GFF - Griffon Corporation: Lower Demand Is Priced In Right Now

2023-10-01 05:51:38 ET

Summary

- Griffon Corporation's share price has been steadily climbing but is not yet considered overvalued, with a p/e ratio under 10.

- The company's Consumer and Professional Products segment generates the most revenue, but growth is hindered by rising interest rates and a slowdown in new buildings.

- Griffon is reshaping its product portfolio and making acquisitions to position itself as a leader in the industry, but reducing debt and improving margins are key challenges.

Investment Rundown

The share price for Griffon Corporation ( GFF ) has been on a very stayed climb the last couple of months, but perhaps not yet reached a point where it can be considered overvalued. The p/e is under 10 which represents a discount of around 40% to the sector. That type of discount seems only applicable to companies that are struggling or who are facing weaker demand and the prospects of growth are diminishing. For GFF it seems to be the latter right now as they noted an 11% decline in revenues in the last quarter in a year-over-year comparison. This is a worrying trend that I think has merit to be kept up, unfortunately as long as interest rates remain elevated and consumers have less free capital to spend, lowering the activity in the economy.

However, as I said, the valuation of the business is not overvalued, but rather accounting very well for these risks, and therefore I won't say it's a sell. Instead, I am rating GFF a hold right now and potentially a buy if the demand can increase, and we can see a clear recovery of it as well in coming quarterly reports from the business.

Company Segments

GFF offers an array of consumer, professional, home, and building products across a diverse range of global markets, including the United States, Europe, Canada, Australia, and beyond. The company is included in the industrial sector, but more specifically the building products industry.

