GDOT - Green Dot: Current Troubles Are Hiding Future Potential

2023-11-24 02:22:16 ET

Summary

- Green Dot is a FinTech company focused on cash/debit services, targeting the unbanked and underbanked population.

- My overall investment thesis revolves around the potential of GO2bank as a digital bank for the underbanked population.

- GDOT is currently trading at roughly $8.4 which would give the stock a P/E of 4.9x to 5.2x.

Despite the rally in the S&P 500 in 2023, many smaller cap stocks continue to be trading at near-depressed levels. This gives investors who have the stomach for increased volatility plenty of opportunities. One company I'd like to discuss is Green Dot (GDOT).

Understanding the Business Potential

Just a brief background on the company, Green Dot is a "FinTech" company that offers a whole suite of services through its various segments. Based on the company's disclosures , it operates the following segments;

- Consumer Services - consumer checking accounts, prepaid cards, and secured credit cards among others. In particular the "GO2 Bank" which will be discussed in more detail

- Business to Business ("B2B") Services - Focused on licensing the company's technology and cash distribution capabilities

- Money Movement Services - Cash deposit and disbursement capabilities (Pay Card) as well as its tax refund-related financial services

Green Dot (Investor Presentation)

{kind=link}

The way I think of Green Dot and one that sets it apart from other consumer-focused "FinTech" firms is that it is heavily focused on cash/debit and not the credit side of the equation. For example, its retail business is debit cards and deposits focusing on Americans who are "unbanked" or "underbanked". The company also helps facilitate tax refunds and other benefits for this population. It's basically a poor man's SoFi (SOFI).

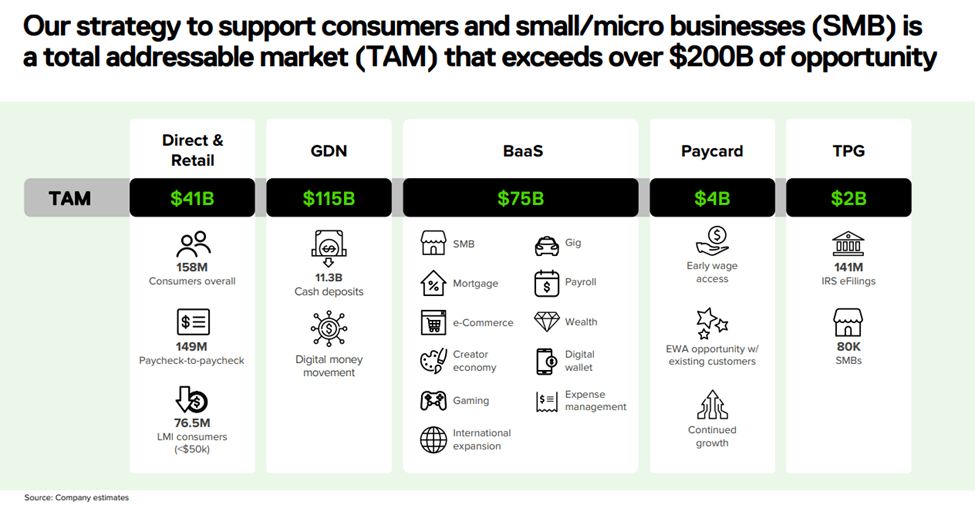

Given these unique capabilities and set of assets, the company has several key areas for growth. In its latest investor presentation , the company has highlighted a total addressable market ((TAM)) of greater than $200 billion.

Green Dot TAM (Investor Presentation)

{kind=link}

One of the key advantages that Green Dot has over a lot of other FinTech companies is that it owns its own bank, Go2Bank. If you recall the hype that was surrounding SoFi as it acquired its own bank charter then you would realize how important this is. Being able to use deposits to fund loans, is a major growth driver for FinTechs and that's a hurdle that Green Dot has already cleared.

