UE - Grocery-Anchored Real Estate: Brixmor's Discipline Surpasses RPT's Value

2023-04-19 15:38:04 ET

Summary

- Grocery-anchored shopping centers look strong fundamentally.

- They are also trading at attractive valuations.

- We analyze the best deals in the sector.

In our previous article , we discussed the idea that grocery-anchored shopping center properties are transacting at about 6% cap rates while the REITs trade at implied cap rates as high as 9%. That is a massive disconnect and I believe a huge opportunity, so my attention turned to finding the best grocery-anchored retail REITs.

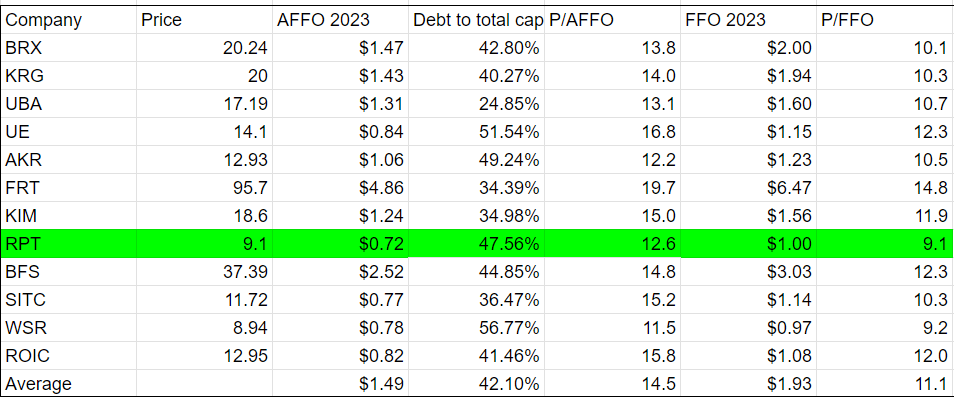

Shopping center REIT valuation

In the past I have liked Kite Realty (KRG) and Acadia (AKR), both of which still look opportunistic to me. Two others have entered the fray with exceptionally attractive valuations: RPT Realty ( RPT ) and Brixmor Property Group ( BRX ).

RPT is the cheapest of the group with a price to 2023 FFO of 9.1X and just 12.6X 2023 AFFO.

{kind=link}

Brixmor is not far behind with 10.1X P/FFO and 13.8X P/AFFO. With slightly lower leverage at 42.8% debt to capital compared to 47.6% at RPT one could argue the valuations are very close on a leverage neutral basis.

Therefore, the better REIT is to be determined by fundamentals.

