GDYN - Grid Dynamics: Better Visibility In The Near Term

2023-11-04 02:40:22 ET

Summary

- Grid Dynamics focuses on fast-growing areas of digital transformation, with potential for margin expansion and reduced client concentration.

- Q3 results showed signs of stability, with new client additions and stable operating margins, and the Q4 guidance further provides signs of demand stabilization.

- Cash to market cap remains significantly higher at 35% compared to peers trading at <10%, and current PEG of 2.2x provides a strong potential for an upside. Initiate a Buy.

Investment Thesis

We Initiate with a Buy rating on Grid Dynamics ( GDYN ) on the back of 1) strong focus on the fastest growing IT areas within digital transformation including application development, AI and data engineering and consumer experience 2) Growing customer base which has been able to reduce client concentration over time (Top 10 client concentration reduced from 61% to 54% YoY in Q3) and potential to reduce dependency further due to smaller base 3) Margin expansion potential as witnessed for other digital peers as the current margins remain well below its pre-COVID highs of 20% and is likely to rebound as demand stabilizes 4) Cash to market cap ratio is significantly higher at 35% compared to peer average of less than 10% 5) Visible signs of demand stability with flattish sequential growth and guidance and 6) comfortable valuation at 2.2x PEG compared to peer average of 4.2x

Company Background

Grid Dynamics is a global digital engineering and IT service provider focused on enterprise level digital transformation in Fortune 1000 companies. The company offers consulting, custom software design and development, testing, analytics, and internet service operations through its engineering centers across the US, Europe, Mexico and India. It has diversified revenue base with Retail and Telecom, Media and Technology contributing a third of revenue each along with CPG (20%) and Finance (7%) with other sectors making up the rest of the contribution. North America contributes more than 80% of the total revenues with top 10 clients contributing about 60% of the revenues.

Historical Financials

The company had a robust growth profile particularly post COVID as companies scrambled to boost its digital transformation amidst remote working becoming a norm. Adj. EBITDA margins dipped significantly in 2020 as a result of a decline in revenue particularly due to its relative higher exposure to retail at the time (57% contribution from retail in 2019) which was the worst affected. Adj. EBITDA margins still remains below pre-COVID levels as the company focuses on adding new customers and focusing on growth leading to slightly higher marketing spends and operational deleverage partially offset by higher utilization.

{kind=link}

The company added over 200 customers in 2021 with stable net total customers at the end of 2022 as a result of macro uncertainties leading to dollar churn and slowing technology spends. Despite that, its focused upselling and cross-selling initiatives have helped them to generate more revenues from existing customers with 48 customers spending more than $1mn in 2022 compared to just 34 in 2021 and enabled them to generate a revenue growth of 33% despite no new net customer additions.

{kind=link}

Sustained Q3 Results with Signs of Stability

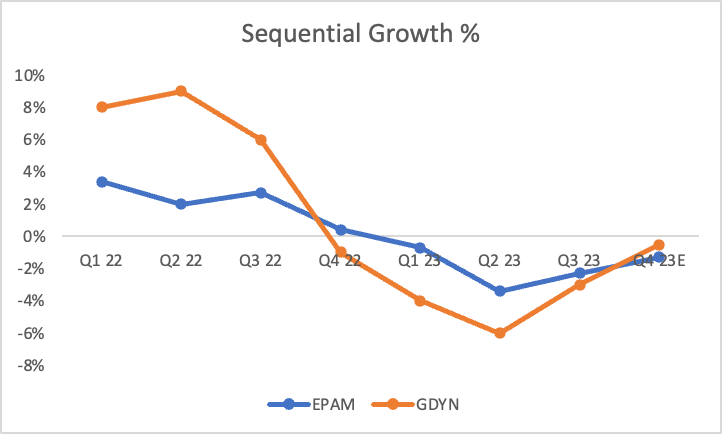

The company reported in-line Q3 results with revenues down 5% YoY driven with organic growth declining by over 11% YoY and mildly negative QoQ growth. The revenue decline was driven by weakness at large clients in the Tech and CPG verticals, in line with the consensus estimates. New client additions remained strong with the company adding a total of 10 new enterprise clients for the quarter with total of 28 clients added YTD. The growth was primarily witnessed within the financial services segment which jumped 8.2% sequentially in a tough macro environment driven by a ramp up in financial technology customers and new logos. Sequential organic growth has significantly ramped up after lagging its larger peer EPAM ( EPAM ) over the historical period.

