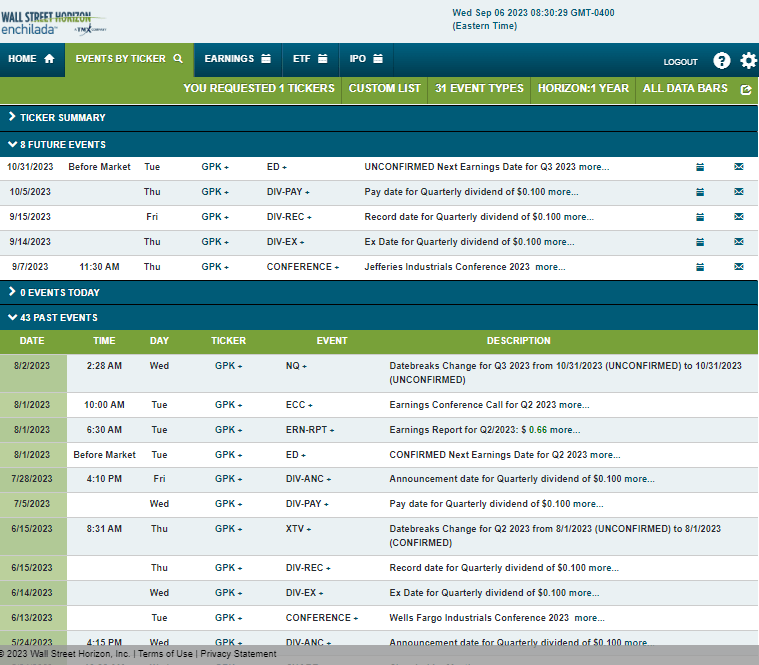

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q3 2023 earnings date of Tuesday, October 31. Before that, shares trade ex-dividend on September 14. There could be volatility in the near term as the firm’s management team is slated to present at the Jefferies Industrials Conference 2023 which takes place from September 6-7.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

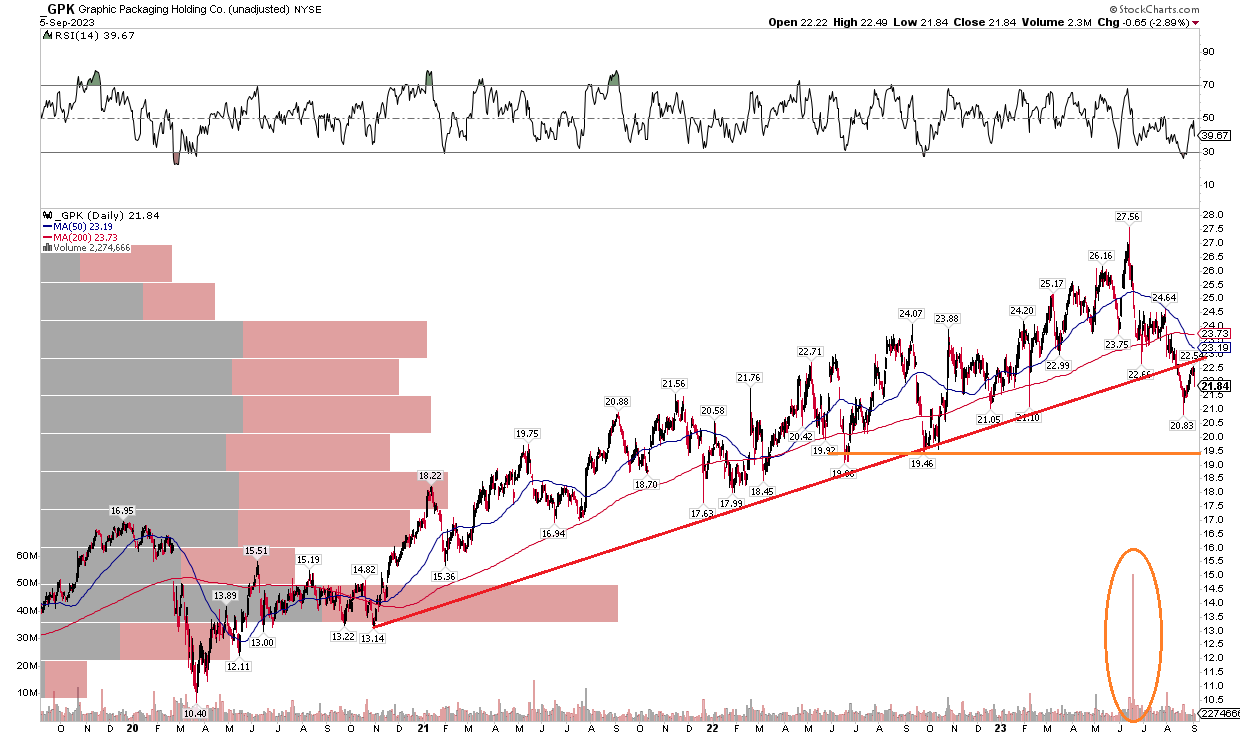

GPK rallied some 20% after I initiated coverage in January, but shares have taken on water in recent weeks. Notice in the chart below that shares plunged from above $27 to a low just above $20 last month. A modest bounce to start September stalled as the 50-day moving average crossed below the long-term 200-day moving average for the first time (with gusto) in about three years. So, the trend has clearly reversed, and that is made all the clearer given a flattening out of the 200dma.

Of course, the clear pattern even novice chartists see is the trendline break. An uptrend really gained steam at the March 2020 lows, and a series of higher highs and higher lows took place all the way through June of this year before a high-volume selloff occurred. I see the risk of a bearish trend reversal as being high despite the favorable valuation. Support is seen in the $19 to $919.50 range with longer-term support in the high $16s as I outlined in the previous article. Selling pressure may be seen on rallies to the 200-day MA.

GPK: Bearish Trend Reversal, Eyeing Sub-$20 Support, But the Dip

{kind=link}

The Bottom Line

I am downgrading GPK from a buy to a hold. I very much like the valuation, but the technical trend change and weak share-price momentum are too much to overcome right now. I would look to buy a dip toward $19.50.

For further details see:

Graphic Packaging: Strong Free Cash Flow With A Low P/E, But Bearish Momentum (Rating Downgrade)