LEN - Green Brick Partners: A Second Bullish Update After The Run-Up

2023-03-06 12:17:40 ET

Summary

- GRBK has recorded an impressive 44.9% TTM stock price return, despite broader market selling pressures.

- The company finished a record financial year in 2022, while analysts expect sales and earnings to return to normal in 2023.

- Even after strong gains in 2022, the stock remains attractively valued.

Thesis

Green Brick Partners ( GRBK ) is a company I have covered before and one I have taken a particular interest in over the past couple of years. In a previous analysis on November 21, 2022, I laid out the reasons why I thought 2022 was going to be a year of great performance for the stock. And in fact, it was; despite a broader market decline. In this analysis, I will once again update my thesis for the stock and re-explore its valuation attractiveness after a +29% price gain since November 2021.

Recent Stock Price Performance

Despite interest rate hikes and record low house affordability, The Homebuilder industry has outperformed the market over the trailing 12 months. [[XHB]] has gained 0.4%, when for the same period the broader market has declined -5.0%, in terms of total return. Beating both, GRBK has recorded an impressive 44.9% TTM return, with the stock currently sitting near 10-year highs. GRBK trades at $33.01 ($1.52B market cap) and pays no dividend.

Current State of The Homebuilder Industry

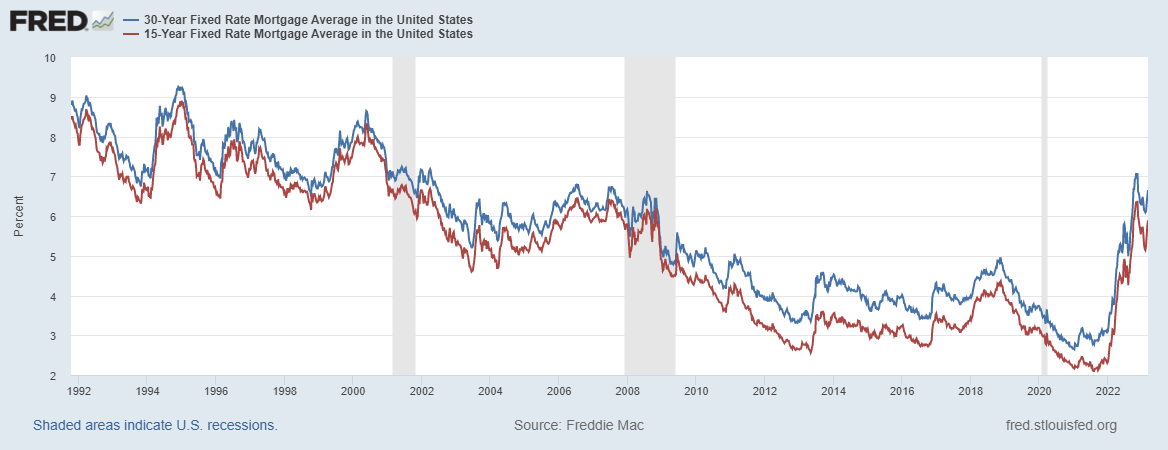

The cost of buying a house has significantly increased over the past couple of years as interest rates increase and demand reaches record levels. Currently, 30 and 15-year mortgages are climbing to the 6% mark, surpassing 10-year high levels. On the other hand, as millennials enter their prime homebuying years, representing one of the largest generations in recent memory, macroeconomic tailwinds remain favorable for the long term. Land scarcity in key growing markets also puts a strain on the supply of homes, leaving companies like Green Brick, that maintains large land capacity in advantageous positions.

{kind=link}

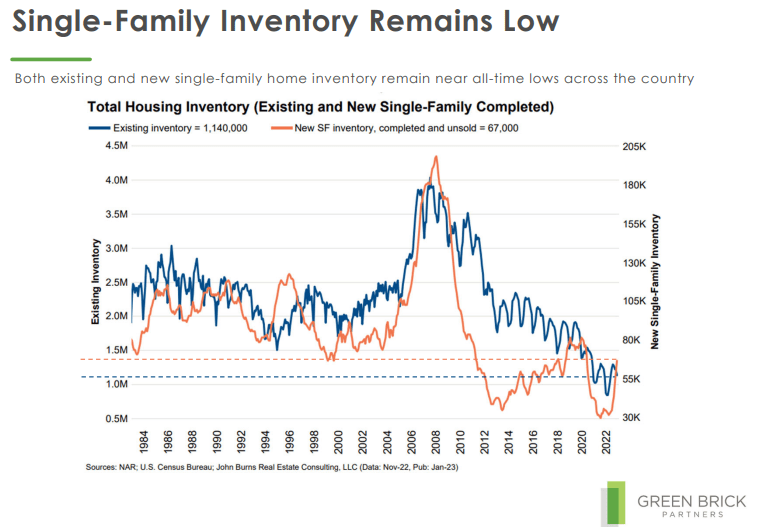

Across the country, house inventory remains low, which means that despite elevated prices and interest rates, demand still exceeds supply. When it comes to single-family homes, where the company specializes in, supply appears also highly constrained, leaving room for sales growth, at least in the mid-term.

