GRVY - Gravity: Upside Potential From This Overlooked Company

2023-08-18 07:05:07 ET

Summary

- Gravity's share price has outperformed the market by a 72% increase YTD.

- The company's flagship game, Ragnarok Online, is highly popular and downloaded in Asia.

- Q2 2023 revenue and operating profits have seen significant growth, indicating strong financial performance.

- Gravity Co.'s Asian - centered market is the world's largest and fastest growing gaming markets.

- The triple-digit upside potential from my DCF calculator could suggest that Gravity Co. Ltd is significantly undervalued and underappreciated by investors.

Investment Thesis

The share price of Gravity Co., Ltd (GRVY) has significantly outperformed the market in 2023. While the S&P 500 has averaged a return of 17% YTD, investors of Gravity Co have seen their investments go up by 72%. 2023 has been a fruitful year for Gravity Co, Ltd. Based on its latest Q2 2023 financial report, its revenue has seen an exponential growth of 147.5% YoY to 239 billion KRW (US $181 million), while its operating profit has soared by an astonishing 138.3% YoY to 53 billion (US $39.9 million). Alongside the rising popularity of its online and mobile games like Ragnarok Origin and Ragnarok: The Lost Memories launched this year, Gravity Co, Ltd.'s share price has skyrocketed this year.

Nonetheless, I still consider GRVY a fundamentally strong company. In spite of the popularity of the Ragnarok series among gamers, the management team of Gravity Co. are planning to grow Ragnarök's intellectual properties by diversifying its IP Business laterally. For example, Gravity is planning to debut its first Blockchain NFT Game Ragnarok: Monster World in 2024 to expand its gamers base and improve its gamers' loyalty.

Furthermore, looking through a financial lens, the company has a robust balance sheet, with an ample amount of cash and no debt, which may allow the management team to return value to shareholders in the future through share buybacks and dividend distributions. Given its now trading a single-digit P/E and P/FCF multiple, I rate Gravity Co, Ltd as a "Strong Buy" due to its cheap valuation and ample growth opportunities in the future.

Business Overview

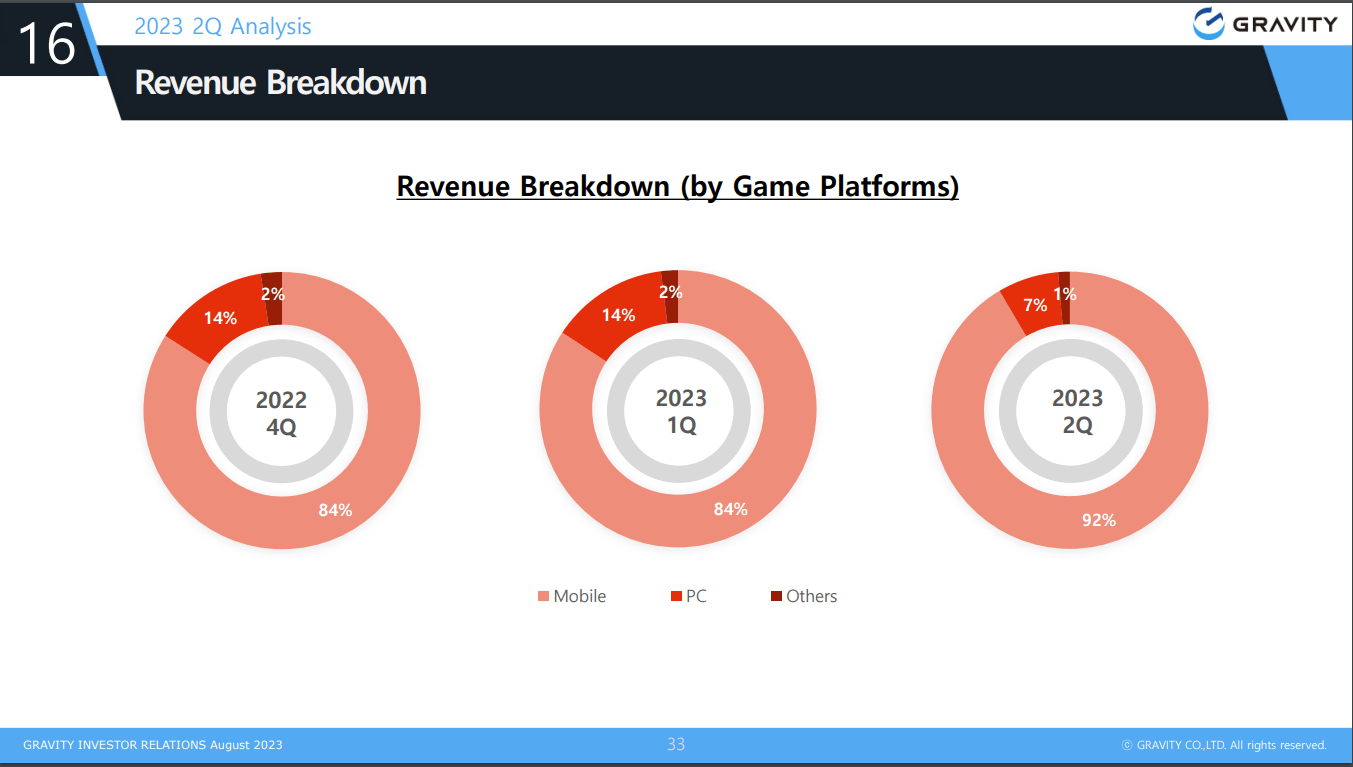

Revenue Breakdown (Q2 2023 Investors Presentation)

{kind=link}

To those who are unfamiliar with the company, Gravity Co, Ltd. is a Korean gaming company that specializes in developing and publishing online games and mobile games. The company also licenses its intellectual properties ((IP)) to 3 rd parties and joint ventures to earn commissions and royalties. It has been listed on the NASDAQ stock exchange since 2005.

Gravity Co Ltd.'s revenue streams are divided primarily into 2 segments, which are namely the online gaming (PC) and mobile gaming segment.

The online gaming segment includes computer games like Ragnarök Online that allow a large number of gamers to interact with one another in the gaming community. Gravity earns its revenue primarily through micro-transaction fees (i.e., In-app purchases) and royalties/commissions through 3 rd party licenses. Its contribution to Gravity's total revenue has declined from 14% to just 7% in Q2 2023

The mobile gaming segment accounts for up to 92% of Gravity's total revenue. It allows gamers to download mobile games like Ragnarok X: The next generation and Ragnarok Origin through Android or IOS to their devices, and targets less sophisticated gamers. Gravity also earns its revenue primarily through micro-transaction fees (i.e., In-app purchases) and royalties/commissions from 3 rd party licenses

The popularity of the Ragnarok gaming series in Asia

I view the intellectual properties that the company possesses, including the successful publication of Ragnarok Online by Gravity Co, Ltd, as one of the major competitive advantages of the company. In fact, Ragnarok Online has 1.1 million total players/subscribers and 32.1k active users per day . The number of subscribers and players is often considered an invaluable asset to the company, as the company could raise its retail prices among gamers for its gaming items without the fear of losing too many gamers.

