GRTS - Gritstone bio: Keep An Eye On This Discounted Cancer Vaccine Developer In 2023

Summary

- Gritstone stock has tanked since the company's IPO but 2023 could be the year this biotech delivers.

- A personalised cancer vaccine specialist at heart, Gritstone's pivot into developing a COVID vaccine may have been an unwelcome distraction.

- Two PCV assets have made it into Phase 2 studies and results have been encouraging, if not conclusive.

- The GRANITE program may deliver Phase 2/3 data in 2023 that could be good enough to secure accelerated approval.

- That scenario would definitely send the share price skyrocketing. The next 12 months will be an exciting period for the company.

Investment Overview

Gritstone bio ( GRTS ) IPO'd in September 2018, raising ~$100m via the issuance of ~6.7m shares at a price of $15 per share.

The company was founded in 2015 by Andrew Allen - co-founder and former chief medical officer ("CMO") at Clovis Oncology, the now defunct (its shares were delisted from the Nasdaq this month) developer of Rubraca, a poly-ADP ribose polymerase ("PARP") inhibitor indicated for late line Ovarian and Prostate cancer treatment.

Given that he left Clovis in 2015, Allen cannot be blamed for Clovis' bankruptcy, and in setting up Gritstone the President and CEO is now focused on a field of oncological research that is beginning to attract a lot of attention - namely the use of tumor-specific neoantigens, and viral antigens, to try to generate a therapeutic immune response in patients.

Often referred to as Personalised Cancer Vaccines ("PCVs") in the oncology setting, these types of therapies are designed to work alongside existing cancer drugs - usually immune checkpoint inhibitors ("ICIs") targeting the programmed cell death protein ("PD1"), or programmed death ligand ("PDL1") - to enhance the immune response they generate.

After an initial surge to a price of $28, Gritstone shares had fallen in value to ~$2.5 per share by November 2021 - a not untypical decline for a recently IPO'd biotech - before skyrocketing briefly to >$25 after the company's pivot into designing a COVID vaccine, leveraging a self-amplifying mRNA approach produced some strong preclinical data , generating "potent neutralizing antibody titers in rhesus macaques at all dose levels".

Although Gritstone secured additional support from both the National Institutes of Health ("NIH") and the Coalition for Epidemic Preparedness Innovations ("CEPI") to fund further development of its vaccine, and there were some positive Phase 1 data shared by management in late October showing a "broad and durable immune response; high neutralizing antibody and T cell responses at 6 months post-boost vaccination" - the company has its work cut out if it is going to produce a COVID vaccine which can compete against the likes of Moderna ( MRNA ) and Pfizer ( PFE ) / BioNTech's ( BNTX ) all-conquering vaccines in the much smaller private COVID vaccination market that is expected to emerge in 2023 and beyond.

The market generally seems to have been viewing Gritstone through the prism of its COVID vaccine and as the pandemic has subsided, Gritstone stock has slipped to a low of $3.3 at the time of writing, which values the company at just $277m.

A return to its dual BAU neoantigen development programs GRANITE and SLATE - which have entered Phase 2/3 studies, and Phase 1/2 studies in patients with Microsatellite-stable colorectal cancer ("MSS-CRC"), and patients with KRAS-mutated solid tumors - primarily MSS-CRC and non small cell lung cancer ("NSCLC") - respectively, could be the ideal tonic for Granite's share price in 2023.

A few weeks ago, Moderna and Pharma giant Merck & Co ( MRK ), who market and sell the best-selling ICI cancer drug Keytruda, announced some promising results from their Phase 2, Open Label KEYNOTE study of Moderna's PCV candidate MRNA-4157 plus Keytruda in patients with melanoma, which:

demonstrated a statistically significant and clinically meaningful improvement in the primary endpoint of recurrence-free survival (RFS) versus KEYTRUDA alone for the adjuvant treatment of patients with stage III/IV melanoma following complete resection.

Adjuvant treatment with mRNA-4157/V940 in combination with KEYTRUDA reduced the risk of recurrence or death by 44%

The data has been hailed as a validation of the PCV approach, and the beauty of the science is that these "vaccines" (vaccine is something of a misnomer since PCVs are more complex in their design and mechanism of action) can be adapted to target each different patient based on the neoantigens detected in their tumor DNA.

There are certainly some caveats here - the Moderna / Merck data was based on melanoma patients, and melanoma is one of the easier cancers to treat. The data came from a patient population of 157, which is reasonably large, but would need to be expanded in a confirmatory study i.e. a study that would persuade the FDA to approve the drug.

Data from other combinations of drugs i.e. Bristol Myers Squibb's ( BMY ) ICI Opdivo in combo with Yervoy - another BMY drug that targets the antigen CTLA-4 - are arguably as impressive as those generated by MRNA-4157, and critics of the data released by Moderna and Merck also note the use of a "one side p-value" when achieving statistical significance, when the more commonly used 2-sided value would not have shown a statistically significant effect.

