GPRE - Green Plains' Future Looks Bright

2023-03-21 11:37:26 ET

Summary

- In this article, we discuss one of America's largest ethanol producers, Nebraska-based Green Plains.

- While 2022 was a tough year due to terrible margins, the company is about to see a major rebound thanks to high volumes and its value-adding production technologies.

- On top of that, it benefits from new ethanol regulation, the Inflation Reduction Act, and long-term partnerships.

Introduction

It's time to talk about ethanol, as I haven't covered Green Plains Inc. ( GPRE ) since August 2022. This Nebraska-based ethanol giant is currently struggling with low ethanol margins, which has led to the partial curtailment of production. Moreover, high costs have added to the failure to generate a positive operating result at the end of 2022. Nonetheless, the company is on track to boost higher-margin production as it benefits from positive ethanol developments in Washington D.C., and decarbonization projects.

So, in addition to discussing the company's attractive valuation and stock price characteristics, we'll cover interesting ethanol fundamentals, that shed some light on the bigger picture in North American agriculture.

Investors Wait For New Tailwinds

The (future) drivers of profitability & why GPRE has been struggling.

GPRE has gone sideways since entering the volatile sideways trend between $40 and $25 in early 2021. While the stock's performance isn't something to write home about, it has refrained from entering another downtrend after breaking a seven-year downtrend in the last quarter of 2020.

