GHI - Greystone Housing: Solid Q2 Results Reaffirm Strong Dividend Yield

2023-08-14 04:57:01 ET

Summary

- Greystone Housing reported revenue of $28.30 million, up 64.24% compared to $17.23 million in Q2FY22.

- GHI can maintain its quarterly dividend of $0.37 in the next two quarters as well which can make the annual dividend $1.48, representing a forward dividend yield.

- After comparing the forward P/E ratio of 5.74x with the sector median of 9.24x, we can say that the company is undervalued.

Investment Thesis

Greystone Housing Impact Investors LP ( GHI ) primarily specializes in mortgage revenue bonds that are financed for student housing, multifamily, and commercial properties. It has recently delivered solid quarterly results and I believe it can sustain this performance in the future as a result of disruptions in commercial bank lending which can help it in generating additional cash flows and increase its dividend payout.

About GHI

GHI mainly deals in mortgage revenue bonds that are financed for student housing, affordable multifamily, and other commercial properties. The partnership primarily invests in Mortgage Revenue Bonds ((MRB)) and Government issuer loans ((GIL)). It conducts its business in four reportable segments : Affordable Multifamily MRB Investments, Seniors & Skilled Nursing MRB Investments, Market-Rate Joint Venture Investments, and MF Properties. The Affordable Multifamily MRB Investments segment mainly deals with offering construction and permanent financing for commercial and residential properties. The partnership owns 74 MRBs and 9 GILs with aggregate outstanding principals of $766.3 million and $184.8 million respectively. This segment contributes 78.16% to the partnership's total revenues. The Seniors & Skilled Nursing MRB Investments segment offers construction, acquisition, and permanent financing mainly for skilled nursing & senior housing properties. It has one MRB and generates 0.87% of the total partnership's revenue. The Market-Rate Joint Venture Investments segment comprises joint venture equity investments. These investments are mainly focused on market-rate multifamily properties. The segment activities are managed by its joint venture partner and it represents 11.26% of the total revenue. The MF Properties segment includes student housing residential property which is held by partnership and contains 384 rental units for one MF property. This segment accounts for 9.68% of the partnership's total revenue.

Financials

The adverse macroeconomic conditions in the U.S. have negatively impacted the bank lending situations and it has also hampered the growth of commercial banking due to elevated interest rates. The credit policies were also tightened after the second quarter in the previous year which reduced the operations in the industry. It experienced significant liquidity issues which led to a decline in lending activities. All this uncertainty and weaker performance of commercial banking sectors created ample opportunities for GHI to cater to the credit needs in the market. The demand for mortgage revenue bonds has grown rapidly after the disruptions in the banking sector. I believe these macroeconomic changes can further accelerate the partnership's growth and increase its profit margins as it continuously focused on tapping opportunities where traditional finance is not available. It is concentrated on acquiring strong sponsors within its existing clients which can contribute to its revenue growth. In addition, GHI's healthy cash flows make it well-positioned and competitive in the market to capture the additional market share. All these positive industry trends have benefited the partnership in the current fiscal year which is also reflected in its quarterly results.

GHI has recently delivered its strong quarterly financial results . It reported revenue of $28.30 million, up 64.24% compared to $17.23 million in Q2FY22. This growth was mainly fueled by a 62.13% growth in investment income. It has managed to beat the market's revenue expectation by $1 million or 3.67%. GHI reported a net income of $20.48 million in Q2FY23 which is a rise of 21.30% YoY compared to $16.89 million in last year's same period. Increased net income resulted in net income per BUC (beneficial unit certificates) of $0.85. GHI has managed to exceed market's net income per BUC consensus by $0.1234 or 16.98%. GHI reported $59.25 million in liquidity and total assets stood at $1.66 billion.

