GPRE - Green Plains Partners: Can Its Nearly 14% Dividend Yield Be Sustainable?

2023-12-15 18:23:40 ET

Summary

- Green Plains Partners LP warrants a buy rating for its high dividend yield and sustainability.

- The ethanol market is expected to see significant growth, benefiting GPP's revenue from storage and transportation.

- Despite potential risks, GPP has stable fundamentals and low volatility, making it a solid choice for dividend investors.

Investment Thesis

Green Plains Partners LP (NASDAQ: GPP ) warrants a buy rating for its high dividend yield and sustainability. Despite a high payout ratio, the company’s dividend payments appear to be safe due to forecasted industry growth, GPP’s consistent unlevered cash flow, and its control over debt. Downsides to GPP are the company’s share price performance as well as unremarkable growth. Despite these drawbacks, GPP is worth buying for dividend income seekers.

Company Overview and Competitors

Green Plains Partners was founded in 2005 and is a company that develops, stores, and transports biofuels such as ethanol. Ethanol is an additive to gasoline and has numerous other applications including medical uses and alcoholic beverages. The company owns or leases 27 storage tanks in addition to 19 trucks and tankers for transportation. GPP’s parent company is Green Plains Inc. ( GPRE ) which owns an almost 49% stake in the company and has multiple commercial agreements that greatly benefit GPP. For comparison purposes, peer competitors examined are StealthGas Inc. ( GASS ), Martin Midstream Partners L.P. ( MMLP ), Plains All American Pipeline, L.P. ( PAA ), and Global Partners LP ( GLP ).

