GEF - Greif Inc: A Company With Untapped Potential

2023-04-28 11:42:11 ET

Summary

- The low PE ratio is what attracted me to investigate the company further.

- Upon digging deeper, I noticed the company is generating very decent unlevered free cash flow and has a decent balance sheet.

- The industry’s outlook is not very exciting, which means the investor may not come to unlock the company’s potential.

- A DCF model suggests class A shares are trading at a discount while B shares are fairly valued.

- I give the company ahold rating as I’d like to see more progress.

Investment Thesis

Q1 earnings missed by quite a bit, I wanted to take a look at one of the lesser known and covered stocks Greif Inc ( GEF ) (GEF.B), as the low PE ratio compared to its competitors drew my attention. I will briefly look at the outlook of the paper and packaging industry while taking a deeper dive into the company's financials and possible revenue growth going forward. I believe that the company is flying well under the radar of investors which may mean the company is undervalued, but the risk is that the company is so under the radar that it may never reach its potential. For that reason, I give it a hold until the company's initiatives get some traction with the investors as the upside is potentially there, coupled with a decent dividend, it might end up rewarding shareholders in the future.

Industries Outlook- Sustainability

In terms of the paper packaging sector, there isn't much growth projected, however, a lot more people are becoming environmentally conscious which will drive a switch to using more paper-based packaging to replace plastic. According to Fitch Ratings , there is no expectation that an upcoming recession is going to hurt the industry, and rates it neutral. Packaging of foods will always be in demand.

With time people will try to stay away from plastic packaging as much as they can, and opt for more sustainable packaging, which I believe the company is positioned well and will see some growth.

In terms of the company's main packaging business, which includes plastic and steel containers, there is a lot of criticism and a lot of demand for more sustainable plastic and steel products that would harm the planet less. Every company in the world these days is coming up with new initiatives that include improvements to their operations. GEF is no different. The Build to Last initiative, although still in the early years, is working out as intended, with more uses of recycled plastic, steel, and other materials is going to be seen as a very positive for the company, which most likely attract many investors if the initiative is a success. We are already seeing the demand for sustainable plastic and steel outpacing the supply , which can present an opportunity for companies like Greif going forward.

I do think that the biggest catalyst the company could see is sustainability. There are so many environmentally conscious investors out there, especially with the younger Gen Z's that may look at the company like Greif and walk away because of the product they're producing. If the company can get on the good side of these investors by promoting sustainability further with initiatives like Build to Last and prove that it is working, I can see the company becoming more mainstream, although, not much, since the company may seem quite boring still.

Financials

I wanted to focus mostly on the company itself here rather than where the industries are going to go in the future as I believe the company itself has a lot of potential.