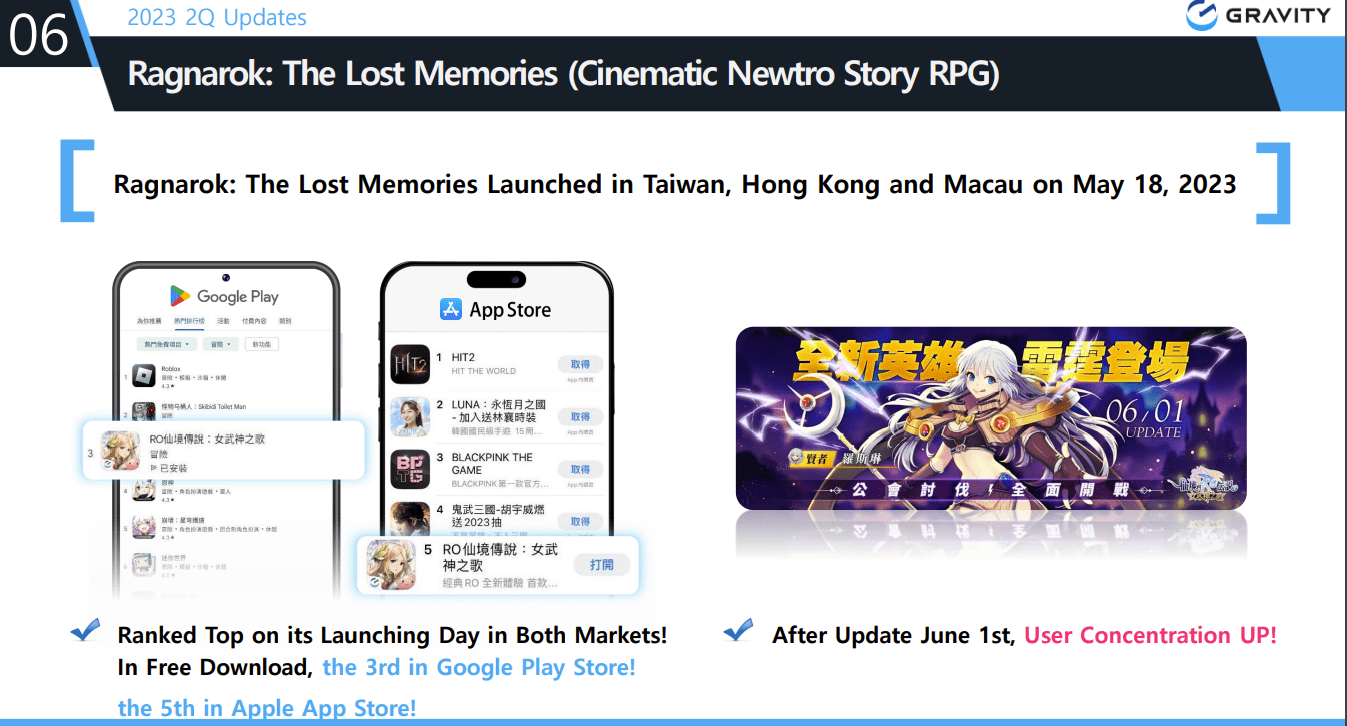

Ragnarok: The Lost Memories (Q2 2023 Investors Presentation)

{kind=link}

Extending the successful campaign of Ragnarok Online, Gravity Co, Ltd. also leverages its intellectual properties to offer new mobile games to gamers, which creates synergy within its gaming ecosystem. For example, the company recently launched Ragnarok: The Lost Memories back in May this year in HK & Taiwan, which has taken gamers by storm, ranking 3rd in Google Play Store and 5th in App Store respectively. This illustrates the strong gamer's loyalty and ecosystem stickiness for Gravity's mobile games.

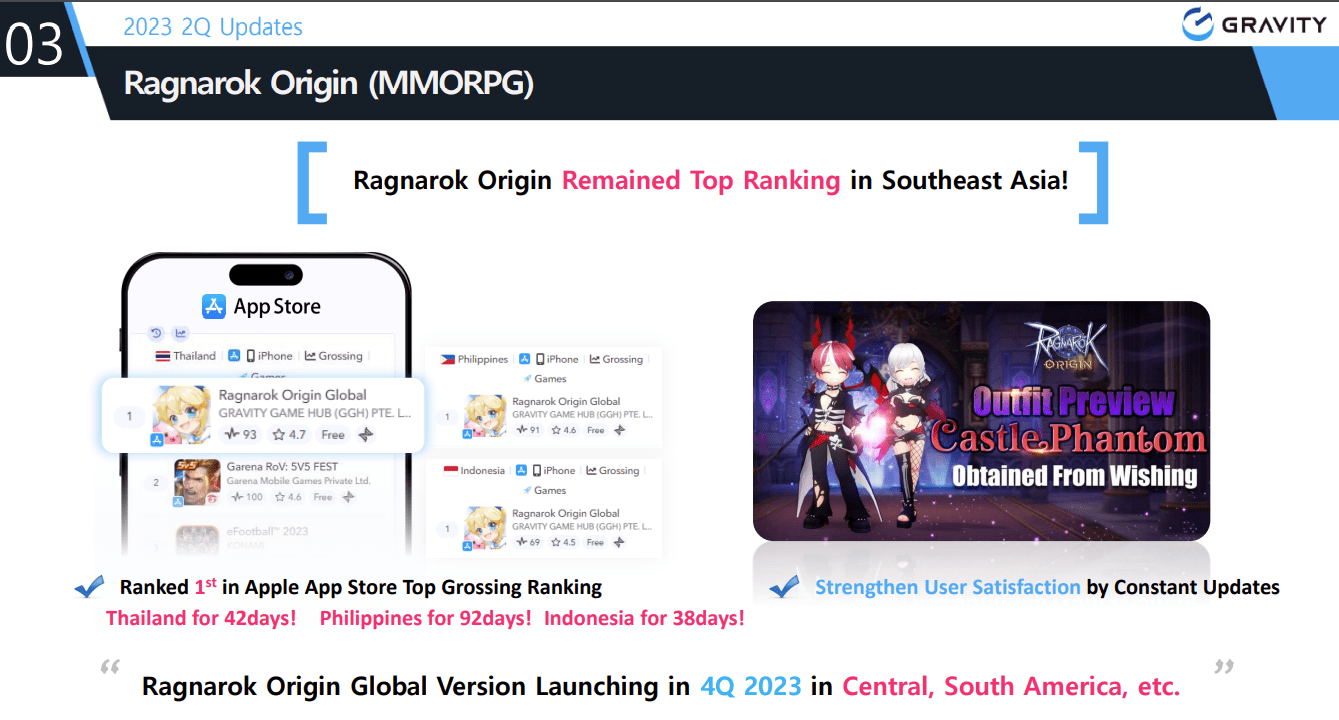

To add on, another Massively Multiplayer Online Role-Playing Game (MMORPG) - Ragnarok Origin also ranked 1st in App Store in SE Asia, which epitomizes the brand reputation and strong popularity of its Ragnarok gaming series from Gravity among gamers in the SE Asian markets.

