GSL - Grindrod Shipping: Why Have Good When You Can Have Great

Summary

- Grindrod Shipping's business has remained highly profitable, and management is looking to pay out 30% of net income as dividends.

- A recent offer at a 17% premium has not been accepted, as investors see value greater than its current trading price.

- Our economic analysis suggests charter rates will fall further in 2023 as a result of a decline in demand, with supply remaining fairly fixed.

- Unfortunately, we see nothing to suggest GRIN stands out from the pack, boasting inferior profitability and scale.

Company Description

Grindrod Shipping Holdings Ltd. ( GRIN ) is an international shipping company that owns, charters, and operates a fleet of 31 dry bulk vessels . These include 15 handysize bulk carriers, 10 Supramax/Ultramax carriers, and 6 Supramax/Ultramax chartered-in.

The company is based in Singapore, with South African routes. Its Primary listing is on the NASDAQ, with a secondary on the JSE.

Dry bulk commodities are raw materials which are shipped globally for manufacturing and production, such commodities include grain and metals.

GRIN has had an eventful few years with serious volatility in its share price. The boom post 2021 is a reflection of the COVID-19 backlog, where companies struggled to meet enormous demand in the West as their supply chains staggered to come back online following lockdowns. Charter rates grew quickly, and shipping companies were rewarded handsomely.

The inevitable hangover arrived, with much of 2022 seeing corrections across the board. Charter rates fell and stabilized from unsustainable highs, but with inflation now at the forefront, shipping will play its part in economic developments in 2023.

We have previously covered both GSL ( linked ) and EGLE ( linked ) that are both up since said publication. In this case, the objective remains the same, we are looking for a business with high-quality assets, strong charter rates and contract durations, a bulletproof balance sheet and a management team which is invested in the sustainable performance of the company.

