GRIN - Grindrod Shipping Holdings: Higher TCE Rates But Not Much

2023-03-22 01:27:33 ET

Summary

- Grindrod reported a 4Q 2022 loss of $0.24 per diluted share, compared with a 4Q 2021 profit of $2.67 per diluted share. The company’s annual profit decreased by 11% YoY.

- As TCE rates for handysize and supramax/ultramax vessels dropped in 2022, Grindrod’s net cash flows generated from operating activities slashed.

- The company’s liquidity condition in terms of cash and current ratios weakened and reached 0.58 and 1.16 in 4Q 2022, respectively.

- However, the TCE rates increased in the past month and GRIN’s financial position is expected to improve in the second quarter of the year.

- GRIN stock is a hold.

In the past six months, Grindrod Shipping Holdings ( GRIN ) stock price halved as TCE rates dropped and the company's financial results impaired. The dry bulk shipping market was weaker than I expected a few months ago. GRIN's 1Q 2023 TCE revenues are not going to be high. However, as the stock's price has already slashed, the company's 1Q 2023 financial results may not cause the stock price to decrease further. On the other hand, in the past month, TCE rates for handysize and supramax/ultramax vessels partially recovered. I don't expect TCE rates for handysize and supramax/ultramax vessels to increase significantly in the following months. However, they are high enough to make the company's 2Q 2023 results to be better than in 1Q 2023. Based on the current market outlook, a hold rating is suitable for the stock.

Quarterly results

In its 4Q 2022 financial results, Grindrod reported total revenue of $51 million, compared with $142 million in the same period last year. The company's gross profit dropped from $67 million in 4Q 2021 to $23 million in the fourth quarter of 2022. GRIN's profit from the operating operations of $23 million in the fourth quarter of 2021, turned into a loss of $5 million in the fourth quarter of 2022. Also, the company reported a full-year 2022 profit of $103 million, compared with $133 million in the full-year 2021. GRIN reported 4Q 2022 handysize segment revenue and gross profit of $27 million and $5 million, respectively, compared with 4Q 2021 revenue and gross profit of $51 million and $29 million, respectively. The company's supramax/ultramax segment revenue dropped from $91 million in 4Q 2021 to $54 million in 4Q 2022. Also, its supramax/ultramax segment gross profit slashed from $36 million in 4Q 2021 to $17 million in 4Q 2022. Grindrod's current assets dropped in 2022 as its cash and bank balances more than halved to $52 million from 31 December 2021 to 31 December 2022.

The company's net cash flows used in financing activities increased from $139 million in 2021 to $243 million in 2022, driven by hiked dividends paid and higher principal repayments on lease liabilities. However, the company's forward dividend yield of 1% is much higher than its TTM dividend yield of 11%. "As a result of the weaker markets and the special dividend already paid in fourth quarter, the Board elected to declare a base quarterly dividend of $0.03 per share for the fourth quarter," the CEO commented. "As we look forward, the Company will be prioritizing net debt reduction and liquidity flexibility, particularly as the seasonally weaker first quarter has not rebounded materially after the conclusion of the Lunar New Year holidays in Asia. As already recently disclosed, we have committed to reduce our leverage, which may include further ship sales," he continued. It is worth noting that on 16 December 2022, GRIN entered into a contract to sell one of its ultramax vessels for $23.75 million (before costs) to be delivered on 31 March 2023.

