GLDD - Great Lakes Dredge & Dock May Offer Recession-Proof Opportunity

2023-04-25 17:32:05 ET

Summary

- GLDD has been beaten down by many things going wrong, seeing its weakest operating margin in 20 years in 2022.

- GLDD is a market leader in an oligopolistic market with barriers to entry due to the Jones Act and high capital intensity. The majority of revenue comes from the government.

- Recent Q1 contract wins suggests things may be stabilizing.

- While it's not yet possible to say if 2023 will be a good year for GLDD, it seems highly probable that the next 1-3 years will see robust improvement.

- A price of $5-$9/share appears fair, and with the price towards the lower end of that range, the setup seems attractive for this defensive stock today.

Great Lakes Dredge & Dock ( GLDD ) may be getting cheap in absolute terms compared to its own history. That's in part because recent results have been poor with falling revenue, a shrinking backlog, narrowing margins and ballooning capex. However, things may now be stabilizing and the valuation is attractive. This company will likely continue to exist, perhaps for decades and current results may represent a relative low-point as we've seen before in 2004 and 2017.

GLDD is an attractive investment in a recessionary environment since over 90% of revenue comes from the government, either Federal or State and Local, and contracts are typically work that has to be done like maintaining ports and coastal areas or making rivers and lakes navigable for shipping.