FINVIZ

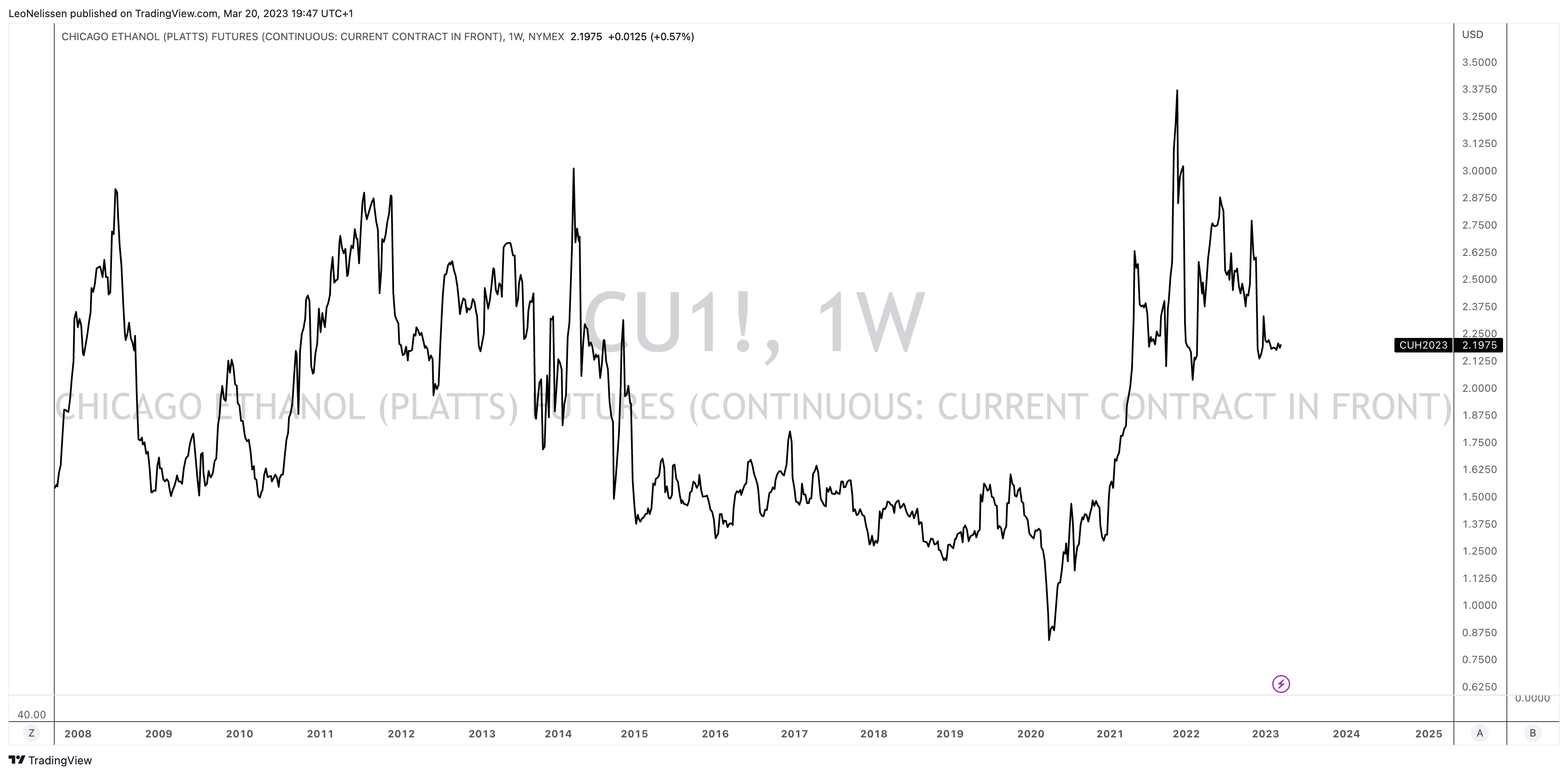

We're now in a situation of elevated commodity prices and high energy demand. Both tend to be bullish for ethanol producers.

As the chart below shows, ethanol prices are still elevated, despite retreating from their 2021 highs. Chicago ethanol futures are still roughly 50% above the pre-pandemic median.

{kind=link}

TradingView

With that said, it's not that straightforward. For example, we cannot compare an ethanol producer to an oil company when it comes to the impact of commodity prices on operating income. After all, ethanol producers need to buy corn to produce ethanol. Oil companies pump oil out of the ground.

Producing ethanol is based on finding a balance between input and selling prices.