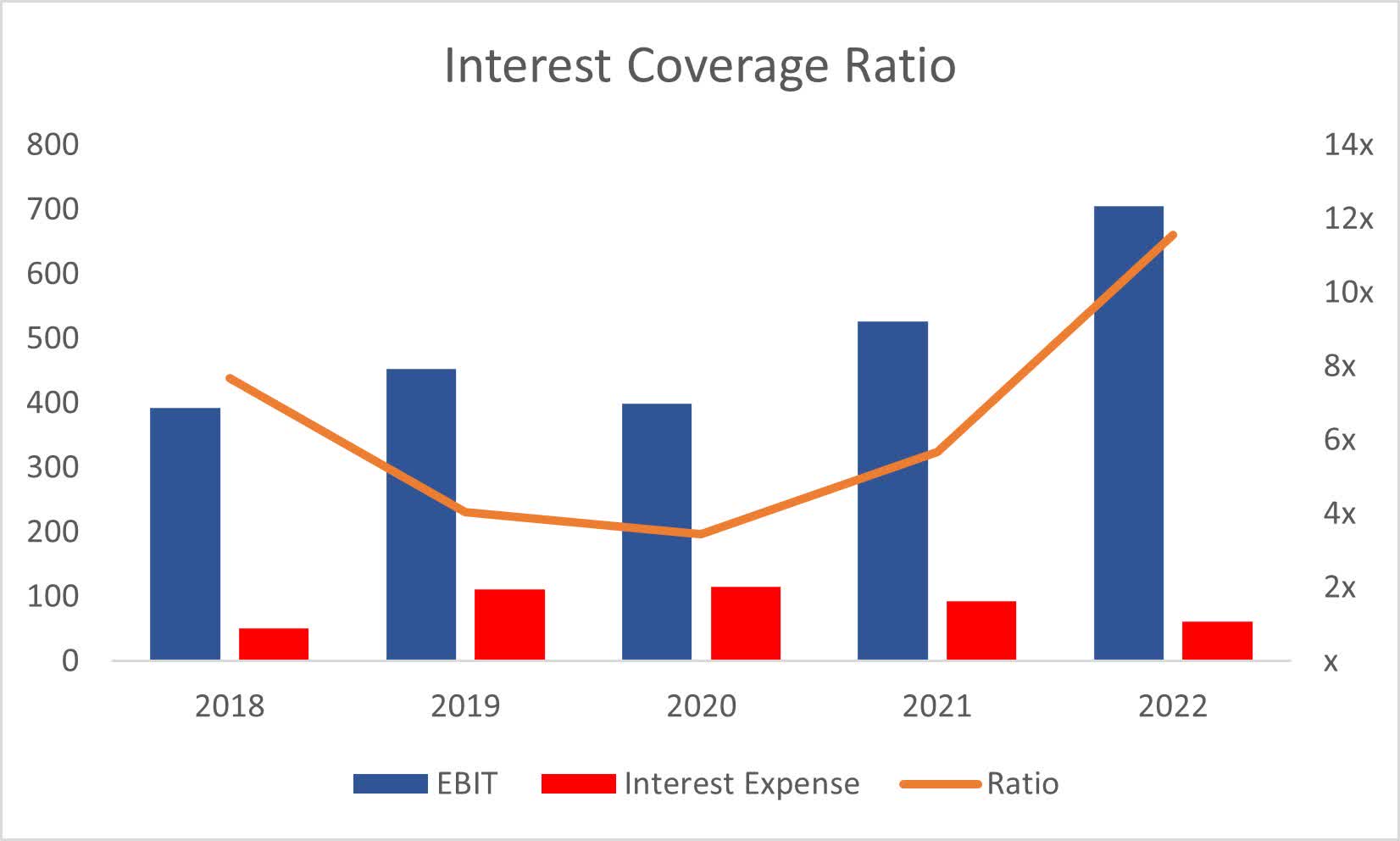

The company had $161B in cash in Q1 '23 and $2.1B in long-term debt. This may deter a lot of investors who are not particularly fond of debt, especially if that debt is more than half of the company's market cap. I don't think debt is an issue here, and as long as the downturns in the economy are going to be mild for the industries that the company is in, I don't see how the company would not be able to pay off debt. The company generated over $600m in operating cash flow and around the same amount in EBIT, which more than covers annual interest expense of $60-$70m. The interest coverage ratio is outstanding as you can see below from the graph, with a nice little smile.

Interest Coverage Ratio (Own Calculations)

{kind=link}

The company is very open to organic and inorganic growth in terms of reinvesting back into the company and M&As and I can see the company keep employing debt for these reasons.

