TGLS - Griffon Corporation: Opening The Door To Higher Returns

2023-03-20 18:01:10 ET

Summary

- Griffon Corporation has done quite well recently from a sales, profit, and cash flow perspective.

- The company looks solid, and management expects growth to continue this year.

- Shares look cheap at this point in time, and it's likely that the business won't experience material weakness until after 2023.

In this environment, with high inflation and rising interest rates aimed at combating it, it may seem a bad idea to buy into anything that's connected to the construction space. After all, parts of this market are experiencing weakness already, while others could face weakness in theory because of the impact that both inflation and interest rates have on the ability and willingness of individuals and companies to spend. However, one company that operates in this space that I do believe offers additional upside is Griffon Corporation ( GFF ), an enterprise that produces and sells home and building products such as garage doors, rolling steel doors, and more. It also produces consumer and professional products such as tools for home storage and organization, landscaping, and other activities. In recent months, shares of the business have risen even as the broader market declined. Because of how the economy is performing more broadly, investors may think that now would be a good time to cash out. But between how cheap the stock is and because of some favorable economic data, I do think that further upside from here is warranted.

Don't close the door on this one yet

Back in July 2022, I found myself taking a bullish stance on Griffon. Management had been forecasting strong results for the 2022 fiscal year on both the top and bottom lines. Shares of the firm looked cheap, and the company was undergoing a strategic alternatives review to see whether it might make sense to sell the company, merge it with some other player, or engage in some other transaction that would add value to its shareholders. All of these factors combined led me to rate the business a 'buy' to reflect my view at the time that shares should generate an upside that would exceed what the broader market would experience over a similar timeframe. As of this writing, I would say that this particular call was a success. While the S&P 500 is down 2.7%, investors in Griffon would have made 8%.