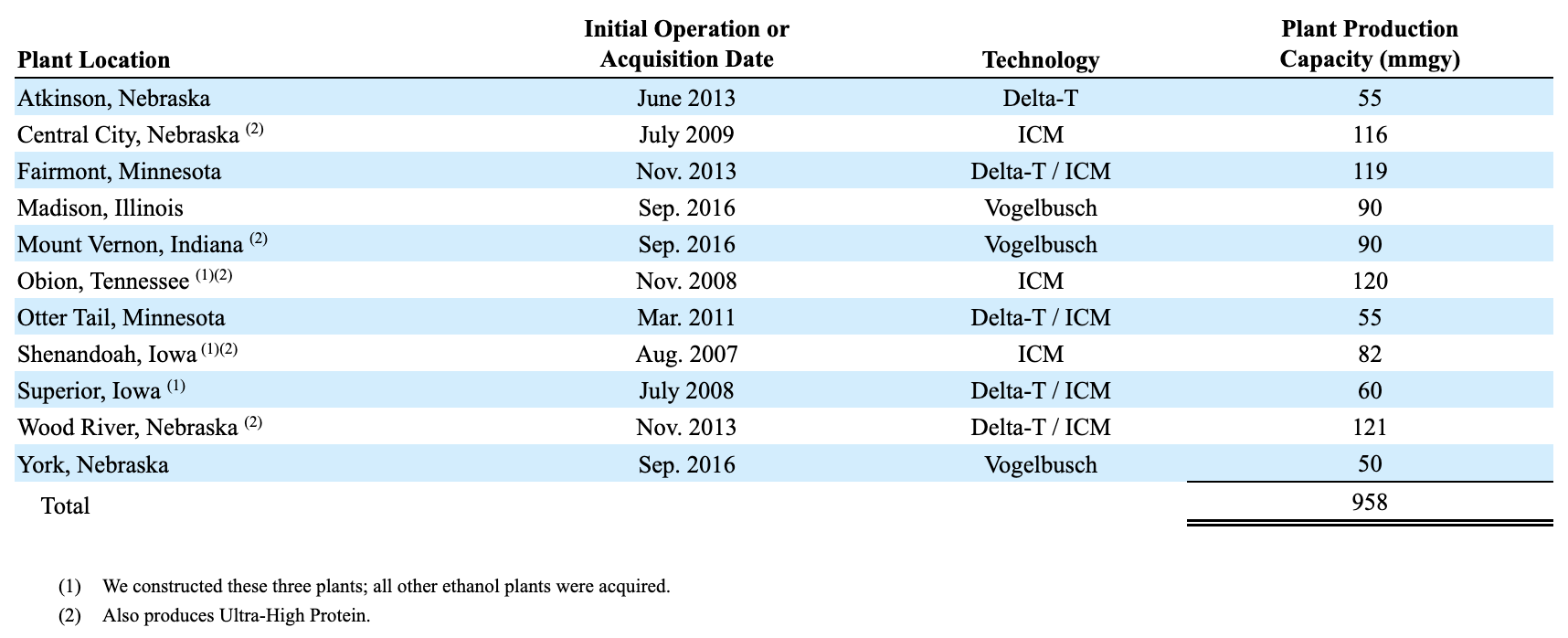

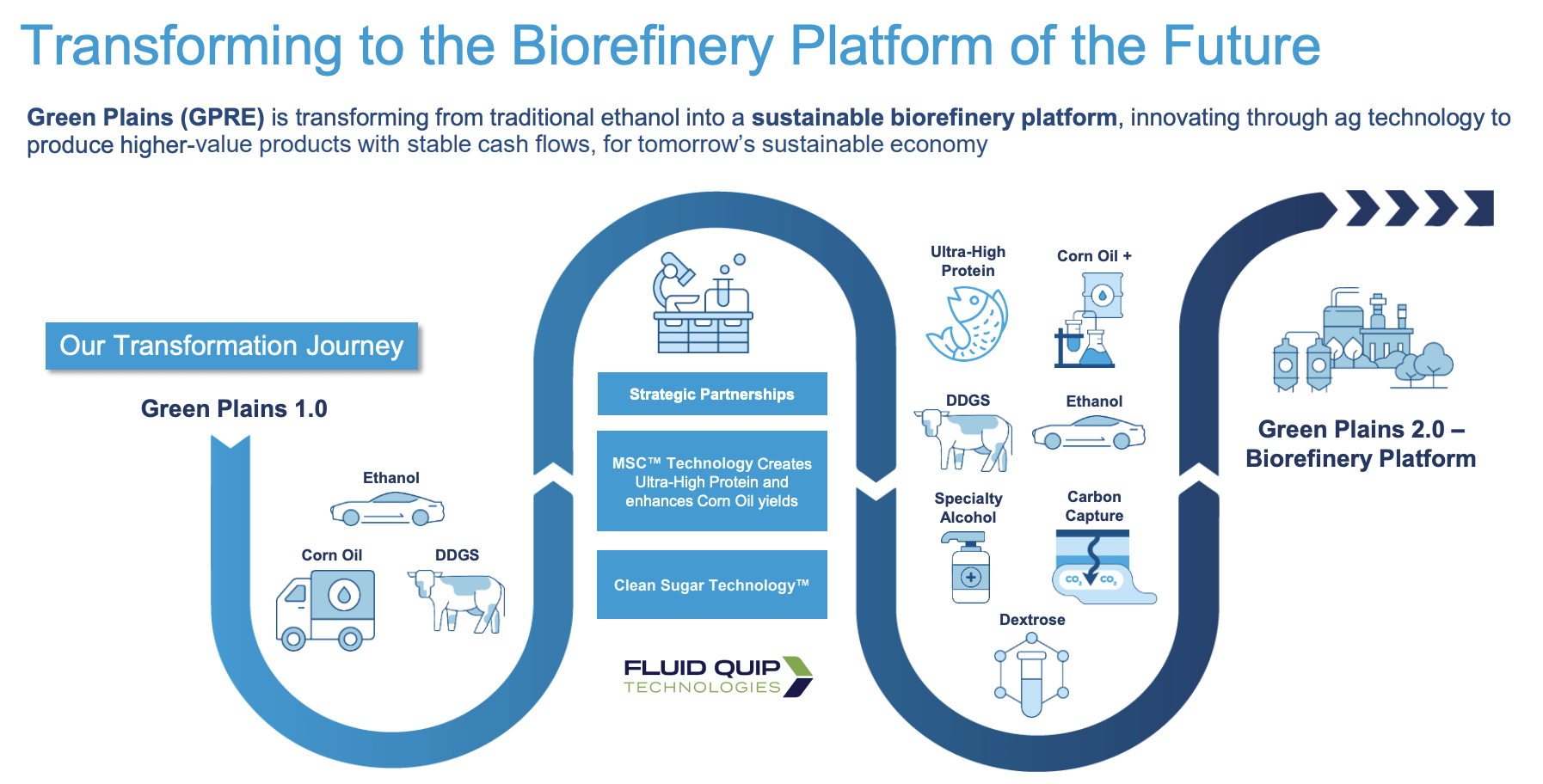

Green Plains owns eleven ethanol plants in six states. These plants produce ethanol and by-products like distillers grains, ultra-high protein, and renewable corn oil.