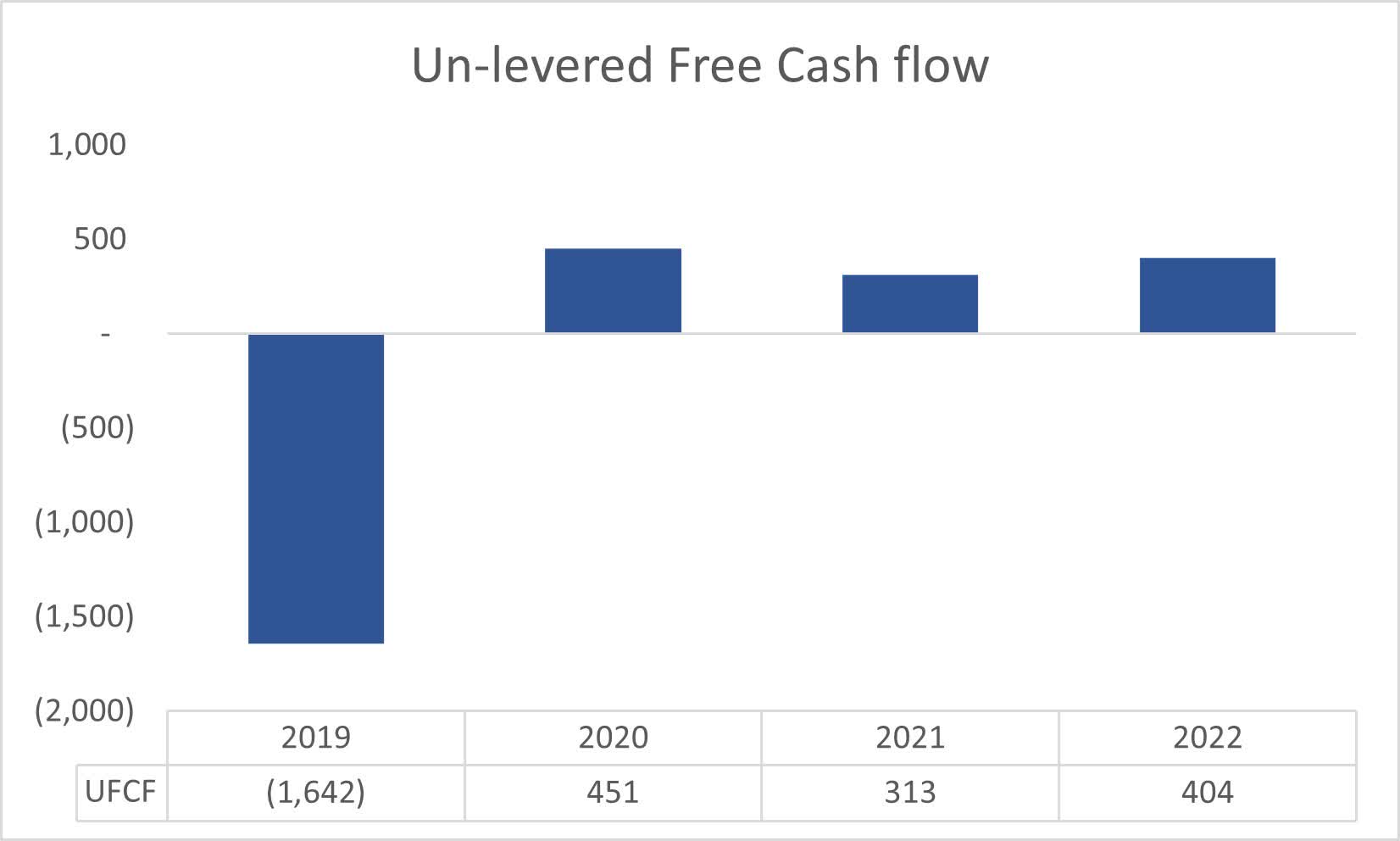

In terms of cash flow, the company managed to turn around quite well since 2019 when unlevered free cash flow was well in the negatives, and now for the last 3 years, it seems to be quite steady from $300m-$450m, which if the company manages to achieve in the later years, is a very good sign.