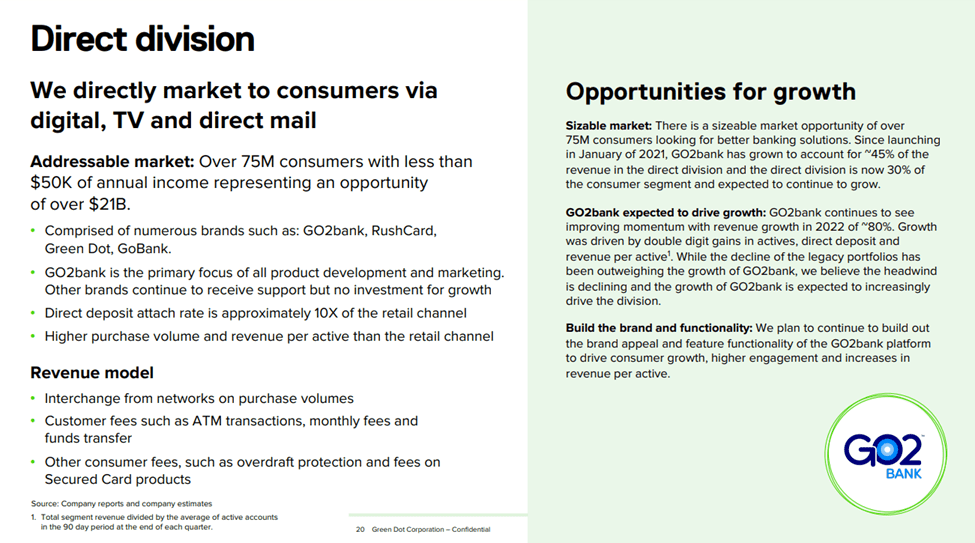

GO2bank will be the Primary Driver for Future Growth

Green Dot operates a whole host of brands and programs. One of the challenges of the new CEO is to streamline the company's offerings and operations. This involves sunsetting a lot of the company's old products and moving customers to GO2bank. This explains why the Consumer Segments saw a decline of 14.5% in Q2 2023 and 20% in Q3 2023.

My overall investment thesis revolves around the potential of GO2bank as a digital bank for the underbanked population. With poverty still remaining high in the US, there is still a huge population without sufficient access to traditional banking institutions.

In the last two quarters, GO2bank has shown remarkable growth. In Q2 2023 direct deposit accounts up were up roughly 40% . Unfortunately, Q3 2023 has seen direct deposit growth slow to just over 20%.

This growth although relatively solid is disappointing to see. It's something to keep watch on for the next few quarters as the company cannot afford to have deposit growth stall. The company has multiple retail partners, including all the household names, totaling approximately 90,000 locations. Therefore, in theory, Green Dot has the distribution reach to grow Go2bank's deposit base.

GO2bank (Investor Presentation)

{kind=link}

Q3 Results and Valuation

Green Dot's revenues have remained roughly flat reflecting the pivoting of its business. Net Revenues grew by 2.7% in Q3 2023 from $343.7 million to $353 million. Year to date had similar results with Net Revenues growing by 2.5% from $1.1 billion in 2022 to $1.135 billion.

Not surprisingly the segment that lost revenue the most was its Consumer Services segment which saw Gross dollar volume drop from $6.6 billion in the start of 2022 to $4.6 billion. This was mostly due to the sunsetting of other business units as discussed. Green Dot's updated guidance for revenues for the full year of 2023 is between $1.465 billion to $1.48 billion, which is flat compared to the $1.47 revenue of 2022.

In terms of valuation, the company expects its adjusted EBITDA to be between $170 million to $175 million which is roughly a 7% decrease compared to previous guidance. Green Dot has reduced its EPS guidance as well to between $1.62 and $1.69 for full-year 2023 compared to its original guidance of $1.80 and $1.90.

