GP - GreenPower Motor: Sales Surge Capacity Grows I Am Buying

Summary

- GreenPower Motor reported a 400% sales jump for the quarter ending Dec 2023 and said more growth is to come.

- A new manufacturing site is due to come online in 2023 dedicated to School Bus production.

- A streamlined product line from a low cost producer with positive gross profit and significant orders is going to drive share price gains in the short to medium term.

- GP has a focus on two products one assembly site for each and OEM only.

In March, I wrote my first article on GreenPower Motor Company (GP). I said they were making good sales progress and had a positive gross profit but had a cash problem they needed to solve. I have often said that everything else can be fixed if a company has sales. A 400% (YoY) sales jump for the quarter ending December 2022, combined with guidance for even higher sales for the first quarter of 2023, will solve this particular cash problem.

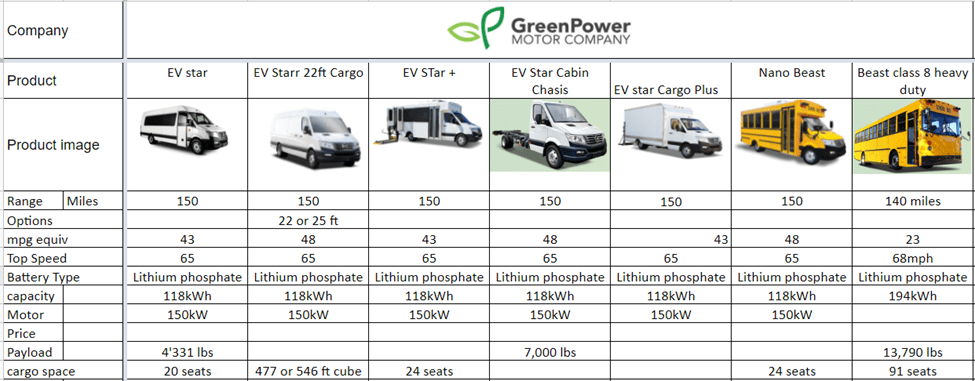

GP is an OEM manufacturer of battery electric vehicles

In truth, they now have two products, School buses which come in two variants a class A called the Nano and a class D called the Beast. The second product is the EV star, a class 4 truck platform currently available in 5 variants. In my last article, they had three other vehicles, but the large buses and autonomous vehicles have not been discussed in recent reports.

{kind=link}

I like the synergies here. The EV Stars and the Nano Beast are all based on the same electronics, and all the variants of the EV Star are on the same chassis. It is an excellent way to deliver economies of scale and gives the company a real focus. Focus is a keyword when considering GP.

Vehicle sales

{kind=link}

The EV Star Cabin Chassis is a focus for management. In July 2022, they completed the acquisition of Lion Truck Body . The rationale for this deal is clear: customers currently buy an EV Starr CC and have it shipped to a third party that builds the required truck.

In the future, the EV star CC will have its build-out performed by GP at the Lion Truck facility. GP expect increased margins and profit per unit as well as being able to offer a turnkey solution to customers; they will eliminate the possibility of poorly fitting build-outs or electrical problems. This facility will add extra features that the dealer network can use to increase sales.

GP paid $215K and assumed liabilities of $1.45 million with the potential for further cash payments to secure the company.

Sales Forecast and The Workhorse deal

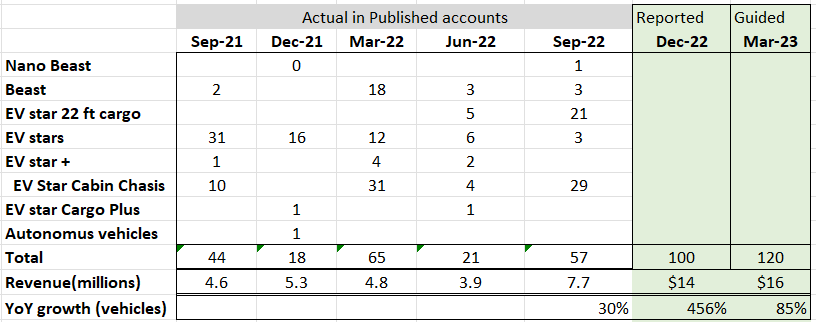

In the Q2 earnings call , CEO Fraser Atkinson said that they had finished goods inventory that will translate to $40 million of revenue, and they are currently focused on delivering these to customers (the last complete year of accounts was in March 2022, when they reported $21 million in sales).

