PAR - Griffon Corporation: Activist Pressure

Summary

- Since 2021, Griffon Corporation has been under pressure from activist shareholder Voss Capital (5% stake).

- Voss has criticized management’s excessive compensation as well as underperformance and has been pushing for splitting up the businesses.

- GFF’s management has been playing along with the activist thus far, with the defense electronics segment already sold and an ongoing strategic review of the garage door business.

- It seems that Voss’ campaign might be approaching the finale. Recently, the activist noted intentions to nominate its slate of directors during the upcoming shareholder meeting.

- GFF seems to be fairly valued and I would wait for a more attractive price before re-entering here.

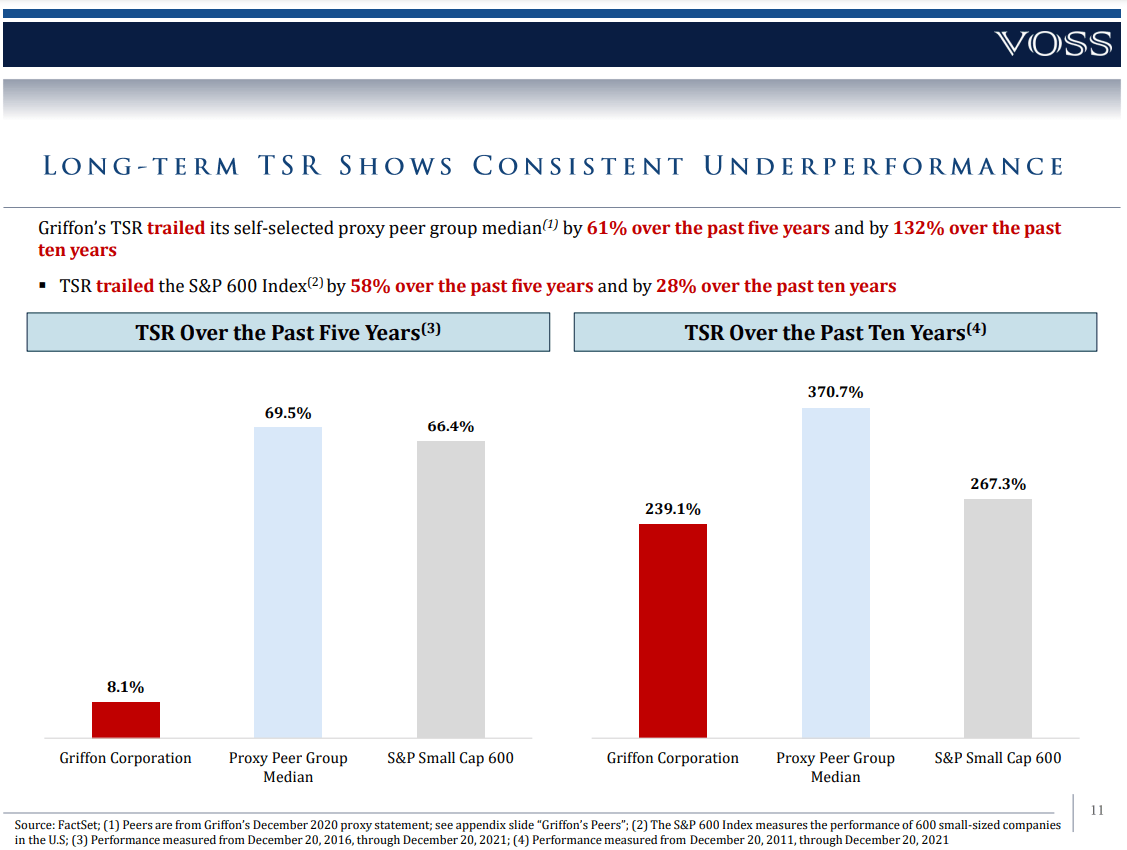

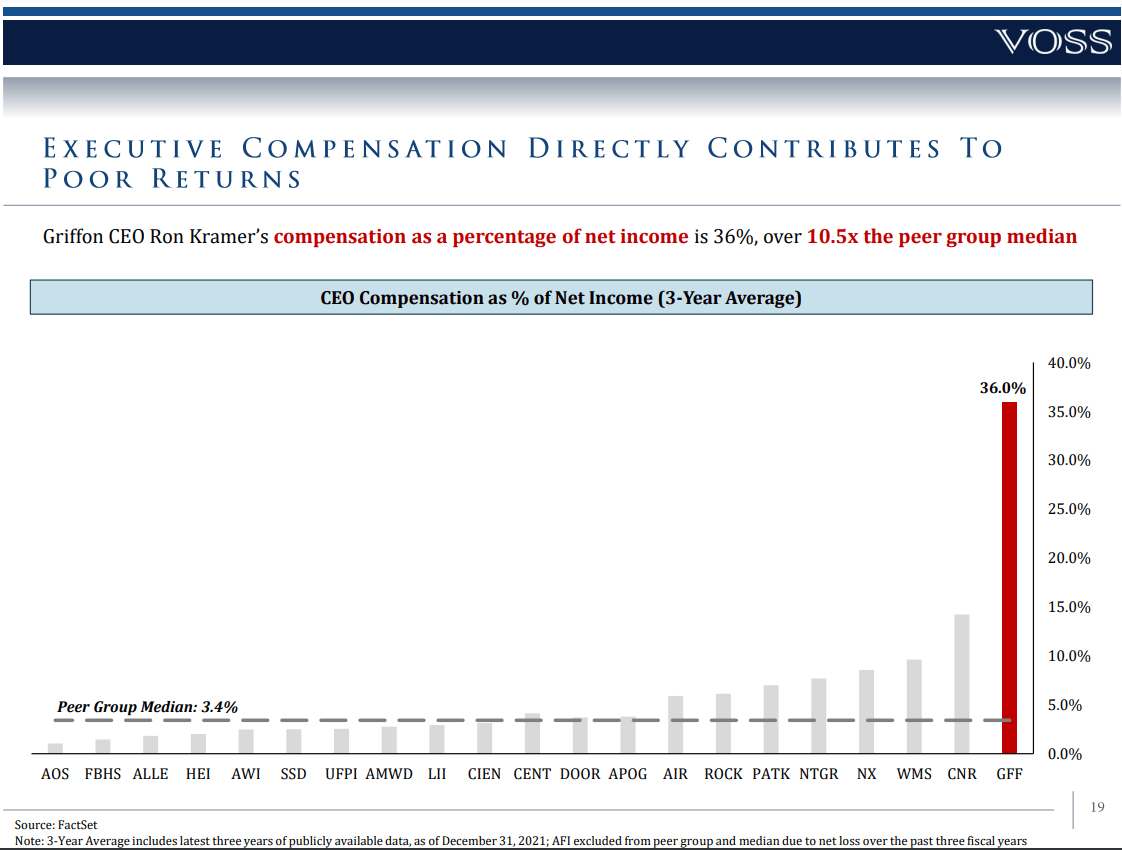

I first highlighted Griffon Corporation ( GFF ) to Special Situation Investing subscribers in late October. GFF is a $2bn market cap conglomerate which used to operate three businesses - outdoor consumer products ('CPP'), residential and commercial garage doors ('HBP'), and defense electronics ('DE'). In Aug'21, activist Voss Capital acquired a 2% stake, pushing the company to split up. The activist stated that GFF has in recent years underperformed its peers and the broader market. Meanwhile, the company's management has continued to pay themselves egregious salaries and bonuses, with the top four executives raking in $30m in FY2021 compensation. Below are several slides from Voss Capital's deck (published in Jan'22) illustrating the activist's claims:

Voss Capital Presentation, January 2022

{kind=link}

Voss Capital Presentation, January 2022

{kind=link}

The activist argued that the most valuable garage door segment was worth the entire EV of GFF at the time. Voss has been pushing GFF's management to initiate several strategic steps aimed at removing the conglomerate discount, including selling the DE segment and initiating a strategic review of the HBP business. Other potential measures including right-sizing corporate overhead as well as reducing debt and paying a special dividend were suggested. Finally, Voss Capital noted that there is substantial room to improve margins of the underperforming CPP business which has been lagging behind its closest peers.

