GFF - Griffon Corporation Decides To Carry On With Its Current Strategies

2023-06-11 07:36:29 ET

Summary

- Griffon Corporation's sales in the repair and remodeling market have improved, and the company is focusing on capturing additional business in this space.

- The company faces challenges in the Consumer and Professional Products segment, with low demand in lawn & garden, storage, and organizational markets affecting sales and margins.

- Despite high leverage, Griffon Corporation's stock appears relatively undervalued, and investors are advised to hold the stock for medium-term gains.

Opportunities And Challenges

Griffon Corporation's ( GFF ) consumer brand portfolio includes residential, industrial, and commercial fans, home storage, residential and commercial sectional garage doors, rolling steel doors, and grille products. In recent months, GFF's sales in the repair and remodeling market have improved remarkably. Its current strategy involves capturing additional business in this space as it leverages its sectional and rolling steel products. After exploring various strategic options, the company's management believes that its plans are optimized to maximize shareholder returns. So, it has increased dividends and initiated a share buyback plan.

But the company faces various obstacles in the Consumer and Professional Products business. Low demand in the lawn & garden, storage, and organizational market reduced sales and adversely affected the segment's operating margin. Underperformance in the segment also led to a significant impairment charge in Q1. Despite high leverage (debt-to-equity), long debt maturity relieves short-term financial risks. The stock appears relatively undervalued. I would suggest investors "hold" the stock with an expectation of higher returns in the medium term.

Market Trends

{kind=link}

In April 2023, the US unemployment rate declined to one of the lowest rates in the past several decades to 3.4%, falling from 3.5% in the previous month. The ISM Manufacturing PMI improved (47.1) marginally month-over-month but remained below 50. Economic activity in the manufacturing sector shrank due to higher borrowing costs. Total output and new orders also softened during the month.

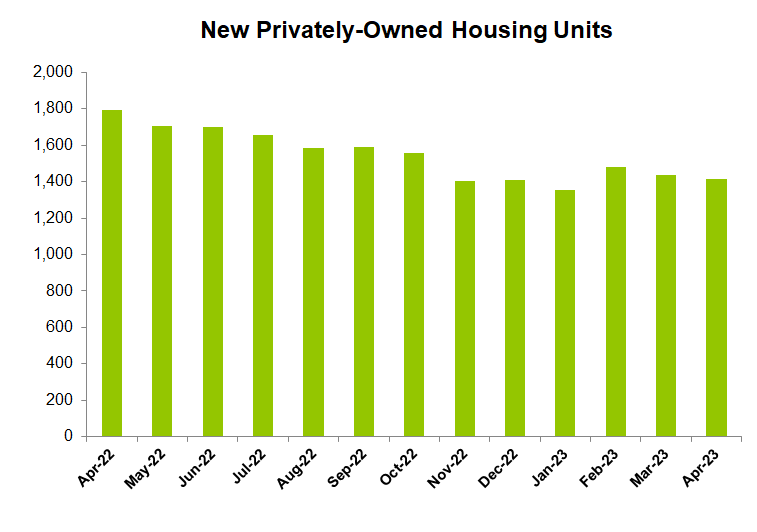

The new privately-owned housing units in the US are returning to the pre-pandemic level. From April 2022 until January 2023, it dipped by 25%. Since then, it has shown signs of consolidation and increased by 4.6% until April. In the residential product market, this allows GFF to improve sales for the repair and remodeling market. On the other hand, the company's Consumer and Professional Products segment has grappled with various challenges. But the company's management is optimistic that the scenario will stabilize over time.

Understanding The Drivers

{kind=link}

Let us dive into the nuances of the Home and Building Products segment business and why it has strengthened. Nearly all the sales tenets have improved, e.g., volume, price, and mix. Residential volume was an exception, but still performed better than the company's estimates. Moreover, its sectional door backlog, which saw increased lead time during the pandemic, appears normalizing. The company's current strategy involves capturing additional residential and commercial businesses. It plans to leverage its sectional and rolling steel products, complemented by innovative product offerings.

