GUNGF - Gravity: A Benjamin Graham Net Cash Pick

Summary

- Gravity is a leading online game maker in Asia, with rising cash holdings approaching the total market capitalization of share ownership.

- Solid income levels and a stable future are completely mispriced today, in my view.

- A variety of options exist for the cash to support its stock price and grow the company in a 2023 recession scenario.

- Much stronger accumulation patterns in January may hint at an upturn in the share quote soon.

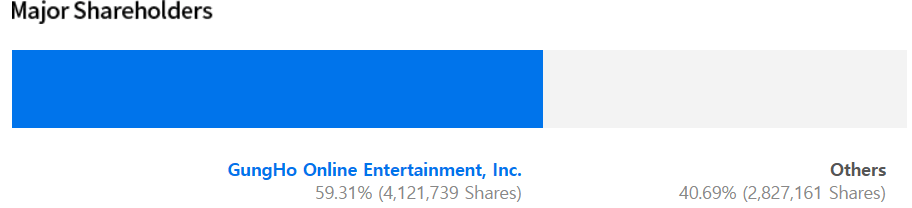

Gravity Co., Ltd. ( GRVY ) is a South Korean gaming company 59% owned by GungHo Online Entertainment ( OTCPK:GUNGF ) in Japan, with institutions and the general public owning the other 41% of shares. Its claim to fame, Ragnarok Online just celebrated its 20th anniversary, launched in Korea on August 1st, 2002.

Company Website - Shareholder Ownership GungHo Website - Gravity, Ragnarok Update, September 2022 Quarter GungHo Website - Gravity, Ragnarok Update, September 2022 Quarter GungHo Website - Gravity, Ragnarok Update, September 2022 Quarter

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Cash Hoarding

Gravity has been a real beneficiary of the COVID pandemic with its focus on Asian markets. Residents of this region have experiencing extra lockdowns vs. the American reaction, being forced to spend more time at home. One entertainment outlet has been gaming, which pushed company sales and profitability to records in 2020-21. Management has not been very aggressive expanding into or purchasing new unrelated titles, although a number of them are on the market with varying success. Instead, the company has kept cash coming in the door in a neat pile that has grown quite large.

Cash is held in the South Korean won (KRW), which could provide a smart hedge against a declining dollar over time (my personal forecast). Converted at the end of September (at a rate less desirable than current conversions), the equivalent U.S. dollar cash stash was $205 million four months ago. This sum measured quite favorably against just $66 million in total liabilities holding zero debt. Net working capital grew $40 million (mostly from cash increases) vs. the end of 2021.

From both the effects of rising cash levels and a declining stock price, enterprise value calculations have shrunk from US$1.1 billion in 2021 at the peak valuation for stay-at-home entertainment names during the pandemic to around $120 million in late 2022 and early 2023.

YCharts - Gravity, Market Cap vs. Cash, Enterprise Value, 10 Years

The fascinating part of the investment story, opening a unique Ben Graham-like opportunity, is the company has been approaching a net business valuation near "zero" despite record profits. If you are looking for a limited downside pick (under normal political and tax circumstances in South Korea and Japan), with a high “margin of safety” for underlying valuations, Gravity is a top choice right now.

Below I have charted the insanely low enterprise value vs. gaming competitors and peers. This list includes Activision Blizzard ( ATVI ), Electronic Arts ( EA ), Take-Two ( TTWO ), Skillz ( SKLZ ), DoubleDown Interactive ( DDI ), Roblox ( RBLX ), Nintendo ( OTCPK:NTDOF ), and NetEase (NTES).

YCharts - Gaming Industry, Enterprise Values, 3 Years

You will notice Gravity’s lowballed business value, after subtracting its cash stash, is the same as smaller companies actually losing money on an operating basis. In contrast, Gravity earned $35 million over the trailing 12 months. Does it make sense for a company with $200+ million in cash and no debt, with sizable profitability, to be valued as if it is going out of business? The answer is absolutely not, which is my reason for writing this article.

YCharts - Gaming Industry, Final Income Margins, 3 Years

Undervaluation Stats

Reviewing valuations for the gaming peer group on book value alone, price is incredibly low at 1.5x this data point. Again, it is hovering around the same multiple as three other businesses operating at large losses for owners.

YCharts - Gaming Industry, Price to Book Value, 1 Year

When we subtract the cash (not needed to run the business) and look at EV multiples, you can really see the bargain setup for investors. EV to revenues of 0.38x is essentially the lowest of the group pictured, priced similarly to the two with the worst income generation. The average ratio of the subset actually delivering operating earnings is 5x! So, you could argue Gravity is selling for a 90%+ discount ratio on sales, assuming game demand by consumers does not implode in 2023. Most of the analyst arguments I have read, explain the logical outlook for somewhat lower sales in 2023-24, but not a total collapse. Seeking Alpha contributor Valkyrie Trading Society made this case in January here .

YCharts - Gaming Industry, EV to Revenues, 1 Year

On EV to EBITDA there is no comparison for the valuation between Gravity and peers. A multiple of 1.7x is nowhere near the 14x average from the companies generating basic apples-to--apples cash flow.

YCharts - Gaming Industry, EV to EBITDA, 1 Year

EV to earnings is today at a 5-year low for the company at 3x. Basically, at today’s $35 to $40 million rate in annual after-tax profits, a single owner (if you purchased the whole company and ran it is a private enterprise) would theoretically be getting the company’s operating future past 2026 for free at $48 per share.