{kind=link}

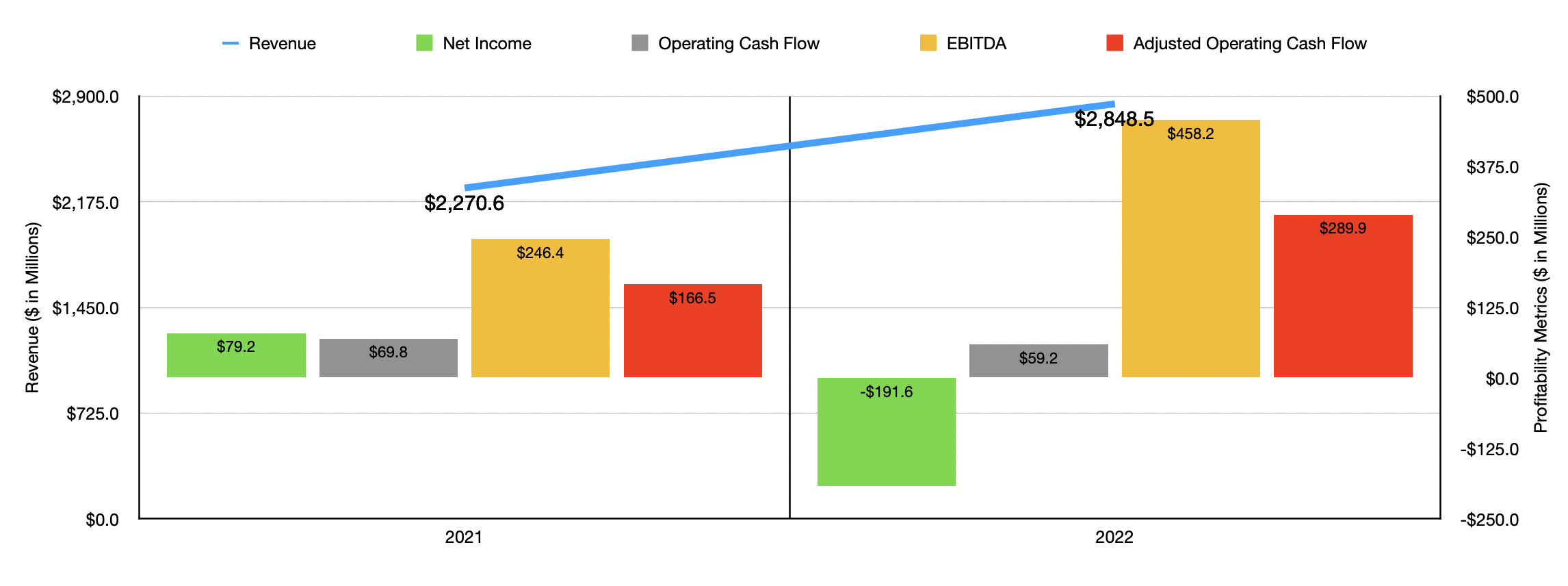

If you look at the headline data, the picture for the business looks rather robust. In the chart above, you can see financial data for both 2021 and 2022. You'll notice that sales and cash flows, for the most part, rose materially. The bottom line for the company as measured by its net income did take a hit. By considering that cash flow should be considered more important and considering that it fared very well, I would call 2022 a win for the business. In the chart below, you can see that the positive trend for the firm has continued.