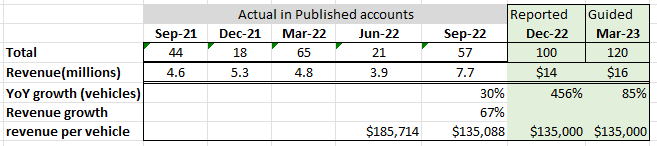

In December, GP released a press release that said they had delivered 100 vehicles in the Quarter to December and expected to deliver more than that in the next quarter. Extrapolating previous results gives the following table.

{kind=link}

The table gives a forecast of FY 2022 Turnover in the region of $41 million, very close to the figure Fraser Atkinson gave in the earnings call. All of this points to a doubling of revenue.

(Revenue from December and March was out of step as 28 vehicles that had been previously leased had their leases canceled and were sold; however, they were not new unit sales, just additional revenue.)

Sales Forecast by Product

1. The 22ft Cargo EV Star

In reply to an analyst question, Brendan Riley (President) spoke about the demand for the newly released 22 ft Cargo vehicle. He said it had only been marketed in California and New Jersey so far and that most deliveries have been made in New Jersey. He then said that they had demand for an additional 80 units that they have started building for California and added.

So I'd have to say that that 22-foot cargo is a home run of a product for us. I expect that product, to be honest for that vehicle to outstrip -- the demand outstrip our capacity in the next little while

80 Units represents a 400% increase in the 22 ft Cargo sales, definitely a home run.

2. The EV star Cab and Chassis

The Workhorse deal

GP and Workhorse signed a deal in March 2022 that gives WKHS the exclusive rights to use the EV Star cab and chassis base vehicle to build step vans; the companies agreed to a 21-month deal for the delivery of 1,500 vehicles, which represents a further 71 vehicles a month on average for 2023 and some of 2024.

This deal was highlighted in the recent MDA:

First, GreenPower began manufacturing its first few tranches of EV Star CC's for the 1,500 unit purchase and sale contract with Workhorse Group, Inc ("Workhorse"). During the quarter, GreenPower coordinated with its suppliers for the delivery of key components and initiated production of 100 vehicle tranches of EV Star CC's. By the end of the quarter the first 100 EV Star CC's were near completion, the next tranche had entered production and key components for additional tranches had been ordered. The first deliveries to Workhorse began in July, with follow-on deliveries made in August. GreenPower's team is working closely with Workhorse to assist with the integration on the EV Star CC's.

3. School Buses

Sales of School buses have been slower than I forecast in my earlier article. One of the main drivers here is government funding; the funding facilities have been finalized recently. California Resource Board has awarded $198,000 per vehicle, with public schools eligible for a further 65%. With a total of $130 million set aside, San Joaquin Valley has set a figure of $400,000 per school bus, and the Federal EPA program has a figure of $375,000. With all of these figures now available, I expect schools and areas to press on with orders. (detail from earnings call answers) More than 8,000 type A school buses are sold each year in the US.

The EPA launched its Clean Bus Program in May 2022 and will invest $5 billion over the next five years in emission-free vehicles.

This is a large industry of 480,000 school buses in operation in the US, powered mainly by internal combustion engines. Unsurprisingly with low running costs and government incentives, take-up of BEV trucks is growing. In 2020, there were 821 BEV school buses, and by 2021 this had grown to 11,000. Electric buses have an annual cost of only 50% of the comparable diesel bus.

In my opinion, the industry is ripe for disruption. Dominated by three legacy players Blue Bird Corporation ( BLBD ), IC Bus, and Thomas Built Buses. These companies are transitioning to electric. Like GP, they are OEMs and purchase components from other manufacturers ( the Meritor inc deal with Thomas Built Buses ). The Blue Bird electric uses a Cummins powertrain with a Sumo motor giving it a smaller range (120 miles v 150 miles) and fewer seats (84 v 91) than the GP competitor.

Although the EV star has been driving the growth in vehicle sales at GP I expect to see the school bus sales grow significantly over the next few years and perhaps see them reaching 1,000 unit sales per year.