{kind=link}

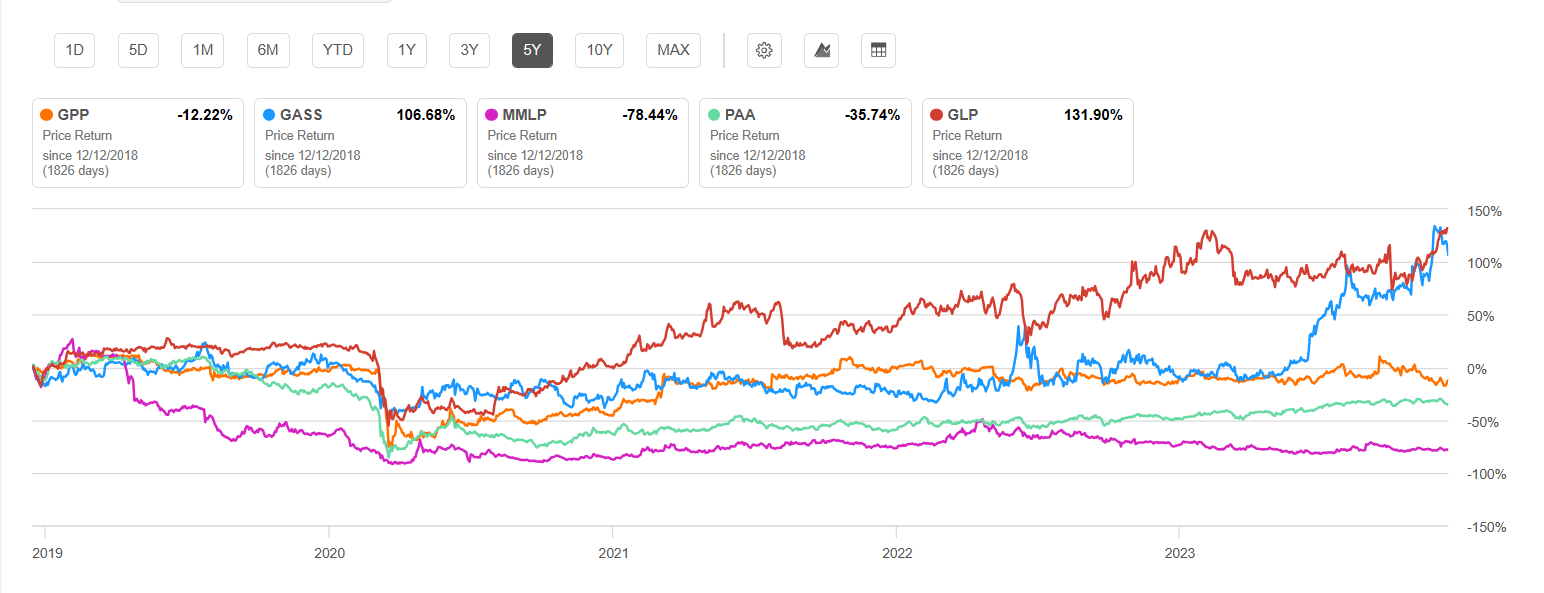

GPP and Peer Competitor 5-Year Price Return (Seeking Alpha)

Historically, GPP’s share price has seen a slight CAGR decline. Even going back to 2015, GPP traded at just under $15 per share. At the time of this article GPP is at $13.65 per share. However, as I will cover later, GPP offers a considerable dividend yield. Therefore, while not a stock for growth investors, it is very appealing for income seekers that are willing to accept essentially a flat share price in exchange for high dividend yield.

Outlook for Industry

The ethanol market is expected to see a 4.6% CAGR between 2023 and 2033. The U.S. is the world’s largest ethanol producer in 2021 at 53% of the world’s supply. Overall demand for ethanol will likely have a direct impact on GPP since it gains revenue from the storage and transportation of biofuels.

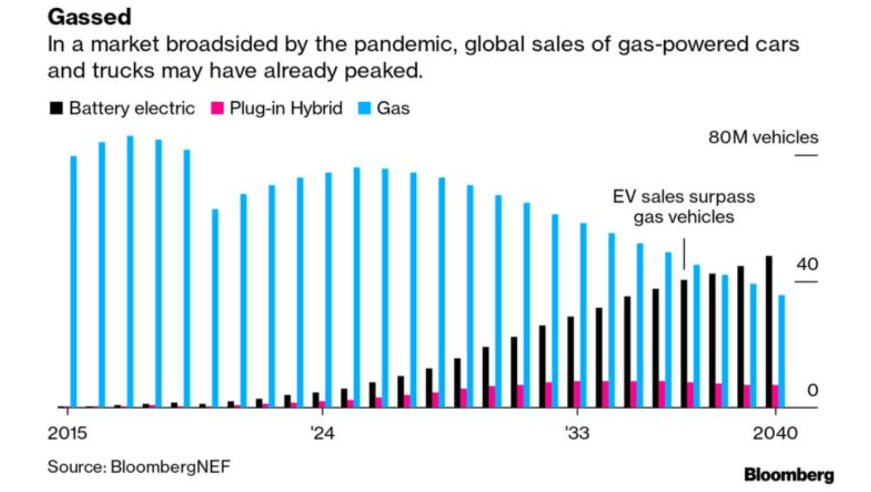

The key dampener on future demand will likely be electric vehicles taking a larger portion of the overall car and truck market. Because gasoline takes a portion of ethanol market share, this will have an impact on GPP. However, gas-powered cars and trucks are expected to see an increase until mid-2020s and then a gradual decline. This trend will continue until EV sales surpass gas vehicles in late 2030s .

{kind=link}

Gas, Electric, and Hybrid Vehicle Demand Forecast (BloombergNEF)

Despite the reduction in gas-powered vehicles, overall demand for ethanol will remain substantial. GPP is postured to support that growth with low debt, high cash flow, and its efficient partnership with its parent company. Therefore, an investor can reasonably expect a sustainable dividend given the overall ethanol market. However, to further validate this claim, we must look at GPP’s financials more closely.

Dividend Sustainability

GPP provides a high dividend yield of 13.96% with an average four-year yield of 12.23%. The company has also been providing dividend payments for 8 years and has seen two years of consecutive growth. With such a high dividend yield, the key question in my mind is regarding its sustainability. To determine dividend sustainability, the most obvious metric to me is GPP’s payout ratio. While trending downward, GPP has a dividend payout ratio of greater than 100%. This is normally a red flag to me since theoretically more than 100% of the company’s income is going to the shareholder. But we must dive deeper to determine if its sustainable.