{kind=link}

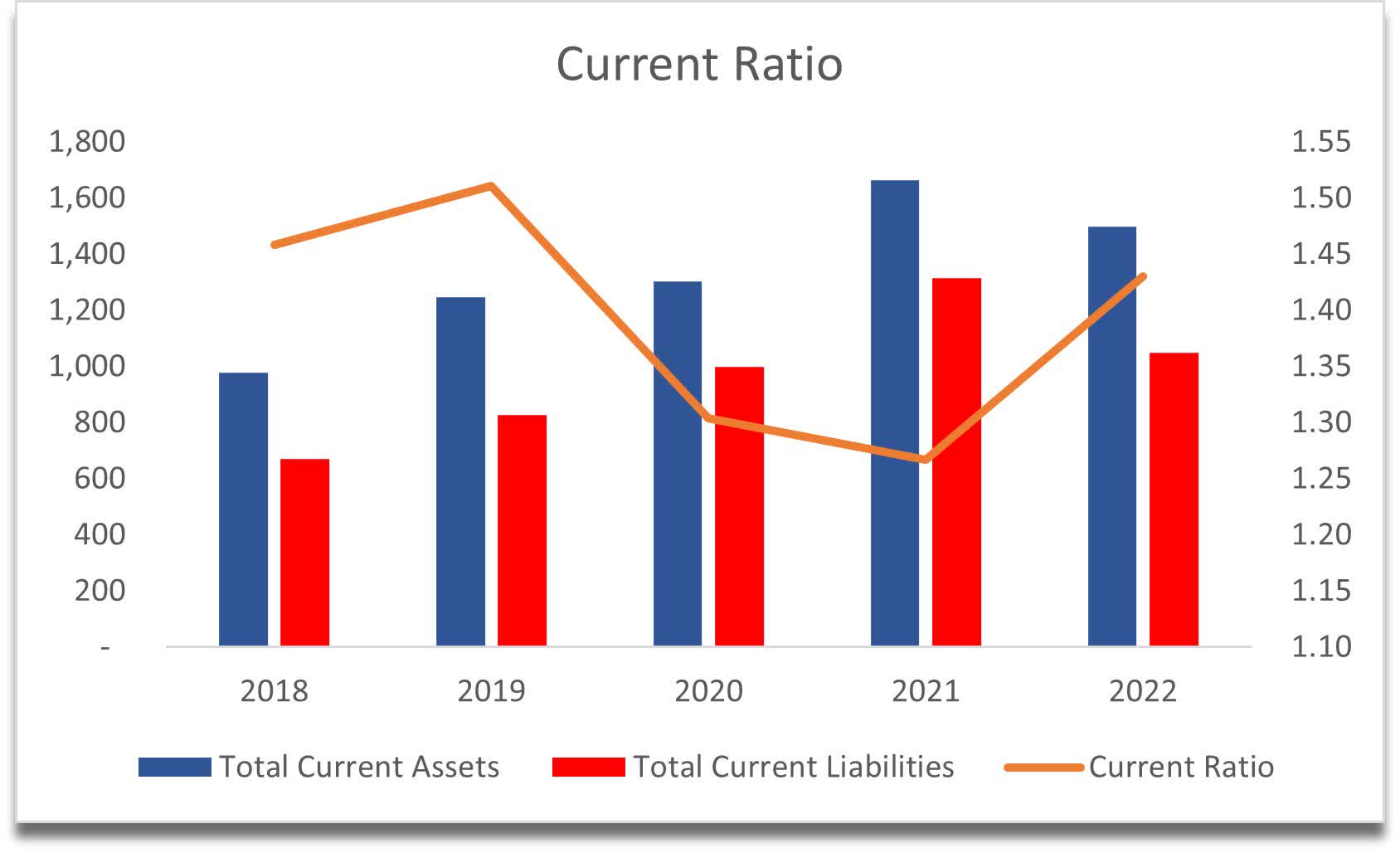

Further on the company's liquidity, the current ratio has gotten better in the last year, and it has been quite healthy over at least the last 5 years, currently at 1.43, which means the company can pay off its short-term obligation 1.4 times over. It has no liquidity problems by the looks of it.

Current Ratio (Own Calculations)

