GLDD - Great Lakes Dredge & Dock: An Interesting Infrastructure Play

2023-07-11 17:10:44 ET

Summary

- Shares of dredging services provider Great Lakes Dredge & Dock Corporation have fallen over 40% since YE21 as the federal government bid market inexplicably dried up in FY22.

- Despite the obvious need for its services and an improved bidding market environment versus FY22, the company is not expected to return to profitability in FY23.

- With negative Adj. EBITDA generated over the past 12 months and net debt of $339.2 million versus a market cap of $545 million, the recent insider buying merited further investigation.

- A full investment analysis follows in the paragraphs below.

Fidelity purchased with money, money can destroy ."? Seneca.

Today we look at a small infrastructure concern. The company recently won a couple of nice contracts and has had some recent insider buying. An analysis follows below.

{kind=link}

Company Overview:

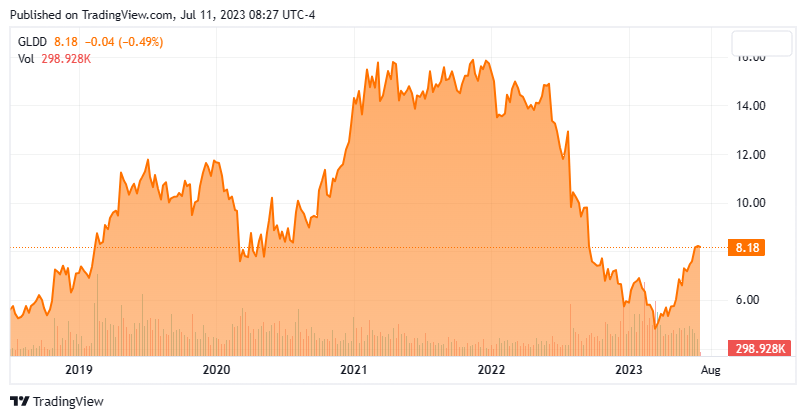

Based in Houston, Great Lakes Dredge & Dock Corporation ( GLDD ) is the largest provider of dredging services in the U.S., employing a fleet of 17 dredges, 17 material transportation barges, one drill boat, and other support vessels. It has been awarded 21 contracts since the onset of 2021 with its largest customer the U.S. government (primarily the U.S. Army Corps of Engineers (USACE), responsible for 67% of the company's FY22 revenue (from 34 contracts). It was founded in 1890 as Lydon & Drews, rebranded to Great Lakes in 1905, and most recently went public in 2006 when it merged into special purpose acquisition company Aldabra Acquisition Corporation, with its first trade conducted at $5 per share. Its stock trades just above at $8.00 a share, translating to a market cap of $545 million.

May 2022 Company Presentation

Dredging Market

Dredging consists of four primary types of contract work: capital; coastal protection; maintenance; rivers and lakes.

May 2022 Company Presentation

Capital dredging programs are predominantly port expansions, coastal restorations, land reclamations, and construction projects (e.g., canals), as well as trench digging for pipelines, tunnels, and cables. This work is an area in which Great Lakes dominates, commanding 49% of the domestic capital bid market share over the past three years. Capital dredging accounted for 53% of the company's FY22 top line.

Coastal protection work- essentially moving sand from the ocean floor to the shoreline to combat beach erosion - is Great Lakes' other strength. The company owned 54% of the domestic coastal protection bid market share over the prior three years. This work was responsible for 30% of the company's FY22 revenue.

Maintenance work involves the removal of silt, sand, and other accumulations to re-deepen channels and other capital dredging projects. Great Lakes "only" commanded a 17% share of the domestic maintenance market over the past three years, providing it with 15% of its FY22 top line.

Rivers and lakes are not as big a market opportunity, with Great Lakes' 17% domestic market share since FY20 providing it with only 2% to 3% of its revenue during that period.

Overall, its average total market share of 35% over the past three years is larger than that of the next two largest market participants: R.B. Weeks (21%) and Manson Construction (9%).

Great Lakes is also moving into the offshore wind market, seeing an opportunity to provide scour protection installation (i.e., preventing underwater soil erosion around the foundations of a structure). The company is contracting the construction of a $197 million rock installation vessel to support its scour protection contract for Empire Wind offshore wind farms off New York, slated to begin in 1H25.

The total domestic dredging market was ~$1.8 billion in FY21, consisting primarily of the USACE putting work up for bid and (in most cases) awarding it to the lowest bidder. However, most of the anticipated FY22 work was not put out for bid.

Challenging FY22

As a profitable concern (GAAP basis) on revenue between $711.5 million to $733.6 million during 2019-2021, there was nothing at the onset of FY22 to indicate that it would be any different. Viewed as essential work during the pandemic, Great Lakes wasn't initially affected by the shutdown of the economy and ended FY21 with a total contract backlog of $551.6 million, off 6% from a pre-pandemic level of $589.4 million in FY19. Furthermore, the USACE budget was at a record $8.3 billion.