The net income for the quarter has experienced impressive growth, and I think that since there are more lending opportunities going forward, this performance may sustain in the future as well. In addition, I believe that these disruptive situations in banking can sustain for a long period as the Senior Loan Officer Opinion Survey on Bank Lending Practices conducted in April 2023 has estimated that lending standards can tighten in the remaining time period of 2023. As per my analysis, the next two quarters can also be impressive and we can expect significant growth as a result of reduced commercial bank lending.

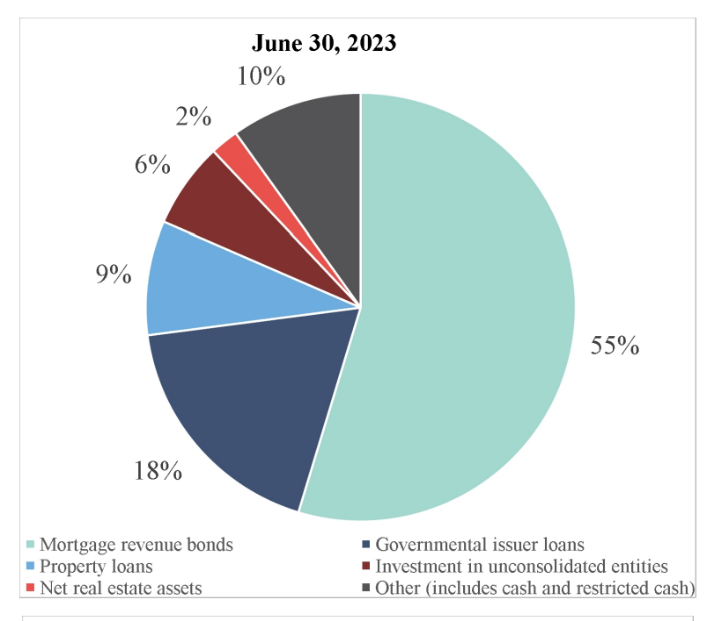

GHI's Portfolio Composition (Financial Supplemental Report: Slide No:8)

