GRIN - Grindrod Shipping: Favorable Outlook M&A Completion And Very Cheap

2024-01-14 03:48:00 ET

Summary

- Grindrod didn’t only continue to reduce its total amount of debt in the last quarter, management also reported the completion of the acquisition of Tamar Ship Management Limited.

- Favorable outlook for the geared dry bulk segment and expected market growth in the Asia Pacific region could lead to net sales growth.

- Stable balance sheet with negative working capital and recent debt reduction promises may positively impact future valuation multiples.

Editor's note: Seeking Alpha is proud to welcome Mitrai Stock Picks as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Grindrod Shipping Holdings ( GRIN ) recently delivered higher quarterly revenue than expected, and the recent acquisition news and fleet utilization increase imply business growth. Besides, taking into account favorable outlook for the geared dry bulk segment expressed in the last quarterly report and expected market growth in the Asia Pacific region, GRIN could deliver net sales growth in the coming years. Yes, there are risks from lower synergies than expected, lack of coverage, competition, or lower demand for dry bulk carriers. However, I believe that GRIN could trade at better price marks. I am bullish on GRIN stock.

Grindrod's Business

Grindrod owns, charters, and operates a fleet of dry bulk carriers along global shipping routes. Its vessels are located in subsidiaries that are also fully owned, and are of Japanese origin.

Its businesses focus mainly on the handysize cargo transportation segment, for which it reports conveyors. The company also reports the supramax/ultramax size cargo segment. Eventually, the company charters other vessels on a short-term basis to take advantage of specific commercial opportunities. Goods transported include minerals, coal, grains, forestry products, steel products, and fertilizers. The following table is from the most recent 6-k .

Source: 6-k Source: 6-k

The last quarterly report included lower EPS than expected. The EPS GAAP stood at close to -$0.44, with quarterly revenue close to $34 million. I believe that the recent earnings report and detrimental reports delivered in 2023 pushed the valuation of the company down. However, I believe that recent information about EPS revisions was beneficial. There was one upward EPS revision in the last 90 days, and expectations for 2025 seem beneficial.

Source: Seeking Alpha

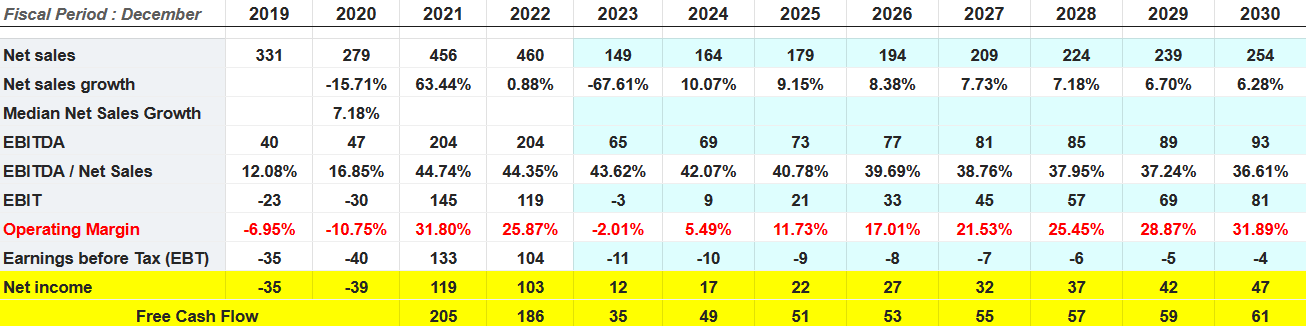

Market estimates include 2024 net sales of about $164 million, 2024 EBITDA of $69 million, EBITDA / Net sales of 42%, EBIT of $9 million, and net income of $17 million. Finally, free cash flow is expected to be close to $49 million. In sum, I believe that the figures are expected to be a bit better than that in 2023.

Source: S&P Global Ratings

Stable Balance Sheet With Negative Working Capital

With negative working capital, a significant amount of cash, and a small amount of accounts payables, Grindrod appears to use some long term debt to finance the ships. I believe that the recent decline in working capital is quite beneficial. It means that Grindrod does not need a lot of financing to operate.