The Problem

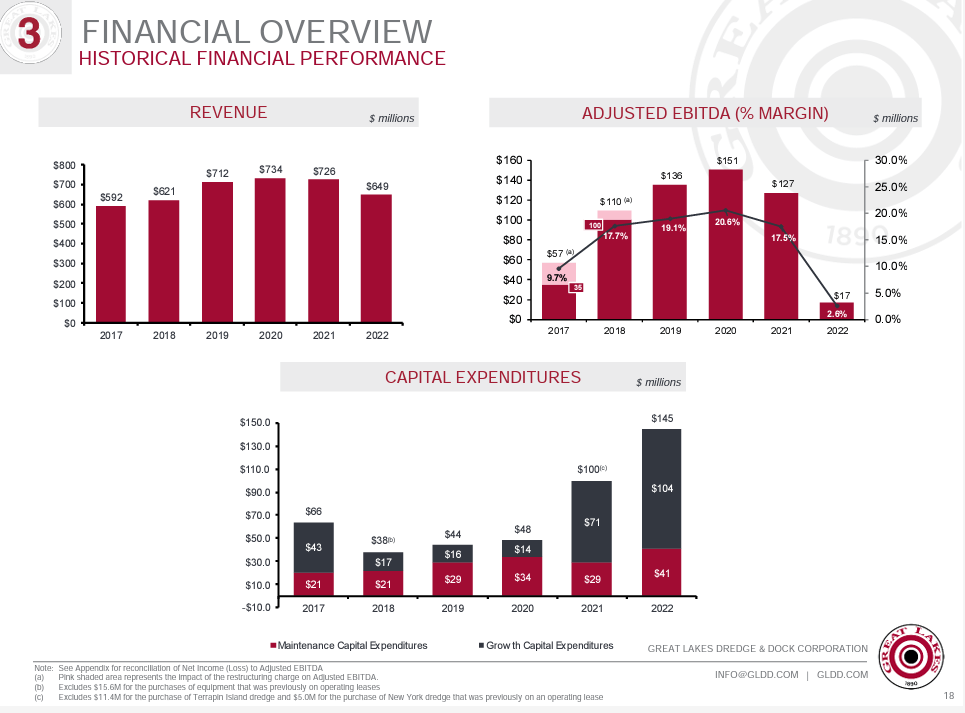

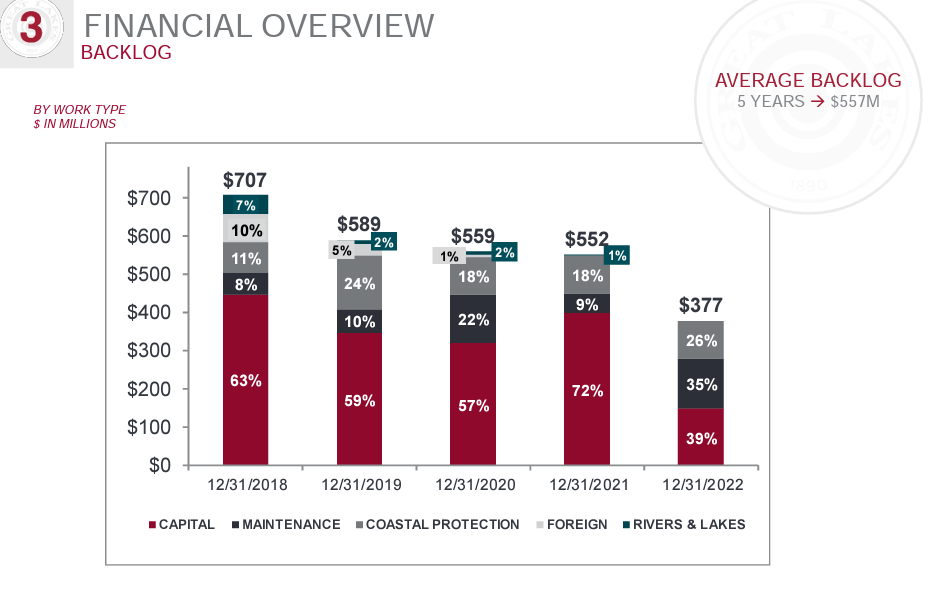

Today, things don't look good for GLDD. Margins appear in decline as revenue falls and capex spikes. The backlog is also at multi-year lows.

{kind=link}

{kind=link}

Why The Backlog Will Improve

However, the backlog seems set to improve. Here's why. On March 20, 2023 the company announced $139M of new project wins . That's not enough to turn around the backlog by itself, in fact it's similar to projected wins in March 2022, an ultimately disappointing year. However, it's substantially ahead of similar announcements in Q1 of 2020 of $72M and Q1 of 2019 of $93M. So it's not enough for investors to get excited, yet, but it does signal that things are not getting worse so far in 2023. A necessary step before improvement. Also, we should note that historically higher revenues have not always meant improved margins, but at this point margins will almost certainly improve from current levels.

Market Structure

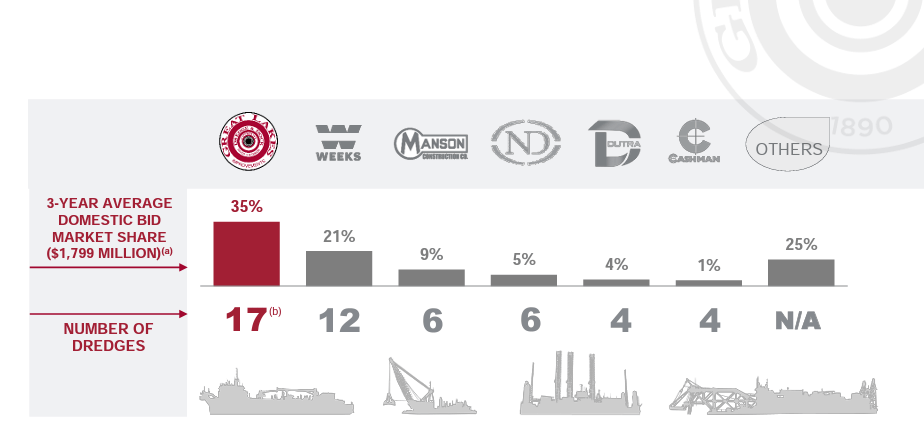

Next let's take a moment to think about market structure. Dredges are very expensive to build, furthermore a rule called the Jones Act (Merchant Marine Act of 1920) means that U.S. built and owned ships must transport goods between U.S. ports. That's a substantial barrier to entry. Few U.S. dredges are being built helping keep supply in check and foreign assets cannot compete on many contracts. That's one reason why I think we can be reasonably confident that GLDD will still be here 10 years from now maybe even 40 years from now in some form, their dredges will still represent a material proportion of the market and should win their fair share of contracts. I don't know if that will be 35% or 25% but it should be around that level given their share of the asset base of ships that can do the work. This implies that for revenue to fall much below 2022 levels, management would have to severely mismanage their bidding strategy.

GLDD Market share overview (GLDD February 2023 Presentation)

{kind=link}

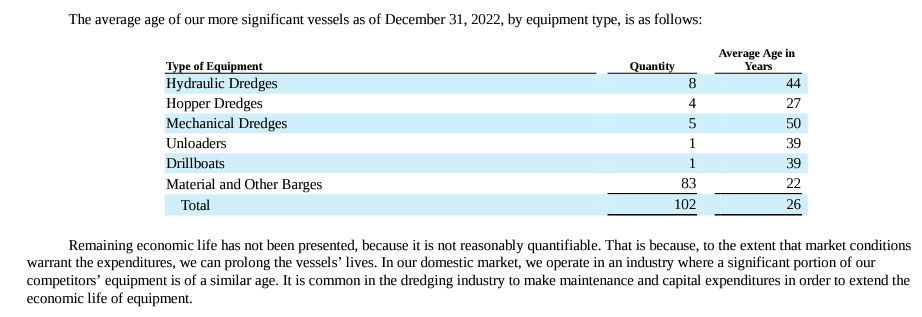

This is different to other industries where market share can change hands relatively rapidly. In order to enter this market you need to commission a dredger and support vessels and then hope for appropriate contracts whilst making sure your enterprise is fully U.S.-based. These challenges imply a degree of predictability for the industry, and if not stellar returns then at least a reasonable return on capital. You may also have to plan for decades, the average age of GLDD's fleet is over 26 years and those ships don't necessarily need to be replaced just repaired over time.