YCharts - Gaming Industry, EV to Earnings, 3 Years

Improving Technical Momentum

Another characteristic arguing in favor of ownership is other investors appear to be buying shares since late summer. While Gravity's 1-year share total return performance chart is highlighting relatively average change vs. the peer gaming group, underlying momentum indicators have been perking up.

YCharts - Gaming Industry, Total Investment Returns, 1 Year

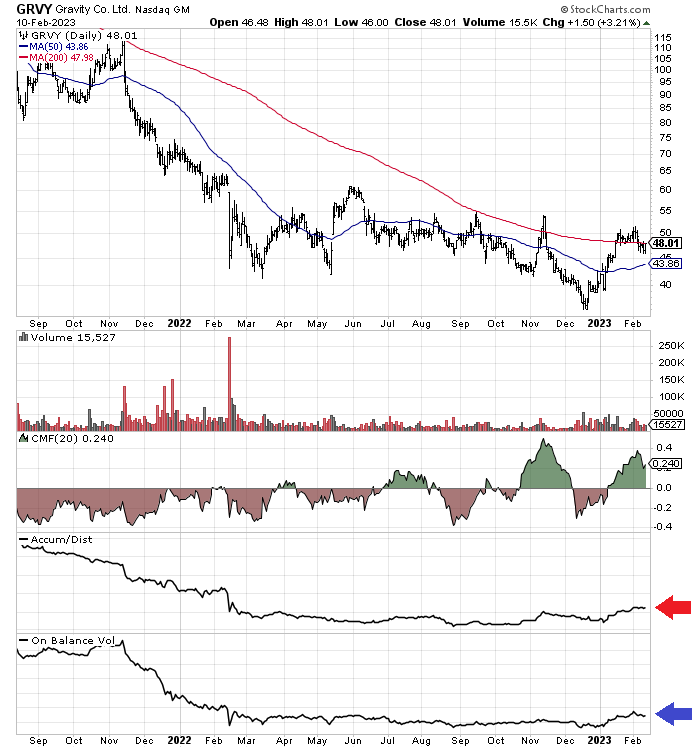

On the 18-month of daily price and volume trading below, the first thing to recognize is price has been trying to move back above its 200-day moving average of late. At $48, the quote is trading right at this important trend creation, while it has already bested the shorter-term 50-day MA. Any further upside beyond $52 may prove a breakout situation.

In addition, the 20-day Chaikin Money Flow has been increasingly positive, after sitting in negative territory consistently over the first year of the chart into July. From October, lower volume buying has been able to support nice price gains, which is a different formula for success than early 2022. To me it signals overhead selling and share supply is fading.

Lastly, the Negative Volume Index (marked with red arrow) and On Balance Volume (blue arrow) performed strongly in January, both reaching their highest net level since February 2022. The change in behavior from straight down patterns a year ago is what I like best.

StockCharts.com - Gravity, 18 Months of Daily Price & Volume Changes, Author Reference Points

{kind=link}

Final Thoughts

Gravity reminds me a little of King World , the producer and syndicator of popular television shows in the 1990s and beyond. Titles from talk-show queen Oprah to game shows like Wheel of Fortune and Jeopardy! were the staples generating mountains of cash. King World paid off all its debt and accumulated cash yearly before it was eventually acquired by CBS in 1999. Of course, there were dips in price along the way, but steady 10% to 15% annualized returns were the end result for long-term shareholders.

Gravity is kind of unique in early 2023 holding both a large cash position and a super-low valuation on the operating business. Real financial flexibility and a conservative internal funding source are byproducts of the cash. For example, parent GungHo could spend down the existing liquidity to buy back shares and achieve total 100% ownership over time, if it wanted. Gravity could “purchase” outside gaming assets to bring accretive growth without the use of debt or equity issuance. Perhaps, management will decide to pay a huge special dividend to shareholders. There are a variety of positive options to drive underlying business worth (other companies do not have), especially if a deep recession hits.

What’s the downside risk? However you slice it, you cannot argue Gravity is overvalued at a market of $325 million, with $35 million for yearly EPS and $205 million in cash at the bank. Sure, GungHo could make an unfair, low bid around the current quote to purchase the other 41% of Gravity not already owned. But, why not just use the cash on hand to slowly buy out minority owners?

The gaming market could slide globally in a recession, or consumers may become bored with its main Ragnarok product title. Both have decent odds, potentially lowering sales and profit levels in 2023 vs. 2022. Yet, I doubt the company will net-net lose money from operations anytime soon.

The stock quote of $48 is the same as early 2018 (five years ago), despite a jump in cash on the balance sheet from $50 to $205 million. The outstanding share count hasn’t changed; the operating business and margins are effectively the same; and the long-term outlook for the gaming industry remains as bright as ever.

YCharts - Gravity, 5-Year Chart of Price

Using my King World analogy, I have a bullish but muted forecast for the share quote. I peg worst-case scenario downside to $40 per share (-15% loss), which would roughly equal rising cash levels, assuming the company remains profitable. Upside potential over the next 12 months is in the $65-$70 range (+35% to +40% gain) for a best-case scenario, depending on future sales and income growth, on top of a possible slide in the U.S. dollar’s exchange rate vs. the South Korean won. Modeling $50 to $55 (slight 5% to 15% for total returns) is my baseline forecast for yearend 2023. Part of my projection includes a lower S&P 500 price and at least a mild recession this year. Given both outcomes, steady gains from Gravity would create solid "outperformance" vs. most Wall Street alternatives.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Gravity: A Benjamin Graham Net Cash Pick