GRVY - Gravity's Impressive 2023: A Strong Buy With The Potential Behind Ragnarok Online

2023-11-02 04:00:56 ET

Summary

- Gravity experienced a 47.9% share price increase in 2023, emphasizing the success of its core products like Ragnarok Online.

- Gravity's mobile game revenues soared by 57.3% QoQ, contrasting with a decline in online game revenues, highlighting a shift towards mobile gaming.

- GRVY is exploring the blockchain gaming sphere, with titles such as Ragnarok Landverse and Ragnarok Monster World set to release between 2023 and 2024.

- The company's valuation suggests considerable undervaluation, with a fair value of $1.8 billion compared to its current market capitalization of $435.0 million.

- Despite inherent risks, such as dependency on the Ragnarok series and competitive challenges, GRVY is rated as a "strong buy" due to its promising growth trajectory.

Gravity Co., Ltd. ( GRVY ) is predominantly active in markets like Japan and Taiwan. The company's portfolio is impressive, with the renowned Ragnarok Online standing out as a primary contributor. In my view, the 47.9% rise in their share price during 2023 is a testament to the enduring appeal of their core products and the company's nimble approach to market changes. As Gravity sets its sights on multiple gaming arenas, particularly the budding blockchain sphere, it's crucial, in my opinion, to delve deep into its business growth trajectory, assess stock valuation, and forecast its future moves. I believe GRVY's current metrics suggest potential undervaluation. Therefore, in my assessment, even accounting for its intrinsic risks, I'd categorize it as a "strong buy."

Business Overview

Gravity operates in the online and mobile gaming arena, primarily catering to the markets of Japan and Taiwan from its base in South Korea. The company's core competency lies in developing, distributing, and publishing a suite of interactive gaming products, with Ragnarok Online being its flagship offering. Gravity's portfolio spans multiple online games, including Ragnarok Online II, Requiem, and Dragonica, and mobile games like Ragnarok Online-Uprising: Valkyrie and Ragnarok Online Mobile Story. The firm also delves into the console gaming domain, providing titles for platforms like Nintendo DS and Xbox 360. In my view, the expansive and diverse gaming portfolio positions Gravity well in capturing a broad spectrum of the gaming market, evidenced by its remarkable 47.9% YTD share price increase in 2023, largely propelled by the enduring popularity of Ragnarok Online.

Moreover, Gravity has successfully anchored itself within the online and mobile gaming landscape, primarily propelled by the achievements of its Ragnarok series . Among its diversified portfolio, Ragnarok Online emerges as an enduring classic, celebrated for its captivating open world, job system, and community camaraderie it engenders. While some players express dissatisfaction with the dated graphics and the pay-to-win model, the game proudly boasts a user score of 8.2/10 on Metacritic and an 8.4/10 rating on IGN. Although Steam reviews present a mixed picture, the nostalgia the game commands continues to be a significant magnet.

Also, GRVY’s Ragnarok M: Eternal Love is a bet in the mobile arena and encapsulates the quintessence of Ragnarok Online while proffering a rejuvenated gaming experience. It has garnered accolades for its graphics, music, and expansive world, clinching a rating of 4.5/5 on the App Store and 3.7/5 on Google Play. However, the gacha system and monetization framework have been bones of contention. Subsequently, Ragnarok Origin, a novel mobile rendition, is notably lauded for its class selection feature, albeit holding a modest rating of 3.3/5 on the App Store, possibly hinting at similar monetization and technical challenges encountered by its predecessors.

Source: GRVY's IR Presentation

Embarking on a broader horizon, GRVY is delving into the burgeoning realm of blockchain gaming with anticipated titles like Ragnarok Landverse, Ragnarok Monster World, and Ragnarok Poring Merge NFT, slated for release between 2023 and 2024. Beyond the Ragnarok universe, the company triumphantly launched WITH: Whale In The High globally on June 29, 2023, and is poised to release White Chord in Japan on August 29, 2023. In the traditional gaming sector, the eagerly awaited releases of Ragnarok Begins, Ragnarok V: Returns, Ragnarok: The Lost Memories, and Ragnarok 20 Heroes are strategically lined up from Q3 2023 to 2024 across South Korea, Vietnam, and other regions. Each title, whether in Closed Beta Testing or recently launched, extends the rich Ragnarok legacy, exploring various gameplay styles and narratives. In my view, GRVY's expedition into blockchain gaming and the methodical amplification of its established IPs demonstrate a broad and astute strategic outlook. This strategy adeptly capitalizes on the nostalgic charm of Ragnarok while seamlessly adapting to new technological frontiers and market segments, showcasing a forward-thinking approach to navigating the dynamic gaming industry landscape.