The change in these guidance numbers has caused a massive sell-off in the stock. GDOT stock fell by 33% that morning of trading which in my view was grossly overdone. As of writing, GDOT is currently trading at roughly $8.4 which would give the stock a P/E of 4.9x to 5.2x. This is a pretty cheap valuation considering that larger peers like SoFi and Affirm ( AFRM ) aren't even profitable yet.

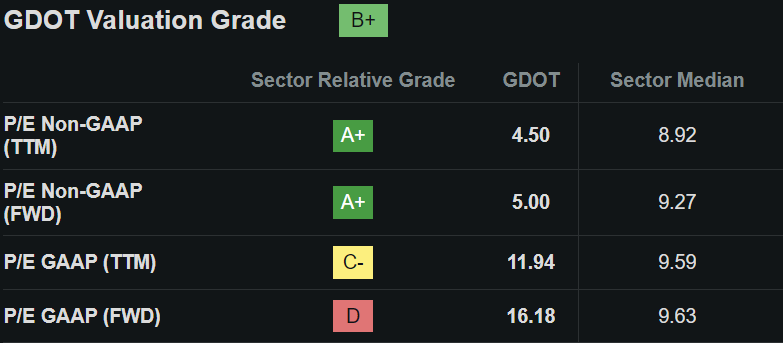

Seeking Alpha's valuation metrics has the company at a B+. The score would have been much higher strictly using non-GAAP figures. Given that the company is in the midst of a restructuring (as discussed above), non-GAAP earnings might be a more appropriate measure in my view. The company has also expressed that the drop in earnings and the reduced guidance could be transitory in nature as mentioned in the company's earnings call .

Though we made progress on our major strategic goals, these results were below our internal projections due to a variety of transitory factors. We have had a lot going on this year. We deconverted several partners, we sunset legacy brands within our direct-to-consumer business to invest in and GO2bank, and we were impacted by increasing interest rates due to partner interest sharing arrangements negotiated in a zero interest environment.

Quant Valuation (Seeking Alpha)

{kind=link}

Key Risks

As a small-cap that has lost more than half of its value in recent weeks, it wouldn't be prudent of me to not discuss the risks associated with Green Dot. There are a few key risks that I see. The main one is concentration risk. Green Dot has a handful of very important partners in its retail distribution and tax refund business.

In its retail distribution, Green Dot's largest partner is Walmart (WMT) through its "Walmart Money Card". This partnership accounted for 17% of total revenue in Q2 2023 and 19% of revenue in Q3 2023.

The main risk is for Walmart to either go at it on its own or find another partner. Green Dot's diversifying revenue means that this risk is slowly going down. The concentration of the Walmart partnership vis-à-vis Green Dot's business was much higher in previous years. Walmart's distribution represented approximately 21%, 24%, and 27% of total operating revenues for the years 2022, 2021, and 2020, respectively. Green Dot's Walmart partnership is set to end on January 2027.

The same concentration risks also exist for Green Dot's tax refund business which is highly dependent on a small number of tax preparation companies. The company does not have any sort of long-term contractual agreements. There is a lot of uncertainty will this revenue stream. In particular, the company's relationship with Turbo Tax maker Intuit (INTU) is a critical one.

The other issue that Green Dot faces is with regard to execution. In August this year, there have been multiple reports of customers unable to access their funds. This technical difficulty persisted for days leading to multiple complaints to the regulating authorities. What makes this worse is that a huge chunk of Green Dot's customers live paycheck to paycheck. Therefore not having access to their funds can cause severe emotional stress or financial hardship.

Conclusion

Despite these risks, I believe that Green Dot's stock is still something for investors to consider. The company is in the midst of restructuring its business in order to capture future growth. Go2bank is well positioned to be a "Fintech app" similar to SoFi and other digital offerings. Finally, the company is profitable and the stock is trading at depressed valuations.

I believe that Green Dot could warrant a speculative buy for investors willing to be patient (while the growth and turn-around story plays out) and accept the stock's volatility.

For further details see:

Green Dot: Current Troubles Are Hiding Future Potential