Its total capacity is 958 million gallons per year.

{kind=link}

Green Plains

On average, a 56-pound bushel of corn produces roughly 2.9 gallons of ethanol, 17 pounds of dried distillers grains, and 0.6 pounds of corn oil.

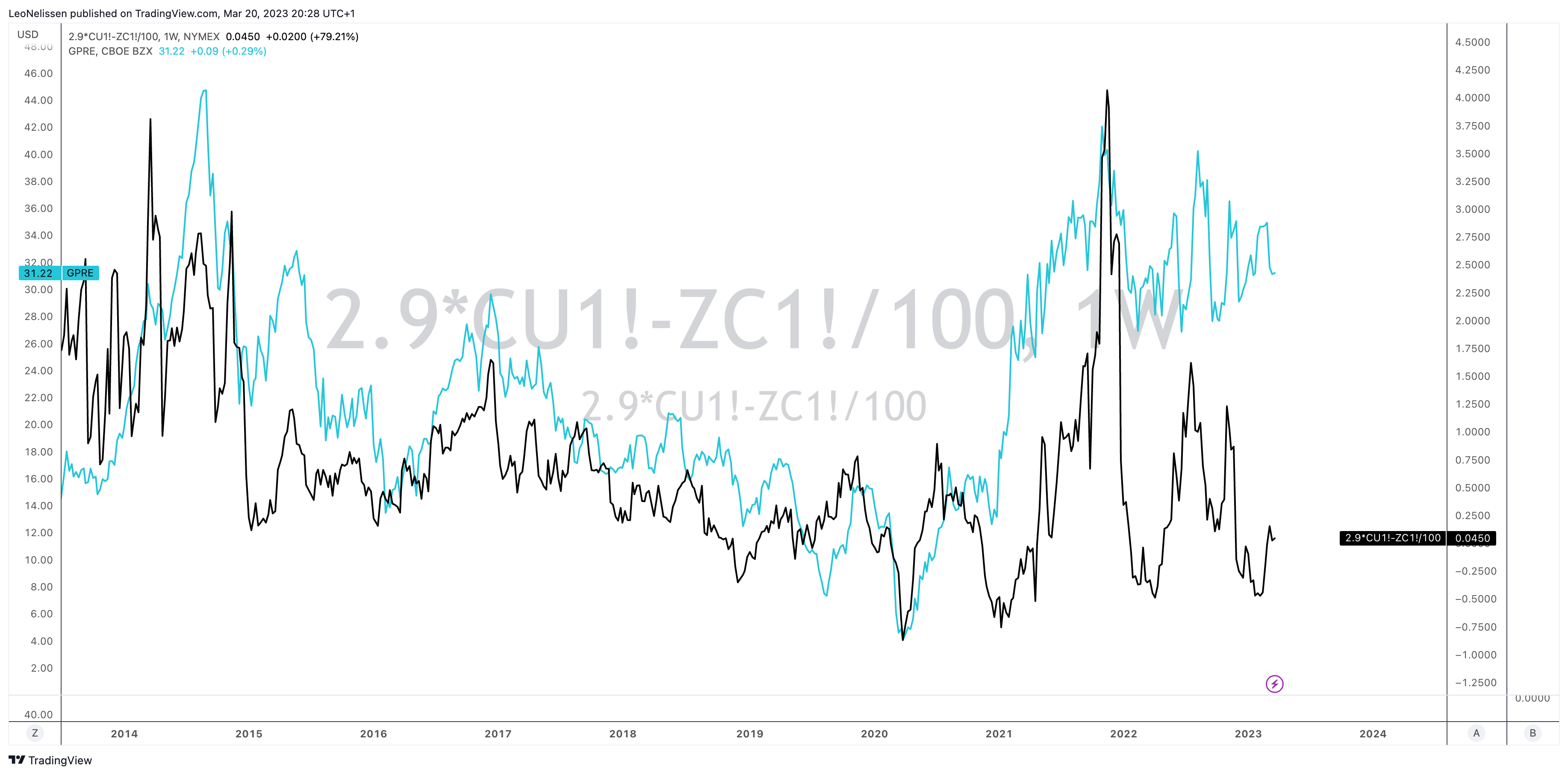

The chart below compares the GPRE stock price (the blue line) to an ethanol production margin proxy I made. The black line displays the price difference between a bushel of corn and 2.9 gallons of ethanol. It does not take by-products into account. Distiller grains futures have been discontinued.

