PAR - Greenhaven Road Capital - PAR Technology: Growing Faster Than Evidenced By Sell-Side Reporting

Summary

- While we own PAR Technology for their enterprise software business, the company has three revenue streams.

- When PAR’s 3 business lines are consolidated, the numbers do not look very appealing.

- When you combine the constraints of a standardized sell-side firm’s model and the fact that PAR reports its numbers in a way that camouflages the underlying economics of its enterprise software business, a divergence of views can emerge.

- My approach to looking at PAR is different - I don’t have the constraints of a standardized firm model, which is effectively trying to fit a square peg into a round hole.

- My expectation is that the company will change the reporting and thus force/help the analysts to notice.

The following segment was excerpted from this fund letter .

PAR Technology ( PAR )

PAR Technology is one of our largest holdings. We can consider the analysis by a 163-year-old bulge bracket sell-side research firm as a proxy for how the company is analyzed broadly. After ignoring PAR for several years, the firm in question was effectively obligated to initiate coverage after underwriting a convertible bond offering. With a $27 price target and a neutral rating, this bank is decidedly not excited by PAR.

While we own PAR for their enterprise software business, the company has three revenue streams: a government contracting business, a hardware business, and a software business. I am not sure which analyst coverage universe is most appropriate, but PAR was assigned to the Payments and Digital Assets analyst who covers approximately 25 companies, including Mastercard ( MA ), Visa ( V ), and Charles Schwab ( SCHW ). (Note: Payments represented 0% of PAR’s revenue when he initiated coverage).

From what I can tell, sell-side analysts have two goals. The first is to predict revenue and earnings, typically in the same format in which the company announces its results. The second is to present the information in their own firm’s framework. As research has been standardized, many firms use a set of ratios for all companies (P/E, etc.) as well as a standardized balance sheet, income statement, and cash flow statement. This approach yields a consistent, standardized research process and product, but it can also create blind spots, especially as each analyst is being asked to cover an increasing number of industries and companies in the face of dwindling research budgets.

On PAR’s last conference call, the CEO laid out a credible path to dramatically improving the software business’ profitability by holding its expenses flat while growing revenues. While I was ebullient, the sell-side was “meh.”

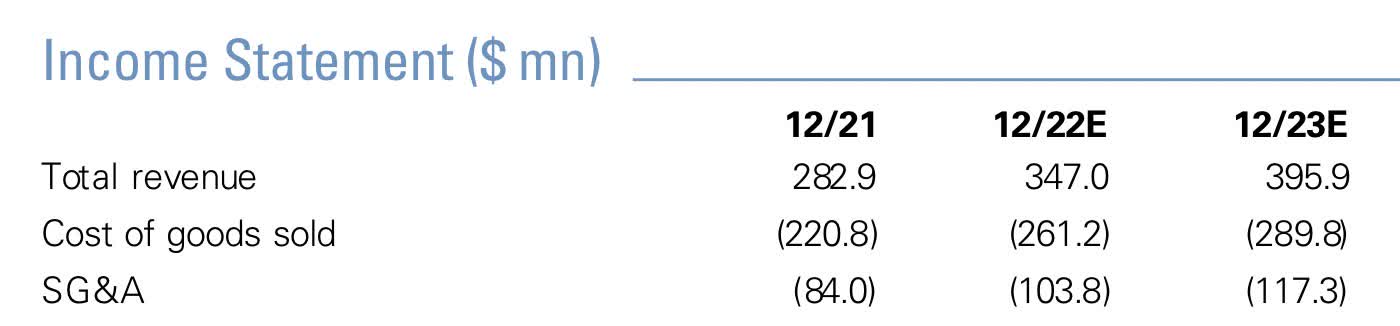

The aforementioned analyst’s projections and models are for PAR as a whole, looking at the company’s revenue in aggregate and reporting it as such in the firm’s standardized template. As you can see in the table below, when PAR’s 3 business lines are consolidated, the numbers do not look very appealing.

