GLDD - Great Lakes Dredge & Dock: Turnaround In The Bidding Market Makes It A Good Buy

2023-09-21 12:44:31 ET

Summary

- Great Lakes Dredge & Dock's revenue growth is expected to benefit from recent project wins, entry in the US offshore wind market, as well as bipartisan support for infrastructure funding.

- The company's backlog has significantly increased, indicating a strong bid market and potential for meaningful revenue recovery in Q4 2023 and FY2024.

- GLDD's margins should also benefit from improved utilization in the coming quarters.

Investment Thesis

Great Lakes Dredge & Dock's ( GLDD ) revenue should benefit from a meaningful improvement in the bidding market, which has resulted in its backlog swinging from the lowest in a while at the end of Q1'23 to record highs recently. Additionally, the company's entry into the offshore wind market as well as healthy bipartisan support for infrastructure funding should help the company in the long term.

On the margin front, the company should benefit from improved fleet utilization, cost-cutting measures, and delivery of its more efficient Galveston Island dredger. The valuations are reasonable, and the stock is trading at a discount on FY24 consensus EPS estimates compared to its 5-year historical average P/E ((FWD)). The company’s good growth prospects coupled with a reasonable valuation makes GLDD a buy.

Revenue Analysis and Outlook

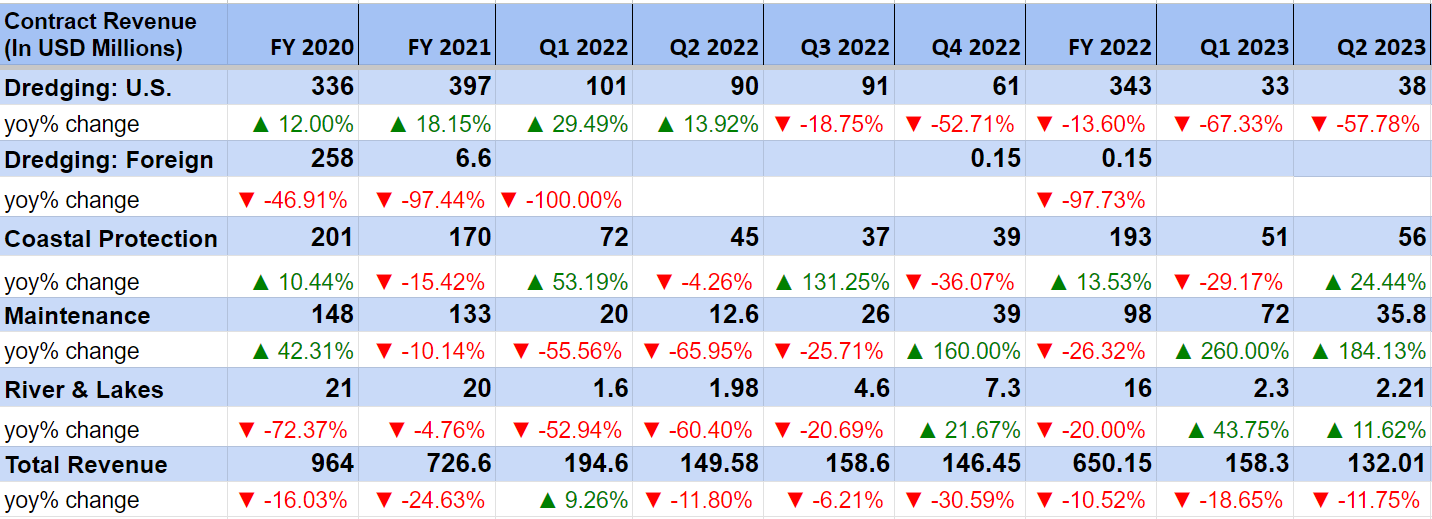

In the last few years, GLDD has faced challenges like post pandemic supply chain disruptions and difficult onsite conditions, weather delays in the Northeast as well as a slow bid market in FY22 which adversely impacted the company’s sales growth. As a result, in the second quarter of 2023, the company's revenue declined 11.75% Y/Y. This decrease was driven by a steep decline in capital projects, partially offset by higher maintenance and coastal protection projects. The company's U.S. capital dredging revenue declined 58% Y/Y while coastal protection revenue and maintenance revenue increased 24% Y/Y and 184% Y/Y, respectively.

GLDD’s Historical Sales (Company Data,GS Analytics Research)