The market outlook

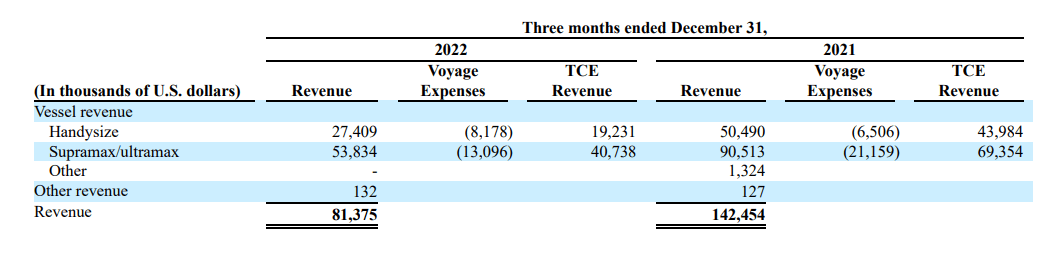

According to Figure 1, in the fourth quarter of the last two years, the handysize segment's revenue accounted for about 35% of GRIN's total revenue, and the supramax/ultramax segment's revenue accounted for 65% of its total revenue. The company's handysize TCE per day decreased from $28842 in 4Q 2021 to $14427 in 4Q 2022. GRIN's handysize segment's operating days decreased by 12.6% in 4Q 2022 to 1333, as its short-term charter-in days decreased from 206 to 23. Also, its TCE per day decreased from $30089 per day in 4Q 2021 to $21739 in 4Q 2022. The company's supramax/ultramax segment's operating days decreased by 18.7% to 1874 in 4Q 2022, as its long-term charter-in days and short-term charter-in days decreased by 87 and 445 days, respectively.

As of 10 February 2023, GRIN had contracted 1035 operating days of its handysize vessels at an average TCE per day of $9888. Also, the company had contracted 1127 operating days of its supramax/ultramax vessels at an average TCE per day of $11897. As of 10 February 2023, GRIN's average long-term charter-in costs per day for supramax/ultramax fleet for 1Q 2023 was expected to be $14593 per day. Thus, the company's 1Q 2023 revenues are expected to be lower than in 4Q 2022. What about 2Q 2023?