{kind=link}

PAR’s combined 2023 growth numbers are fine, growing the top line at 14%, but the overall company is still losing money. Without a more granular analysis, it hardly seems a place to put a significant portion of my life savings or yours. When you combine the constraints of a standardized sell-side firm’s model and the fact that PAR reports its numbers in a way that camouflages the underlying economics of its enterprise software business, a divergence of views can emerge.

My approach to looking at PAR is different. I don’t have the constraints of a standardized firm model, which is effectively trying to fit a square peg into a round hole. I also spend almost no time on the government business because I believe it is not a core part of their business and something they could (should) sell this year. As a crude overall calculation, I suggest that the government business + cash on hand + hardware = debt. Under this framework, all that matters is the enterprise software business, which I define as software revenue + support + payments. While sell-side analysts spend their time trying to estimate a quarterly earnings number down to the penny, I spend my time trying to understand the growth trajectory, duration of that growth rate, and magnitude of the operating leverage.

Now, so far, PAR does not do itself any favors in its reporting methodology. They do not report a single enterprise software number that includes support and payments revenue, thus modeling the enterprise software business has been very difficult. And when you have 25+ companies to cover as an analyst, you are seemingly not equipped to back into the number on your own.

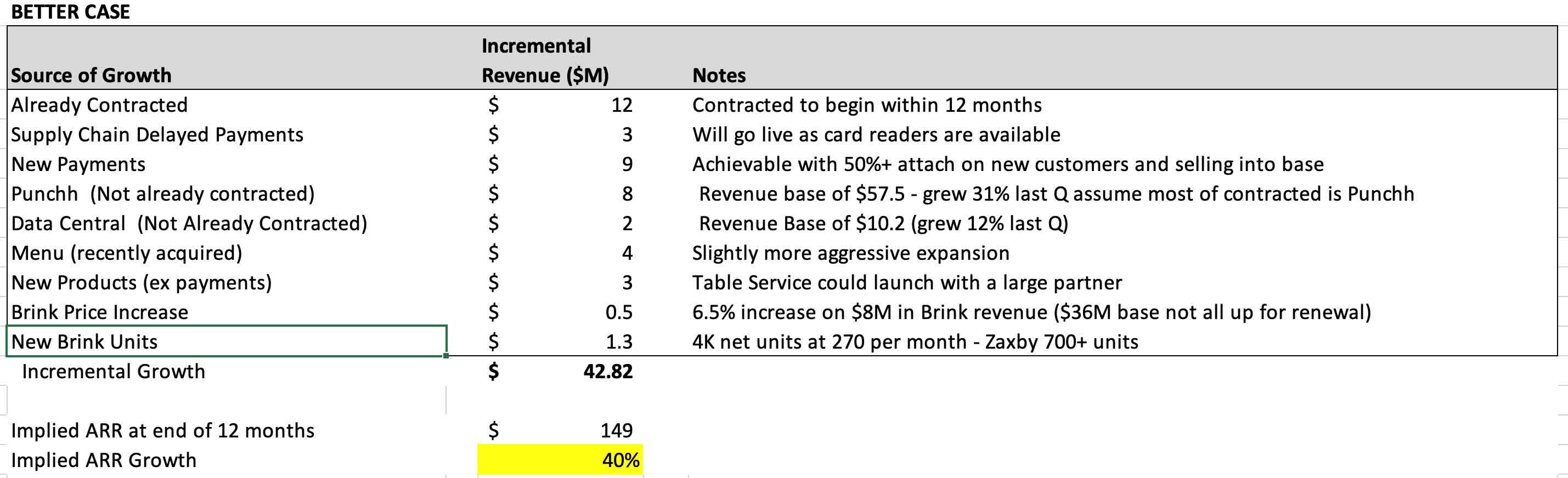

Fortunately, PAR does report Annualized Recurring Revenue ((ARR)) for the enterprise software business and, in my opinion, the growth of the ARR and the profitability of the software business are by far the biggest drivers of the company’s future returns. I am most interested in how much ARR can grow in the next 12 months. My “better case” model for incremental ARR over the next 12 months (below) has it growing from $107M to $149M.