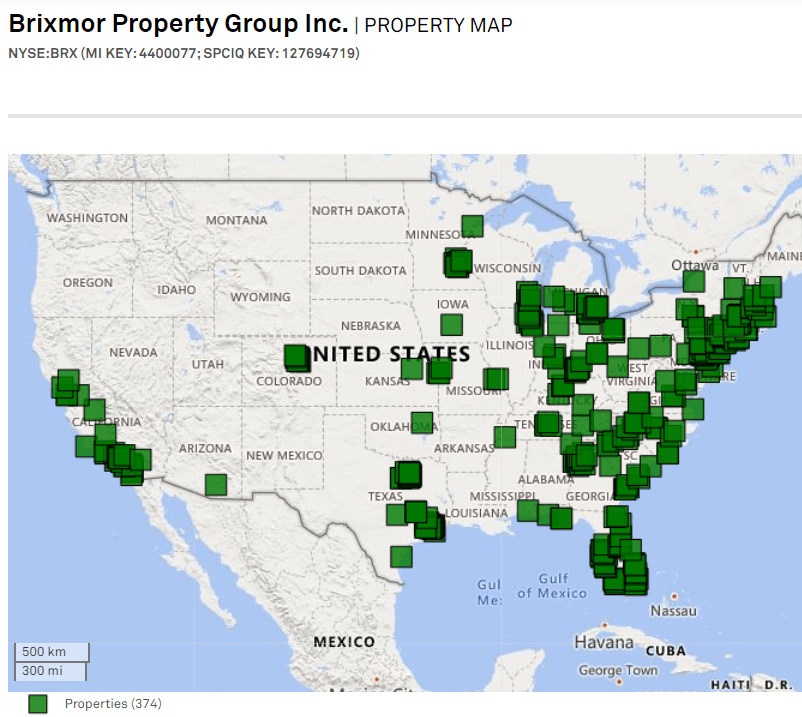

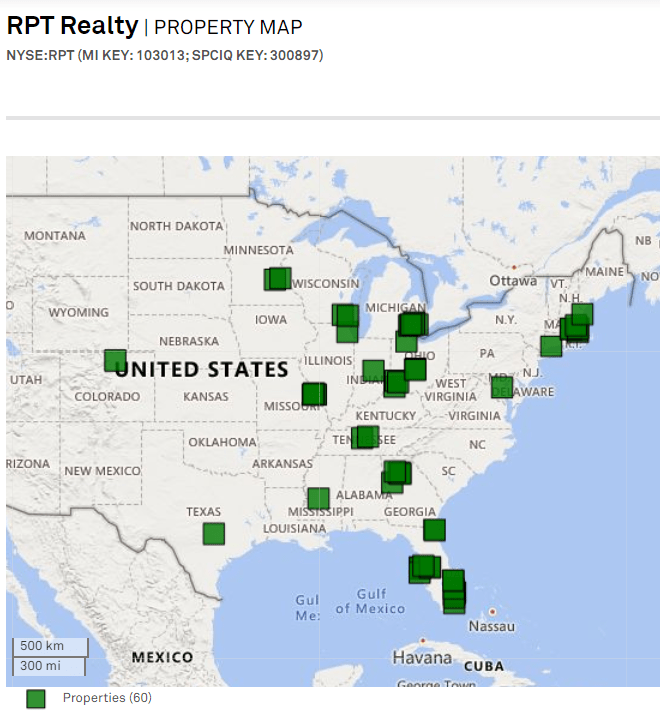

Property locations

Brixmor is a large cap with hundreds of properties located in just about every major MSA.

{kind=link}

This is nice for diversification but doesn't really target any particular areas.

RPT is a bit more concentrated in Boston and Florida.

{kind=link}

Florida submarkets are in a great place right now with significant population inflows so I marginally prefer RPT's locations.

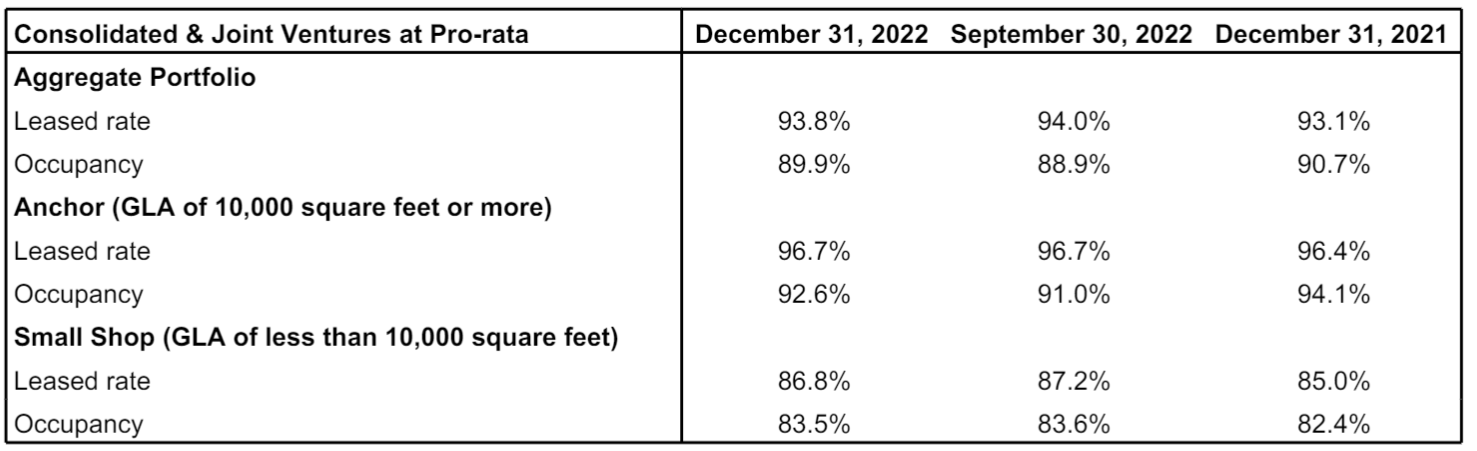

Rent per square foot is quite comparable with both companies in the $16s. Occupancy is also comparable with BRX at 90.2% and RPT at 89.9%

Leasing growth

Retail real estate is simultaneously rapidly growing and potentially troubled.

On the positive side, the paucity of new supply over the past 15 years has limited the amount of available square footage in good locations which puts power in the hands of the landlords. As a result, the REITs are enjoying the ability to hike rents up 10%-30% on new leases over their expiring rental rates.

This creates two sources of growth:

- Mark to market

- SNO (signed not operating) lease commencements

Expiring leases were previously signed at rates far below current market rates and the escalators have not kept up so renewals and new leases are getting marked up quite a bit. Here is Brixmor's leasing activity below.

{kind=link}

When new leases are signed it can take a while for them to actually kick in as tenant move-ins can sometimes be set for a future date. 2022 was a huge year for retail leasing so there is quite a backlog of leases that are signed but not yet commenced.