Nevertheless, besides Merck / Moderna, only BioNTech - developing PCV's in collaboration with both Regeneron ( REGN ) and Roche ( OTCQX:RHHBY ) for both melanoma and head and neck, lung, and pancreatic cancers, with data expected next year - Gritstone's pipeline is the most advanced in this new field of treatment.

With $152m of cash and equivalents reported as of Q322, and a net loss for the year to date of $45m, Gritstone may not be wealthy, but has the funds to progress all its candidates through their current studies.

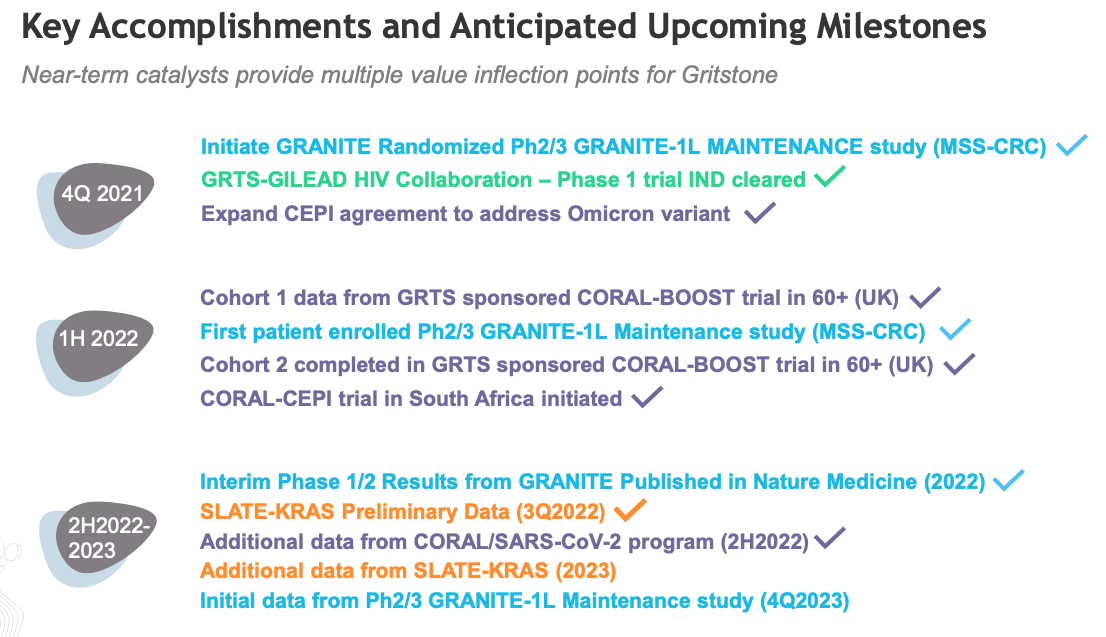

If the data promised in 2023 - initial data from the GRANITE Phase 2/3 study, Phase 2 SLATE data and updates from an intriguing collaboration with HIV therapeutic giant Gilead Sciences ( GILD ) over a candidate that had its Investigational New Drug ("IND") application cleared in late 2021, enabling in-human studies to begin - is positive, then Gritstone shareholders can look forward to a strong year of share price growth in 2023, and likely a fundraising or two, with any dilution offset by gains from the data catalysts.

Before we get too far ahead of ourselves, however, it is worth checking in on the current state of play with GRANITE, SLATE, and CORAL (the COVID studies).

GRANITE - Edging Towards An Approval Shot

In a recent investor presentation Granite describes the mechanism of action of its GRANITE program as follows:

Individualized tumor specific neoantigens delivered as a vaccine using an adenoviral vector priming ("CHaD") followed by a self-amplifying mRNA (samRNA) vector boost

The self-amplifying DNA approach is a unique feature of this program designed to increase levels of immunogenicity and help deliver more "robust and persistent" immune responses from CD8+ and T-cells to the tumor specific neoantigens.

In the Phase 1 study of 14 patients and Phase 2 expansion study in 15 patients, GRANITE was used alongside Opdivo (Nivolumab) initially and also Yervoy (Ipilimumab). The safety profile of GRANITE appeared to be satisfactory, with serious adverse safety events observed in 6 patients, including increases in alanine aminotransferase, hyperthyroidism and oesophagitis.

Gritstone published the results of the study in the peer reviewed journal Nature Medicine. Those patients who demonstrated a "molecular response" - measured by a reduction in circulating tumor DNA ("ctDNA") levels from baseline - achieved much better results than those who did not, with a median overall survival ("OS") that exceeded 18 months, versus 7.8m in those patients who did not demonstrate a molecular response. Essentially, this means that although Gritstone's PCVs are unlikely to work in every patient, certain patients who achieve molecular response may benefit substantially.

The randomised, controlled Phase 2/3 study that Gritstone has now embarked on with GRANITE seems to be being conducted in combo not only with Opdivo / Yervoy, but also with the chemotherapies Fluoropyrimidine and bevacizumab and it will focus exclusively on MSS-CRC patients, with 80 patients in the Phase 2 portion, and 200 patients in the Phase 3 portion. The endpoints are molecular response and Progression Free Survival ("iPFS").