Green Plains Partners Dividend Payout Metrics (2022 Q4 through 2023 Q3)

| Dividend Payout Metric |

| 2022 Q4 |

| 2023 Q1 |

| 2023 Q2 |

| 2023 Q3 |

| Payout Ratio |

| 166.60% |

| 108.88% |

| 115.49% |

| 114.79% |

| Dividend per share |

| $0.46 |

| $0.46 |

| $0.46 |

| $0.46 |

| Common Dividends Paid |

| $15.7M |

| $10.6M |

| $10.6M |

| $10.6M |

Source: Seeking Alpha, 14 Dec 23

Despite a high payout ratio, GPP has been able to maintain a consistent asset to liability ratio. Furthermore, its cash position is higher than the previous two quarters. Finally, the company has net debt that is controllable. These metrics match with what GPP reports in its annual report that it can achieve sustainable cash flows through the agreements it has established. In these agreements, there are minimum commitments in its rail, storage, and transportation services that provide consistent cash flow.

GPP Assets and Liabilities Metrics (2022 Q4 through 2023 Q3)

| 2022 Q4 |

| 2023 Q1 |

| 2023 Q2 |

| 2023 Q3 |

| Total Assets |

| $121.4M |

| $137.8M |

| $127.5M |

| $120.3M |

| Total Liabilities |

| $120.7M |

| $137.8M |

| $129.0M |

| $121.4M |

| Net Debt |

| $86.7M |

| $101.7M |

| $98.4M |

| $87.0M |

| Cash and Equivalents |

| $20.2M |

| $18.1M |

| $15.6M |

| $19.1M |

Source: Seeking Alpha, 14 Dec 23

Therefore, while GPP has a high payout ratio, I conclude that it has multiple indications for being sustainable. To explore another aspect of its dividend sustainability we must look at the company’s growth and profitability. As one might expect, a company with such a high dividend yield has little to reinvest into its own growth.

Growth and Profitability

Any company could be providing a high dividend yield only to be dropping precipitously in share price due to increasing debt and declining cash reserves. However, this has not been the case with GPP. The company has demonstrated consistent revenue and net income as well as a high net income margin of 45.54%.

Growth and Profitability Metrics for GPP

| 2022 Q4 |

| 2023 Q1 |

| 2023 Q2 |

| 2023 Q3 |

| Revenues |

| $20.9M |

| $20.8M |

| $20.5M |

| $20.1M |

| Net income |

| $9.4M |

| $9.7M |

| $9.2M |

| $9.2M |

| YoY Revenue Growth |

| 9.70% |

| 8.77% |

| 4.42% |

| 0.39% |

Source: Seeking Alpha, 14 Dec 23

While GPP has maintained consistent revenue and net income, my only area for concern is its YoY revenue growth over the last four quarters. However, this is not out of the ordinary for high-dividend companies. Because GPP is not utilizing its profits for expanding storage facilities and vehicles, muted revenue growth is fairly expected.

