GUNGF - Gravity: Overlooked And Undervalued

2023-11-21 10:27:37 ET

Summary

- Gravity Co., Ltd. is a developer and distributor of online and mobile video games based in South Korea.

- The company is far from perfect, and has multiple risks worth considering and monitoring.

- Despite the flaws of the company, the valuation is extremely compelling.

Editor's note: Seeking Alpha is proud to welcome Frederick Wittmann as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Although rare, the market occasionally presents investment opportunities to the patient investor that are simply too cheap to ignore. These investments can sometimes be priced so low that they act like a coiled spring - with the slightest change in investor sentiment causing a sudden and drastic unraveling of suppressed value. I believe Gravity Co. (GRVY), while not without its blemishes, has the potential to be one of these opportunities.

Business Summary

Gravity is a developer and distributor of online and mobile video games headquartered in Seoul, South Korea. Originally established in April of 2000, the company really gained notoriety with the release of its staple game, Ragnarok Online , in September, 2002. Ragnarok Online is an MMORPG (Massively Multiplayer Online Role-Playing Game) for the personal computer ((PC)) market which, since 2002, has provided a sizeable chunk of the company's cash flow and created their tenaciously popular Ragnarok brand. As of the end of 2022, the Ragnarok Online game still generates approximately 19% of overall revenues for the company.

Starting in 2017, GRVY broke into the mobile gaming world with the release of the game Ragnarok M. Eternal Love in Taiwan - an MMORPG game built for mobile platforms. The game was promptly released in other geographic areas such as South East Asia, Europe/Russia, The USA and Japan. Starting in 2020, two more MMORPG mobile games, Ragnarok Origin and Ragnarok X: Next Generation , were also introduced for mobile platforms - creating fresh streams of revenue for the company.

Revenue Breakdown

GRVY makes most of its money via microtransactions, or in-game purchases, as well as royalty/licensing fees where third-party licensees operate the game. The company's major markets are Taiwan, Thailand, Korea, USA/Canada, Japan, Philippines, Hong Kong, and Malaysia.

Right off the bat, there are two important things I believe prospective investors should acknowledge about GRVY's revenue:

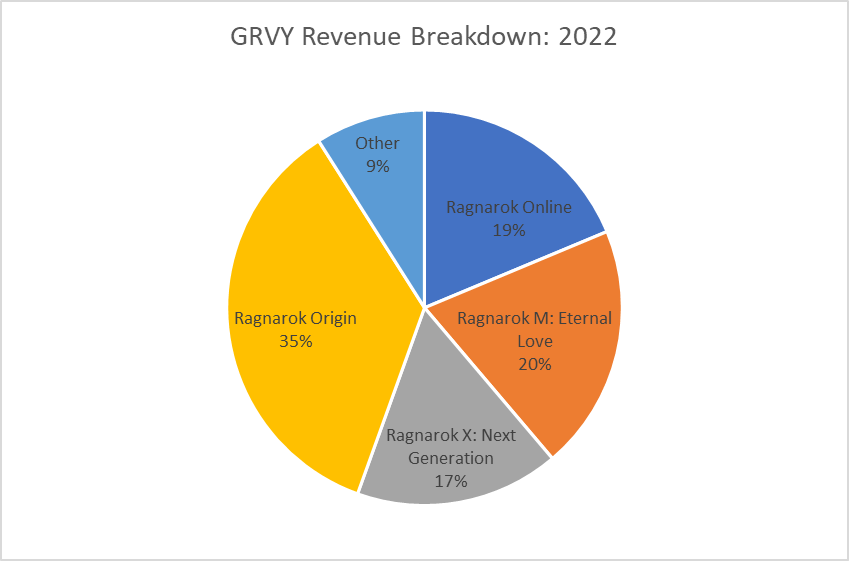

First and foremost is GRVY's almost sole reliance on the Ragnarok IP. This is clearly evident from the revenue breakdown taken from the company's most recent annual report (FY 2022):