Although there is no guarantee of success in this trial, the Phase 1/2 data certainly offers some hope that there could be a positive result, and if that were to be the case Gritstone could be in line for an accelerated approval in an indication estimated to be worth ~$9.6bn per annum, rising to $17bn by 2026.

Of course, a GRANITE product could earn only a tiny fraction of that amount given it is an adjuvant style therapy, and peak sales would likely be capped in the low-triple digit millions. Nevertheless, it would represent a huge breakthrough for Gritstone in a harder to treat patient population than melanoma, and therefore a positive result from a potentially pivotal study ought to send Gritstone's stock price surging by at least 2/3x.

SLATE - Off-the Shelf, Individualised, Delivering In The Clinic

"Off-the-shelf" essentially means that SLATE has been designed to meet the needs of patients with similar neoantigens that have become driver mutations, and does not therefore have to be custom designed to meet the needs of each individual patient, as GRANITE is.

SLATE has evolved into a KRAS targeting drug. KRAS is a gene and protein that forms an essential part of the downstream signalling process, and 2 drugs have been approved this year that target KRAS - Amgen's ( AMGN ) Lumakras and Mirati Therapeutics ( MRTX ) Krazati, to much fanfare. Once thought undruggable, KRAS is expressed in multiple solid tumor cancers and could become a cornerstone of the immunotherapy field over the next decade.

Like GRANITE, SLATE has presented a satisfactory safety profile in its Phase 1/2 studies, with only a single Grade 3 or worse adverse event recorded. Once again, molecular responses in patients were correlated with best results, and the trend in OS amongst those patients was superior to non responders - a 9.6m OS versus 4.5 months in NSCLC patients. In a press release management broke down efficacy results as follows:

- 39% (7/18) molecular response rate in evaluable patients with MSS-CRC and NSCLC. Evaluable subjects had detectable KRASmut ctDNA at baseline and a post-baseline sample. All patients with NSCLC had progressed on prior (chemo)immunotherapy.

- In 18 patients with NSCLC, a molecular response was correlated with extended OS. NSCLC patients with a molecular response demonstrated a median OS (9.6 months) more than double those without (4.5 months). The OS analysis included patients with no detectable ctDNA or no data at baseline (n=7) in the "no molecular response group." At the time of data cut-off, there were insufficient evaluable patients in the CRC patient set to support a similar analysis.

On the face of it these results suggest SLATE is potentially another drug whose progress ought to be worth watching in 2023. If I had a criticism of Gritstone's progress to date it would be that it is quite reliant on biomarkers e.g. CTDNA / molecular response, as opposed to more trusted measures such as Objective Response rates, duration of response, progression free survival etc. CEO Allen did address this on the Q322 earnings call, commenting:

As we move into an earlier disease context with healthier patients, better immune systems and more time for immune responses to mount and take effect, it is likely that the frequency and magnitude of GRANITE benefit will increase. This is a truly exciting prospect for a large population of patients for whom immunotherapy has not yet delivered any benefit.

The same can likely be said for SLATE.

Conclusion - Keep A Close Eye on Gritstone in 2023 There Are Several Major Upside Catalysts In Play

{kind=link}

As we can see above, and as I hope readers have gathered from my commentary, Gritstone has made a lot of progress in 2022, most of it under the radar as the focus has largely been on the potential of its COVID vaccine.

Gritstone's CORAL COVID vaccine studies could still provide another major catalyst for the company in 2023, as the vaccine's ability to generate potent and durable responses with the samRNA boost offers a point of differentiation from other vaccines, and Moderna / Pfizer will not necessarily enjoy the same monopoly on sales as they did when governments were stockpiling vaccines.

Nevertheless, I would pay closer attention to GRANITE and SLATE in 2023, and also keep an eye on Gilead's Phase 1 studies of its HIV therapy, developed using Gritstone's vaccine platform, given there are $725m of milestone payments in play here based on progress, plus royalties on sales if commercialised. This has the potential to become a major source of revenue for Gritstone although it is very early days.

Neoantigen therapies could become a real story in 2023, however, and Gritstone's results to date have been, in my view, a qualified success. CEO Allen still has much to prove, and the business could do with raising more funds as it will need to keep pace with Moderna, BioNTech, and likely, a host of newer biotechs and pharmas turning their attention to the PCV space.

There are far worse areas to be developing drugs for than immunotherapy, where Keytruda makes sales >$17bn per annum, and Opdivo >$7bn. Reproducing promising Phase 1/2 results in larger patients sets will be time-consuming, expensive, and very tricky - the work that goes into creating these "vaccines' is exhaustive - but another set of good data in 2023 may persuade the market that this is an area, and a company, worth investing heavily in.

Allen and his team have done a good job in the clinic, whilst Gritstone's shares have tanked. That could change in 2023, although scepticism still abounds and clinical failures will be hugely problematic for Gritstone. I remain confident that the share price will not lose value in 2023, however, and that the upside potential warrants extremely close monitoring of this enterprising biotech.

For further details see:

Gritstone bio: Keep An Eye On This Discounted Cancer Vaccine Developer In 2023