Ragnarok Origin (Q2 2023 Investors Presentation)

{kind=link}

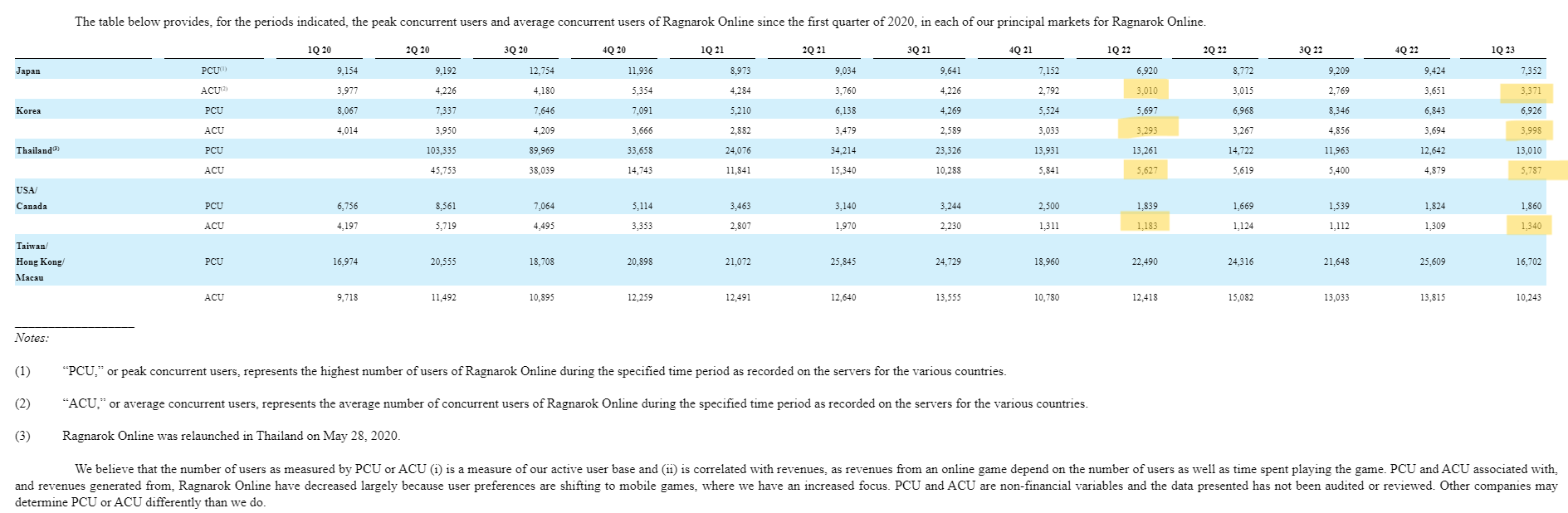

Average number of concurrent users in Ragnarok Online (2022 Annual Report (20-K))

{kind=link}

Furthermore, we can also see an uptick in the average number of concurrent users in Ragnarök Online across Asia over the past year. The average number of concurrent users in Japan grew from 3,010 in Q1 2022 to 3,371 in Q1 2023. In Korea, the number also grew from 3,293 in Q1 2022 to 3,938 in Q1 2023, which demonstrates the growing popularity and reputation of Ragnarok Games across Asian markets.

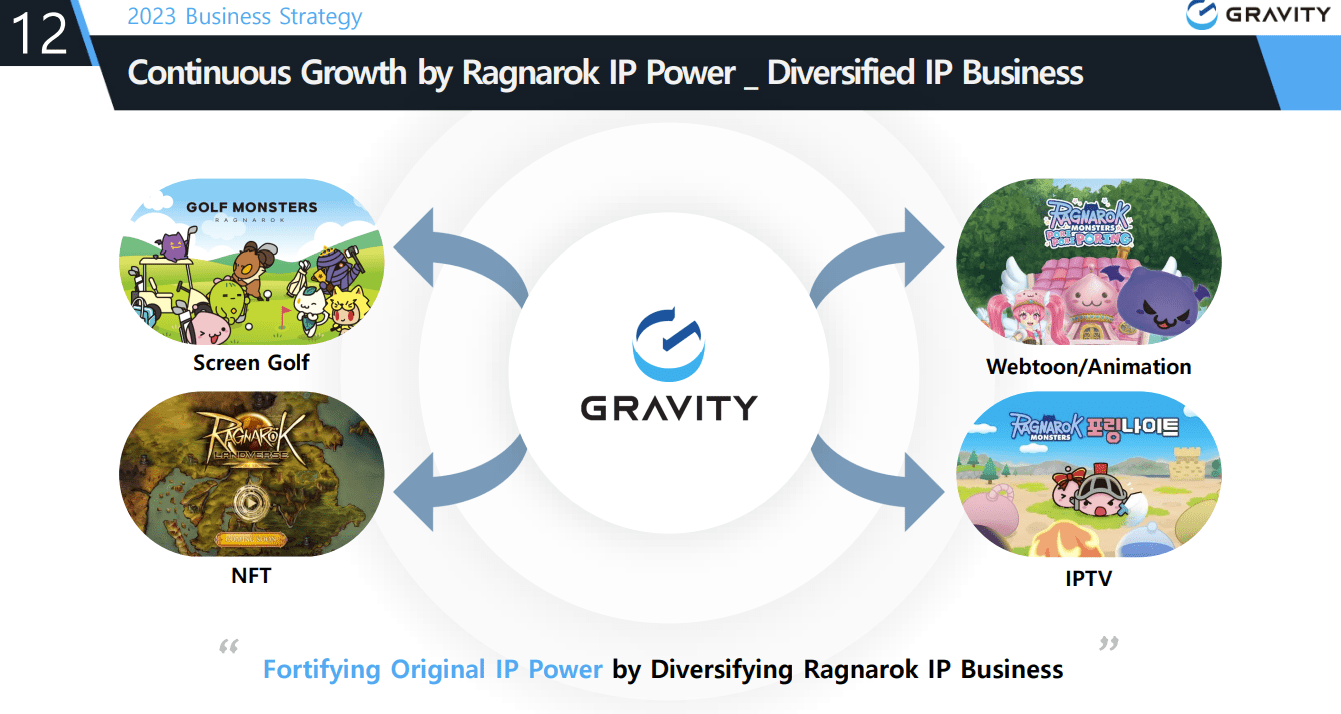

Unlocking the Value of Ragnarök's IP through Gaming Diversification

Ragnarok IP Business Diversification (Q2 Investors Presentation)

{kind=link}

Leveraging its success in its intellectual property on Ragnarok Online, Gravity Co, Ltd. has diversified its IP Business by expanding into the screen golf, NFT, Animation and IPTV markets, which helps to create synergy and develop a sticky ecosystem around the Ragnarok IP.