{kind=link}

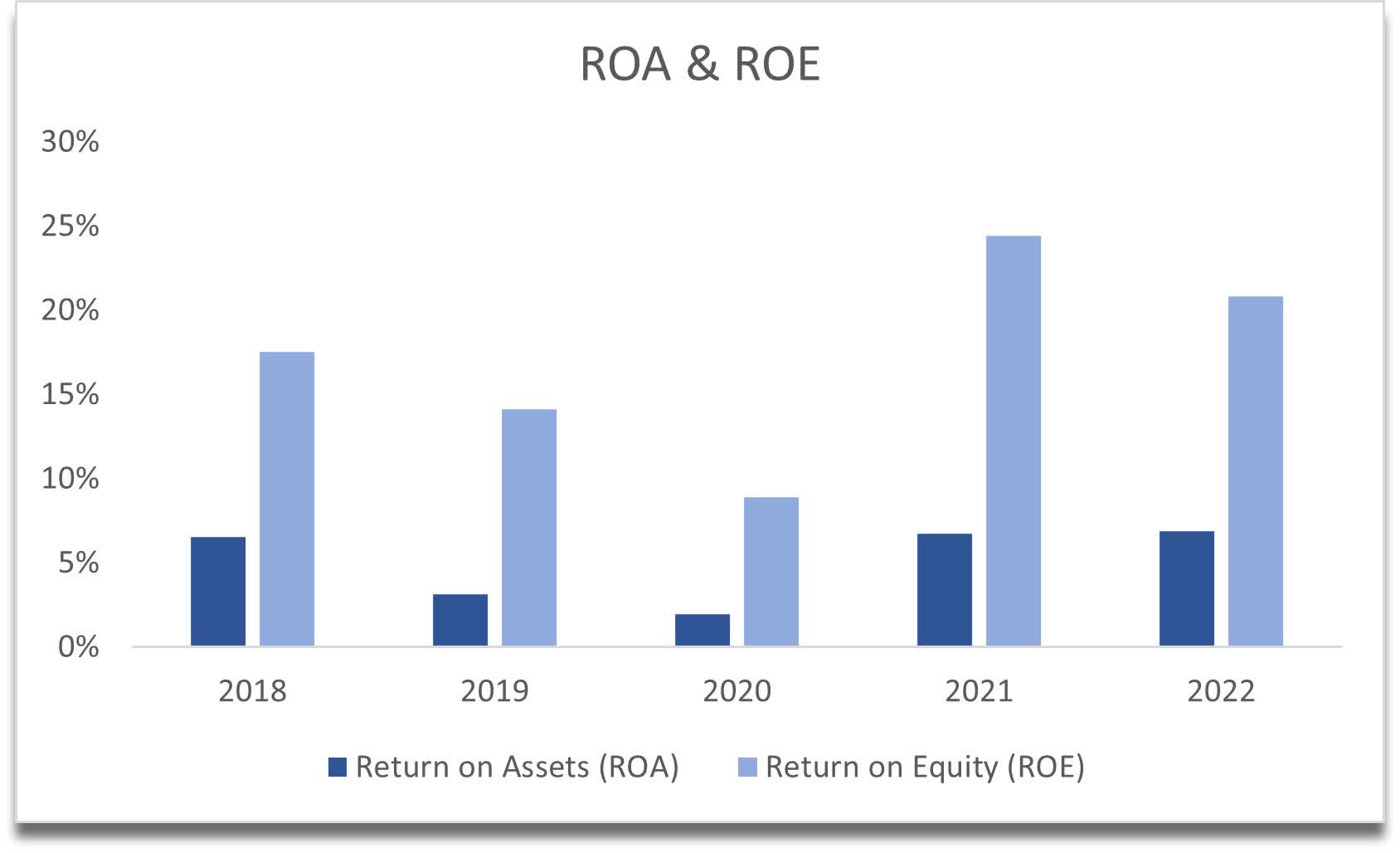

In terms of efficiency and profitability, the company's ROA and ROE are quite decent, also matching the industry's average, which suggests the management is doing a good job at generating returns from shareholders' investments. The management is efficient at investment financing to grow the business. However, ROE may be slightly inflated due to the company's use of debt.

ROA and ROE (Own Calculations)