{kind=link}

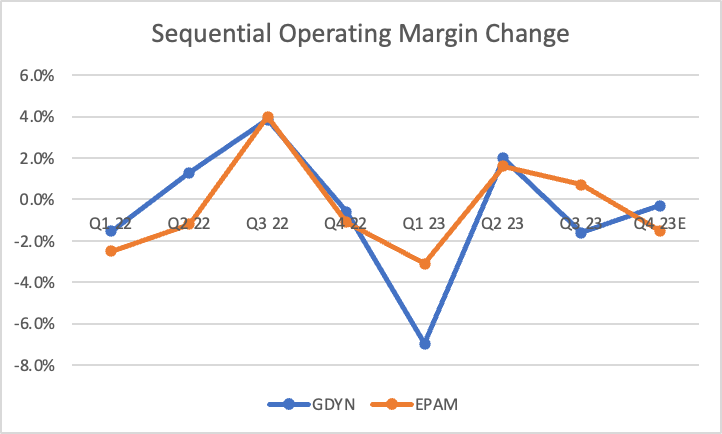

Adj. Gross margin declined over 370 bps YoY to 37% primarily as a result of user churn and relatively lower utilization. Adj. EBITDA margins declined by 720 bps at 14% as a result of decline in gross margins along with SG&A deleverage due to stick fixed costs and higher marketing expenses outpacing the revenue decline. GDYN was more impacted compared to EPAM as a result of its smaller scale and higher client concentration among its top 10 customers ramping down. However, it reported a swift improvement in operating margins with the margins stabilizing around 14% and likely to rebound in 2024 as the demand stabilizes (it already achieve 20%+ margins in Q3 2022 and Q4 2022 driven by strong operating leverage and increasing utilization)

{kind=link}

This was largely in line with the estimates as GDYN faces adverse margin pressure due to negative pricing/ wage inflation just like its peers. In all, it reported a Non-GAAP EPS of $0.08, largely in line with the consensus estimates.

Balance sheet remained strong with the company ending with cash balance of $250 mn+ with no debt allowing sufficient flexibility to invest in growth areas such as AI as well as customer acquisition.

GDYN expects revenue growth of $77 mn at midpoint which provides further signs of demand stabilization and reduction of ramp downs for its clients. Adj. EBITDA is expected to be $10.5 mn at midpoint implying a sequential margin decline by 30 bps reflecting the continued margin pressure as a result of pricing/ wage inflation dynamics. We expect 2024 revenues to grow by 10-15% YoY taking a cautious stance as a result of continued macro headwinds and assume 2024 revenues to be ~$340 - $350 mn implying a 6% growth on a 2 year stack basis. We expect Adj. EBITDA margins of 16% assuming margin expansion of 200 bps driven by improving utilization and better top line ramp up leading to SG&A leverage.