For example, the company plans to tap into the NFT and blockchain gaming market by launching the NFT Collecting RPG Game Ragnarok: Monster World in 2024, which is expected to expand its existing gamers base and attract more gamers from the NFT space. I expect such a movement will help to unleash the IP potential of Ragnarok and allows Gravity Co, Ltd to expand its total addressable market ((TAM)) by attracting more gamers from the NFT space.

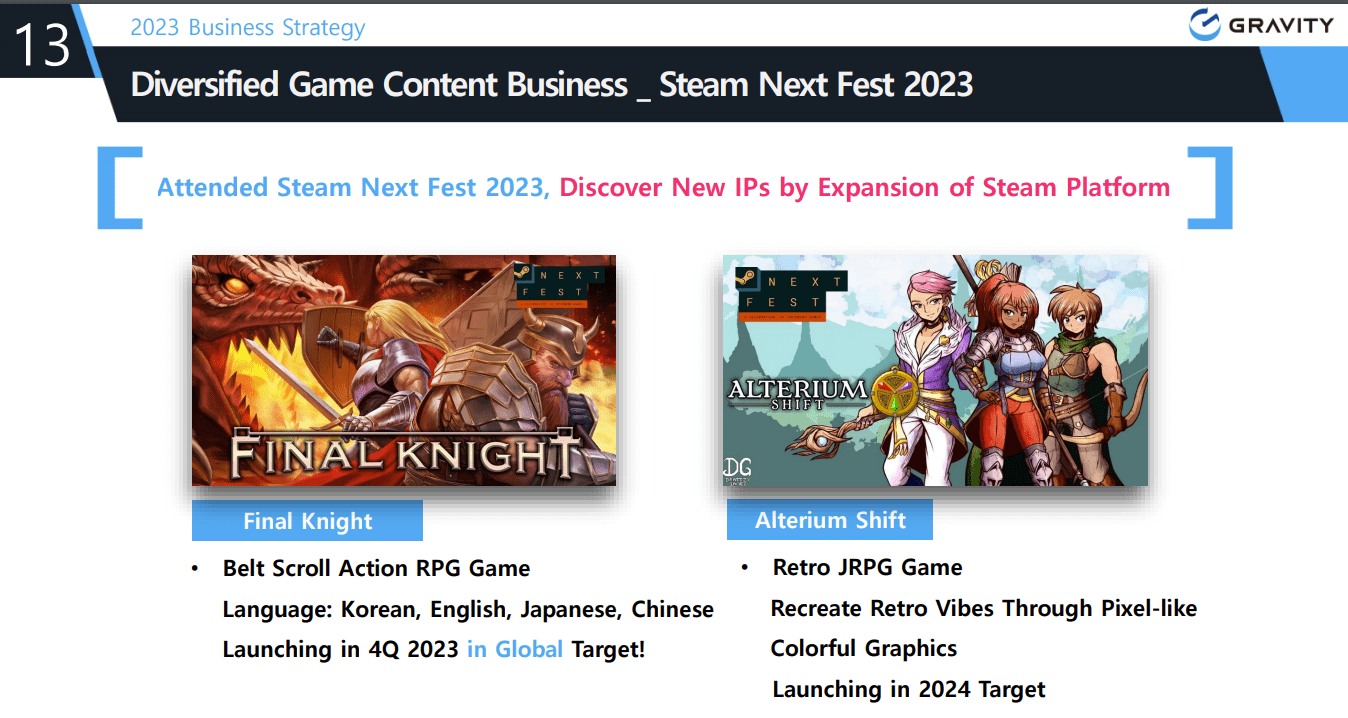

New Gaming Content (Q2 2023 Investors Presentation)

{kind=link}

To alleviate its over-concentration risk on Ragnarok's IP, Gravity Co, Ltd is planning to diversify and expand its number of IPs on the gaming platform. For example, Final Knights and Alterium Shift are the latest gaming genres that the company is developing outside of its Ragnarok IP & its Ragnarok Monsters Animation IP. I expect existing Ragnarok gamers will be tempted to try out other games launched by Gravity Co, Ltd within its ecosystem, which will enhance user loyalty and the customer experience in the game.

As for GRVY, with more gaming IPs and a higher number of active gamers, I expect more revenue streams and cash flows to the business as the company could charge gamers for its gaming items on a wider scope of mobile/online games, which will boost its micro-transaction revenue. Personally, I would be interested to know if Gravity Co, Ltd plans to introduce external advertisements into its gaming products so as to increase its revenue streams in the future.

Industry Overview: Growing gaming markets in Asia

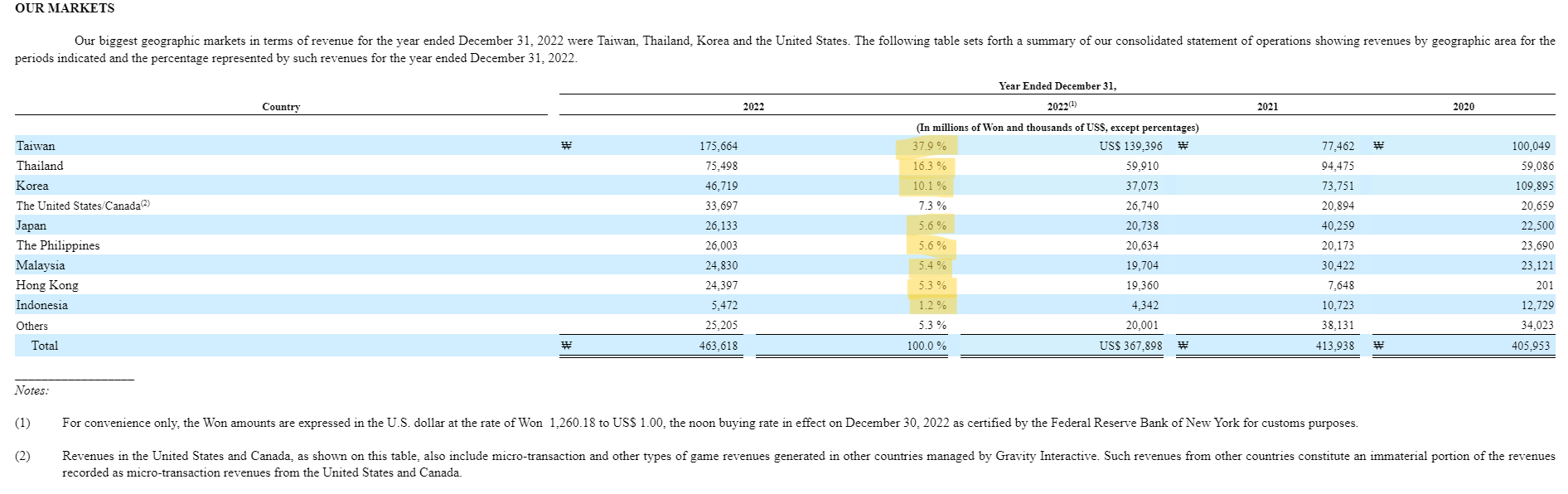

Gravity Co, Ltd.'s geographical revenue breakdown (2022 Annual Reports (20-K))

{kind=link}

As we can see from the above, based on its latest 2022 annual report, the overwhelming majority (87%) of Gravity's revenue comes from Asia, including important markets like Taiwan (37.9%), Thailand (16.3%), Korea (10.1%) and Japan (5.6%).