{kind=link}

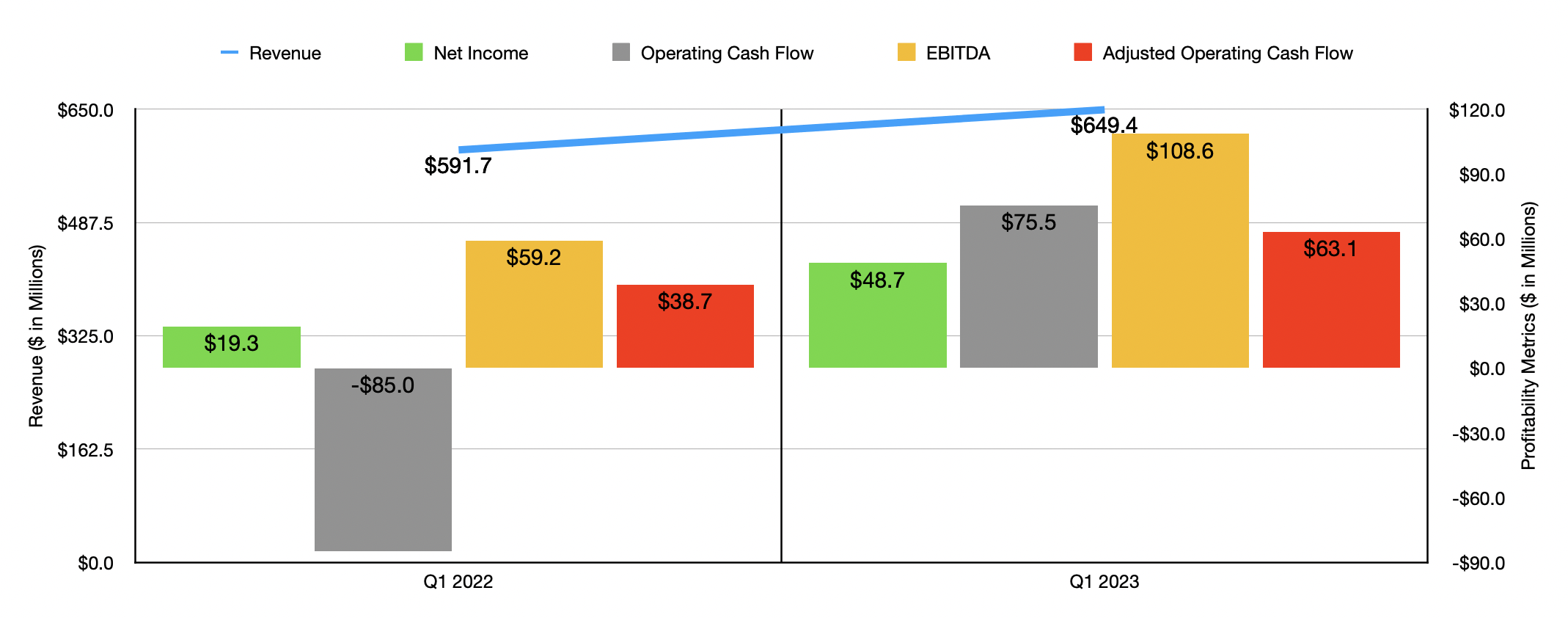

For the first quarter of 2023, revenue came in at $649.4 million. That's 9.8% higher than the $591.7 million the company reported only one year earlier. Even though the company faced significant weakness in some areas, it experienced strength elsewhere. Under the residential repair and remodel category, for instance, revenue skyrocketed 48.2% from $183.4 million to $272.4 million. This increase, management said, was driven in large part by favorable pricing and product mix, as well as a rise in volume, both under the Home and Building Products segment. They were less open regarding the specific cause under the Consumer and Professional Products segment, but it's likely that the rise under the residential repair and remodel category was driven in large part by the same things. The surge in revenue for the company brought with it higher profits as well. Net income more than doubled from $19.3 million to $48.7 million. Operating cash flow swung from negative $85 million to positive $75.5 million. On an adjusted basis, it almost doubled from $38.7 million to $63.1 million. And finally, EBITDA for the company expanded from $59.2 million to $108.6 million.

Although it's still early in the 2023 fiscal year, management does have some pretty solid expectations for how the company should perform for the entirety of the year. They currently think that revenue should come in at around $2.95 billion. That would translate to a year-over-year improvement of 3.6%. In addition to this, EBITDA (excluding certain unallocated expenses) should be $500 million or more. With $56 million worth of costs factored back into the equation that should be there anyways, that number comes down to about $444 million. That's down marginally from the $458.2 million the company reported for 2022. No guidance was given when it came to adjusted operating cash flow. But based on my estimate, it should be around $280.9 million for the year.