Source: GRVY's IR Presentation

GRVY's Mobile Revenue Momentum

The core propellant of growth this quarter has been the remarkable ascent in mobile game revenues, escalating by 57.3% compared to the preceding quarter and a robust 221.4% compared to the same quarter last year. This positive stride stands in stark contrast to the trajectory of online game revenues, which endured a slide of 25.0% QoQ and 31.4% YoY. Other revenues, too, witnessed a modest retreat, marking a 2.3% shrinkage QoQ and a 12.8% contraction YoY. This narrative accentuates a significant momentum within the mobile gaming sector, juxtaposed against a downturn in online and other gaming revenues for GRVY in Q2 2023. I infer that the diverging revenue streams between mobile and online gaming for Gravity in this quarter robustly signify a consumer inclination towards mobile gaming. In my view, this shift aptly reflects the expansive growth potential nestled within the global mobile gaming market, underscoring a promising horizon for mobile gaming ventures.

GRVY will continue enjoying strong secular tailwinds (Source: Precedence Research)

Furthermore, the proliferation of smartphones coupled with the advent of 5G technology will, I infer, markedly lower entry barriers, thus invigorating the market with a fresh influx of gamers across diverse demographics. This booming gamer base, coupled with innovative monetization strategies, could potentially unlock new revenue streams, thereby bolstering the financial fortitude of game developers in the long haul. Nonetheless, the challenges tied to monetization remain a notable concern, necessitating a reasonable balance to ensure a gratifying user experience while securing sustainable revenue channels.

Transitioning to a broader perspective, the global mobile gaming market was valued at $184.4 billion in 2022, with forecasts indicating a surge to around $775.69 billion by 2032, at a CAGR of 15.5% between 2023 and 2032. This anticipated growth trajectory is closely tied to technological advancements such as integrating Augmented Reality ((AR)) and Virtual Reality ((VR)), which substantially enhance gaming experiences. The primary catalysts fueling market expansion encompass the widespread adoption of smartphones and avant-garde game development technologies, rising recognition of esports, and the rollout of 5G technology. In 2022, the freemium business model, delineated by in-game purchases in complimentary games, dominated the market share. Moreover, the 22-24 age bracket emerged as the predominant market share holder in 2022, a testament to their proficiency with sophisticated technologies.

On a regional spectrum, Asia-Pacific, spearheaded by China, is predicted to reign over the market through 2032, courtesy of its substantial mobile gaming market growth. However, the market is confronted with monetization hurdles, primarily the challenge of harmonizing user experience with monetization via in-app purchases and advertisements. Nonetheless, the enduring uptake of smartphones, which elevates the gaming experience and broadens the gamer demographic, is poised to boost revenue generation avenues for game developers.