Shipping Industry and Dry Bulk

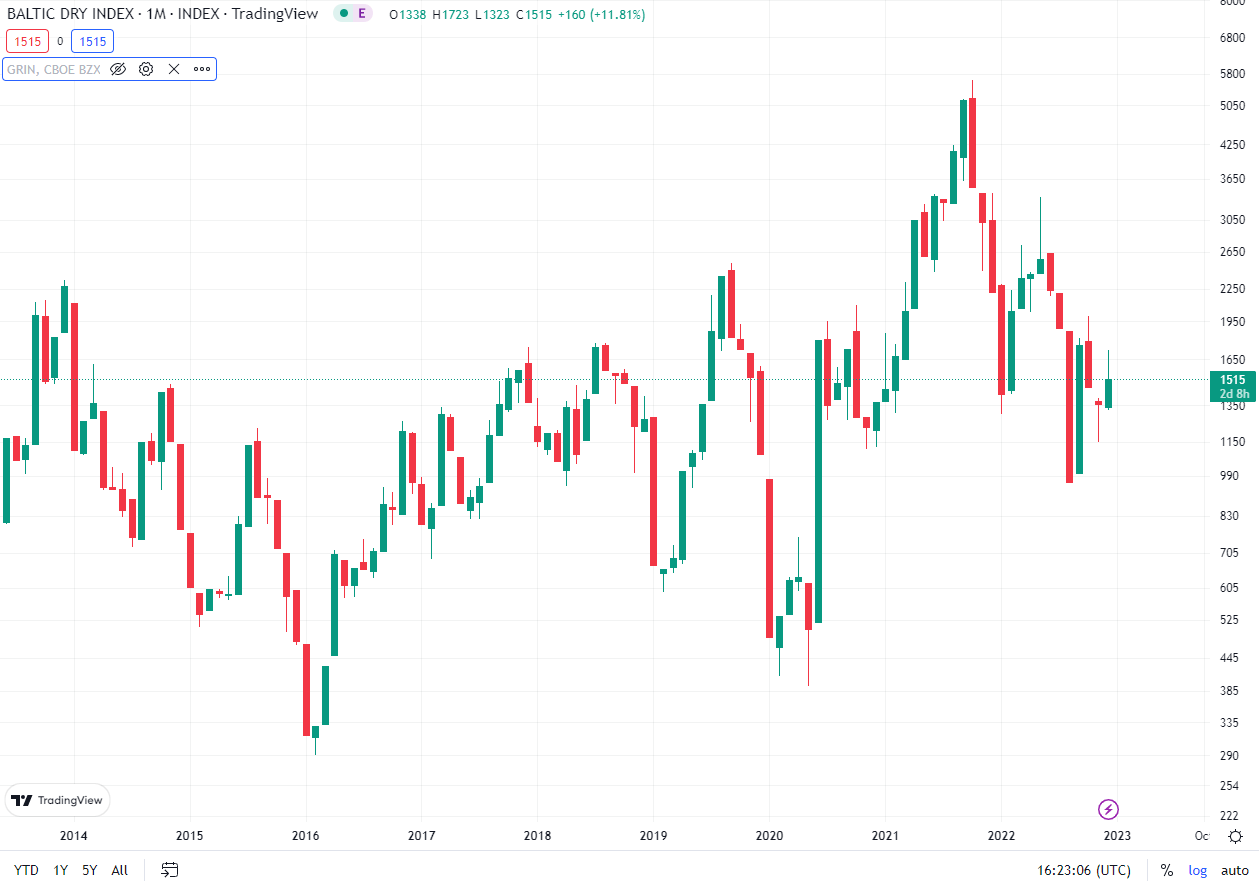

Charter rates are tracked by the Baltic Dry index, which was created by the London Baltic Exchange.

{kind=link}

What we see is a sharp reversal from those levels observed in 2021, but no more volatility than seen in years gone by. Much of the strength in the price levels is likely as a result of inflationary pressures, with charter rates remaining strong to reflect the cost to the businesses themselves. This said, it is undeniable we are positioned for a downward trend.

Trading Economics had the following to say :

"The Baltic Dry Index, which measures the cost of shipping goods worldwide, slumped 8.2% to an over one-week low of 1,515 points on Friday, the second day of losses. The capesize index, which tracks iron ore and coal cargos of 150,000 tonnes, tumbled 13.9% to mark its worst day since late August at 2,261 points; and the panamax index, which tracks about 60,000 to 70,000 tonnes of coal and grains cargoes, fell 1.8% to 1,535 points. At the same time, the supramax index shed 21 points to 1,062 points. The main index plunged 13.9% this quarter and 31.7% for the year, the most since 2015".

The reason for this is twofold. Firstly, things in China are getting complicated. The Chinese government has been hell-bent on its Zero-COVID policy. The problem with this is that it is bound to fail in a country with >1bn people and currently as infection rates reach record levels . This is seriously impacting production lines and domestic demand in China, which is having a knock-on effect on related industries such as Shipping. Further, things in China have been on shaky grounds for a while, with COVID arguably knocking China's fragile economy over. Growth has been slowing and said growth has been of questionable quality, with hundreds of Ghost towns built for nothing more than to drive growth for growth's sake . But with Xi's common prosperity speech and policy changes, China may no longer continue as it has. So, what does this have to do with Shipping? Well if China decides it is not going to build unnecessary buildings anymore, or rely so heavily on Australian raw materials, this will impact the global demand for commodities shipping.

Secondly, the West is in the grips of a Cost of Living crisis . Inflation is out of control and the only weapon that can be used against it, interest rates, is used with extreme caution due to the debt-laden reality of these countries. This is further harming society as they have greater interest costs alongside more expensive goods. This can only go on so long before demand declines substantially. We are already seeing European countries slowing to a standstill , with the US inevitably soon behind. If we use 2008/09 and early 2020 as an indicator of where things could go, the BDI index fell to ~650 in 08/09 and ~420 in 2020. At those levels, most if not all profits will be gone.

Financials

For the 9 months ended Sept. 22, GRIN posted revenue of $379.1M, EBITDA of $171.9M, and net income of $110.4M. This compared to $131.5M for the Sept. 21 period. The growth can be observed when we look at TCE per day, which is up to $24,396/$27,015 (Handysize/Supramax) from $18,847/$21,514. Much of this greater TCE is derived from the greater daily rates, as opposed to any cost savings made.