{kind=link}

Dividend Yield

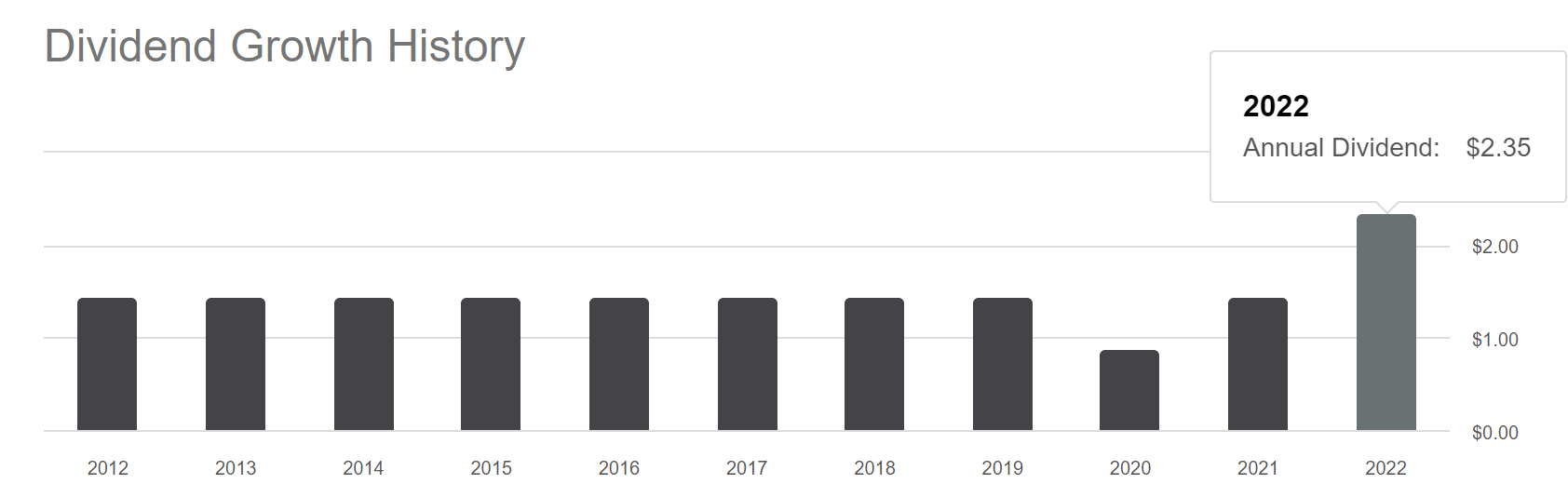

GHI has a remarkable history of dividend payouts which indicates its healthy positioning. It has paid dividends to its unitholder for ten consecutive years. The firm distributed $2.35 (including special and regular dividends) per unit yearly dividend payment in FY2022 which is a dividend yield of 14.9% compared to the current unit price. Increased investment operations in FY2023 led to a healthy performance and therefore it paid a $0.37 per unit dividend in the first quarter and sustained the same payout in the second quarter. After analyzing, the partnership's strong cash positions and growth prospects, I believe it can maintain its quarterly dividend (regular) of $0.37 in the next two quarters as well which can make the annual dividend $1.48, representing a forward dividend yield of 9.40% compared to current unit price. I am only estimating regular dividend payments to keep my estimates conservative as there is no certainty about special dividends. GHI's forward dividend yield of 9.40% is 159.43% higher than the sector median dividend yield of 3.61%. GHI's forward dividend yield of 9.40% is 26.85% higher compared to its 5-year average dividend yield of 7.38%. This appealing dividend yield makes the firm an attractive stock to hold in the portfolio to mitigate the recessionary impacts.

{kind=link}

What is the Main Risk Faced by GHI?

The partnership faces the risk related to the increasing interest rates. A significant rise in global inflation levels has driven the rise in the interest rates which has ultimately increased the cost of funding for the partnership. If the interest rates surge, it can negatively affect the partnership's operational activities due to high finance costs and may generate comparatively lower cash flows which can also further affect its dividend payout by contracting its profit margins. The increased interest rates can also negatively impact the asset valuation which can further lead to a reduction in net income.

Valuation

GHI has delivered a healthy performance which was mainly fueled by a significant rise in lending opportunities. As per my analysis, these macroeconomic conditions can prevail this year and reduce commercial bank lending by creating more opportunities for GHI. According to seeking alpha GHI's revenue for FY2023 might be $110.3 million and I believe this estimate perfectly captures the impact of above-mentioned opportunities. Therefore, I think seeking alpha's estimates are accurate. Its 5-year average net income margin is 56.1%. After considering the disruptive situations in banking sector and reducing commercial bank lending, I think GHI can maintain net income margin of 56.1% in FY2023 which gives net income of $61.88 million or earnings per unit [EPU] of $2.74. After considering all the above factors, I am estimating an EPU of $2.74 for FY2023 which gives forward P/E ratio of 5.74x.

After comparing the forward P/E ratio of 5.74x with the sector median of 9.24x, I think GHI is undervalued. I believe the partnership might grow in the coming quarters as a result of reduced commercial bank lending and ample lending opportunities which can help it to trade at its sector median P/E ratio. Therefore, I estimate GHI might trade at P/E ratio of 9.24x in FY2023, giving the target price of $25.32, which is 60.9% upside compared to the current unit price of $15.74.

Conclusion

GHI's growth has remained solid in Q2FY23 which is reflected in its financial results. It has significantly expanded its investment portfolio which has helped it to overcome macroeconomic headwinds to a large extent. However, it is exposed to the risk of fluctuations in interest rates which can contract its profit margins. The partnership pays high dividend yield which makes it an appealing option for investors who are looking for fixed regular income along with capital appreciation. GHI is undervalued and we can expect decent 60.9% growth from the current price levels as a result of ample growth opportunities due to reduced commercial lending. Considering all these factors, I assign a buy rating to GHI.

For further details see:

Greystone Housing: Solid Q2 Results Reaffirm Strong Dividend Yield