Moreover, companies usually hedge input costs and selling prices.

While these numbers need to be taken with a grain of salt, the bigger picture is important. Right now, ethanol margins are weak in the industry. In other words, this is the main difference compared to the chart that only showed the price of ethanol.

{kind=link}

TradingView

With that in mind, GPRE's financial numbers reflect these developments.

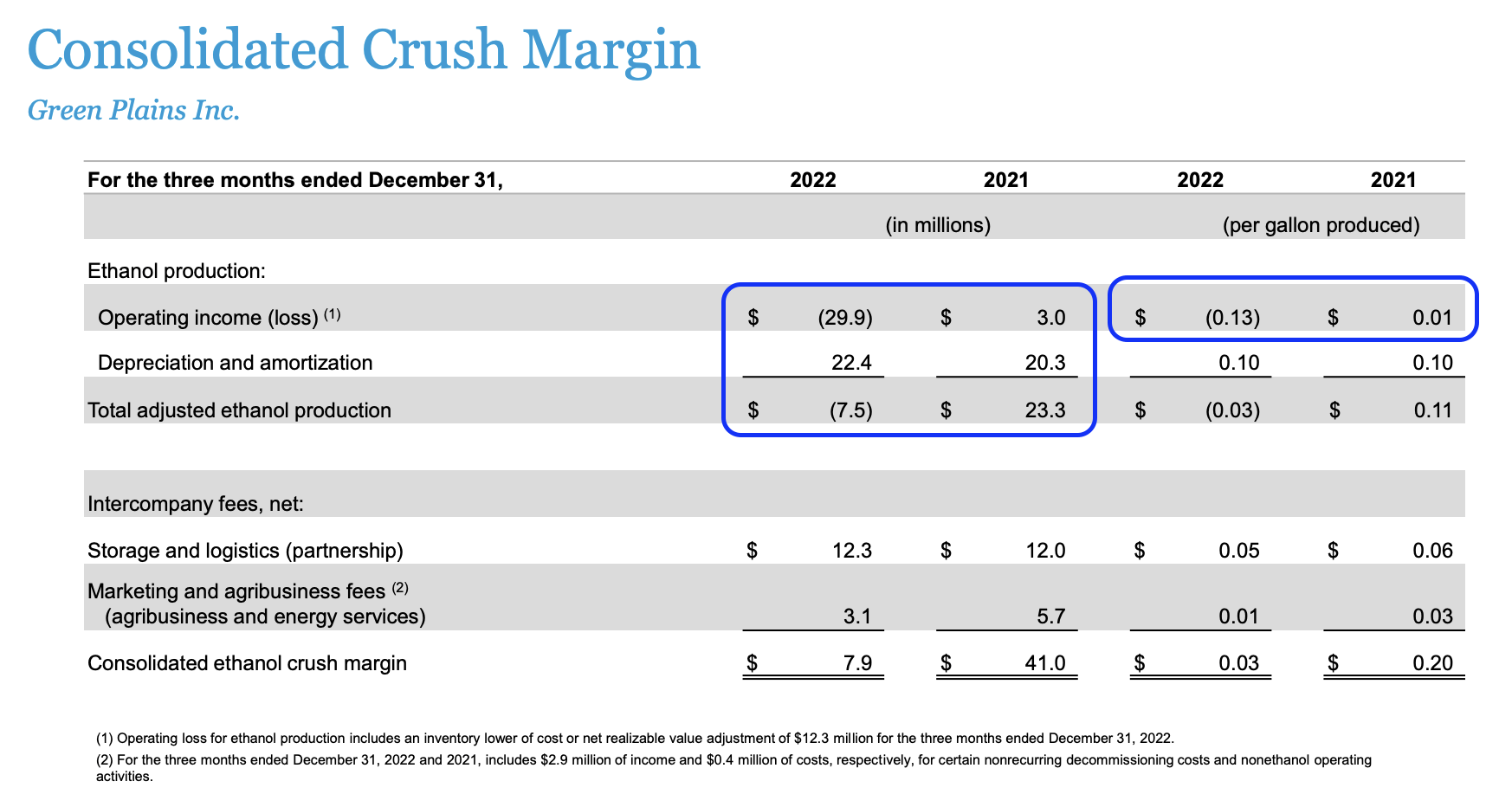

In 4Q22, the company produced 225 thousand gallons of ethanol, excluding its by-products. In 4Q21, production was 201 thousand gallons.