Further, management notes that the orderbook remains low, which was an observation we noted in our previous Shipping papers. Given the time it takes to build a dry bulk carrier, we may not see an impactful increase in ships till 2024/2025. This is beneficial as if things were to slow down, supply-side shifts would significantly compound GRIN's problems. Notably, GRIN's ships have outperformed their larger counterparts, which is not unheard of in uncertain times due to their flexibility and logistical cost superiority.

Problems are found when we consider forward-looking data; however, management state that they are contracted for a TCE per day of $15,688/$22,850 in Q4 2022, which is a noticeable reduction from Q3. Management has referred to charter rates as having "persistently declined over the course of the quarter". Evidence suggests this has only continued since then.

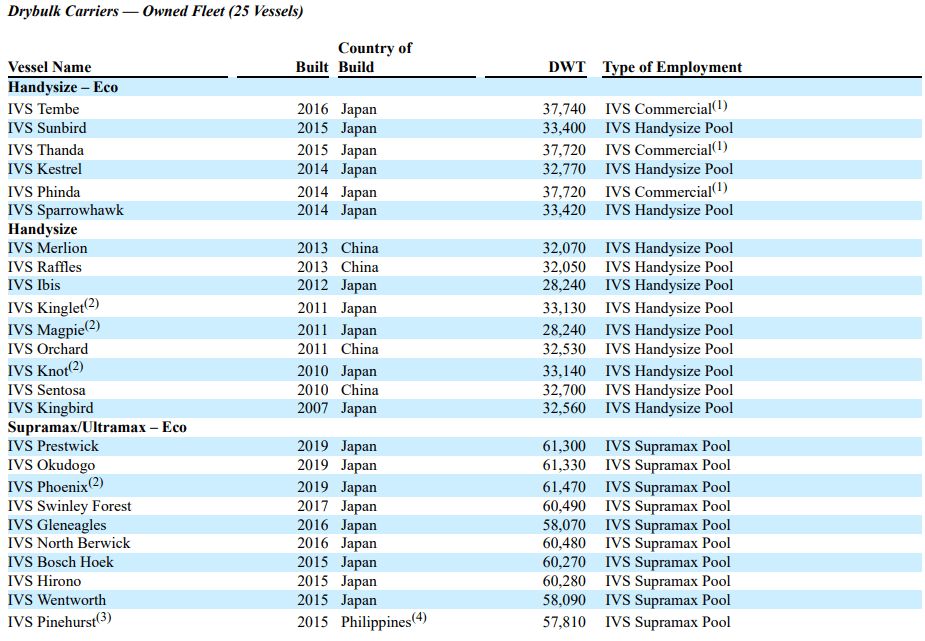

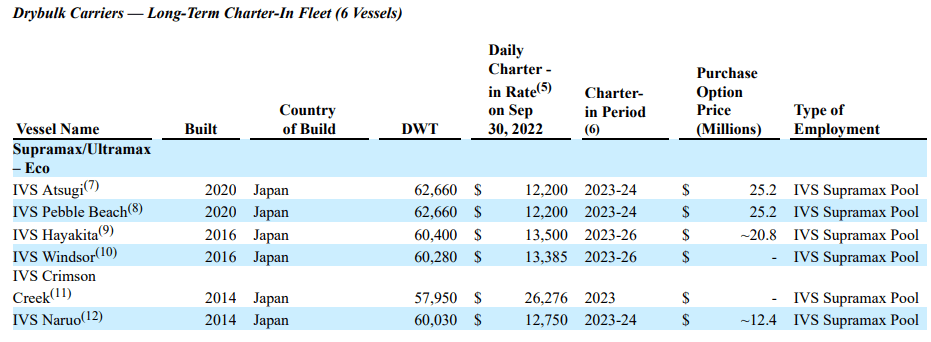

During the quarter, a single 2015-built carrier was purchased, with the extension of multiple charter-in carriers. These were at rates in excess of those previous. GRIN's fleet is of good quality, with the majority of ships built post 2014 and being Japanese Eco Vessels. This said, we should acknowledge that much of the aged fleet is in the Handysize category, this is GRIN's most profitable segment and so greater capex could impact margins going forward.