Figure 1 - GRIN's revenue

{kind=link}

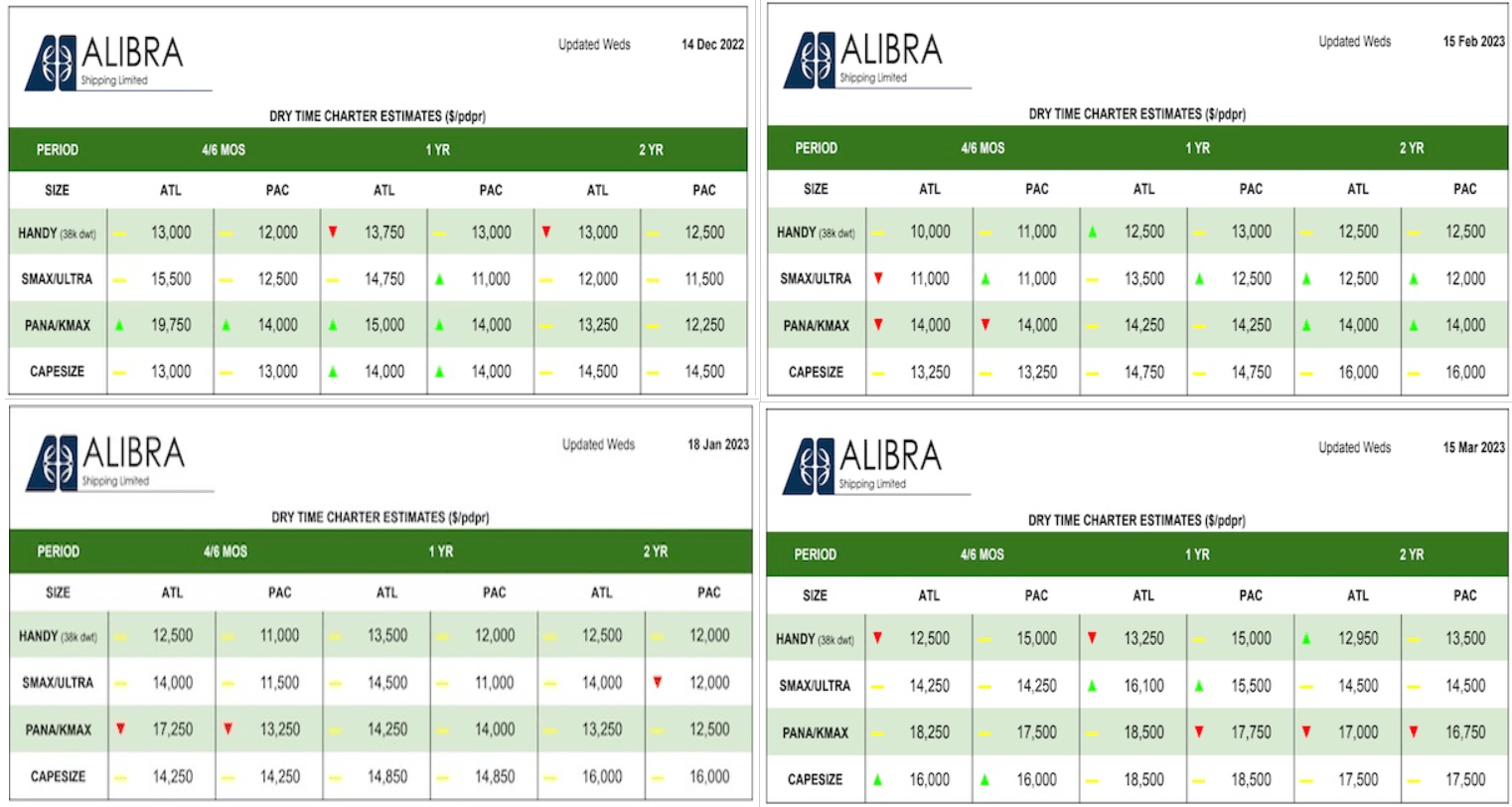

In February 2023, the Baltic Dry Index dropped to below the 1-year trend line and bounced back in March, reaching the 1-year mean. Figure 2 shows that dry time charter estimates (1 year) for handysize vessels dropped from 15 December to 15 February However, in the past month, the TCE rates for handysize vessels partially recovered. Also, dry time charter estimates (1 year) for ultramax/supramax vessels increased by 30% in the past month. As of 15 March 2023, the average TCE rate (1-year) for ultramax/supramax vessels was $14250, compared with $15500 on 14 December 2022, $14000 on 18 January 2023, and $11000 on 15 February 2023.