Valuation

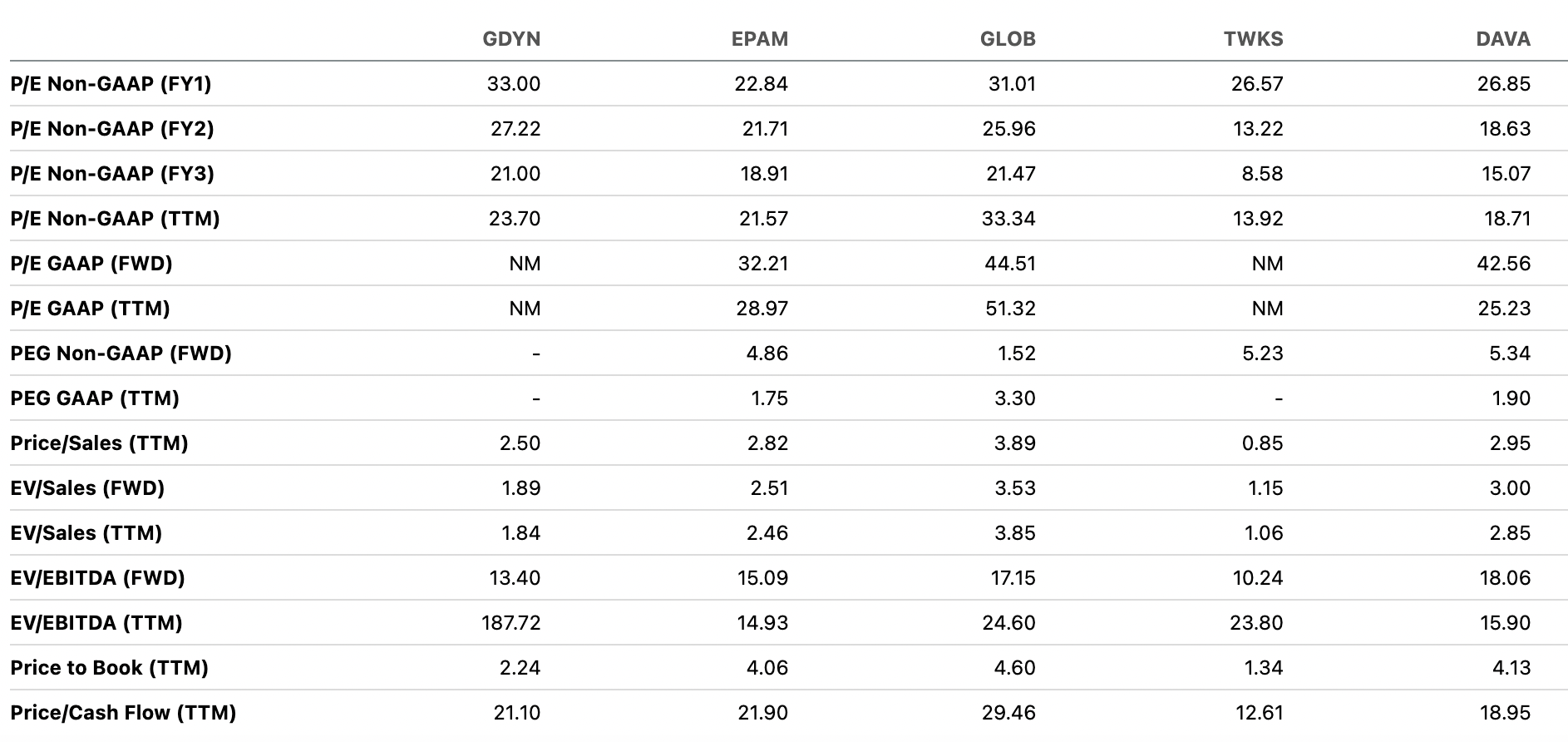

GDYN trades at 27.2x P/ 2024 EPS which appears to be at a premium to its pure play digital peer set. However, given its relatively smaller scale and growth potential compared to its peers, we believe a PEG method is a better metric to gauge the valuation. Considering a 10% growth and corresponding margin expansion, we believe the EPS growth to be at least 12% for 2024 and PEG ratio to be 2.2x which is at a discount to its peer average of 4.2x.

{kind=link}

In addition, Grid Dynamics has a sizeable cash balance with cash to market cap ratio of about 35% compared to its peers which has about 4-7% cash to market cap ratio with the exception of EPAM which has a higher 14% ratio, still significantly below GDYN. We Initiate GDYN with a Buy rating as a result of growth potential and sizeable cash balance along with valuation comfort and ascribe a target price of $15 (at 2.9x 2024 PEG, 30% discount to its peer average given smaller size and lower margin profile)

Risks to Rating

Risks to rating include

1) High customer concentration : Top 10 customers contribute about 54% of the revenues with the largest customer contributing about 14% of total revenues. This can cause significant volatility in the revenue trends and its inability to retain larger customers can adversely impact its financials

2) Geopolitical challenges : GDYN's delivery comes mostly from Central and Eastern Europe and any geopolitical issues such as Ukraine-Russia War where in it had to transfer the majority of employees in Russia outside with Russia being a key delivery center can lead to business disruptions

3) Limited Fixed Contracts : GDYN's contracts are essentially on Time & Material (T&M) model with clients not having a longer term commitment for projects which can cause volatility as witnessed during 2020 as well as currently

4) Macro Pressures : Prolonged macro pressure leading to a continued muted technology spends can adversely impact recovery

Final Thoughts

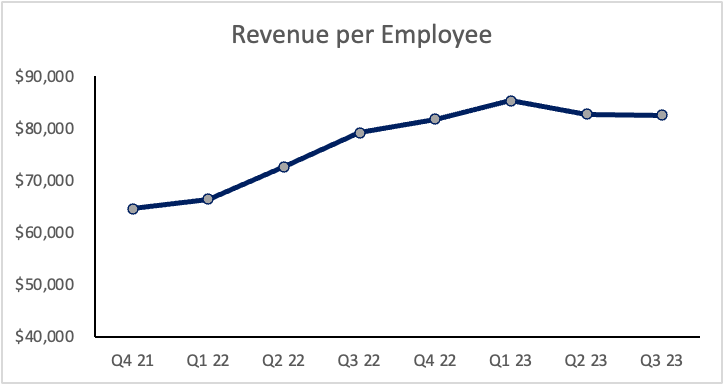

We are encouraged by the signs of stability in GDYN's results with Q4 would be the second consecutive quarter of largely flattish sequential growth, according to management's guidance. Operational metrics are trending towards positive as the company returns to growth in 2024 driven by 1) continued customer additions 2) steady increase in billable headcount with growing revenue per employee 3) traction in AI capabilities and 4) demand stability amidst flattish sequential growth with reduced client churns

{kind=link}

Initiate with a Buy and ascribe a target price of $15.

For further details see:

Grid Dynamics: Better Visibility In The Near Term