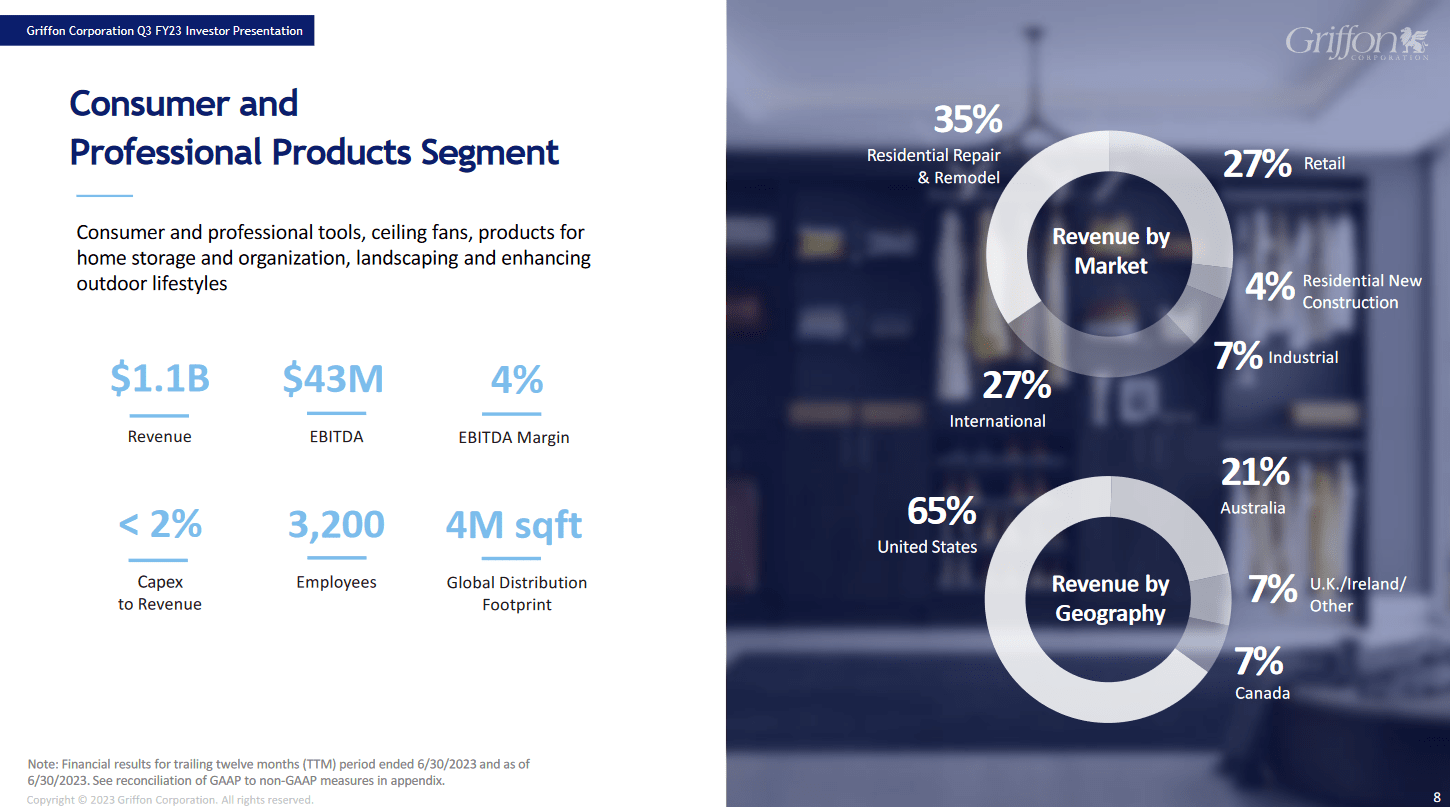

Within its large product and service portfolio, the company's Consumer and Professional Products segment stands out, focusing on the design, manufacturing, and distribution of a wide spectrum of long-handled tools and landscaping products. These offerings cater to both homeowners and professionals alike, catering to a broad spectrum of customers with varying needs and preferences. This is also the segment that is generating the largest amount of revenue for the business at $1.6 billion in the last 12 months.

