GRPH - Graphite Bio: Reverse Merger Leading Into Big Special Dividend And Q2 Phase 3 Trial

2023-12-25 05:22:26 ET

Summary

- Graphite Bio announces a reverse merger with LENZ Therapeutics, with GRPH shareholders receiving a $60 million dividend.

- Graphite Bio stockholders are expected to own 35% of the combined company before the PIPE financing.

- The combined company is expected to have approximately $225 million in cash and will focus on advancing LENZ's lead programs for the treatment of presbyopia.

Graphite Bio ( GRPH ) is left with no viable project and $230 million in cash or equivalents vs ~$60 million in liabilities (mostly operating leases). Its market cap is $160 million, a restructuring announcement, and potential cost cuts left a lot of meat on the bone, and with activists present on the shareholder list, I expected something could happen. I expected to see some JNCE-type of deal where shareholders would receive a premium of ~30%-50% to the share price with or without a CVR or contingent value right. I expected this to occur sooner rather than later (i.e. 2nd or 3rd quarter).

With sufficient cost-cutting, the company could end up in a relatively balanced situation because money market yields are quite strong and the securities/cash portfolio is quite large. In the first restructuring plan dating back to February 2023, the company terminated 50% of its workforce. In August 2023 it started to implement a 2nd restructuring plan and reduced its workforce by a further 33%.

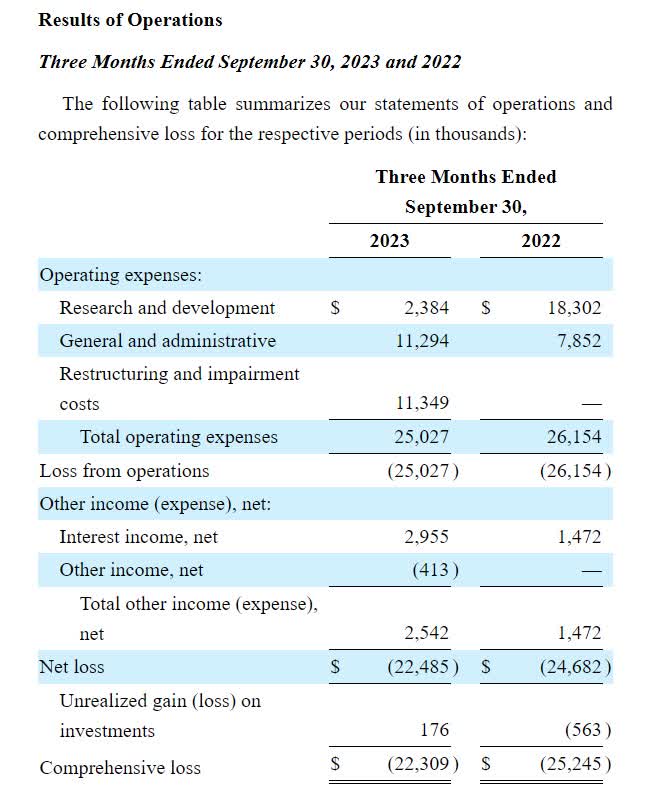

At the end of September 2023, the company was still burning through $22 million per quarter. I expect this to decrease further because restructuring expenses should come down as well R&D and G&A as the benefits of the 2nd restructuring plan fully come through. The company also entered into several sub-lease agreements post the reporting period, although these only cover part of their space.