The pandemic effects were felt in FY22, as the company was impacted by a confluence of events, the most important of which was a delayed bid market, with 40 expected contracts not put out for bid, the market size shrunk by ~50% in 1H22 vs. 1H21. As a result of these developments, Great Lakes was compelled to cold stack two major dredges, while retiring a 42-year-old hopper dredge. Many of the projects in question were of the large port deepening variety, which impacted not only fleet utilization, but also the company's bottom line as they were somewhat replaced with low-margin maintenance work. Also hurting the bottom line was significant weather-related delays on projects throughout the year, high inflation (dry dock and labor costs), supply chain issues that deferred scheduled dry docking of some of its fleet - resulting in delayed reentry into projects - and unanticipated conditions at several sites that made work significantly more challenging.

Thus, after earning $0.75 a share (GAAP) and Adj. EBITDA of $127.4 million on revenue of $726.1 million in FY21, the company lost $0.52 a share (GAAP) and generated Adj. EBITDA of only $17.0 million on revenue of $648.8 million in FY22. Backlogs plummeted 32% to $377.1 million at YE22, punctuating a disastrous year for a normally steady financial performer.

The biggest effect on the balance sheet was to the cash line, which plunged from $145.5 million to $6.5 million. As such, shares of GLDD fell 61% from YE21 until the time it announced 4Q22 and FY22 financials on February 15, 2023. Owing to persisting uncertainty regarding the federal government bid market, the slide continued with Great Lakes stock eventually bottoming out at five-year lows below $5 a share in March 2023.

Q1 2023 Financials & Bid Market

That ambiguity was not completely put to bed when the company reported 1Q23 financials on May 2, 2023, although it did produce a better than expected stanza. Specifically, Great Lakes posted a loss of $0.05 a share ((GAAP)) and Adj. EBITDA of positive $10.2 million on revenue of $158.0 million versus a gain of $0.17 a share ((GAAP)) and Adj. EBITDA of $29.7 million on revenue of $194.3 million in 1Q22. Although net income fell by $13.3 million, Adj. EBITDA by 66%, and its top line by 19% versus the prior year period, the bottom line was $0.16 better than Street expectations while the top line was $5.0 million better.

The company was busy - in terms of fleet utilization - during the quarter, but low-margin maintenance projects accounted for 46% of its top line. Furthermore, backlog continued to plummet, down 13% sequentially and 31% year-over-year to $327.1 million. Higher-margin capital and coastal restoration projects only comprised 55% of its backlog on March 31, 2023, as compared to 93% of a much larger pie ($473.5 million) on March 31, 2022.

On a positive note, management announced that it was the low bid on the Freeport Capital Port Deepening project, which at $160 million represents the third-largest domestic capital project in the company's history. Great Lakes was also the low bid on a $90 million coastal protection project in the Northeast. If both of these projects are officially awarded in 2Q23, work should commence in 2H23. Also, the backlog does not reflect ~$50 million of performance obligations related to the offshore wind projects.

However, even though the total bid market improved $125 million (1Q23 vs. 1Q22) to over $300 million, that run rate still represents a 33% decline from the $1.8 billion total in FY21. No clear explanation has been offered as to why the federal government bid market has slowed considerably over the past year.

Balance Sheet & Analyst Commentary:

Losing money while it has new dredgers under construction, Great Lakes was compelled to draw down $50 million on a revolver, exiting 1Q23 with cash of $32.5 million against debt of $371.7 million. With Adj. EBITDA of negative $2.5 million over the prior twelve months, a net leverage ratio is not meaningful. That said, if the dredging market normalizes - i.e., significantly more capital and coastal protection work put out for bid by the USACE - the company has the capacity to generate as much as $151.1 million in Adj. EBITDA, which it achieved in FY21. Capex, which was $28.7 million in 1Q23, is slated to reach $175 million in FY23.

Although CJS Securities, Noble Financial, and Thompson Davis follow Great Lakes, no analyst has proffered commentary in over a year. That said, on average, they expect the company to lose $0.04 a share on revenue of $655.4 million in FY23, followed by a gain of $0.63 a share on revenue of $760.0 million in FY24.

Board member Ryan Levenson, representing the interests of Privet Fund, purchased 200,000 shares at an average price of $6.09 on May 10th-12th.

Verdict:

With $2.3 billion (of a total budget of $8.7 billion) allegedly set aside for maintenance and modernization of domestic waterways, there is plenty of money for the USACE to spend. Add in $1.5 billion earmarked for coastal resiliency under the Disaster Relief Supplemental Appropriations Act, and it is easy to see why management is more optimistic about its outlook beyond 1H23. The risk-reward is slightly asymmetrical with the company able to generate as much as ~$150 million in Adj. EBITDA in the right bid (and operating) environment. Assigning an EV/Adj. An EBITDA multiple of 8 in that scenario provides a share price of ~$13 (given no change in debt).

That said, owing to the very demarcated amount of business it can perform (due to fleet size constraints), Great Lakes Dredge & Dock Corporation stock should only be purchased for a trade, and not as a long-term investment. Therefore, GLDD makes a decent and small trade for investors looking for more exposure to the infrastructure industry.

That is one of the bitter curses of poverty; it leaves no right to be generous ."? George Gissing

For further details see:

Great Lakes Dredge & Dock: An Interesting Infrastructure Play