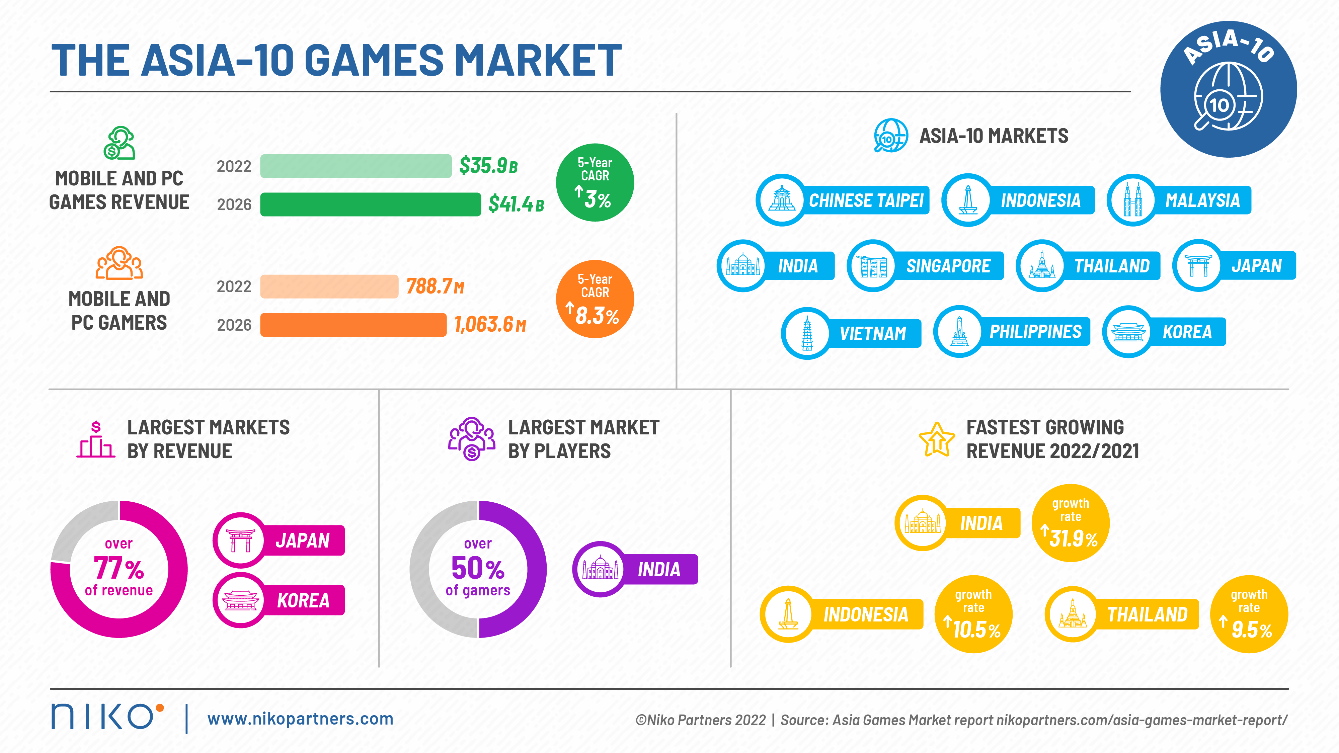

Asia gaming market (Niko Partners)

{kind=link}

According to Niko Partners , a research firm that specializes in video games markets and consumers in Asia has revealed that excluding China, the number of mobile and PC gamers is expected to grow by an astonishing 8.3% CAGR from 788million users in 2022 to more than 1 billion of active gamers in 2026 due to the prevalence of mobile devices and improvements in online network infrastructure in Asia. I expect such a tailwind to expand Gravity Co, Ltd's Total Addressable Market ((TAM)) and its number of gamers in the foreseeable future, providing more business opportunities for Gravity Co to exploit these underpenetrated markets in the future.

In particular, Gravity Co Ltd shall see ample revenue growth opportunities in its ASEAN markets like Thailand and Indonesia, whose mobile and PC gaming revenue is expected to grow at a CAGR of 9.5% and 10.5% respectively. Thus, in the foreseeable future, I would expect a larger proportion of revenue for Gravity Co to come from SE Asia, which will likely bring in more revenue and cash flow for the business itself.