GRIN's fleet (1/2) (GRIN Q3 investor pack) GRIN's fleet (2/2) (GRIN Q3 investor pack)

{kind=link}

{kind=link}

GRIN has been able to maintain respectable utilization levels, with Handysize falling to 97.2% from 97.8% between the 3 months Sept. 21 and Sept. 22. Supramax has actually increased to 98.4% from 97.4%.

On the balance sheet side, we observe a successful deleveraging process. Total debt has fallen from $330M in 2020 to $226M as of Sept. 22. That said, the levels remain high but are far more manageable. Further, large debt balances are commonplace in the shipping industry due to the cost of ship ownership. GRIN's EBIT/interest expense ratio is 11x, which is very comfortable. No notable loans are due to mature.

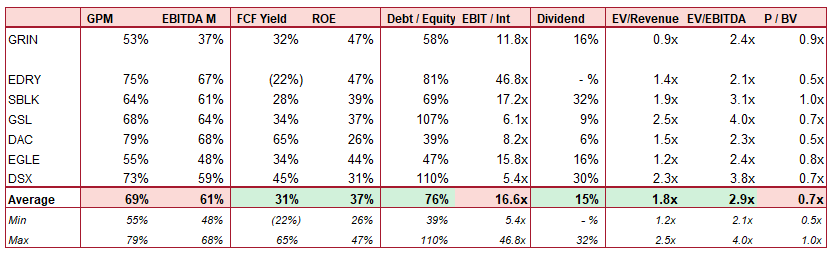

Peer comparison

In order to adequately assess GRIN as a business, we must compare it to similar investment opportunities using appropriate metrics.

Peer group analysis (TIKR Terminal)

{kind=link}

What we have identified is that GRIN is very much a "member of the pack". It is not terrible in any metric, just outperformed. Although GRIN is the worst performer from a profitability standpoint, it boasts a respectable FCF yield, which should not go unnoticed. Further, the prudent financing of the business means the return on equity is best in class. This said, both DAC and EGLE are more profitable with less debt.

So, what is the draw? Well, GRIN is cheaper than the peer group as a whole, and so is an opportunity for investors to get cheaper exposure. This is where value can be found for investors.

Valuation

Valuing shipping businesses, especially in times like this, is no easy feat. Charter rates remain volatile, and in many cases, it is very difficult to find a "base-line" on which to compare current trading. GRIN, for example, was loss-making up until 2021.

What we find quite compelling is management's decision to pay out 30% of net income as dividends. With their current cash position and deleveraging efforts, this is certainly sustainable. At current levels, this represents a dividend yield in excess of 10%, even if profits were to dip.

Other matters for consideration

Steel demand

Although we have highlighted the risks around China already, it would be prudent to touch on the demand for Steel/Iron Ore. This represents one of the most shipped commodities globally and China is a major player. Currently, a large number of Chinese producers are struggling, with many fearing bankruptcy. This will have a ripple effect across the market and impact demand for iron ore.

Taylor Maritime Investment Ltd

16% of GRIN is owned by TMI, which made an offer to purchase GRIN at $21-a-share. This offer expired on the 19th December 2022 . Investors should consider the impact of TMI's interest going forward and their intentions for their 16% should another offer not be forthcoming.

Conclusion

GRIN is a great business which has done well to capitalize on the recent spike in charter rates post-COVID-19. It has deleveraged and invested into a young fleet of ships. This said, times are not what they were 1 year ago and investors will need to be pickier when it comes to Shipping stocks. Alpha can still be generated, but GRIN is not ahead of the pack. Although it is trading at a discount, this is not attractive enough to justify the investment. Dividends are good and so this is an attractive hold, but a new investor may be better placed looking at great stocks such as EGLE or GSL.

For further details see:

Grindrod Shipping: Why Have Good, When You Can Have Great