{kind=link}

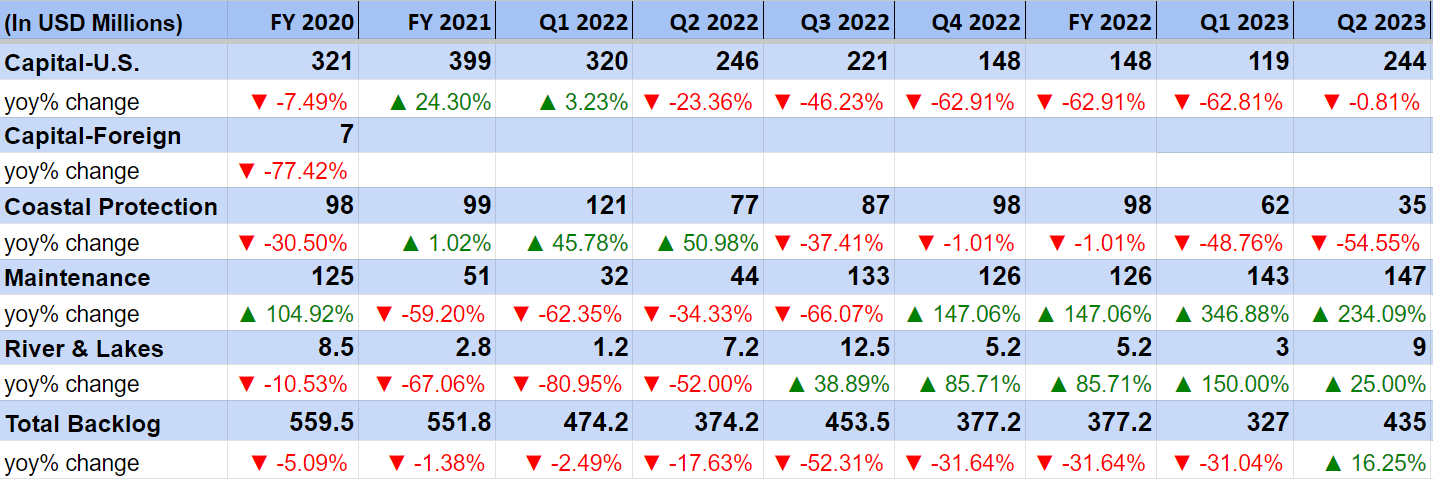

The bid market has shown a remarkable improvement in the last 4–5 months, and the company's backlog has seen a significant increase as a result. The company's backlog improved $327 million at the end of Q1 2023 to $435 million at the end of Q2 2023. According to management's latest update the company has been awarded multiple large contracts post Q2 2023 and its backlog has swelled to $1.1 billion. So, the company has seen an amazing turnaround in the recent months, with its backlog swinging from the lowest in a while to a record high.

GLDD’s Historical Backlog (Company Data, GS Analytics Research)

{kind=link}

Looking forward, with no further regulatory dry dockings or shipyard stays planned for the remaining year and the Galveston Island vessel coming online in the current quarter, the company is well-placed to convert this backlog into revenue and I expect a steep recovery in revenues in Q4 2023 and FY2024.

Longer term, the infrastructure funding environment in the U.S. remains healthy and is getting bipartisan support. In addition to regular maintenance work and small capital projects, there is significant long-term opportunity for GLDD from large multi-billion projects like coastal Texas Program and deepening of New York and New Jersey shipping channels, on which initial studies are being done.

Additionally, GLDD should also benefit from its entry in the offshore wind-market. The company has already been awarded a contract from Equinor ( EQNR ) and BP ( BP ) which involves laying subsea rock installations for Empire 1 and Empire 2 projects. The company's first wind rock installation vessel, the Acadia, will start its operation in 2024, and I believe this business has good long term growth potential. The U.S. Maritime Administration (MARAD) is providing low cost funding for vessels involved in offshore wind projects, and GLDD has applied for the same. This should improve the company's returns from these kinds of projects.

Overall, I am optimistic about the company’s near term as well as long term revenue growth prospects.

Margin Analysis and Outlook

GLDD margins have suffered from lower volumes, high inflation (increase in subcontractor pricing and labor costs), supply chain delays and unfavorable mix (lower capital work which carries higher margins) in recent years. However, in Q2 2023, the company was able to offset these headwinds through improved project performance and cost-reduction efforts like cold-stacking of less-efficient vessels, which resulted in lower operational and maintenance costs. As a result, the company’s gross margin increased 650 bps Y/Y to 13.5% adjusted EBITDA margin increased 570 bps Y/Y to 12.5%.

GLDD’s Gross Profit Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking ahead, the company’s margin prospects appear good, especially starting Q4 2023 as the company’s record high backlog starts contributing to revenue growth and results in improving utilizations. The company has also done a good job in terms of SG&A cost reductions, and management plans to continue focusing on cost reduction by avoiding unnecessary overhead costs even as the business activity improves. Further, the delivery of a new, more efficient Hopper dredger vessel, the Galveston Island, in the current quarter should also contribute positively to the margins.

Valuation and Conclusion

GLDD is trading at a 10.94x FY24 consensus EPS estimate of $0.76 . Over the last 5-years, the stock has been traded at an average forward P/E of 18.57x. Back in 2021 and early 2022, the stock was trading in the mid-teens as the market was expecting the company to benefit from increased infrastructure spending by the Federal Government to stimulate the economy. However, it took the bidding market longer than expected to see the benefit from government spending, and the stock started declining in mid-2022 due to slow bid market conditions last year. With the government spending now flowing through and the company seeing a meaningful improvement in its backlog, I believe the stock can again trade in the low-double-digits/mid-teens levels in the coming quarters. Hence, I see a further upside from the current levels and rate the stock a buy.

For further details see:

Great Lakes Dredge & Dock: Turnaround In The Bidding Market Makes It A Good Buy