Financial Analysis

1. Robust growth in revenue and operating profit

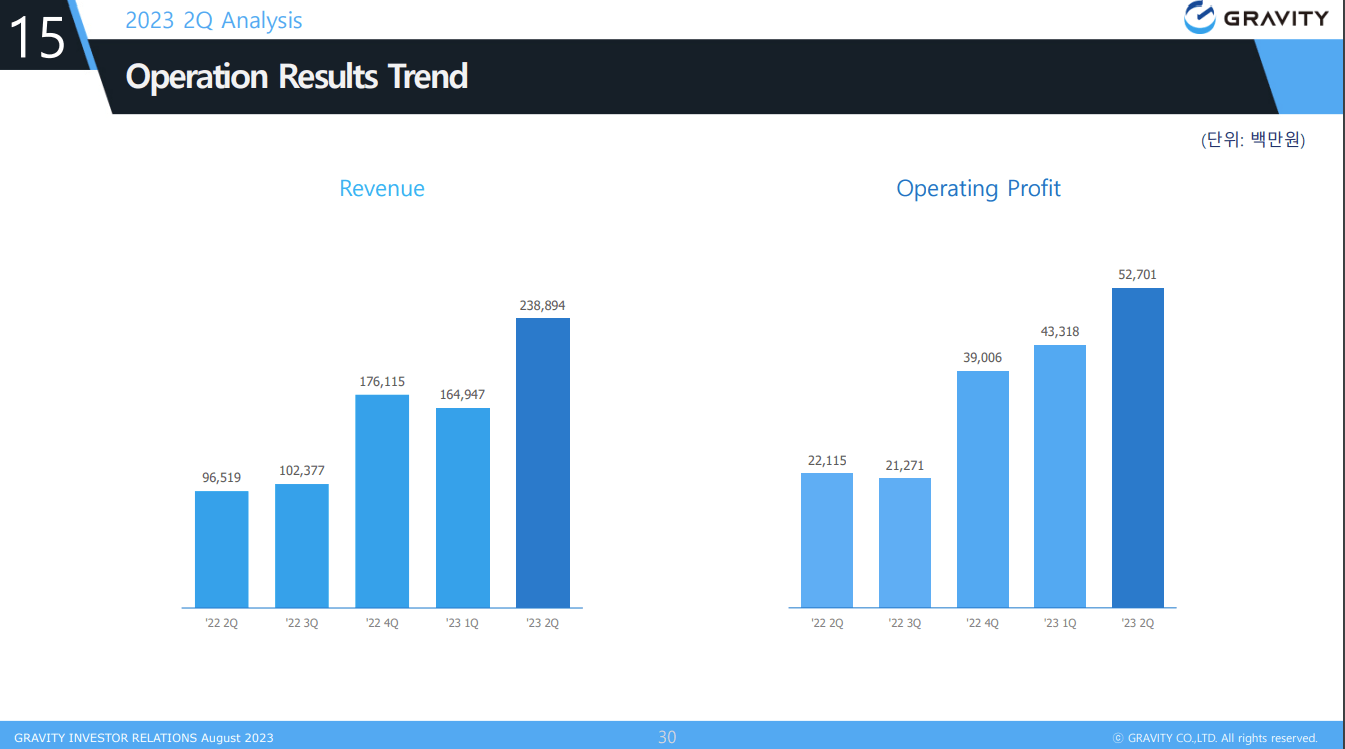

Gravity Q2 2023 Revenue & Operating Profit (Investors Presentation)

{kind=link}

Overall, 2023 has been a year of resounding triumph for Gravity. Its total revenue grew by 147.5% YoY from 96 billion KRW in Q2 2022 to 238 billion KRW ($181 million USD) in Q2 2023. Its operating profit has also soared by an astounding 138.8% YoY from 22.1 billion KRW in Q2 2022 to 52.7 billion KRW ($40 million USD) in Q2 2023. The success was primarily driven by growing revenues from Ragnarok Origin and Ragnarok X: Next Generation , which was launched in Southeast Asia, Korea, Japan, Taiwan, Hong Kong and Macau between 2H 2022 and 1H 2023.

Looking forward to the future, with a number of mobile games like Ragnarok: The Lost Memories and Ragnarok V: Returns scheduled to be debuted later this year, I expect Gravity Co, Ltd. to continue its revenue growth trajectory in high double-digits given the popularity of these games.

2. Strong Balance Sheet with minimal debt

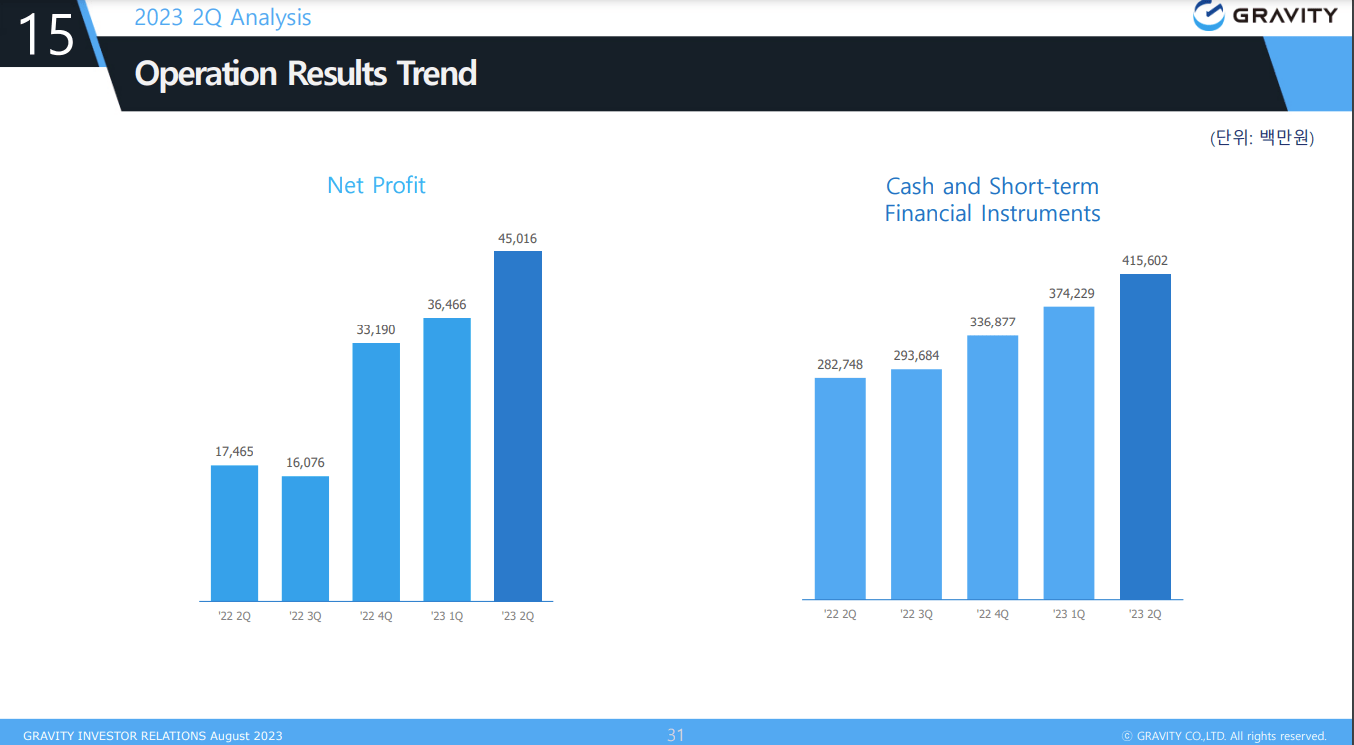

Cash Position for Gravity Co. (Q2 2023 Investors Presentation)

{kind=link}

Another thing I like about Gravity Co, Ltd is the strong balance sheet it possesses. Its Cash pile has been accumulating over the past year, growing from 282.75 billion KRW in Q2 2022 to 415.6 billion KRW (US $318 million) in Q2 2023.

The company primarily uses its cash to acquire more gaming intellectual properties or finance its future gaming development to maintain its competitive advantage. However, I think it would be appropriate for the management team to use those cash reserves to return value back to shareholders through share buybacks or dividend distributions.

Another highlight of its shareholders-friendly balance sheet is the company has Little to No Debt at all. Gravity Co, Ltd has no long-term debt. The management team has argued that the company is self-sufficient to finance its daily operations through its cash reserves, which minimizes its external dependence on leverage.