Source: Ycharts

More in particular, as of September 30, 2023, Grindrod reports cash worth $71 million, trade receivables of about $4 million, and inventories of close to $11 million. Besides, total current assets stand at close to $107 million, implying a current ratio of more than 1x. I really do not see that Grindrod suffers from liquidity risks.

The largest asset is represented by ships, property, plant, and equipment, worth close to $330 million. Additionally, right-of-use assets are equal to $23 million, and the company also noted total assets of about $471 million.

Source: 6-k

The list of liabilities does not really seem worrying. Trade and other payables stand at close to $17 million, with contract liabilities of $3 million, bank loans and other borrowings of about $18 million, and total current liabilities of about $61 million.

Additionally, with bank loans and other borrowings close to $128 million and retirement benefit obligation close to $1 million, total non-current liabilities are close to $130 million. The asset/liability ratio is larger than 1x, so I would say that the balance sheet remains stable.

Source: 6-k

Given that the company reported some debt, I took a look at the interest rate paid. In the past, the weighted average interest rate was between 3% and 8.16%. With this in mind, I believe that cost of capital between 8% and 14% appears quite conservative.

The weighted average effective interest rate on our outstanding debt increased substantially from 3.82% in 2021 to 8.16% in 2022. The increase in the weighted average effective interest rate was primarily due to the increase in LIBOR as a consequence of the rising inflation.

For the years ended December 31, 2022, 2021 and 2020, we paid interest on our outstanding debt at a weighted average interest rate of 8.16%, 3.82% and 3.71%, respectively. A 0.5% increase or decrease in LIBOR would have increased or decreased our interest expense for the years ended December 31, 2022, 2021 and 2020, by $0.3 million, $0.5 million and $1.1 million, respectively. Source: 20-F

Forward Freight Arrangements Could Enhance FCF Visibility

In my view, optimization of the utilization of its dry bulk carriers to maximize charter revenue, while mitigating risk through a combination of charter, forward freight arrangements, and contracted shipping arrangements, could enhance future income and create visibility into cash flow. We are talking about a business model that was founded in 1910 . I think that Grindrod has accumulated a significant amount of know-how in the industry, which will most likely help management reach agreements with partners and clients.

In addition to its extensive reputation in the industry, the company appears to have a central presence and main offices in Africa and Asia, where it maintains strong commercial relationships with critical end users in key geographic regions for the growth of dry bulk cargo demand. The global dry bulk shipping market is expected to grow at close to 4% CAGR from now to the year 2030. However, market experts believe that the Asia Pacific region, where Grindrod runs some operations, is one of the world's fastest expanding markets. I believe that Grindrod’s net sales could benefit from the growth in the market.

Dry Bulk Shipping Market is Anticipated to Grow at a CAGR of 4% by 2030. One of the world's fastest expanding markets for dry bulk shipping is the Asia Pacific region. Source: Report by Market Research Future

Fleet Utilization Increased

In the last nine months ended September 30, 2023, the company sold a few vessels, which may explain the recent decrease in the total amount of assets and ships, property, plant, and equipment.

Revenue decreased due to weakening market conditions in the drybulk business, partially offset with the sale of three handysize and four supramax/ultramax vessels compared to the sale of a medium range tanker in the first half of 2022 (included in the Other segment under a bareboat charter). Source: 6-k

It is also worth noting that the company appears to sell underperforming ships. In the last report, fleet utilization increased. In my view, if the company continues to increase its fleet utilization, I would expect an increase in the FCF margin and EBITDA margin growth.

Source: 6-k

Debt Reduction Promised May Enhance EV/EBITDA Multiples

I believe that the recent decrease in the total amount of debt and promises about future debt decreases are remarkable. With a favorable outlook for the geared dry bulk segment and further declines in leverage, I believe that the EV/FCF and EV/EBITDA ratio may increase. In this regard, I believe that the following lines from the last quarterly report are worth taking a look at.

In total, we have now paid $36.1 million of bank debt since the start of the year, equating to a reduction in interest payments of $1.9 million on an annualised basis. Overall, we maintain a favourable outlook for the geared dry bulk segment and we remain committed to continuing to reduce debt and improving our position to deliver long-term value to shareholders. Source: 6-k

Source: Ycharts

Synergies May Appear In The Coming Years

In my view, the M&A deal reached in 2023 with Tamar Ship Management Limited and Taylor Maritime Management Limited clearly indicates that Grindrod is trying to grow again.