{kind=link}

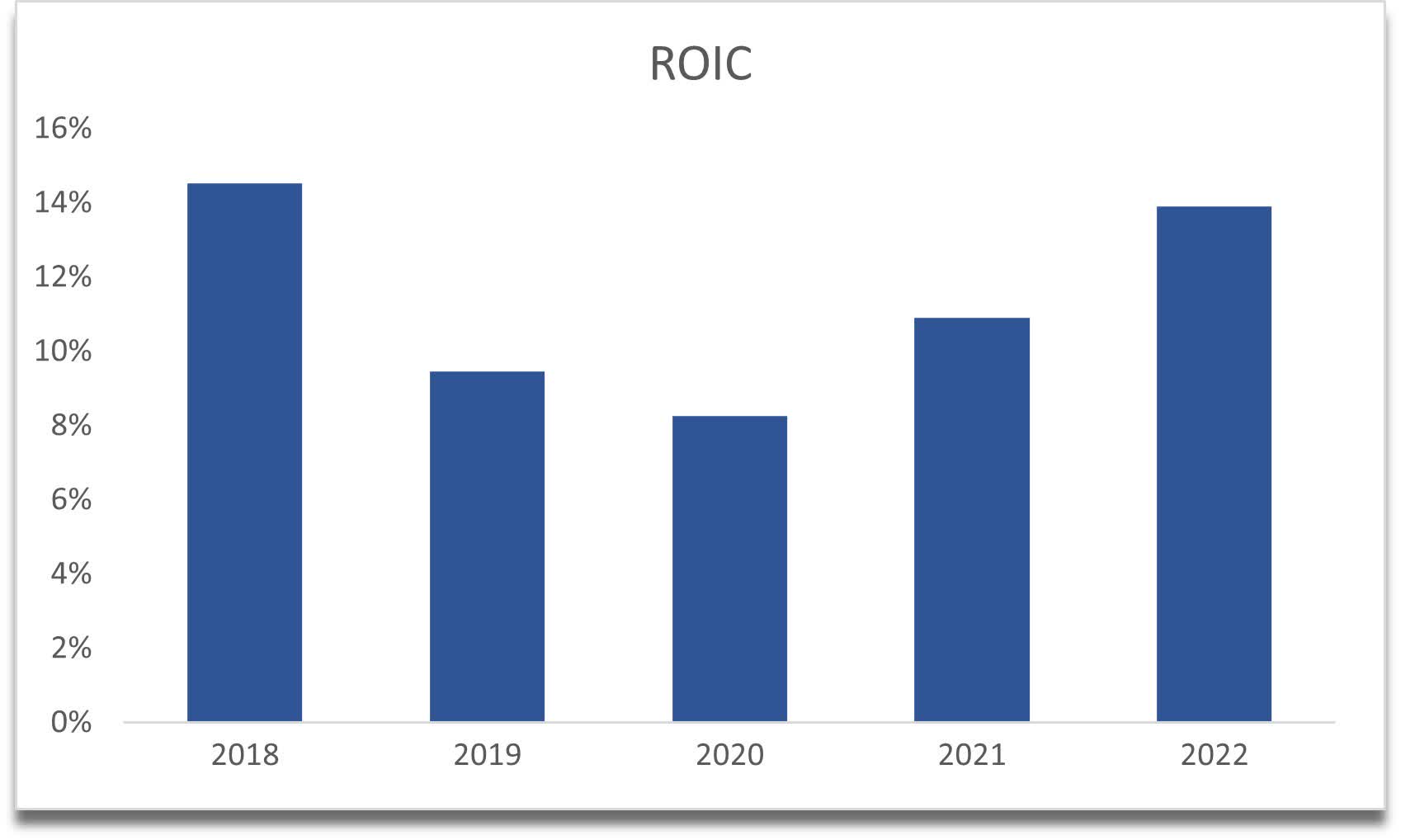

The company's ROIC is also quite decent, at around 14%, which suggests the company has some competitive advantage and a decent moat. The management can invest in projects that bring in positive NPV. It's worth noting that it is also on an uptrend which is a good sign if it continues to go up.

{kind=link}

Overall, I would say the company's financial health is quite good. If the company continues to generate good free cash flow and steadily grow, it won't have any issues paying off that massive debt balance, so for now I do not see any red flags.

Valuation

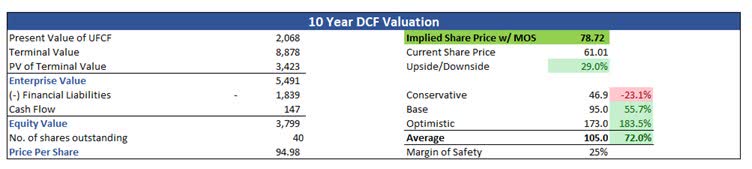

I decided to anchor my short-term valuations to the lower guidance that the management presented for FY23. The company expects the lower range to be around 730m for the year on EBITDA. I achieved this by contracting margins in the short run and over time I have linearly improved them to the levels the company saw at the end of FY22. This to me seems like a conservative play because I do believe, over time the company is going to achieve better margins with more technology utilization and other digitization efforts.

For the base case, I went with -a 5% decrease in revenues for '23 to reflect softer demand for the products, and then a 10% rebound the next year which will linearly decrease growth to 5% by '32, giving me a 6.3% average annual revenue increase.

For the optimistic case, the average annual return is 8.3%, while for the conservative case its 4.3%. to give me a range of possibilities a company can be worth.

I also added a 25% margin of safety to the intrinsic value calculation to be even more on the safer side. With that said the company's intrinsic value is $78.72 a share, implying a 29% upside from current valuations to GEF or right on the mark with GEF.B, which pays 1.5 times more in dividends but is lacking trading volume.

Conservative DCF Valuation (Own Calculations)

{kind=link}

Closing Comments

Mathematically, it seems like the company is trading at a discount, with good free cash flow projections into the future. PE ratio indicates the company is trading very cheaply; however, it may also indicate that the lack of growth in the industry keeps investors at bay. This may mean that the company will not reach the potential it seems to have, as the management seems to be running a very good company that is able to deliver great returns and free cash flow. In my opinion, the growth in the industry doesn't matter as much as expansion in margins, which in turn delivers more value to its shareholders in terms of increasing dividends, share buybacks, and other growth initiatives.

In my opinion, the stock is a hold right now due to economic headwinds that may present some volatility in the share price in the short run. I would like to see a couple more financial reports to see how the company is going to weather the softness of demand and how the management is going to be able to control costs so that margin contraction is mitigated.

For further details see:

Greif Inc: A Company With Untapped Potential