{kind=link}

Q4 Results Are Here

On February 27, 2023, Green Brick Partners reported financial results for Q4 2022 and the full fiscal year. The release propelled the stock higher as the company delivered a beat in both GAAP EPS ($1.18 vs $1.14 expected) and revenue ($431.09M vs $359.40M expected). Despite delivering fewer homes compared to Q4 2021 (727 vs 823 homes) the average sale price increased significantly from $509.3K to $589.5K, a number indicative of an expensive housing market given that the company mainly focuses on single-family homes.

For the entire 2022 fiscal year, residential units revenue grew 30.1%, while the average sales price increased 26.3% to $582K. Green Brick finished the year with a record number of delivery of over 2,900 homes.

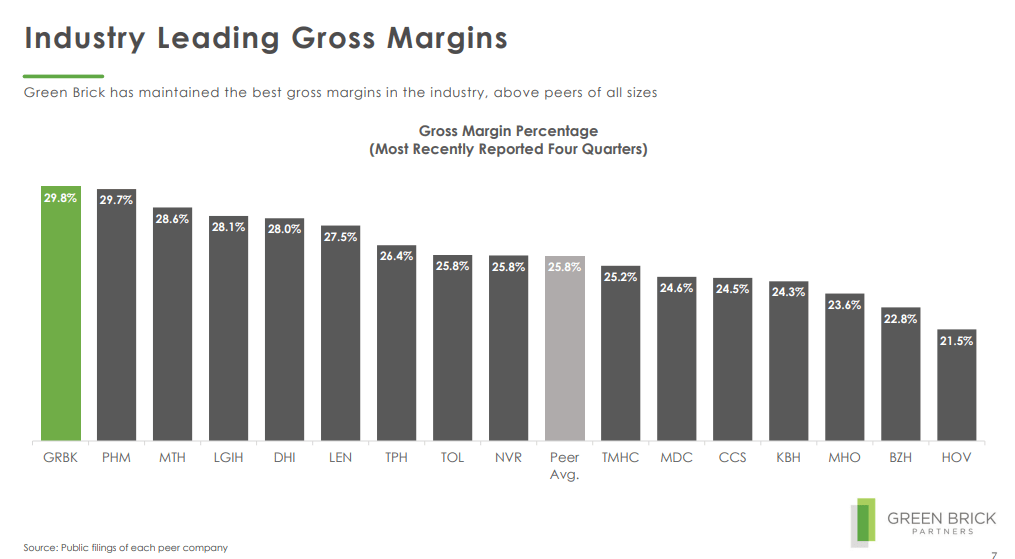

Building on continuous, strong growth performance over the past 5 years, in 2022, GRBK delivered record sales and profit. Return on equity reached an impressive 31% in 2022, increasing aggressively from 19.5% in 2021. The company's gross margin has also increased significantly YoY, reaching an industry-leading 29.8%. GRBK displays stronger profitability compared to a peer average gross margin of 25.8%, while large competitors like D.R. Horton ( DHI ) and Lennar ( LEN ) displaying gross margins of 28% and 27.5%, respectively.

{kind=link}

The markets Green Brick operates in, including Dallas-Fort Worth, Atlanta, and Florida, continue to exhibit strong demographic tailwinds in terms of strong employment, population growth, and domestic migration flows. Home supply constraints in these markets are also relatively favorable to homebuilders.

Green Brick Partners maintains one of the lowest net debt to total capital ratios among peers of 25.7%, which is considered especially low in the homebuilder industry. Liquidity is also strong, with GRBK carrying very high Current and Quick ratios, as well as a $77M cash balance.

Expectations Going Forward

Both management and analysts see sales and earnings declining in 2023 to recalibrate back to normalcy after record years in 2021 and 2022. Management points out, in the recent earning call , that backlog value and units have declined over 50% YoY, a function of both slowing sales and higher cancellation rates across the board. Analysts expect EPS to decline to $3.39 per share and increase again in 2024 to $4.08 per share. Revenue is forecasted to follow a similar trajectory.

{kind=link}

As the company looks to decelerate its land acquisitions in 2023 more cash flow generated by the business will be available to shareholders. Share buybacks and acquisitions will be evaluated carefully by GRBK's management, looking to preserve the impressive return on equity trajectory of the company.

Valuation Revisited

Even though Green Brick Partners has seen a significant stock price run-up since 2021, its valuation metrics remain attractive. Currently, GRBK trades at a 5.47x TTM and 9.75x FWD P/E multiple and a 0.89x TTM and 1.27x FWD P/S ratio. Both metrics position the company's valuation lower than many of its competitors, including D.R. Horton, NVR, Inc. ( NVR ), LGI Homes ( LGIH ), and others, while not significantly exceeding its own historical, 5-year averages. Green Brick also trades at a relatively cheap Price/Book ratio of 1.5x TTM and 1.27x FWD. Overall, the company's valuation can be considered inexpensive.

Final Thoughts

After all things are considered, Green Brick Partners remains in a rather advantageous position in the homebuilding industry, despite an expected slowdown in sales for 2023. The firm's valuation is also still attractive, discounting a large portion of the anticipated declines. For these reasons, I would keep my Buy rating for the stock.

For further details see:

Green Brick Partners: A Second Bullish Update After The Run-Up