{kind=link}

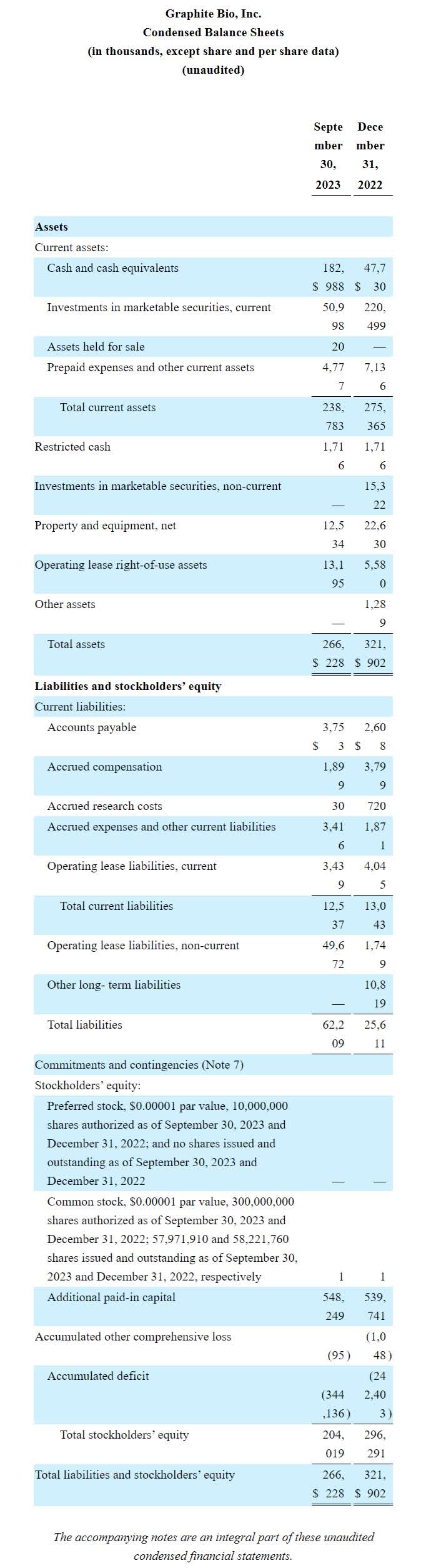

The balance sheet is fairly simple. On the asset side, what matters are the cash and marketable securities. All of the liabilities matter and add up to $62 million, most of which consists of lease obligations.

{kind=link}

The company expects to have sufficient liquidity to last another 12 months without much of any revenue, except for interest income. The exact burn rate, and cost-cutting programs, aren't as crucial anymore because on November 15, the company announced a reverse merger. In my experience, these tend to be subpar outcomes for restructuring failed biotechs. But not everything is lost.

For starters, in the deal, GRPH shareholders are getting a $60 million dividend. That's 45% of the current market cap. Then on a pre-merger basis, Graphite Bio stockholders are expected to own approximately 35% of the combined company and pre-merger LENZ Therapeutics stockholders are expected to own about 65% of the combined company upon the closing of the merger prior to the additional PIPE financing transaction.

With the cash from both companies (likely ~$115 million from GRPH) and the proceeds of the concurrent PIPE financing, the combined company is expected to have approximately $225 million of cash or cash equivalents. Graphite Bio is expected to contribute $115 million to the combined entity

When the deal closes Versant Ventures, RA Capital Management, Alpha Wave Global, Point72, Samsara BioCapital, Sectoral Asset Management, RTW Investments will all be key shareholders and have the company show up on their 13-f's. This could put the company on the radar of other healthcare investors.

The goal of the combined company will be to have a public vehicle for LENZ’s lead programs. These are called LNZ100 and LNZ101. These are presbyopia treatments and the company has a phase 3 trial going. The shareholders and company will probably be looking to get acquired after a positive phase 3 trial or raise money in the public market to fund a rollout of their products.

Presbyopia is a condition where the lens of the eye loses flexibility. This makes it harder to focus on nearby objects, to read, and to see small things. Presbyopia typically develops around age 40 and often worsens over time.

If the phase 3 trial is successful, the company will have a once-daily eye drop that fixes presbyopia for 8 hours or so. LENZ believes this can become a $3 billion product. The myopia and presbyopia market size is estimated to be $17.44 billion in 2022 and to grow at a CAGR of 8.8% up to 2030. I would take these figures with a grain of salt, but I do buy into the notion that it is likely a strong growth market and the addressable market is large.

If the company demonstrates solid growth after approval, the company would get awarded an enormous multiple given the total addressable market. If it were to end up trading at just 1x sales, that's a $3 billion+ valuation, while this deal today is executed at an implied valuation below $400 million. There's a long way to go because the product isn't approved yet (and could fail), and there are obviously no sales yet.

From the perspective of Graphite Bio shareholders, the $60 million dividend is a win. This represents almost 50% of the current market cap. Afterward, GRPH holders are still left with a stake in a publicly traded biotech with a phase 3 trial readout upcoming. You would think the parties are fairly confident about that readout; otherwise, why would you pursue a stock market listing (via reverse merger, no less) while biotech is massacred? This recently changed, but at the time of the deal, biotech was still doing awful:

Note that another $50 million is coming into the combined company via the PIPE financing by existing LENZ shareholders and new shareholders. I estimate that the stake gets these shareholders 13%. That would mean GRPH shareholders are ending up with around 30.5%. The capital raised indicates a valuation of around $370 million for the combined company. This suggests the GRPH stake would be worth $112.85 million.

This means the fair value of the Graphite Bio stake (if the market were to accept the LENZ valuation) would be around $172.85 million. That's approximately 27% more than the current market cap. At the end of the day, I think this is a hold. I'd like to capture the dividend and think there's a reasonable chance the market will be interested in a phase 3 trial, with a strong shareholder list, that could read out in Q2 and has a large addressable market.

For further details see:

Graphite Bio: Reverse Merger Leading Into Big Special Dividend And Q2 Phase 3 Trial