Readers might also want to be vigilant of the challenges in the Consumer and Professional Products business. Reduced consumer demand affected sales in nearly all channels and geographies, leading to higher inventory. The situation was particularly rough in the lawn & garden, storage, and organizational markets because of buyers' diversification following the pandemic. The lower volume also affected the overhead absorption and operating leverage, so some product lines became unviable for profit-making. The company is trying to lower costs by sourcing long-handled tools, material handling, and wood storage from global suppliers to counter lower margins.

Near Term Outlook

The management expects its global sourcing strategy to evolve into being more flexible and cost-effective to meet variable demand and improve profitability. It has leveraged its brands while strengthening its competitive positioning with distributors and customers. In the CPP segment, the company plans to achieve targeted EBITDA margins of 15% compared to an adjusted EBITDA margin of 6.2% in Q2 2023.

FY2023 Guidance

Based on the sales and profitability achieved in 1H 2023 and the continued challenges in the CPP segment, the company's management has lowered its FY2023 revenue estimates by 8.5% to $2.7 billion from previous guidance of $2.95 billion. However, lower sales volume in CPP would be balanced by higher profitability in the HBP segment. So, of the prior guidance, it increased its EBITDA target for FY2023 by 5% to $525 million.

Strategic Review And Outcome

Starting in 2022, GFF began exploring various strategic alternatives to increase shareholders' values. In 2023, it has decided that the company's current plans and growth prospects are second to no other options. So, the Board has concluded it will pursue the current strategic plan to maximize shareholder value. However, the management did express its belief that there is a fundamental disconnect between its share price and the intrinsic value of its businesses. So, it may commit a variety of actions to provide additional value. In the future, it may be open to other opportunities, including capital events like M&As and others.

For example, in recent times, its CPP segment expanded its global sourcing strategy for its US products. It plans to close four manufacturing facilities and four wood mills. The entire restructuring project can complete by 2024-end. It may incur charges in this connection, including employee retention, operational severance transition, and facility costs. In 2022, Griffon acquired one of its competitors – Hunter. The company offers residential ceiling, commercial, and industrial fans, complementing and diversifying GFF's reach.