Company Outlook and Valuation

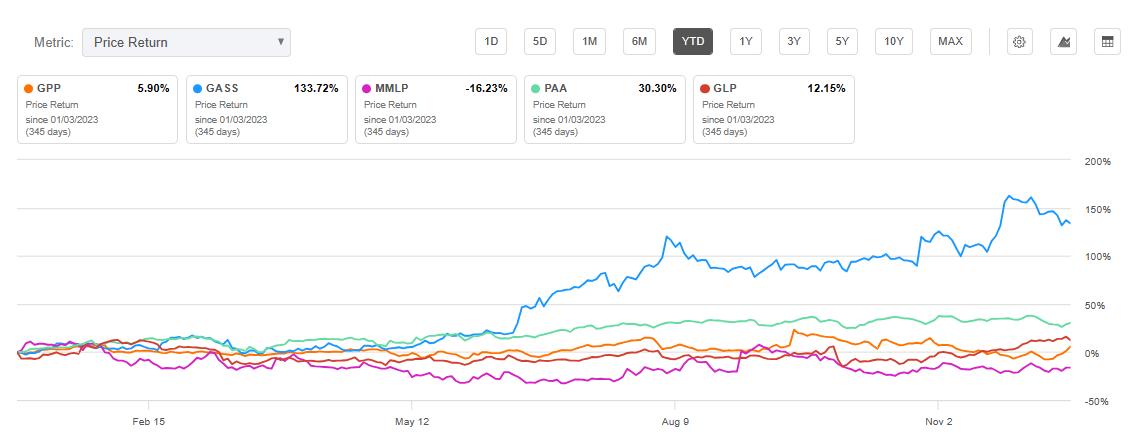

With a current share price of $13.65 at the time of this article, GPP is currently in roughly the middle of its 52-week range ($11.72 to $16.25). Green Plains has demonstrated a YTD price return of almost 6% but has historically been essentially flat. This is not surprising considering so much of the company’s profit are returned to shareholders in the form of dividends versus investment for future growth.

{kind=link}

YTD Price Return: GPP and Peer Competitors (Seeking Alpha)

Compared to the peer competitors analyzed, GPP is priced a bit on the higher side as seen in its price/sales and price/cash flow. However, given its high dividend yield and stability, one can reasonably expect GPP’s share price to not see any major gains or losses. That is, unless a major risk factor unfolds like recession or other impact to the ethanol industry.

Valuation Metrics for GPP and Peer Competitors

| GPP |

| GASS |

| MMLP |

| PAA |

| GLP |

| EV/EBITDA FWD |

| 7.44 |

| 3.45 |

| 6.06 |

| 9.07 |

| 8.28 |

| Price/Sales TTM |

| 3.51 |

| 1.57 |

| 0.11 |

| 0.21 |

| 0.08 |

| Price/Cash Flow TTM |

| 6.28 |

| 2.95 |

| 0.70 |

| 5.07 |

| 5.24 |

| P/E GAAP TTM |

| 7.72 |

| 4.79 |

| N/A |

| 11.05 |

| 9.76 |

Source: Seeking Alpha, 14 Dec 23

Perhaps more important than its share price growth is its expected dividend. While I do not expect GPP to increase its dividend, I believe it is safe through 2024 due to the multiple fundamental factors already covered in this article. Therefore, GPP is a solid choice, particularly for dividend investors.

Volatility and Risks to Investors

There are multiple risks to GPP’s share price and dividend sustainability. The first is economic recession. Because ethanol is used in gasoline, any recession-induced decline in gasoline demand will impact the ethanol industry. In April 2020, during the COVID-19 pandemic, demand for gasoline fell 37% below its April 2019 level leading to a 53% decline in the price index for gasoline.

The second primary risk is electric vehicle production replacing gas vehicles. This is more a certainty than a risk as already covered. However, the shift from gasoline-powered vehicles is not a rapid change, but gradual shift spanning decades. Additionally, as discussed, gasoline only represents a portion of overall ethanol demand.

The third primary risk lies with the crops that produce ethanol. Fuel ethanol is predominantly produced by the sugar of grains like corn, sorghum, and barley. While the corn industry, for example, is robust, impacts to the crop will likely have a direct impact on ethanol supply.

Even if one of these risk factors becomes reality, GPP has stable fundamentals that indicate low volatility. GPP also has a relatively low 60-month beta value of 0.71, indicating low volatility compared to the market overall. This beta value is lower than all four peer competitors analyzed. Therefore, while GPP may decrease its dividend in the event of declining revenue, I find it highly unlikely that the company would eliminate the dividend entirely.

Concluding Summary

GPP warrants a buy rating for me due to its high dividend yield that appears to be safe given the companies steady income, controlled debt, and consistent cash flow. The company’s stock is not suitable for growth investors due to its slow decline in share price historically. However, given the dividend growth CAGR and relative safety, GPP should be considered by income-seeking investors.

Given GPP’s commercial agreements with its parent company, Global Plains Inc., the company appears well suited to take advantage of the 4.6% expected CAGR for the ethanol industry. While gasoline-powered vehicles will eventually decline in comparison to electric vehicles, numerous applications for ethanol will continue to exist.

For further details see:

Green Plains Partners: Can Its Nearly 14% Dividend Yield Be Sustainable?