{kind=link}

Long-Term Results

Now let's look at the longer term results over the past 20 years. This offers some comfort that recent results are likely at trough levels at least for margins.

| 20 year max |

| 20 year min |

| 20 year average |

| 2022 actual |

| Revenue Growth |

| +24% |

| -16% |

| ~3% |

| -11% |

| Operating Margin |

| 15% |

| -4% |

| 6% |

| -4% |

The implications are that revenue will likely grow from here over the coming years, and that operating margins will likely trend back to 6% at least. It is notable that operating margins in 2022 came in at the lowest levels in 20 years, I do see that as a nice setup for mean reversion, rather than a signal of impending doom given the relatively attractive, oligopolistic industry structure here.

Valuation

That suggests operating margins should trend back to around $43M as a multi-year average, less $15M of interest costs and a 20% tax rate that's $22M of net income. With 66M shares out at a 15x multiple that suggests a price of $5.09/share . Not too inspiring. Depreciation relative to capex doesn't help much either as capex tends to track depreciation pretty well. However, in recent years under a new CEO, operating income has averaged 9% suggesting $9.09/share might be a more appropriate valuation if recent performance holds.

Alternatively, the company trades at approximately 1x book today and at an EV/EBITDA of 36x actual 2022 numbers, which, of course, seems alarmingly high, though on a normalized basis assuming 6%-9% operating margins I have the company at 6.5x-8x EV/EBITDA today. That compares to an engineering/construction EV/EBITDA of 14x in the current market, though GLDD may have greater capital intensity than some peer firms and I'm not sure using EV/EBITDA here is necessarily warranted.

As a result if operating income does rebound to favorable levels then the stock may offer a return of ~80% on a P/E basis and perhaps almost 250% on an EV/EBITDA basis. In a sense, the current valuation appears to be something of a floor and with some operational tailwinds and market enthusiasm, the stock could perform well over the coming years.

Downside Protection In A Recessionary Environment

Part of the thesis on GLDD is the degree of downside protection in a recession. Revenue here virtually all comes from government contracts which are relatively slow-moving and necessary to support maritime commerce and other key parts of the economy. This means that even in a relatively extreme recession, the economic impact on GLDD should be minimal. In fact, the company might even benefit from lower operating costs such as fuel expenses and staff costs. Therefore, GLDD is one company that could see a rebound in operating earnings over the coming years, even if a recession happens.

Risks

- This is a value investment, and there is no immediate catalyst. Another mediocre year in 2023 or even 2024 is possible causing this investment to be dead money for investors.

- There is always some risk that the business has structurally changed in a way that I'm missing based on 2022 results (and specifically operating margins) being well below historical trend. I believe we are just seeing 'noise' in the results of a business that bids for contracts and has been hit by inflation, weather and dare I say it, bad luck, but if it is now structurally disadvantaged the stock could of course see long-term underperformance.

- Even though the shares are cheap in the $5 range, we have seen them trade lower in the past. However, the Covid low was around $7, so we have to go back to 2018 to find a price below the current level.

- The repeal of the Jones Act which preserves the U.S.-based shipping oligopoly in which the company operates is a risk, but appears unlikely in near-term given the current more protectionist political climate.

- The business is capital intensive and if the ships do reach the end of their economic lives, or need substantial maintenance going forward, that would break the investment case.

- Seeking Alpha's Quant models also have a negative view on GLDD given the negative price performance and earnings revisions over recent months. That's fair, though arguably things may turn for the company over the coming months and years.

Conclusion

For those concerned about a 2023 recession impacting earnings of companies with more discretionary products, GLDDs contrasting focus on the dredging of waterways, almost exclusively under government contract offers welcome relief. 2022 results were so bad, that mean reversion over the coming years seems probable. That may create a compelling setup over the next 1-3 years, regardless of what the macroeconomic forecast holds. A range of $5-$9/share appears reasonable suggesting a good chance of upside assuming operating results improve over the coming years as anticipated.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Great Lakes Dredge & Dock May Offer Recession-Proof Opportunity