GRVY Revenue Breakdown FY 2022 (GRVY FY 2022 Annual Report)

{kind=link}

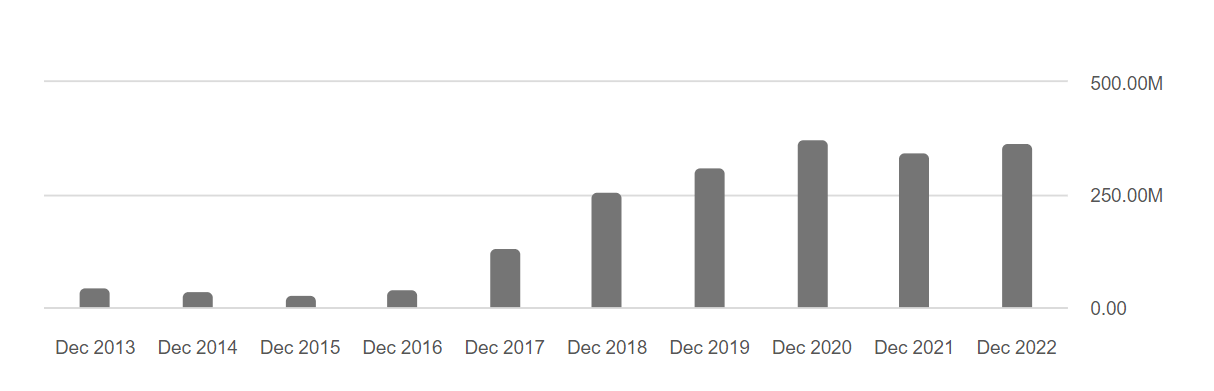

Secondly, when looking at the consolidated income statement , it is immediately noticeable that GRVY's revenue experienced a significant and sustained rise starting in 2017, as seen below ($):

GRVY Revenue 2013 - 2022 (Seeking Alpha)