Capital Structure of Gravity Co. (SeekingAlpha)

Just to provide another perspective, Gravity has a market cap of around US $500M, however, it has cash reserves of over US $318M, which implies that over 60% of its market cap is covered by Cash! This leaves the company's enterprise value just slightly over US $187m.

As an investor looking to invest in a company over the long term, I like owning companies with maximum cash and minimal debt on their balance sheet to avoid the risk of the company going bankrupt.

3. Differentiated profitability and operating efficiency among competitors

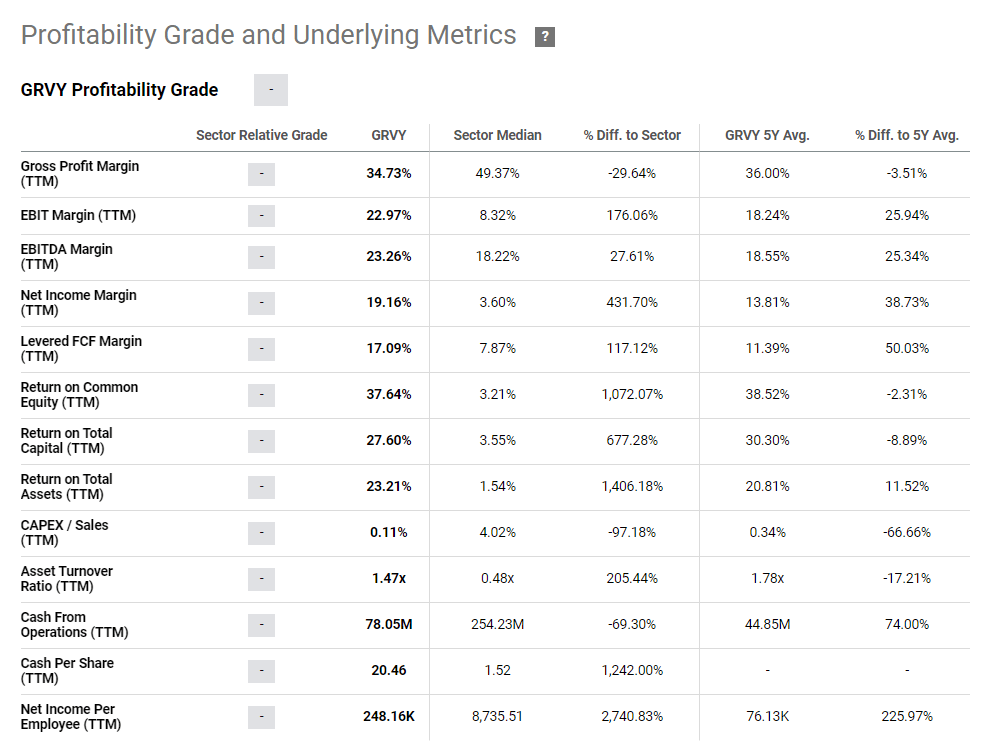

Profitability of Gravity Co. (SeekingAlpha)

{kind=link}

Currently, Seeking Alpha does not offer any grading to Gravity Co, Ltd. However, I would personally rate Gravity an "A" for its profitability given its outperformance in margins compared to the sector median.

For example, GRVY has an Operating Margin and Net Income Margin of 22.97% and 19.16% respectively, which trumps the sector median of 8.32% and 3.60% respectively. Its current operating margins are also higher than its 5-year average too.

Furthermore, Gravity Co, Ltd has a promising operating efficiency track record. Despite dropping slightly recently, The ROA and ROIC remain at 23.2% and 27.6% respectively, which outperforms the sector median of 1.54% and 3.55% respectively, illustrating great capital allocation efforts from the management team.

DCF Valuation: I saw a huge discrepancy between its intrinsic value and its current price

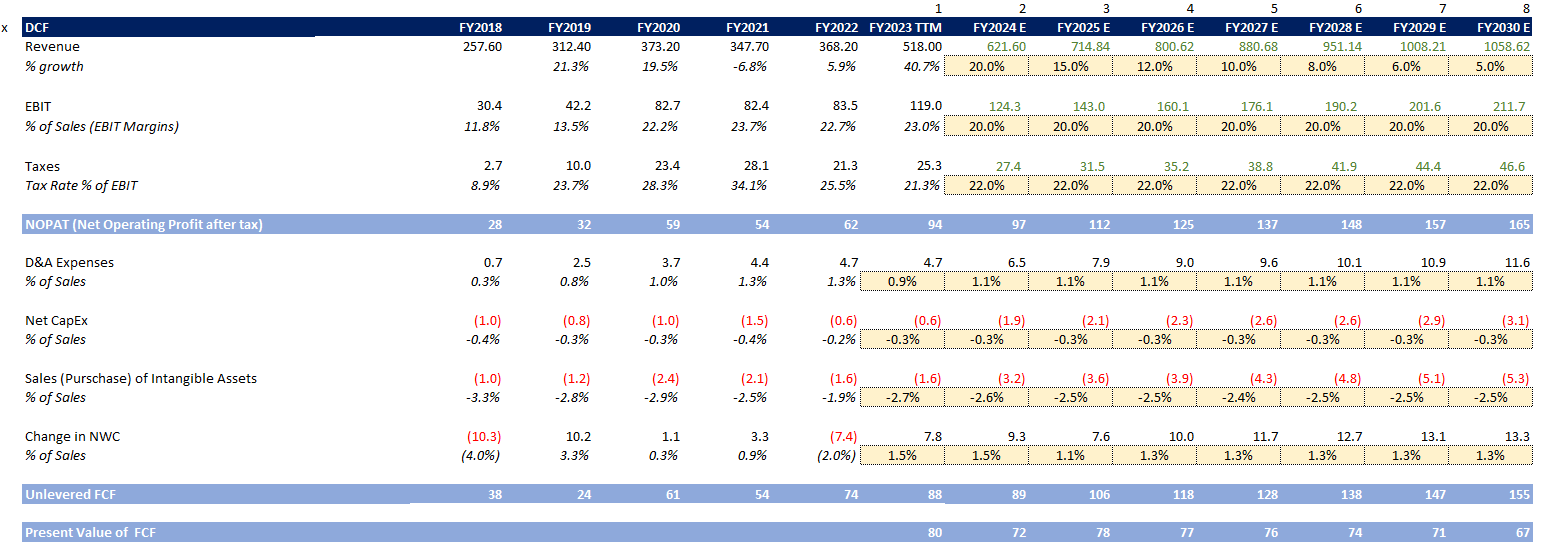

DCF Valuation for Gravity Co. (KL Research)

{kind=link}

For the sake of currency simplicity, I have converted all monetary units from KRW to USD in my financial model. All numbers in my financial model are expressed in millions.