In Feb'22, Voss Capital won 1 out of 13 board seats and the management has been playing along the activist ever since:

- In Apr'22, GFF agreed to sell its DE business for $330m in cash and used the proceeds to repay debt and payout a special dividend.

- A month later, the company initiated a strategic review for the remaining business, hiring Goldman Sachs.

- Then, in Aug'22, Voss raised its ownership stake to 5%, hoping that the strategic review will create value for shareholders. Voss expressed support for management's actions.

- In Oct'22, GFF postponed the shareholder meeting from Feb'23 to Mar'23, namely to give Voss (and potentially other shareholders) more time to properly nominate its director candidates.

- Most recently, last week Voss filed a fresh 13D, putting out its slate of 7 director nominees. GFF's board has 14 directors, one of them already being nominated by Voss.

Clearly, Voss pressure on management has worked well so far. Not surprisingly, the market has reacted favorably to the these developments. GFF is up 22% since my initial highlight and 26% since the beginning of 2022, displaying investors' heightened confidence in the company's prospects given the success of the campaign so far.

Valuation

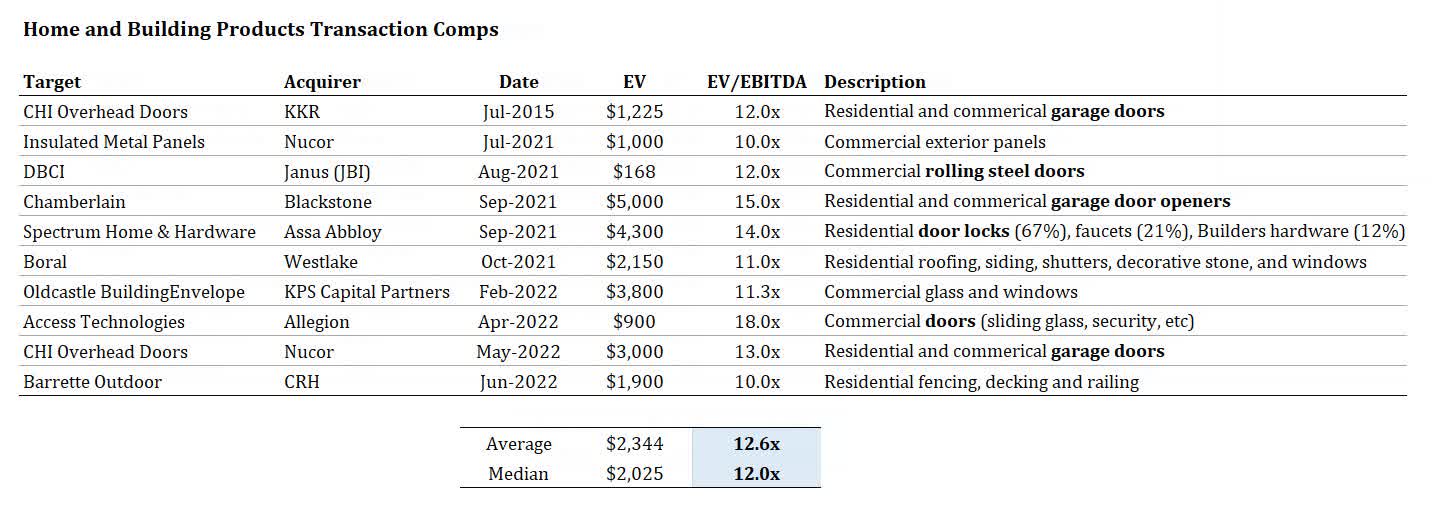

The main question here is the remaining upside. GFF's valuation largely hinges on the multiple assigned to the HBP segment. Comparable industry transactions (provided below) suggest the HBP segment could fetch a 13x multiple in a sale scenario. Note that HBP is industry leader in the garage door market in the US. A noteworthy recent transaction is Nucor acquiring CHI Overhead Doors from KKR in Jun'22 at a 13x TTM EBITDA multiple.