{kind=link}

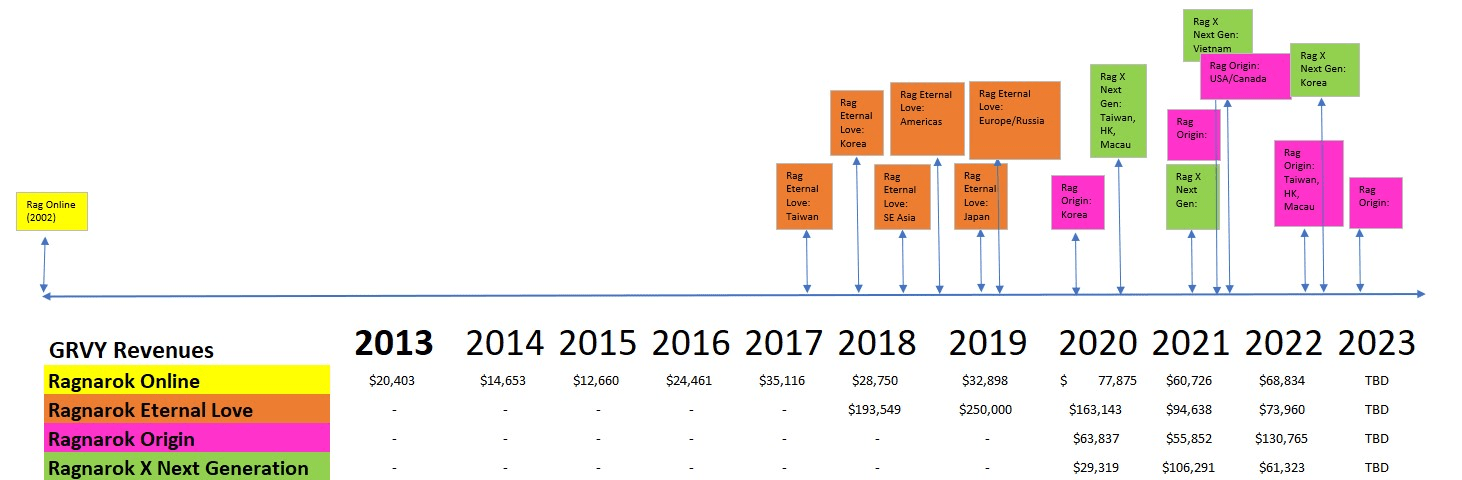

The rise in revenue (and in turn profits and cash flows) in 2017 can be explained by the entry into the mobile gaming space with the launch of Ragnarok M: Eternal Love and subsequent mobile titles mentioned in the first section. While the revenue growth since 2017 has proved sustainable, it should be noted that revenues generated from the mobile gaming market are inherently lumpy. The below timeline of Ragnarok releases and respective revenue generation illustrates this point quite well:

Ragnarok IP Revenues 2013 - 2022 (GRVY FY 2022 Annual Report)

{kind=link}

As an example, in 2018, Ragnarok M: Eternal Love's first full year after release generated $193 million worth of revenue for the company, subsequently peaking at $250 million in 2019 and sinking down to $73.96 million in 2022. The lumpiness of revenue can be explained simply from a statement taken from the company's 2022 annual report:

" the life cycle of a mobile game is relatively short and generally lasts from six to twenty-four months while reaching its peak popularity within the first three months of its introduction, though it varies by genre."

Risks

The above section provides a solid basis for transitioning our discussion to the company's risks:

Firstly, what I believe to be the most obvious risk, is the overreliance, or 'milking', of the Ragnarok brand. Despite having various games outside of the Ragnarok IP, such as mobile games Whale in the High and NBA RISE TO STARDOM , or the newly released game for console, Wetory ; none of these games have generated significant sources of revenue/income for the company. It is therefore reasonable to disregard them when having serious discussions about GRVY.

While overreliance on Ragnarok is indeed a risk that must be considered, it appears that so far GRVY's ability to leverage this brand has been monetarily successful - as is evident by their robust financials. Additionally, a good way to gauge the value of a company's brand is to analyze the return on invested capital ((ROIC)) achieved in recent years. This is particularly apt for GRVY due to their almost sole reliance on the Ragnarok brand. According to Morningstar , GRVY has achieved an average ROIC of 38.2% over the past five years - significantly better than the index mean of 7.67%. This can be viewed as confirmation of the value of the Ragnarok IP in the gaming world.