Segment Performance And Drivers

{kind=link}

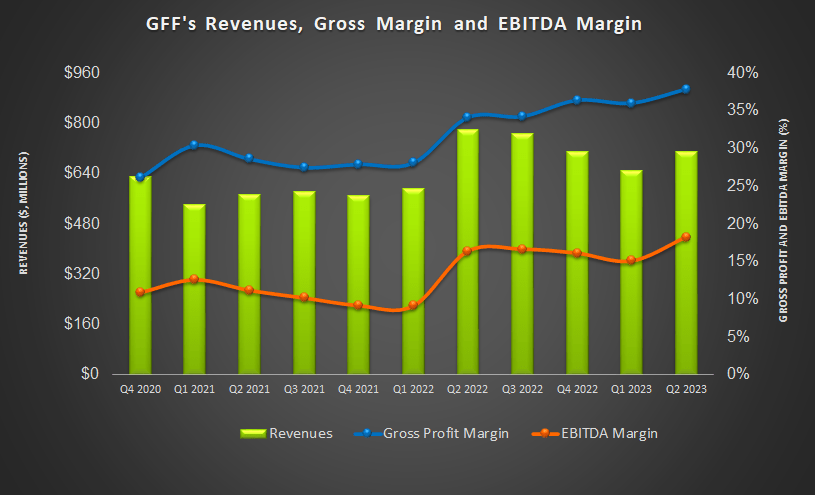

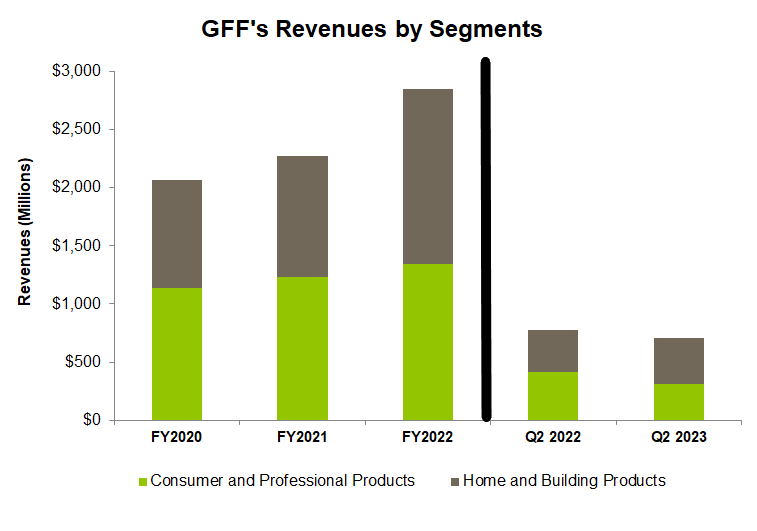

From Q2 2022 to Q2 2023, GFF's Consumer and Professional Products segment revenues decreased by 24%. Less demand and higher customer inventory levels led to the topline drop. The lower volume also triggered higher manufacturing and overhead absorption, leading to a 540-basis point adjusted EBITDA margin fall over the past year in Q1 2023.

In contrast, the company's Home and Building Products segment saw year-over-year revenues increase by 8% in Q1, 2023. The adjusted EBITDA margin in this segment expanded by 490 basis points. Improved pricing and a better mix of commercial and residential products benefited its operating performance. However, increased labor transportation, advertising, and marketing costs partially offset the margin growth during the quarter.

Impairment Charges In Q1

In Q1 2023, the company recorded a net loss of $1.17 per share compared to a net income of $1.23 a year ago. Asset impairments in the CPP segment and global sourcing expansion caused the net income to decline. During Q1 2023, it recorded a $100 million (pre-tax) impairment charge related to the indefinite-lived intangible assets after its 1H 2023 results fell below expectations.

Cash Flows And Shareholders' Returns

In 6M 2023, GFF's cash flow from operations (or CFO) turned strongly positive compared to negative CFO a year ago. Although revenues remained nearly unchanged over the past year, improving working capital led to an improvement in CFO. Free cash flow (or FCF) (excluding acquisition) also turned positive in the past year. Investors may recall that in January 2022, GFF acquired Hunter for $854 million.

The company's debt-to-equity (3.2x) is much higher than its competitors (TGLS, DOOR, and PGTI). Although its debt level is high, most are not due to retire before 2028. It also has $532 million in liquidity as of March 31. As its FCF improved, it recently increased its dividend by 25% to $0.50 (annualized). It also declared a $2 per share special dividend, and then increased its share buyback to $258 million.

Analyst Rating And Relative Valuation

{kind=link}

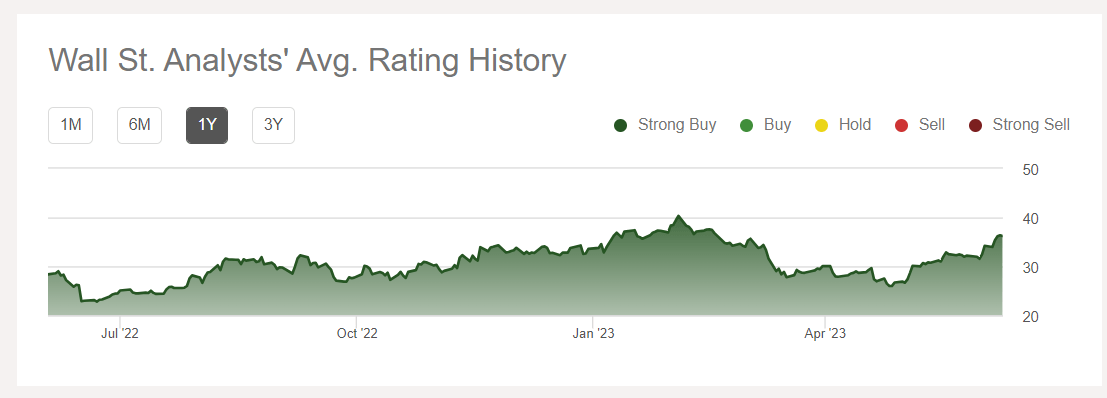

According to data provided by Seeking Alpha, six sell-side analysts rated GFF a "buy" in the past three months (including "Strong Buy"), while none rated it a "hold" or "sell." The consensus target price is $48.6, suggesting a 34% upside at the current price.