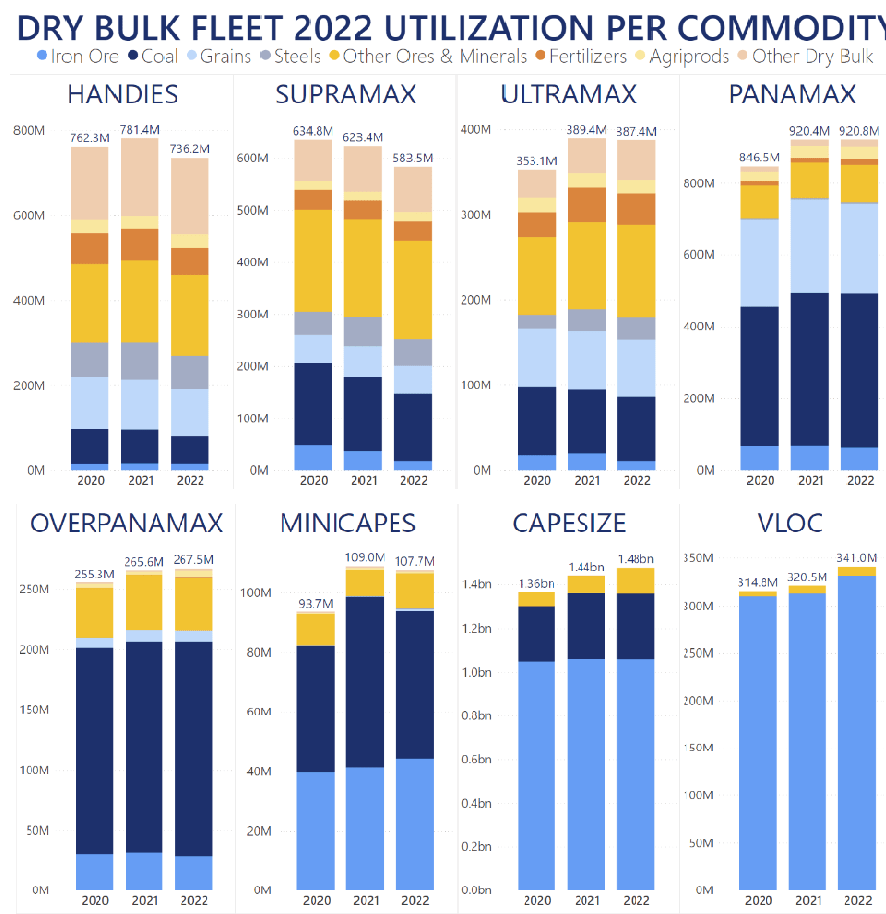

China's economic recovery can increase the demand for dry bulk commodities, especially iron ore, as construction in China is expected to improve in the following quarters. However, it is important to know that more demand for iron ore affects the TCE rates for capsize vessels more than other types of dry bulk vessels, and Grindrod does not have any capsize vessel. According to Figure 3 , handysize and supramax/ultramax vessels are not normally used to carry iron ore and coal. They are normally used to carry grains, steel, ores & minerals excluding coal and iron ore, fertilizers, and other minor dry bulk commodities. Thus, the increasing demand for iron ore cannot increase GRIN's TCE revenues significantly and directly. Due to the global economic headwinds and the sparked fear of financial crises, the market outlook for minor dry bulk commodities is not expected to improve considerably in the next few months. Thus, I don't expect the TCE rates for handysize and supramax/ultramax vessels in the second quarter of 2022 to increase further. However, with the current TCE rates that are higher than a few months ago, GRIN's financial results in 2Q 2023 can be better than in 1Q 2023.

Figure 2 - Dry time charter estimates

{kind=link}

Figure 3 - Dry bulk fleet utilization per commodity

{kind=link}

GRIN performance

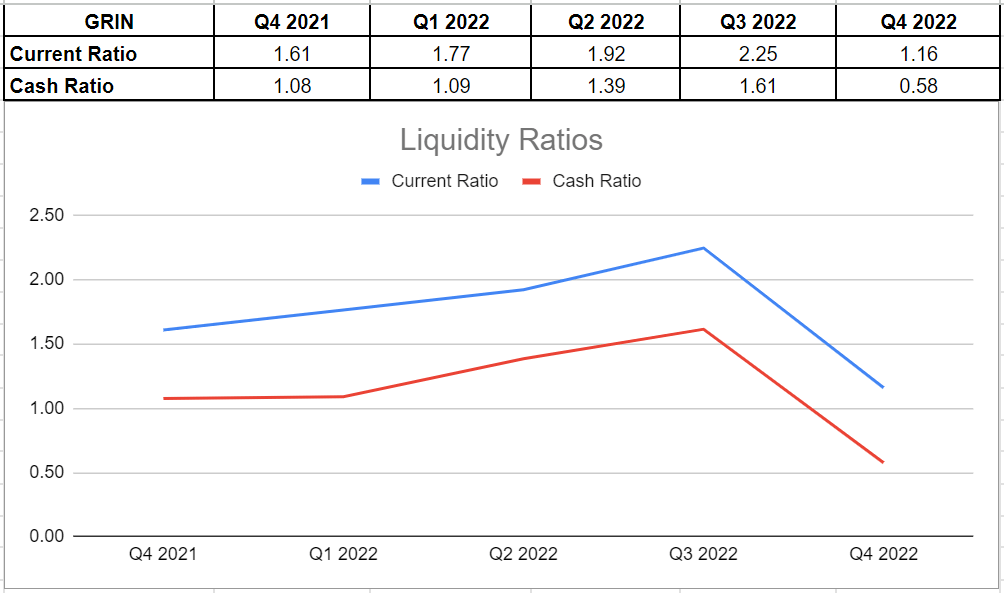

In this thorough section, I analyzed Grindrod Shipping's performance outlook across the board of liquidity and leverage ratios. Liquidity ratios are worthy for indicating a good picture of the company's capability to keep its balance between the ability to safely cover its obligations and improper capital allocations. In this regard, I investigated GRIN's current and cash ratios to more accurately compare with previous quarters.

As the liquidity ratios have assets on top and liabilities on the bottom, it is paramount to consider the ratios if their amount is above 1.0 to analyze if the company is able to face its obligations. GRIN did not end 2022 with an appealing financial condition. In other words, its current ratio dropped by 48% to 1.16 in 4Q 2022 from 2.25 in 3Q 2022. Also, it is 28% lower year over year compared to the current ratio of 1.61 at the same time in 2021. Similarly, the company's cash ratio dropped deeply by 63% to 0.58 in the fourth quarter of 2022 versus its previous level of 1.61 in 3Q 2022 due to a 64% plunge in the company's cash balance. This record indicates that about 58% of the company's liabilities can be paid off directly by its cash and cash equivalents (see Figure 4).