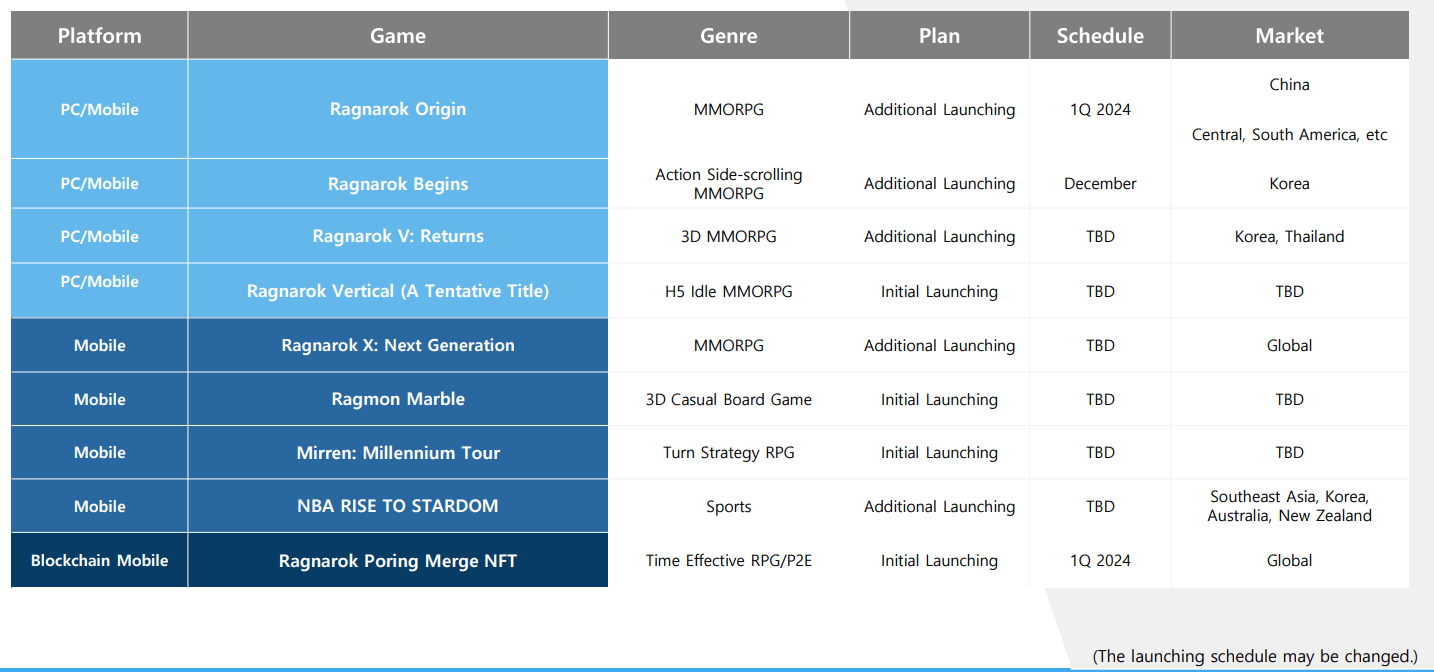

The second risk is the lumpiness of revenues, or the short life cycle of mobile games. So far, GRVY has mitigated any meaningful dips in revenue by constantly releasing new Ragnarok games in a variety of geographic markets. To illustrate, below is the current pipeline of releases slated for 2023 and 2024 taken from their 2023 3Q earnings report :

GRVY Release Pipeline 2023 - 2024 (GRVY 2023 3Q Earnings Presentation)

{kind=link}

While the company has been successful in sustaining revenue since their entry into the mobile market in 2017, I believe it is imperative that they continue to update and release games across their markets to offset any drawdowns caused by short mobile game life cycles. Although it is reasonable to believe GRVY will be successful in sustaining their revenues with their powerful brand and diversified geographic markets, it is a risk that investors must take seriously and continue to monitor.

The third risk is most likely to blame for the company's exceptionally cheap valuation. Put simply, there are concerns that the management team does not care about the shareholders. This, coupled with the fact that GRVY is 59% owned by Japanese gaming company GungHo Online Entertainment ( GUNGF ), causes shareholders to suspect that they will never benefit from the company's success by receiving cash dividends or share repurchases. To put this in context, as of the most recent earnings report, GRVY has $318 million worth of cash on its balance sheet, with virtually no debt (Seeking Alpha).

Management's lethargy is certainly a viable concern in my view. However, it should be considered that GungHo Online Entertainment has participated in share repurchases of its own, reducing its share count from 115.2 million in 2013 to 62.2 million in 2022. Further, upon reaching out via email to the GRVY investor relations team, the following response was received:

" Yes, definitely our upper management acknowledged what shareholders want at this moment and it is under consideration. However, nothing has been decided yet and there are still chances to re-invest the cash to sustain this growth momentum. Many options are being discussed."

Do the above points confirm that management will act to benefit shareholders in the near future? No, but it's promising. Also, if a decision is eventually made by management to pay out dividends or buy back stock, this could serve as a significant catalyst for an upwards revaluation of the company's shares.

Valuation

Moving on to valuation, let's take a look at some of GRVY's key metrics compared to the broader sector:

| Metrics |

| GRVY |

| Sector Median |

| P/Sales |

| 0.87 |

| 1.10 |

| P/Earnings |

| 4.55 |

| 15.88 |

| P/Book |

| 1.44 |

| 1.56 |

From a cursory, relative valuation perspective , GRVY is undeniably cheap - particularly from an earnings perspective. It is important, however, to dig deeper and extract a conservative absolute valuation as well.