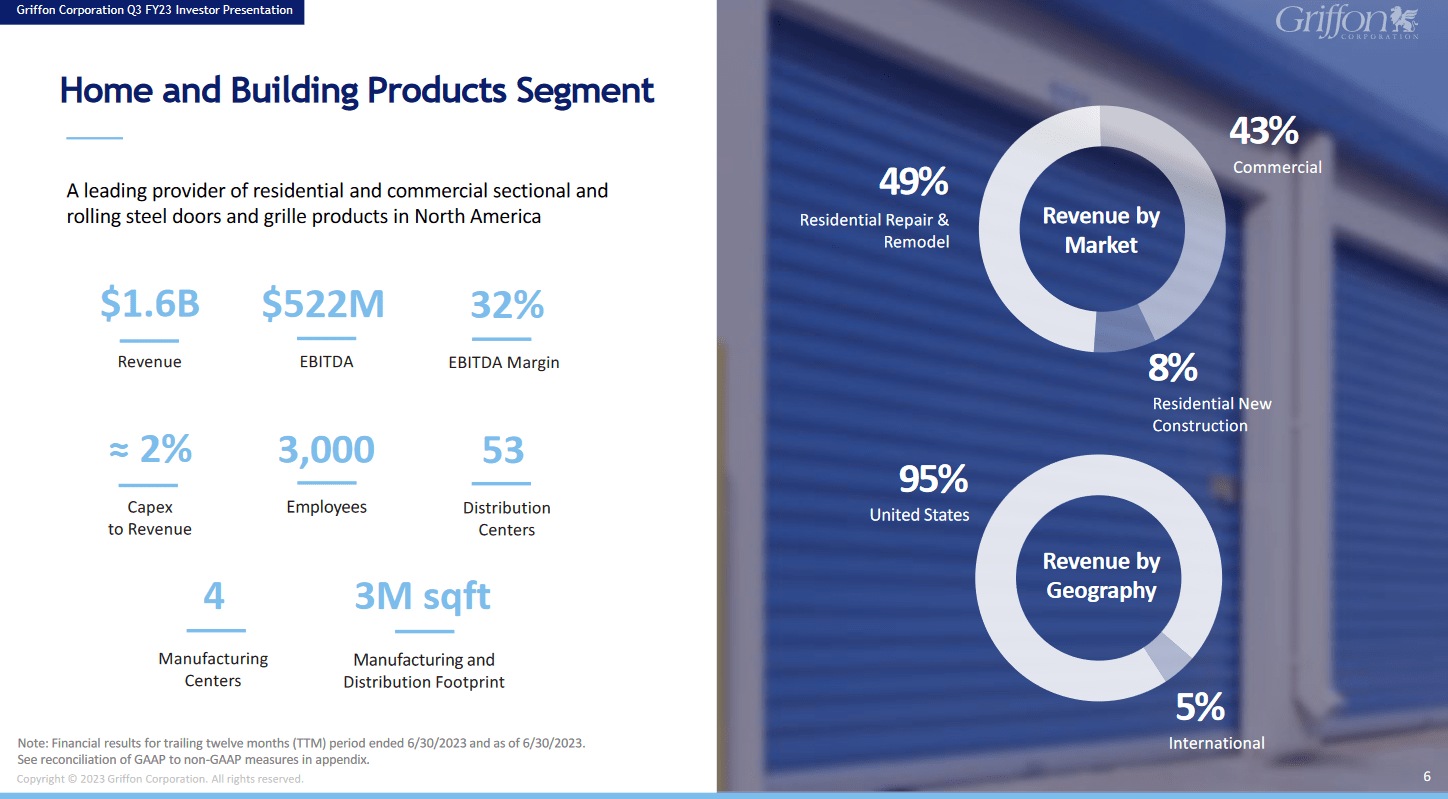

Segment Overview (Investor Presentation)

{kind=link}

What is causing some issues though for the growth of the business is the rising interest rates which are hammering down on the spending of average Americans and their home needs a building products are decreasing. Besides, there is also a slowdown in new buildings in the country which is just adding more fuel to the fire which is the lower demand GFF is faced with.