{kind=link}

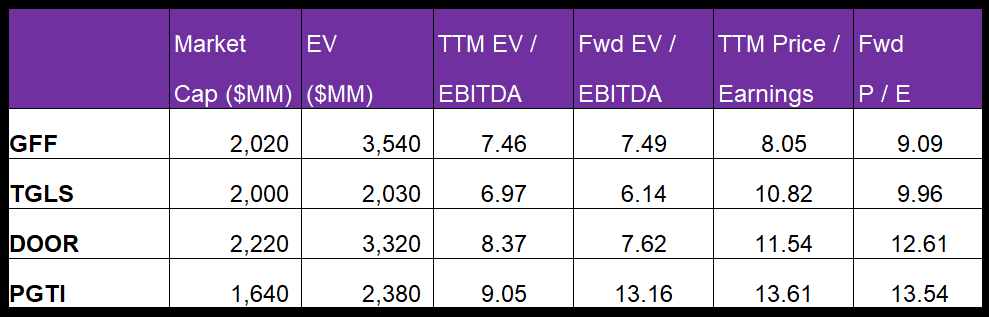

GFF's forward EV/EBITDA multiple changes versus its current EV/EBITDA is expected to remain unchanged, in contrast to a rise in for its peers. This typically results in a higher EV/EBITDA versus its peers' multiple because its EBITDA is expected to remain unchanged compared to a fall in EBITDA for its peers. The company's EV/EBITDA multiple (7.5x) is lower than its peers' (TGLS, DOOR, and PGTI) average (8.1x). So, the stock appears to be reasonably undervalued versus its peers.

What's The Take on GFF?

{kind=link}

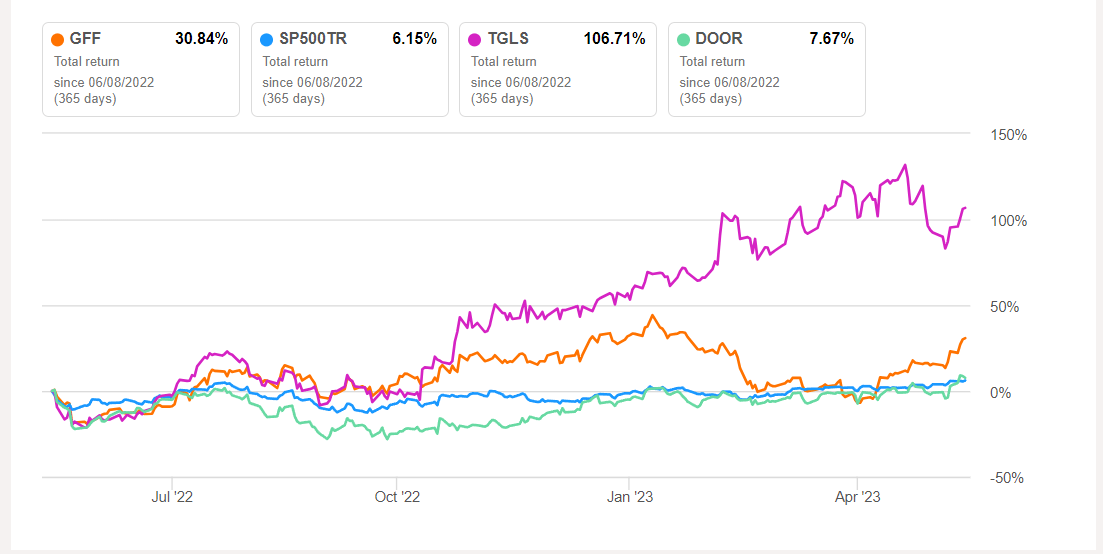

Over the past few months, the US housing market has tightened, allowing GFF to improve sales in the repair and remodeling market. Its current strategy involves leveraging its brands while strengthening its competitive positioning with distributors and customers. In 2022, Griffon acquired Hunter - one of its large competitors that complemented and diversified its global reach. So, the stock outperformed the SPDR S&P 500 ETF ( SPY ) in the past year.

On the other hand, the company's Consumer and Professional Products segment has grappled with various challenges. Low demand in the lawn & garden, storage, and the organizational market looks to continue in the near term. Its leverage (debt-to-equity) is alarmingly high. But it has robust liquidity. Also, in 6M 2023, GFF's cash flows improved significantly due to improved working capital. Given the stock's relative undervaluation, investors might want to "hold" the stock at this level.

For further details see:

Griffon Corporation Decides To Carry On With Its Current Strategies