Valuation Analysis

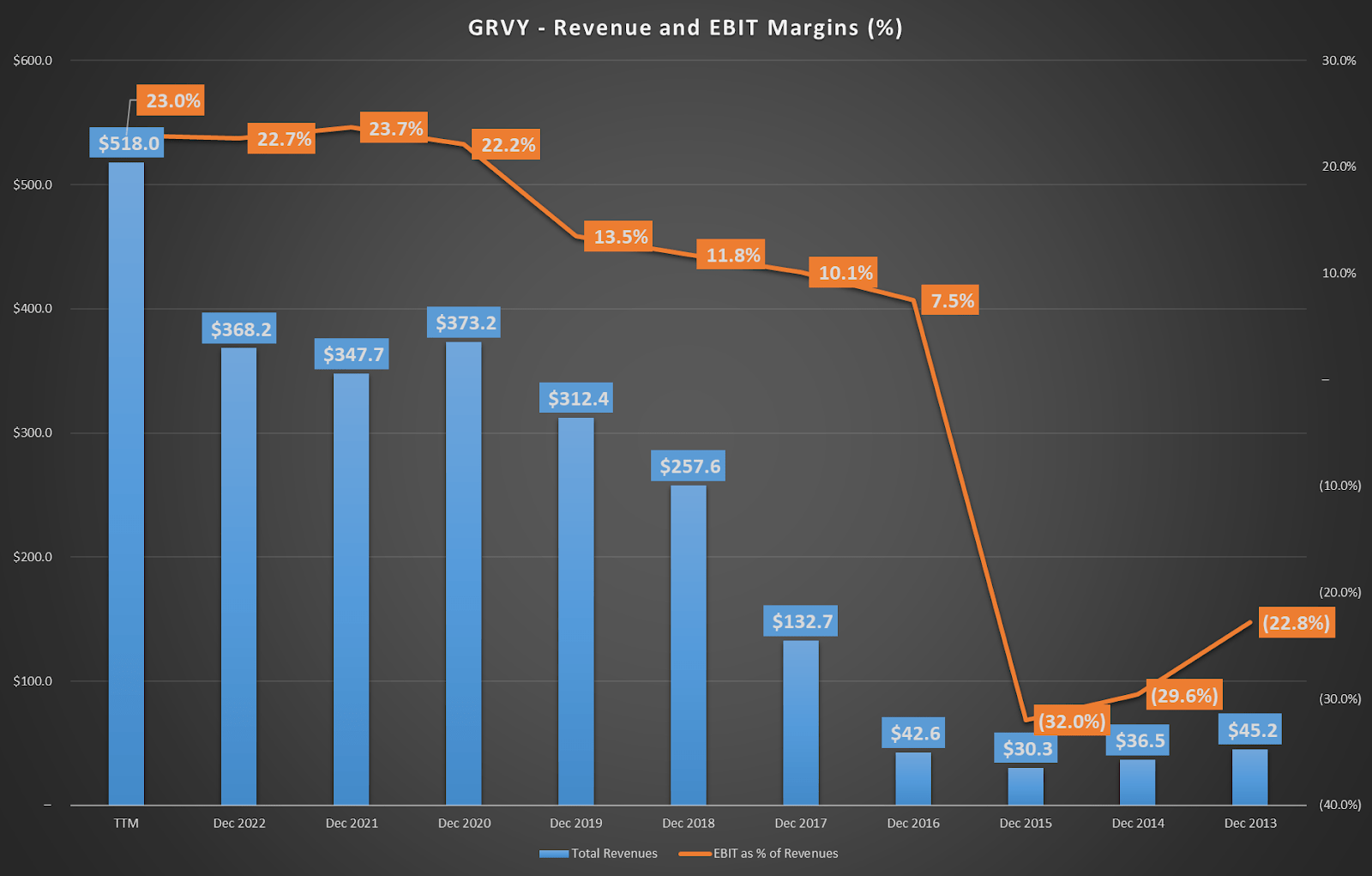

From a valuation perspective, I believe it's crucial to highlight that the company has exhibited commendable financial discipline, reflecting a consistent 27.6% CAGR in its revenues since 2013, inclusive of the recent trailing twelve-month data. In my view, sustaining such a growth rate over an extended period is no minor feat. Moreover, when we compare this with the mobile gaming sector's CAGR of 15.5%, it's evident that GRVY's performance is not just commendable but also superior. This, I think, underscores GRVY's robust position in the market.

{kind=link}

In my opinion, employing a simple DCF model reveals GRVY's considerable intrinsic worth. I have even factored in a tapering growth rate, decreasing to 2% by 2027. I believe this is a particularly conservative approach, especially when considering GRVY's historical growth trajectory. Drawing upon GRVY's past EBIT, D&A, CAPEX margins , and tax rates, the valuation intimates, in my view, a pronounced undervaluation of the asset.

Author's elaboration

In my analysis, the company's fair value is roughly $1.8 billion. This is notably higher than its existing market capitalization of $435.0 million. This valuation infers a price target of $82.70 per share, presenting, in my view, an impressive potential upside of 321.3%. However, I believe it's essential to remember that the market is typically astute in its valuations, and deviations of this magnitude are uncommon.