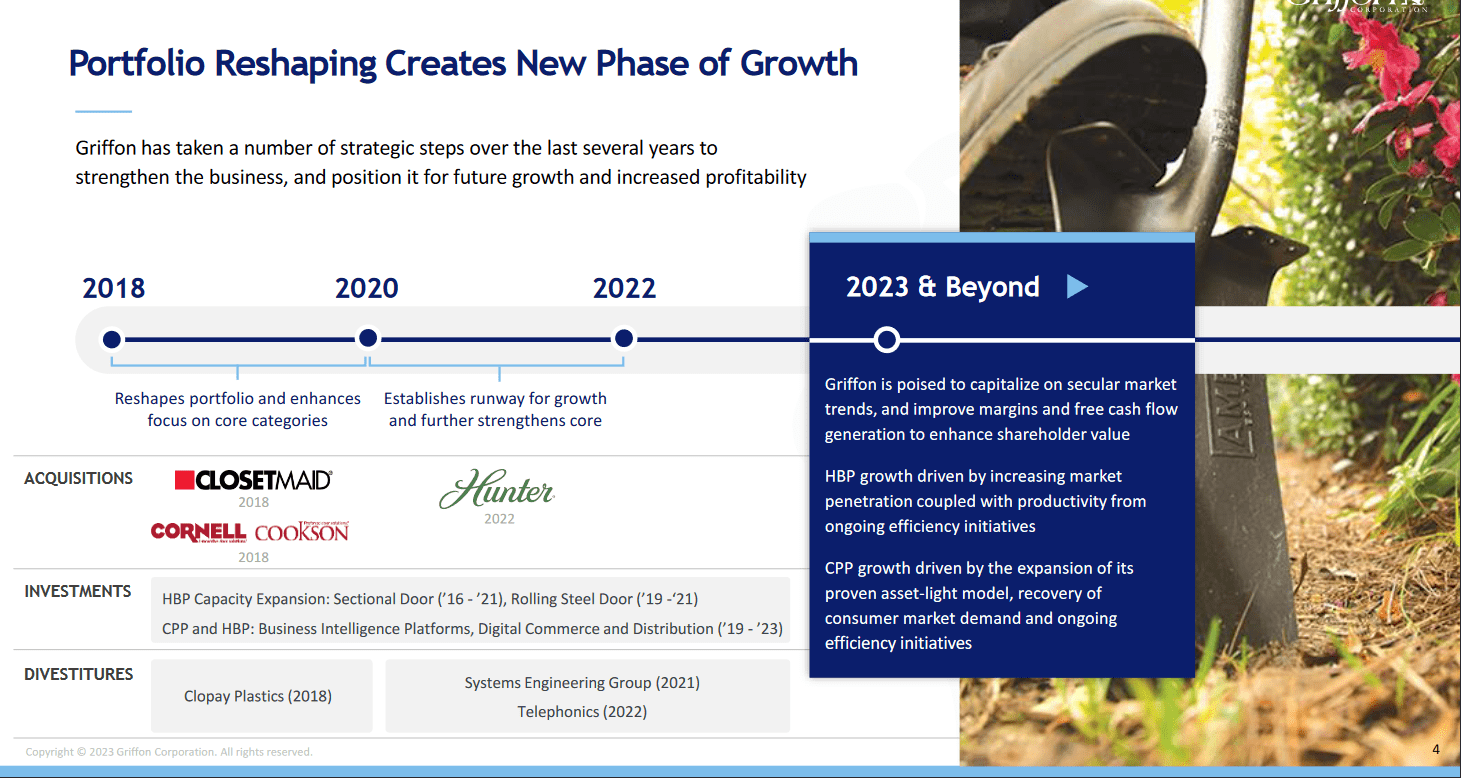

Portfolio Overview (Investor Presentation)

{kind=link}

But GFF is not sitting idle right now to just wait out the lower demand. No, they are reshaping their portfolio of products and focusing on intensifying growth to become a leader in the space once again. The company has made a few acquisitions over the last couple of years and I think this will help carry the company forward once demand resumes. With a more diverse portfolio of services and products thanks to several acquisitions, GFF is in a better position now. In 2022 for example, GFF acquired Hunter Fan Company, essentially netting themselves a significant market share in the market for ceiling fans, another step towards creating a broad set of product names for customers. A leading indication of rising demand will likely come from lower interest rates. More cash available for end consumers will lead to more orders, most likely.