Figure 4 - GRIN's liquidity ratios

{kind=link}

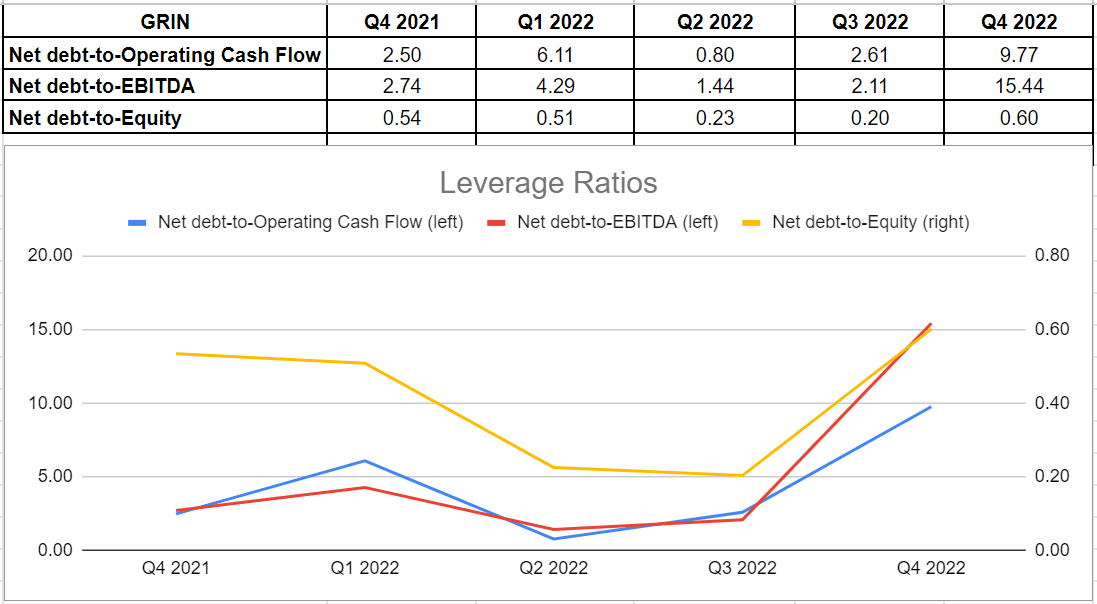

Furthermore, I analyzed how GRIN's assets and business operations are financed by investigating its leverage ratios. As Figure 5 indicates, all mentioned ratios had much higher levels compared with their prior quarters. Grindrod Shipping's net debt level increased considerably from $79.6 million in 3Q 2022 to $172.9 million in 4Q 2022. Also, its cash operation dropped by 42% to $18 million in 4Q 2022 versus its previous quarter. Thus, a combination of an increase in net debt and a decline in the operating cash led to a massive increase in the company's net debt-to-CFO of 9.77 in 4Q 2022 from 2.61 in 3Q 2022. Moreover, GRIN's EBITDA amount, which works as a good proxy for the cash generation capacity of the company, plunged by 71% in the fourth quarter of 2022 versus the previous one, and thus led to the highest-ever amount of net debt-to-EBITDA of 15.44 in 4Q 2022 from 2.11 in 3Q 2022.

Ultimately, the net debt-to-equity ratio or risk ratio indicates how the company's capital structure is titled, whether toward debt or equity financing. GRIN's risk ratio was 0.6 in 4Q 2022, while it was 11% higher year over year compared with its level of 0.54 in 3Q 2021 and far higher than 0.2 in 3Q 2022. As a result, Grindrod Shipping's leverage condition depicts its risky position to face upcoming risks.

Figure 5 - GRIN's leverage ratios

{kind=link}

Summary

When all was said and done, Grindrod Shipping's liquidity and leverage conditions indicate how lockdowns in China, global economic slowdowns, and the higher interest rates to combat them led to lower demand for dry bulk shipping and thus weakened the company's financial structures. GRIN's 1Q 2023 financial results are not expected to be strong. However, TCE rates for GRIN's fleet increased in the past month and thus, I expect the company's financial position to improve in the second quarter of 2022. The stock is a hold.

For further details see:

Grindrod Shipping Holdings: Higher TCE Rates, But Not Much