On October 3, 2023, we announced that the completion conditions included in the two sale and purchase agreements for the acquisition of the entire issued share capital of Tamar Ship Management Limited and Taylor Maritime Management Limited had been met. The acquisition became legally effective on October 3, 2023. Source: 6-k

In my view, successful integration of employees and potential synergies may appear in the coming years. As a result, we may see certain improvements in the FCF margins and EBITDA margin growth.

Started the integration of the management teams which we expect to unlock further commercial synergies and technical savings. Source: 6-k

My Financial Model

My expectations include 2030 net sales of close to $254 million, net sales growth of 6%, 2030 EBITDA of $93 million, 2030 net income of about $47 million, and 2030 FCF of $61 million. I believe that my figures are conservative.

{kind=link}

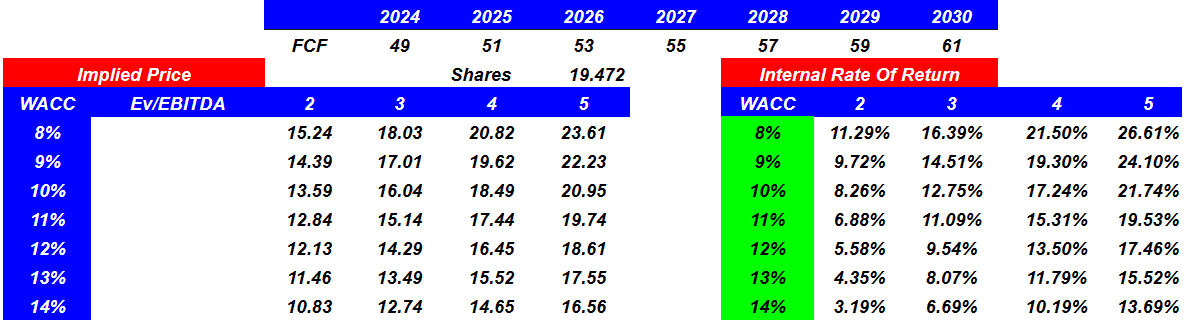

If we assume an exit multiple of EV/EBITDA between 2x and 5x and WACC of 8%-14%, the implied fair price would be close to $10-$23, with a median stock price of close to $13-$17. Besides, the internal return obtained would be close to 3%-26%, but the median IRR obtained is close to 9%-17%. I believe that the exit multiple is close to the multiple at which other peers trade. Sector median EV/EBITDA stands at close to 11x-12x.

{kind=link}

Competition And Risks

The company's vessels operate in a highly competitive market that is capital intensive and highly fragmented. Competition in the market is primarily based on supply and demand, with competition for charters and shipping arrangements contracted based on price and vessel specifications, including fuel consumption, size, and age. The main competitors are other independent companies and state-owned bulk carrier owners, some of which may count with more resources than Grindrod.

The company may be affected by the ups and downs of the regional economies of the Southeast Asian area, and more specifically by the ups and downs of the Chinese economy. It may also be negatively affected by the imposition of trade barriers between the United States and China.

I believe that the new M&A agreements signed in 2023 could fail. Management may have paid more than what Tamar Ship Management Limited and Taylor Maritime Management Limited are worth. If Grindrod reports goodwill impairments, or the value of vessels is downgraded, a decrease in the book value per share could lead to stock price declines.

Right now, I believe that there is a disconnection between the fair valuation of the company and the stock price. The fact that not many analysts are covering the stock could explain why the stock is that cheap. In the future, without new analysts covering the stock, I believe that the EV/EBITDA and EV/FCF ratio may not reach higher marks.

My Conclusion

Grindrod didn’t only continue to reduce its total amount of debt in the last quarter, management also reported the completion of the acquisition of Tamar Ship Management Limited and Taylor Maritime Management Limited. With a recent increase in the fleet utilization and a favorable outlook for the geared dry bulk segment, I believe that there are sufficient reasons to follow the stock carefully. There are some risks from competition, lack of coverage, or lower than expected synergies, but, in my view, the stock is quite cheap.

For further details see:

Grindrod Shipping: Favorable Outlook, M&A Completion, And Very Cheap