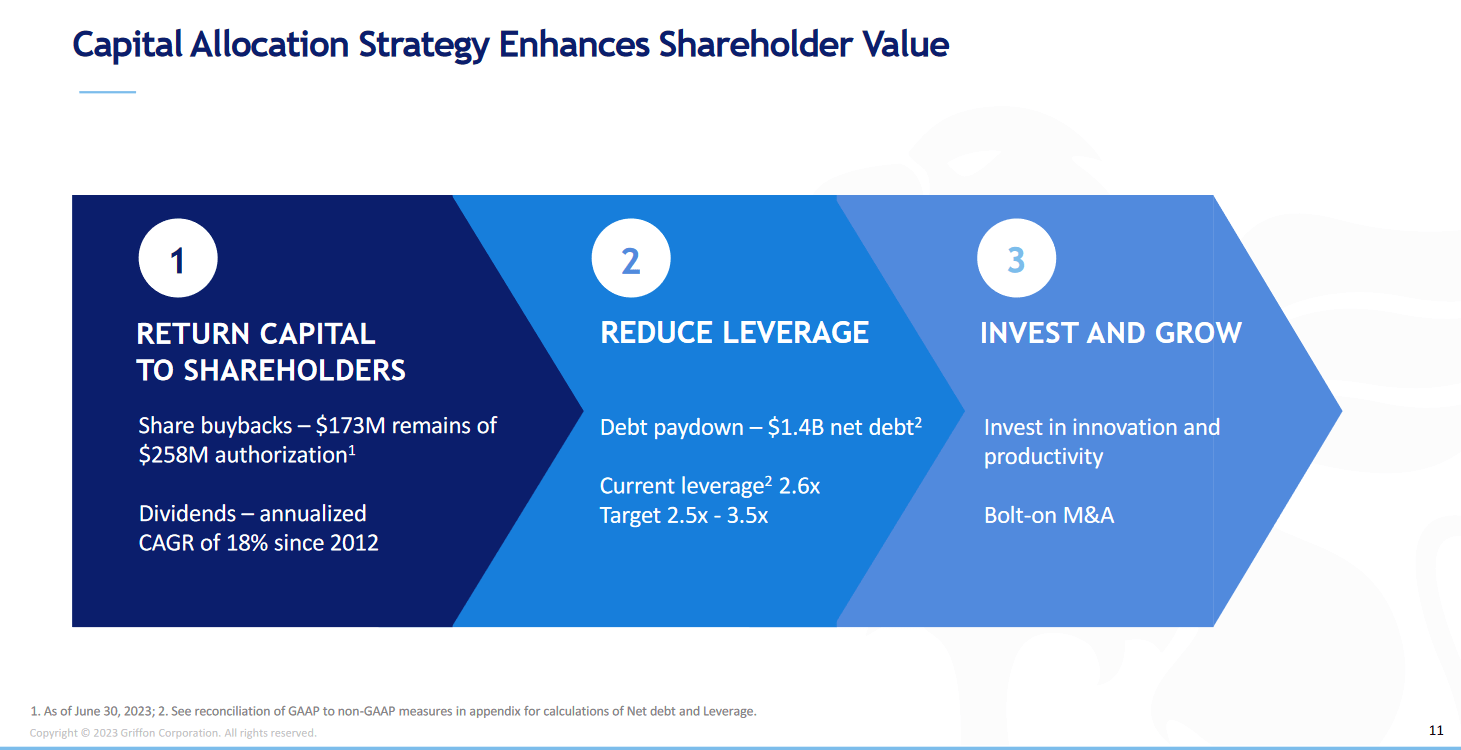

Capital Allocations (Investor Presentation)

{kind=link}

Looking at the capital allocations for the business, the priorities are quite clear in that paying down debt is not at the top, as returning shareholder value is more important. I find that the larger debt position the company has should be prioritized more. It is digging into the earnings of the more important business right now and then ensuring investors get more buybacks. With higher debts comes higher interest expenses, and that diverts earnings away from buybacks in times of higher interest rates environment, like now. A less leveraged position should also lead to a higher price as the risk profile improves. The company however does still have $173 million left authorized for buybacks, which would reduce the outstanding shares by a little over 5% if all used right now. The dividends however have seen a strong momentum in terms of growth as since 2012 it has averaged an 18% CAGR. I think the coming years won't display the same growth, more like 7 - 8% maybe, if demand is finding its floor right now. If times become even worse than perhaps an even lower divine growth rate will be noticed and the share price likely fall as a result of it.

Risks

Within the Consumer and Professional Products business, several challenges loom ahead for the company. Notably, the demand for products in the lawn & garden, storage, and organizational sectors has witnessed a decline, resulting in reduced sales volumes. This, in turn, has exerted downward pressure on the operating margin of this particular segment. It's worth noting that the intricate interplay of market dynamics has posed obstacles to the company's growth trajectory in this area.

Segment Overview (Investor Presentation)

{kind=link}

With a rising debt level as well, the margins for GFF have been under pressure as the company now has the highest interest expenses in its history at nearly $100 million. That is an increase of around 30% since 2021, all the while net incomes have not seen the same improvements. With long-term debts of over $1.5 billion, I think that GFF does have a slightly high leverage ratio, which could be a reason for the lower valuation the company is currently receiving as well. Until there is more cash diverted to paying down debt, I think that GFF will continue to be valued quite low.

Final Words

GFF has had some tough last few quarters as the higher interest rates are digging into the demand from end customers. With less capital available to spend, the customers purchasing directly from GFF are lowering their inventory levels and not refilling them as quickly as before, as was seen in the last report .

The share price is receiving a very high discount based on earnings alone, but it seems warranted given the current market conditions and the uncertainty of when demand will once again start to pick up. For me, GFF represents a hold right now until there are clear improvements in demand.

For further details see:

Griffon Corporation: Lower Demand Is Priced In Right Now