Downside Risks

In my view, Gravity's valuation seems tempered by several factors . Primarily, the company's pronounced dependency on the Ragnarok Gaming Series, which constituted a large part of its 2022 revenue, makes it susceptible to niche market dynamics. Moreover, the controlling stake by GungHo Online Entertainment, Inc., though providing strategic guidance, may, in my opinion, lead to potential disagreements with minority shareholders, potentially denting corporate governance and investor sentiment. The escalating competition from industry powerhouses like NCSoft Corporation, Netmarble Corp., Tencent Holdings, and Activision Blizzard could overshadow Gravity's market stature. Furthermore, I feel that if Gravity's new forays, such as Final Knight and Alterium Shift, don't achieve the expected success, it could be a setback. Additionally, the licensing collaborations with firms like Nuverse and GungHo, which notably bolstered its 2022 earnings, introduce an element of unpredictability. A shift in these partnerships or altered licensing conditions could profoundly influence Gravity's fiscal stability and market valuation.

In my view, the challenge of monetization in the gaming sector cannot be understated. Striking an optimal balance between a fulfilling user experience and effective revenue generation, especially via in-app purchases and ads, is paramount. I believe that leaning too heavily into a pay-to-win model could be detrimental, potentially alienating players. This, in turn, might not only erode revenue streams but also blemish a company's standing in the public eye. Technical disruptions, such as bugs or server outages, can further compromise the quality of gameplay. These setbacks can, in my opinion, lead to tangible user dissatisfaction and consequent financial implications. The gaming landscape is notably competitive. I infer that with the constant influx of new releases, companies like Gravity risk losing players to rival titles. This constant competition could undoubtedly influence user retention and, by extension, revenue. Gamers, I've observed, are known for their shifting preferences. The industry's annals are replete with examples of games that enjoyed fleeting popularity before being eclipsed by newer entrants. If Gravity fails to sustain player engagement or address evolving user needs effectively, I think there's a real risk to their active player base. Moreover, given the evident market saturation – especially with the profusion of titles under the Ragnarok IP – players might seek fresh, unexplored gaming horizons.

GRVY has seen an impressive 2023 rally (TradingView)

Analyzing Gravity's track record, I believe the company has consistently showcased an ability to weather the fickle nature of the gaming industry. In my view, their excellence in game development, further strengthened by strategic partnerships and an expansive global reach forms a robust foundation. Their proactive moves to diversify not only highlight their visionary approach but also underscore a commitment to maintaining a leading edge in the market. I infer from the trends that, despite its occasional downturns, the gaming sector is primed for expansion. A surge in global gaming interest and technological innovations, in my opinion, are paving the way for this growth. With this in mind, I feel the current market valuation might overlook some of Gravity's expansive potential. Consequently, I believe GRVY is notably undervalued. As the company's revenue potential unfolds, I anticipate a consistent uptick in its stock price. Therefore, factoring in all risks and uncertainties, I still assign GRVY a "strong buy" rating, mainly due to its outstanding business model and the market's undervaluation of its prospects.

Conclusion

In my view, GRVY holds a distinctive position in the gaming sector. Their portfolio, highlighted by prominent titles like Ragnarok Online, demonstrates their adeptness at tapping into diverse gamer preferences. Since I last analyzed GRVY in 2020, there has been a notable decline in its stock price. However, in parallel, I've observed enhancements in both its revenues and earnings. This juxtaposition, in my opinion, paints a more favorable investment landscape for the present. While I acknowledge that Gravity has navigated a maze of challenges, from monetization hurdles to fierce competition, their consistent ascent, marked by an impressive 27.6% CAGR since 2013, is a testament to their industry prowess. The gaming domain is intrinsically volatile, with ever-shifting trends. Yet, I believe Gravity's exploration of blockchain gaming reflects more than a mere tactical pivot—it signifies a visionary blueprint for their future. I believe GRVY’s undervaluation offers substantial potential for astute investors. Their strategic diversification endeavors not only underscore their innovative stance but also their unwavering ambition to remain at the forefront of the gaming sphere. Therefore, I rate GRVY as a "strong buy," and I foresee a promising trajectory for the company.

For further details see:

Gravity's Impressive 2023: A Strong Buy With The Potential Behind Ragnarok Online