{kind=link}

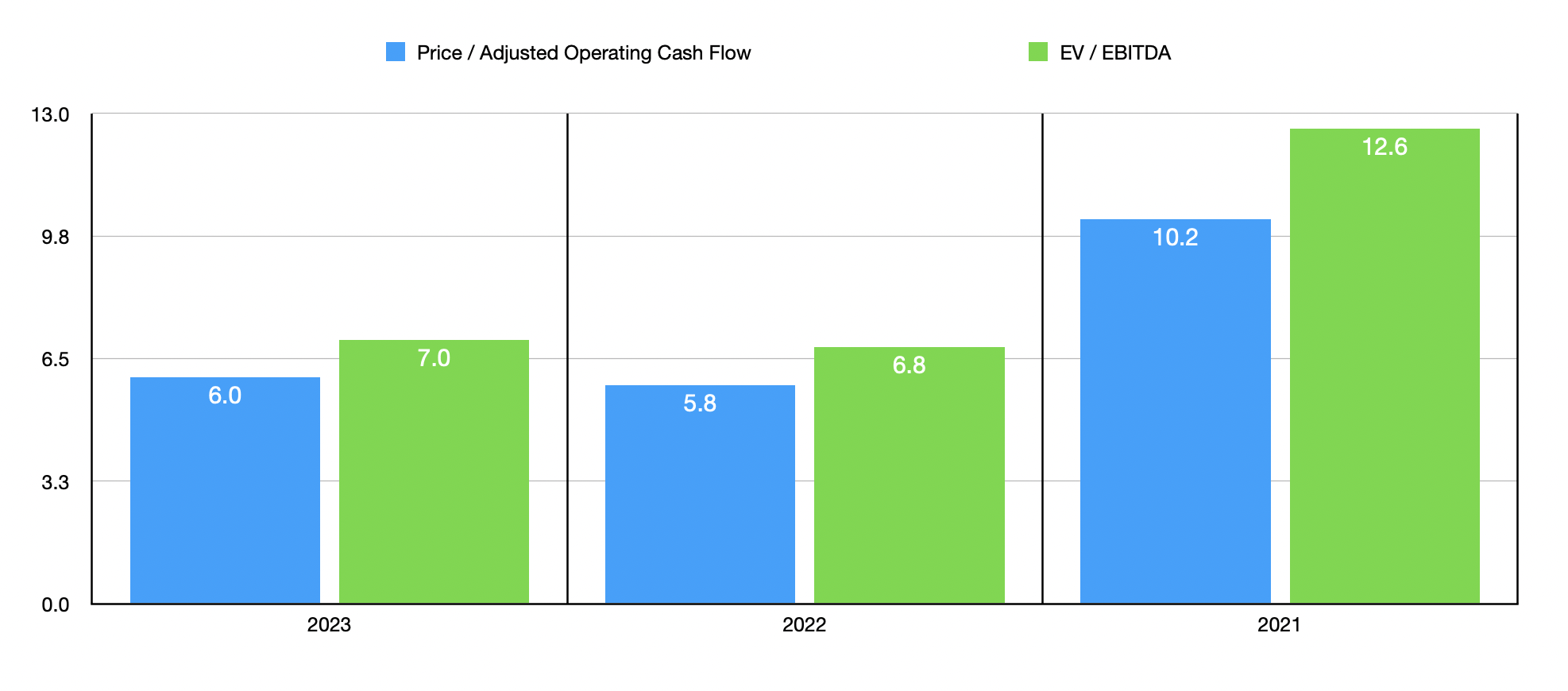

In the chart above, you can see how the company is priced using data from 2021 and 2022, as well as looking at assumptions for 2023. Even if financial performance were to revert back to what it was in 2021, the stock would still look reasonably affordable. As part of my analysis, I decided to compare the company to five similar businesses. On a price to operating cash flow basis, these firms traded at multiples ranging between 6.4 and 19.3. Meanwhile, using the EV to EBITDA approach, we get a range of between 7.5 and 11.4. In both of these cases, Griffon ended up being the cheapest of the group.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Griffon Corporation |