First, we will calculate the Net Current Asset Value ((NCAV)). The NCAV gives us a meaningfully conservative idea of what the liquidation value of the company would be if it closed its doors, paid off its debts, and distributed the remaining assets to shareholders. By taking (from Seeking Alpha) current assets of $407.8 million, subtracting total liabilities of $113.7 million, and dividing the result by shares outstanding of 6.948 million; we get an NCAV value of $42.33 per share.

As the company is currently trading at around $70 per share, one could argue that it's trading above a conservative estimate of its liquidation value. However, this valuation metric does not take into account the value of future cash flows, and merely treats the company as a static, dying entity. I therefore believe it is reasonable to treat the $42.33 number as downside protection for the current share price of approximately $70.

Now, considering future cash flows, let's perform a 'back of the napkin' DCF calculation using the following metrics :

| Free Cash Flow ((FCF)) |

| $17.8 million (FCF number explained below) |

| Cash (minus debt) |

| $315 million |

| FCF Growth (10 year) |

| 0% |

| Discount Rate (desired rate of return) |

| 20% |

| FCF Multiple |

| 8 |

| Shares Outstanding |

| 6.948 |

| Intrinsic Valuation |

| $59.39 |

To summarize the above: theoretically, over the ten-year period in question, we assume the company will generate $17.8 million dollars of FCF per year, discounted each year at a rate of 20%. We then take the sum of these discounted cash flows, as seen below:

| Year |

| FY FCF (millions) |

| Discounted FCF (millions) |

| 2023 |

| $17.8 |

| $14.83 |

| 2024 |

| $17.8 |

| $12.36 |

| 2025 |

| $17.8 |

| $10.29 |

| 2026 |

| $17.8 |

| $8.60 |

| 2027 |

| $17.8 |

| $7.15 |

| 2028 |

| $17.8 |

| $5.95 |

| 2029 |

| $17.8 |

| $4.97 |

| 2030 |

| $17.8 |

| $4.14 |

| 2031 |

| $17.8 |

| $3.45 |

| 2032 |

| $17.8 |

| $2.88 |

| Sum = $74.62 |

Subsequently, we assume we will sell our shares for a FCF multiple of 8 in the final year, giving us our terminal value ($2.88 * 8 = $23.04). After we add the terminal value ($23.04 million) and current net cash position ($315 million) to the sum of our discounted cashflows ($74.62 million), we divide that value by the current number of shares outstanding of 6.948 million. The number we arrive at is $59.39.

In a nutshell - this means that if we want a minimum annual return of 20%, assuming zero percent growth from the initial FCF value of $17.8 million, and assuming we can sell our shares for an 8x FCF multiple in the final year; the most we would pay for a single share today is $59.39.

Unpacking this further, the $17.8 million FCF figure is the annual FCF generated in 2017, before the company really gained traction in the mobile gaming market and far below the FY 2022 FCF number of over $60 million (which is likely to grow further). The calculation above also assumes 0% growth in the $17.8 million FCF number over the next ten years.

Considering GRVY owns a lead brand in a burgeoning industry, the calculation is admittedly arbitrary and perhaps unreasonably and excessively conservative. It was selected, however, to ensure an inherent and undoubtable margin of safety in the final result. After all, as Benjamin Graham opined :

" The function of the margin of safety is, in essence, that of rendering unnecessary an accurate estimate of the future ."

A prospective investor should experiment with the above numbers to find an appropriate valuation for their own assumptions, financial situation and aspirations.

Conclusion

GRVY is by no means a perfect company, and the risks covered in this article are certainly not exhaustive. However, a company does not need to be perfect to be an exceptional investment - and I believe GRVY's shares are trading at such a price that even stagnating or rapidly declining future FCF provides us with an exceptional margin of safety and adequate downside protection. With a rock bottom valuation such as this, the slightest sign of progression in resolving the company's risks could cause a fast and sharp rise in the share price.

For further details see:

Gravity: Overlooked And Undervalued