Bus Manufacturing site

The newly acquired 80,000-square-foot manufacturing site in West Virginia stands on 6 acres of land and represents a partnership with the state of West Virginia. GP took possession of the site in August. The state is providing $3.5 million in employment incentives and has agreed to purchase $15 million of vehicles manufactured at the site. The lease-purchase agreement does not require any money upfront, gives the first year rent-free, and all lease payments will be applied to the property's purchase price. As soon as the lease payments reach $6.7 million title to the property will pass to GP. An excellent deal GP can focus its limited cash resources on growing the business but will gain ownership in the long term and has guaranteed sales of the buses its produces.

The facility will be GP's bus manufacturing site in North America and focus on the Nano and the Beast. The facility will be fitted out in stages but is expected to produce 50 school buses per month by the end of 2023. ( June investor presentation ).

EV Star Manufacturing site

The current production site is at Porterville, California, the original agreement was signed in 2016 for a 9.3-acre plot. There was a newspaper report in 2021 that stated the facility had not been built ; however, a tour of the facility was made available by video . The video shows that the facility is an assembly site and looks low-tech.

GP is an OEM which means it buys parts and builds the vehicle. The original offer document before the Nasdaq listing gives some information. The motor comes from Siemens, the axles are supplied by ZF, and the brakes come from Knorr. The largest component of any BEV is the battery. GP are battery agnostic from page 30 of the offer document.

Where some other electric vehicle manufacturers build their own battery packs we purchase the batteries in a plug-and-play pack for our designs. This provides us with the flexibility to use different cell manufacturers with different battery chemistries. We believe that the underlying battery cells are a commodity and consequently have designed our products to take full advantage of the best batteries that are available at the time we manufacture our products.

This approach may bring supply chain problems, but it is hard to argue with the thought process and makes GP a very low-cost operation compared to its peers.

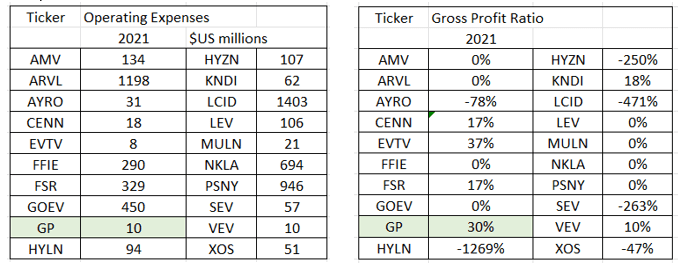

GreenPower Finances

Unlike many of its peers, GP is a low-cost operation with a positive gross margin.

{kind=link}

This has an enormous implication for scaling. If it scales, it will not be long before it covers its costs. As I have already discussed, GP is scaling at quite a pace.

Cash Problem Solved?

In the latest quarterly report, GP reported $2 million in available liquidity and $27.5 million in finished goods, plus $16.5 million of work in progress. In the subsequent notes ( Q2 report ), a share issue reportedly raised $800k.

Management is guiding to a margin of 22%, but that does depend on the product mix, so it could be lumpy. The 100 unit sales which have been reported should generate a revenue of $14 million with a gross profit of $3 million.

Inventory days have been growing alarmingly; if the previously discussed sales figures for the Dec 22 quarter are correct, then they are about to clear the inventory backlog, and inventory days will fall to a more manageable level.

Working Capital (Author Model)

So we have $2 million in cash plus $0.8 from the equity raise, $3 million from the gross profit on vehicle sales, plus a potential $11 million from working capital. We will have to see the actual figures but the cash problem may well have been solved by sales.

Conclusion

GreenPower Motor appears to be a low-cost gross profit generating business; they are focused on their products and have significant sales contracts in place. They have reported an explosion in sales that could well solve their cash issues and put them on a shortcut to profitability.

They have guided to 100 vehicles in the quarter ending Dec 2022; however, the detail of this article suggests that they could be at 100 vehicles per month by the middle of 2023. That would represent a growth of 500% from June 2022 to June 2023.

They have positive gross profit and low costs, this growth in vehicle sales will quickly drive them to bottom-line profit, and as a result, the share price will move significantly higher.

Management is developing two manufacturing sites that will eventually become owned by the company adding to its net worth without depleting cash reserves.

We will get the actual figures for sales and their implications for profit, working capital, and cash within the next couple of months. Therein lies the risk if the increased sales don't solve the problems and push the company towards profit it is hard to imagine what will.

(I will update with a comment and a link to my technical analysis later in the month).

For further details see:

GreenPower Motor: Sales Surge, Capacity Grows, I Am Buying