| 5.8 |

| 6.8 |

| Gibraltar Industries ( ROCK ) |

| 14.6 |

| 11.0 |

| Janus International Group ( JBI ) |

| 19.3 |

| 11.4 |

| PGT Innovations ( PGTI ) |

| 6.4 |

| 8.6 |

| Tecnoglass ( TGLS ) |

| 12.4 |

| 7.5 |

| Apogee Enterprises ( APOG ) |

| 14.0 |

| 8.3 |

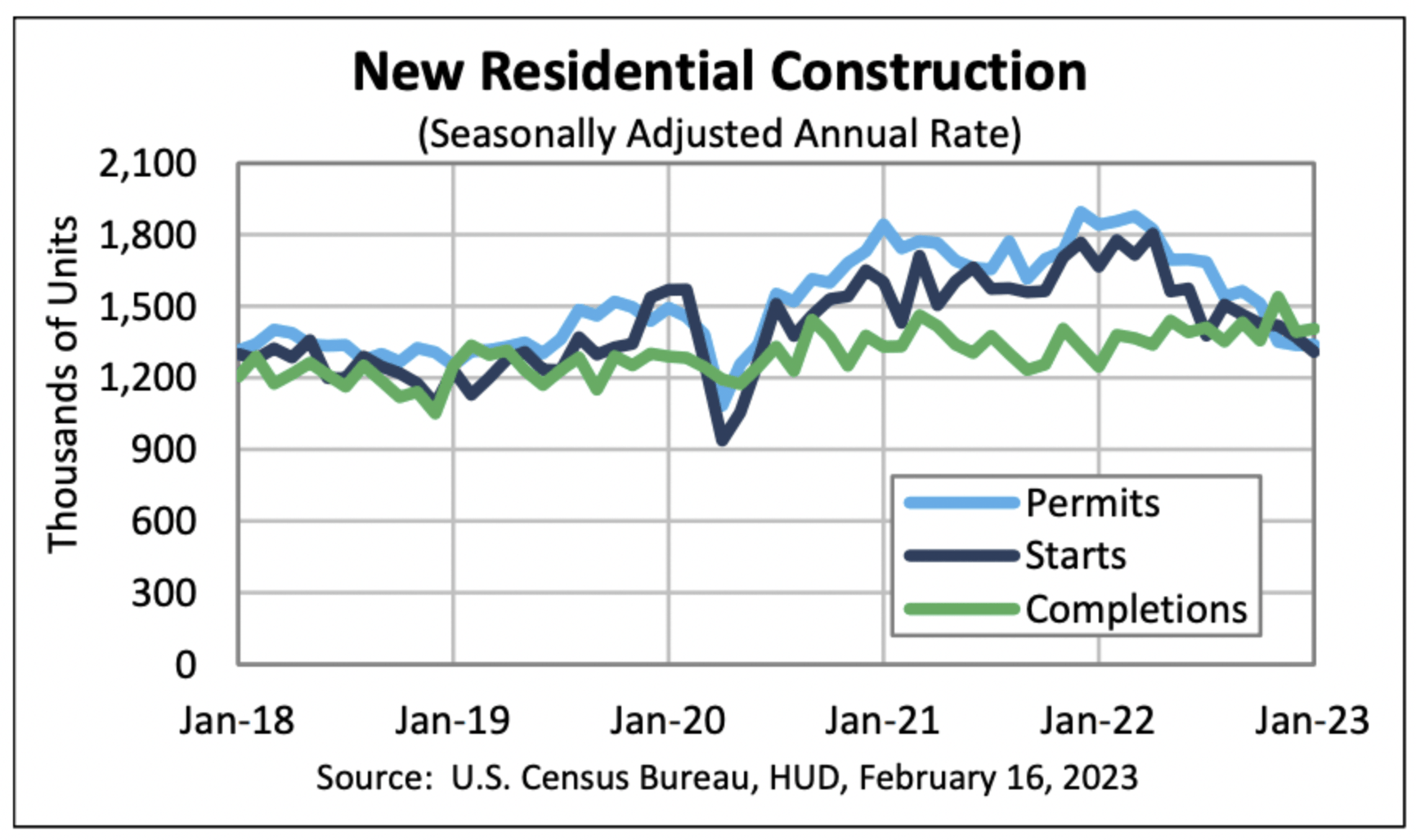

Past data is incredibly important in my assessment of a business. But if market conditions are slated to change materially, the past becomes less important. Right now, with high inflation and rising interest rates, there are plenty of concerns regarding what the future might hold. One easy thing to look at in this regard would be construction data. In theory, where construction goes should be where Griffon goes as well. When you look at new residential construction, I can understand that there might be some concerns. For the month of January, for instance, the number of permits provided for houses in the US totaled 1.34 million. That compares to the 1.84 million reported the same month one year earlier. Over the same window of time, the number of new residential housing starts declined from 1.67 million to 1.31 million. Simultaneously, the number of homes under construction actually rose year over year from 1.55 million to 1.70 million, while the number of homes completed grew from 1.25 million to 1.41 million.

{kind=link}

When you really process what this data is saying, it makes sense why the fundamental data of so many companies related to the home building space has been so robust. In essence, the large lag time between when a home is granted a permit and when a home is completed means that we are still seeing the benefits of a home construction boom. But, the leading indicators imply some meaningful weakness ahead. Why this does not concern me, however, is because, using data from 2022, new residential construction activities accounted for only 6.5% of Griffon's revenue. Admittedly, the retail space accounted for a much larger 16%. But the most significant exposure involved commercial construction at 22.1% of sales and residential repair and remodeling activities at a whopping 39.6%.