Unfortunately, the company lost $7.5 million after taking depreciation into account. In 4Q21, the company's operations generated $23.3 million in operating profit. This is based on a loss of $0.13 per gallon of ethanol. In the prior-year quarter, the company made a penny on each gallon it produced.

{kind=link}

Green Plains

President, CEO, and Director Todd Becker highlighted the operating issues related to high input prices and operating challenges.

"In the Western Corn Belt, the basis remains stubbornly high for this time of year, about $0.45 per bushel higher than the prior five-year average and $0.30 higher than the prior year . A severe cold snap in December caused outages across our platform , and when combined with rail embargoes , which hit Green Plains unusually hard, we had inventory backed up at some of our locations leading to plant slowdowns and some plants going offline for a period of time. We estimate the storm cost our platform around $0.02 per gallon for the quarter alone, just over those few weeks."

Moreover, the company made the decision to temporarily idle 10% of production capacity based on current market conditions. Despite these challenges, the company had a 93% utilization rate across its platform, as it benefited from pulling its seasonal maintenance into the third quarter.

That said, in 2021, GPRE bought Fluid Quip, a company that allowed it to implement an MSC protein technology, resulting in higher protein and corn oil quality and quantities. In other words, instead of just producing ethanol and low-quality by-products, GPRE was able to produce products that go higher up the value chain (higher margins).

So far, the company is seeing evidence that this strategy is bearing fruit.

With that said, I'll give you a look under the hood a bit. Since the inception of the strategy, we indicated that our belief was the base product would sell for a premium of $200 over traditional distillers low protein products, and I'm happy and excited to report we have exceeded this target since inception over the average of the sales book. This is fully consistent with our initial outlook and guidance.

{kind=link}

Green Plains

In 2022, the company completed the construction of three additional MSC technology locations. It now has five MSC locations, and it is breaking ground on its first clean sugar facility in Shenandoah, Iowa.

Furthermore, GPRE announced a sustainable aviation fuel partnership with Tallgrass, PNNL, and United Airlines (UAL ) based on a new alcohol-to-jet fuel technology. On top of that, the company is starting to work on carbon initiatives to utilize carbon from its Southeastern location to produce synthetic fuel and methane products.

Needless to say, these technologies are more important than ever, as the company is struggling with low ethanol margins, as we already briefly discussed. This is what CEO Becker said regarding the importance of this transition:

Today, the fundamentals of our base ethanol business remain challenged, yet as we all have seen things move quickly on our margin structures. We remain open to the forward margin as there has not been real opportunities to hedge forward.

There are times I feel like a broken record, which is why our technology transformation is more important than ever.

Hence, it is beneficial that GPRE is getting some (indirect) help from the government.

- The EPA proposed an RFS (renewable fuel standard) of 15-25 billion gallons per year, as it is pushing for higher ethanol blends.

- This proposal aims to allow the sale of E15 during the summer for the fourth straight year.

- E15 is only available at fewer than 2,700 gas stations in the United States.

Bloomberg

On top of that, last month, the governors of various corn-producing states, including Iowa and Minnesota, started pressing the EPA to stop giving E10 a pass from the volatility requirements in their states. This would put both E10 and E15 on the same footing. In other words, it would be great for ethanol sales.

Needless to say, it's a no-brainer for these states to push for these rules, as it would be great for their farmers and the entire supply chain connected to it. Moreover, I believe that it would also be great for President Biden (and Democrats in general), given that we're about to enter a heated election cycle. Votes in the Midwest are key.

The problem is that this comes with challenges. If Midwestern states are going to push for E15 regulations, it will force other states to follow. After all, the American energy infrastructure is based on providing the same fuels for all states. If that were not the case, producers and pipeline companies would encounter serious challenges.

So, essentially, we're about to enter a period where ethanol demand is about to be boosted. If the Midwest pushes for E15 in a situation where it is allowed to be sold all year, producers will adapt. It will likely end up being the case in other states as well, and benefit producers like Green Plains.