Based on my personal assumption, apart from 2023, where Gravity's revenue is expected to grow by an astonishing 40% from (US $368m in FY 2022 to US $518m in FY2023) due to the successful launch of Ragnarok Origin , and Ragnarok X: Next Generation this year in Korea, Thailand and Taiwan. I consider the revenue growth in 2023 as an outlier.

Based on its historical growth record, I am forecasting growth in its revenue of around 20% in 2024 (i.e., $671 million) and decrease progressively to around 5% in 2030 (i.e., $1 billion), as Gravity Co, Ltd is diversifying its games offerings alongside my expectation of its future continuous success of the Ragnarok gaming series given its popularity among gamers.

As for its Operating Margins, I predict GRVY's operating margins to be around 20-22%, which is in line with the company's historical track record, whereas the effective tax rate of 22% will be in line with Korea's corporate tax rate.

After subtracting the ~ $1-2 million of capital expenditures and ~$ 3-5 million purchase of intangible assets annually, for future gaming content creation and to acquire 3 rd party licenses for gaming operations to maintain its competitive moat, we're left with $80-110 million of annual unlevered free cash flow for the business for the next few years.

By using a Discount Rate of 11% and a perpetual growth rate of 2%, I have arrived at an Enterprise Value for Gravity Co, Ltd of around $1.3 Billion. By adding back, the $381 million of cash while subtracting its total debt of $2.8 million and minority interest of $0.5 million, and dividing it by the total amount of outstanding shares of 6.95 million shares, I have arrived at an Intrinsic Value of GRVY for around ~ $238 per share, implying a 200% upside!

Intrinsic Value for GRVY (KL Research)

{kind=link}

The reason why I think there is a huge gap between its value and price is because the company was disregarded and misunderstood by investors and Wall Street. Currently, there are no Wall Street analysts tracking this company with robust fundamentals.

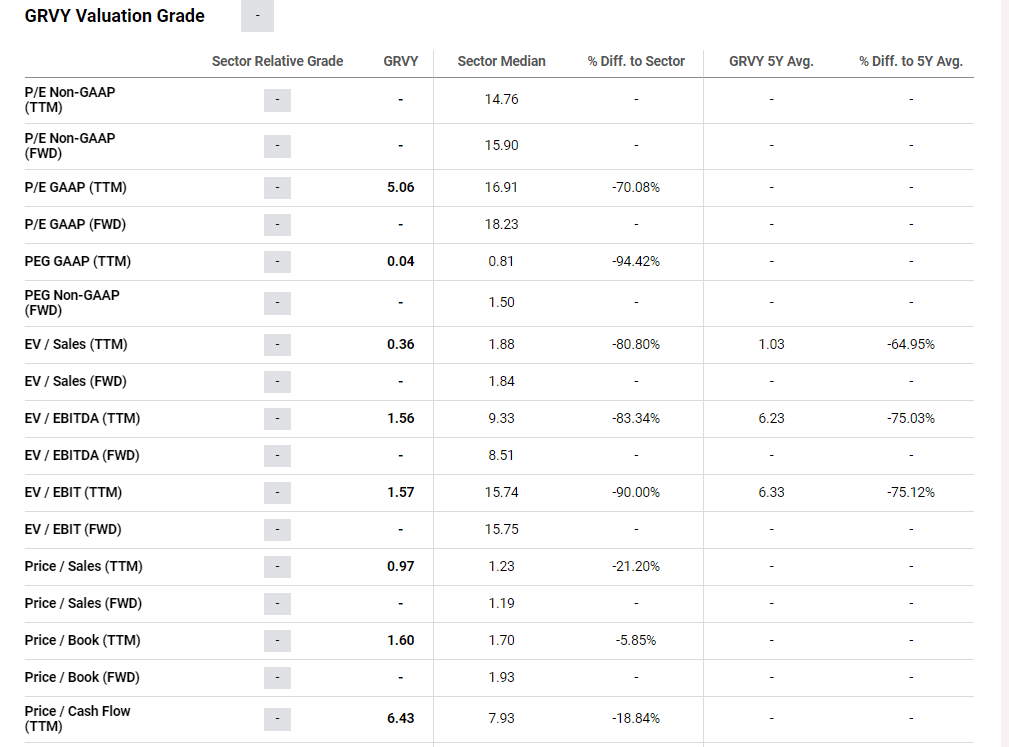

Multiples Valuation: Still undervalued compared to peers

Gravity Co. Valuation (SeekingAlpha)

{kind=link}

Based on Seeking Alpha's Valuation page, Gravity Co, Ltd is trading at a huge discount in all multiples relative to its peers. For example, it is trading at a P/E multiple of 5-6x earnings, well below the industrial average of 15-16x. In addition, its PEG ratio is sitting at a whopping 0.04x, which implies that at the current price, it offers huge growth earnings potential for the stock.

Potential Risks

Despite its strong growth prospect as well as its underappreciated valuation, there are still some underlying risks behind the business that are worth considering before you make an investment.

1. Overconcentration of revenue from its Ragnarok Gaming Series

First of all, Gravity Co's revenue is highly dependent on its Ragnarok Gaming Series. As we can see, the past and recent success of Gravity Co Ltd. hinges on the popularity of Ragnarok Online, Ragnarok Origin , Ragnarok X: Next Generation etc. For example, these 3 games accounted for Gravity's total revenue in 2022 by around 70%.

Revenue distribution (2022 Annual Reports (20-K))

{kind=link}

Acknowledging its concentration risks on the Ragnarok gaming series, Gravity Co is planning to diversify its game offerings by acquiring more intellectual properties (IPs) and by developing more game genres. For example, they are planning to launch new games like the Final Knight and Alterium Shift.

2. Fierce competition in the gaming space

Nevertheless, Gravity Co Ltd. faces enormous competition in the mobile gaming space. Gravity Co, Ltd competes not only with other leading Korea-based gaming publishers such as NCSoft Corporation, Nexon Co., Ltd., Netmarble Corp. and Kakao Games, but also foreign publishers such as Tencent Holdings Ltd., Microsoft, Activision Blizzard, EA, Mihiyo Games, and Playrix Holding Ltd as well.

Thus, to win over the support and loyalty of gamers, the management team is focused on enhancing gamers' experience in its Ragnarok games by constantly updating its existing gaming content and offering new gaming content.

Conclusion

Upon deep diving into the company's fundamentals, I think that Gravity Co Ltd is significantly undervalued and it remains well-positioned for future growth, supported by its user loyalty to its Ragnarok Gaming series, its future IP expansion as well as the growing gaming market in Asia as a whole. Its strong balance sheet and revenue growth also makes the company a compelling investment after all.

Given its trading at P/E multiple of just 5-6x, with an astonishing 200 % upside potential, I rate Gravity Co, Ltd as a great "Strong Buy", offering a strong risk-to-reward perspective.

For further details see:

Gravity: Upside Potential From This Overlooked Company