{kind=link}

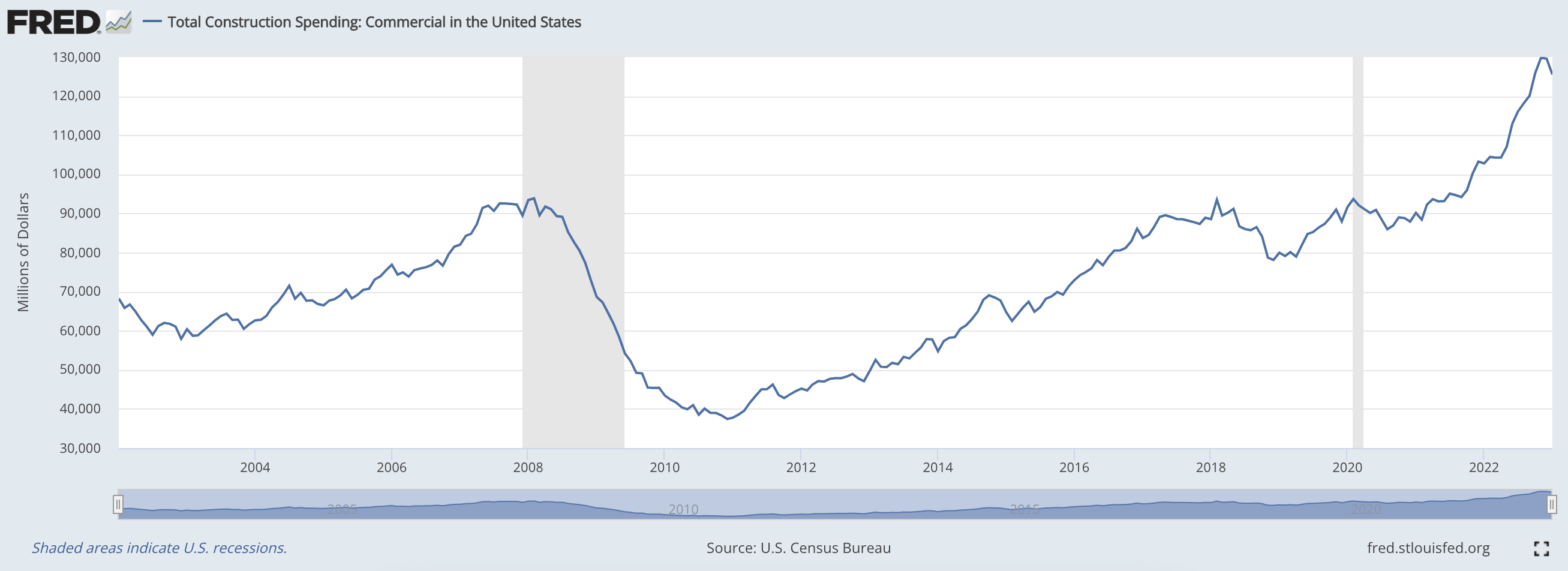

I could not find any reliable data when it comes to projecting out what construction spending might be in the foreseeable future. But the data that's available right now looks quite bullish still. Most likely driven by corporate profits that are at all-time highs (and likely because of inflationary pressures being thrown into the mix), construction spending in the US hit its highest on record in November 2022 by coming in at $129.82 billion. That's 29.5% higher than the $100.28 billion reported only one year earlier. When it comes to the even more vital residential repair and remodeling category, I have found some estimates of what the future might hold. According to Harvard University's Joint Center for Housing Studies, this space is expected to grow by 2.6% during 2023. This is down considerably from the 16.3% seen for 2022. But the gain will still allow the market to grow to $485 billion this year. And with 80.6% of the company's overall revenue coming from the US, what happens here will have a major impact, for better or worse, on the company's fortunes.

Takeaway

From what I can see, we may experience a pullback in some markets that Griffon benefits from. However, the market that it's most exposed to looks slated to continue growing, at least in the near term. The fact that management expects revenue to continue climbing during this time is also a vote of confidence in this forecast. Add on top of this how well the company has done and how cheap shares are, both on an absolute basis and relative to similar firms, and I do think the company offers some nice upside from here. When you add into all of this the fact that management continues to invest time, energy, and money into the strategic review process that the company initiated last year, a process that could result in a significant catalyst in the near term, I do believe that the company warrants not only the 'buy' rating I assigned it previously, but a 'strong buy' rating to reflect the likelihood of significant additional upside.

For further details see:

Griffon Corporation: Opening The Door To Higher Returns