With that said, the company is very upbeat when it comes to the Inflation Reduction Act, which is expected to boost the company's margins in the years ahead. Related to that act, the company also stressed the significance of alcohol-to-jet sustainable aviation fuel as the future of the industry and highlighted a recent development in Illinois. The state has passed a new $1.50 per gallon SAF blender credit on top of the IRA. Green Plains believes that their low-carbon alcohol and waste oils produced for the renewable diesel industry provide a ready-made solution for the aviation industry's need for decarbonization. These could be converted into SAF in the future, making both vegetable oil-based and alcohol-based sustainable aviation fuels important in reducing aviation emissions.

So, what does this mean for the valuation?

Valuation

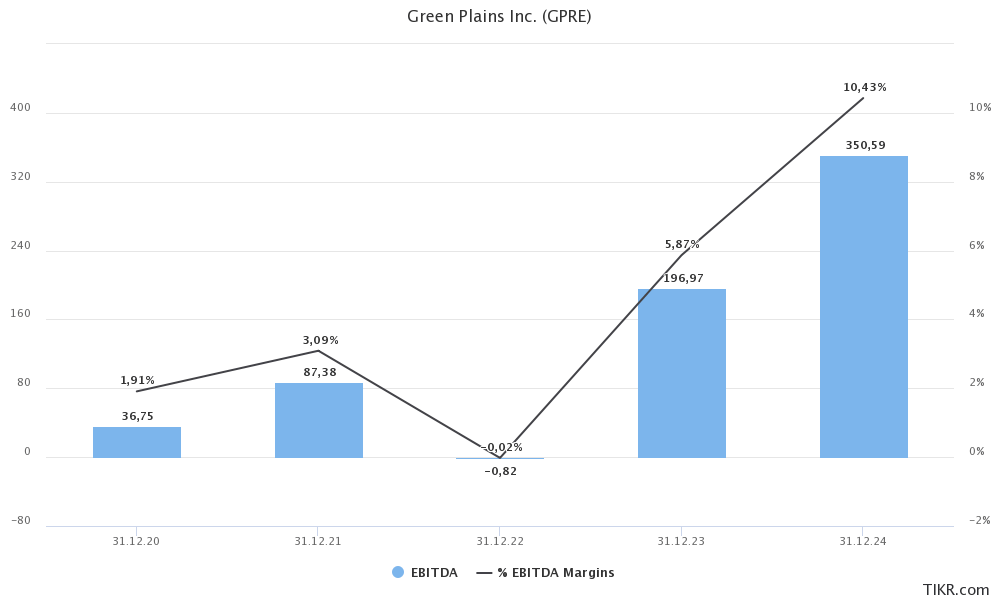

Analysts are buying the GPRE rebound thesis. This year, the company is expected to do close to $200 million in adjusted EBITDA. That's more than twice what it did in 2021. In 2024, that number could rise to $350 million with EBITDA margins exceeding 10%.

{kind=link}

TIKR.com

Moreover, net debt is expected to fall to $140 million next year, which would be less than half of the total expected EBITDA.

When adding the company's $1.9 billion market cap, we're dealing with a 5.7x 2024E EBITDA valuation. Moreover, in 2024, the company is expected to do $170 million in free cash flow, indicating a free cash flow yield of more than 9%.

This valuation is attractive and provides the company with an upside to the $45 to $50 per share range. The current consensus price target is $45.

FINVIZ

It's worth noting that if the company benefits from pricing improvements this year, its results are likely to be even stronger. Therefore, it's advisable to monitor corn crop quality closely. In the event of a good harvest following a disappointing 2022, input prices could potentially decrease. Furthermore, if energy prices remain high, the company could leverage this to its advantage.

Takeaway

In this article, we discussed a corn belt ethanol giant. Nebraska-based Green Plains struggled last year, mainly driven by poor margins and operating headwinds. However, these issues are fading. On top of that, the company's investments are starting to bear fruit. Value-adding production technologies are improving margins, volume growth is strong, and political tailwinds are paving the road for high ethanol demand growth in the years ahead.

Moreover, the company has a healthy balance sheet and an attractive valuation.

While macroeconomic headwinds are pressuring energy prices, I believe that GPRE shares are undervalued with room to grow to at least $45 in the next 12 to 24 months.

For further details see:

Green Plains' Future Looks Bright