{kind=link}

The above implies software ARR growing at 40%. Could it be 30% in a recession? Sure. It might even be 20%, but I have high conviction that the software business is growing substantially faster than is evident in any of the sell-side reporting.

Even more impactful, PAR has said they expect to hold expenses for the software business flat in 2023. The impact of growing revenue by 40% and holding enterprise software expenses flat gets lost in a model that has software, hardware, and government expenses all lumped together. However, if you are focused on just the enterprise software portion of the overall business, the operating leverage (one of our five characteristics) is enormous, adding over 20% points of margin for the year. The enterprise software goes from losing money to making money, and, when analyzed separately, the software business ends the year as a Rule of 40 company. This typically comes with multiple expansion from the recent year-end 4.5X Annual Recurring Revenue ((ARR)). But, given what I believe to be the likelihood for sustained growth for the enterprise software business, we don’t need multiple expansion to compound our investment at high rates of return.

We got our head kicked in owning PAR last year, and you may be asking if any of this software stuff will ever matter. Will the market notice the changing economics or operating leverage? My expectation is that the company will change the reporting and thus force/help the analysts to notice.

Time is our friend here. The business is getting bigger, healthier, and more profitable, and, over the course of this year, PAR’s management will want a brighter and brighter light shining on the software business. So far, the breadcrumbs have been enough that the path can be seen, but only by somebody like me who parses the company like a religious scholar. In a year, it should fit into everybody’s standardized model templates, assuming private equity does not buy the company first. If you apply the multiples recently paid by private equity for the slower growing Coupa Software ( COUP ), you get a price more than twice as high for a company growing less than half as fast .

Disclaimer:This document, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy which may only be made at the time a qualified offeree receives a confidential private placement memorandum (“PPM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications, and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the PPM, the PPM shall control. These securities shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution. While all the information prepared in this document is believed to be accurate, MVM Funds LLC (“MVM”), Greenhaven Road Capital Partners Fund GP LLC (“Partners GP”), and Greenhaven Road Special Opportunities GP LLC (“Opportunities GP”) (each a “relevant GP” and together, the “GPs”) make no express warranty as to the completeness or accuracy, nor can it accept responsibility for errors, appearing in the document. An investment in the Fund/Partnership is speculative and involves a high degree of risk. Opportunities for withdrawal/redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests, and none is expected to develop. The portfolio is under the sole investment authority of the general partner/investment manager. A portion of the underlying trades executed may take place on non-U.S. exchanges. Leverage may be employed in the portfolio, which can make investment performance volatile. An investor should not make an investment unless they are prepared to lose all or a substantial portion of their investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. There is no guarantee that the investment objective will be achieved. Moreover, the past performance of the investment team should not be construed as an indicator of future performance. Any projections, market outlooks or estimates in this document are forward-looking statements and are based upon certain assumptions. Other events which were not taken into account may occur and may significantly affect the returns or performance of the Fund/Partnership. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. The enclosed material is confidential and not to be reproduced or redistributed in whole or in part without the prior written consent of the relevant GP. The information in this material is only current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Any statements of opinion constitute only current opinions of the GPs, which are subject to change and which the GPs do not undertake to update. Due to, among other things, the volatile nature of the markets, and an investment in the Fund/Partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal, and tax professionals before making any investment. The Fund/Partnership are not registered under the Investment Company Act of 1940, as amended, in reliance on exemption(s) thereunder. Interests in each Fund/Partnership have not been registered under the U.S. Securities Act of 1933, as amended, or the securities laws of any state, and are being offered and sold in reliance on exemptions from the registration requirements of said Act and laws. The references to our largest positions and any positions listed in the Appendix are not based on performance. All of our positions will be available upon a reasonable request. All hyperlinks contained herein are not endorsements and we are not responsible for such links or the content therein. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Greenhaven Road Capital - PAR Technology: Growing Faster Than Evidenced By Sell-Side Reporting