{kind=link}

Estimating HBP's normalized EBITDA seems to be the main issue here. The business generated $413m in TTM adjusted EBITDA - materially above FY2019-FY2021 levels of $120m-$181m. This year's performance is explained by a massive increase in pricing despite flat volumes. The company expects $500m in FY2023 adjusted EBITDA, implying earnings of the HBP business in line with TTM figures. These earnings are clearly not sustainable going forward. Estimating HBP's normalized earnings at $290m, the remaining CPP business would be valued at 6.2x EBITDA which seems to be a reasonable multiple. This suggests there might be limited upside from current GFF share price levels.

Risks

The situation has several caveats:

- As discussed above, the main issue here is estimating GFF's normalized EBITDA.

- It is not clear if GFF can find a suitor for the HBP business. The management initially expected to provide an update on the ongoing strategic review in Nov'22 with the release of FY22 annual results. However, in the earnings release, the company noted that process is active and "discussions with potential counterparties are ongoing". The delay in reaching the strategic review conclusion might potentially suggest that the company is having trouble finding acquirers for the HBP business.

- Another risk is GFF's management (10% ownership stake) opposing any transaction or continuing to arguably waste shareholder value even after a potential HBP segment sale. The management is entrenched - the current CEO is the son-in-law of the previous CEO who was the son-in-law of the CEO before that. The leadership is getting compensated very well, with the CEO alone pocketing around $20m per year. Moreover, the company has previously pursued expensive/poor mergers, such as acquisition of Hunter Fan for $845m in Jan'22. These arguments suggest there might be a risk that the ongoing strategic review is just for show. Having said that, the activist Voss Capital seems highly committed here and one cannot neglect the possibility of activist's nominees taking over the board during the upcoming shareholder meeting.

Voss Capital

Voss Capital is a small hedge fund with $360m in AUM. Despite its tiny size, Voss has already achieved quite impressive results in several campaigns:

- In Dec'19, Voss Capital acquired a 10% stake in Benefytt Technologies, noting the company might be an attractive M&A target. Benefytt was eventually bought by Madison Dearborn Partners in Aug'20. Voss pocketed a 66% return in nine months.

- In Jan'20, Voss filed a 13D with Rosetta Stone, disclosing a 5% stake in the company. Rosetta was acquired by Cambium Learning in Oct'20, delivering the activist a 62% return in nine months.

- In Oct'18, the activist sent a letter to PAR Technology (NYSE: PAR ), pushing for the company to split up. While PAR has since retained its two business segments, the activist apparently pocketed 470% return in four years from its position as the share price has soared.

- Voss has also noted a successful participation in Quorum Information Technologies (QIS), which apparently yielded 260% in six years.

Business

GFF's CPP segment conducts its operations through AMES which is a North American manufacturer of branded consumer and professional tools used in home storage, organization and landscaping. The segment includes Hunter Fan business which GFF acquired in Jan'22.

Meanwhile, HBP segment is run through Clopay which is the largest manufacturer of garage doors and rolling steel doors in North America. The segment's products are sold through home center retail chains as well as professional dealers. The business expanded into the commercial rolling steel door segment with the acquisition of CornellCookson in Jun'18.

Both historical segment sales and adjusted EBITDA are provided below:

Author's Calculations.

Note: GFF's fiscal year end in September.

Conclusion

Considering the activist's success thus far, I expect a HBP business sale to eventually materialize here. Having said that, it seems that currently the market values GFF fairly. Given little upside from current share price levels, I am inclined to stay on the sidelines for now. The situation, however, might become interesting again if GFF share price comes back to lower levels.

For further details see:

Griffon Corporation: Activist Pressure