For RPT, the leased occupancy is almost 400 basis points higher than the current occupancy.

{kind=link}

As these leases commence that will be north of $0.10 of FFO/share accretion.

Overall, both companies have strong growth outlook with rent increases and SNO leases.

The key with retail is having this growth be net accretion. If new leases are being signed but old tenants are leaving, the incremental FFO might be lost to vacancies. This is where I think Brixmor has a substantial advantage.

Tenant profile

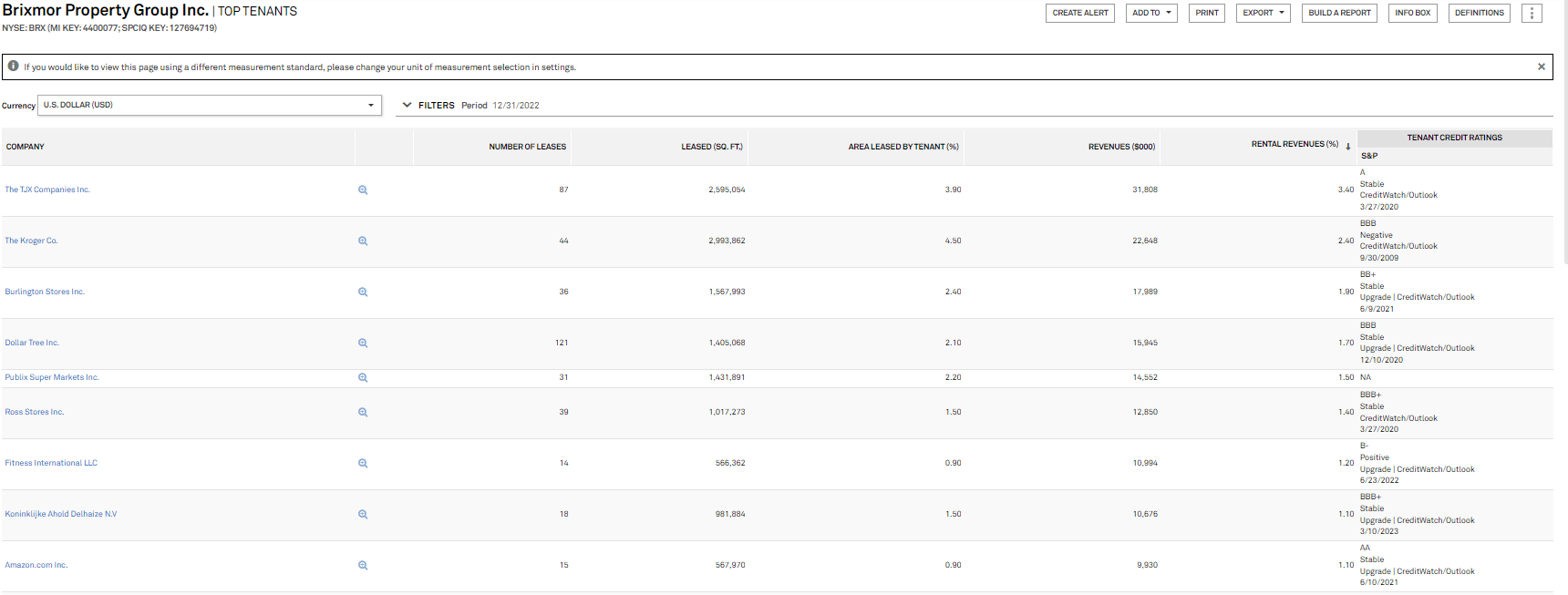

Brixmor has a strong tenant roster with the major grocers and TJ Maxx as its big box stores.

{kind=link}

Big boxes are the space that is vulnerable in this environment, so having these highly successful retailers in BRX big boxes provides a consistent source of foot traffic for the adjacent small shops.

I see RPT's tenants at a bit more risk for two reasons:

- RPT's properties have multiple big boxes

- Some troubled tenancy

Power centers are shopping centers with multiple big boxes and each of these needs to be filled to keep the centers healthy. Grocery stores and companies like Dick's Sporting Goods do a great job filling these spaces and consistently paying rent, but I think Regal Cinemas and Bed Bath and Beyond are on the weaker side.

S&P Global Market Intelligence

The disruption caused by anchor tenant turnover might undo a significant portion of RPT's growth resulting in weaker FFO/share growth than BRX.

RPT acknowledges this drawback in their 2023 guidance.

{kind=link}

Balance sheet

Both companies have strong balance sheets and are reasonably well prepared for this environment. RPT is investment grade, albeit on the bubble due to absolute level of leverage. Its debt is well laddered with minimal maturities during the window of time in which interest rates are expected to remain high.

{kind=link}

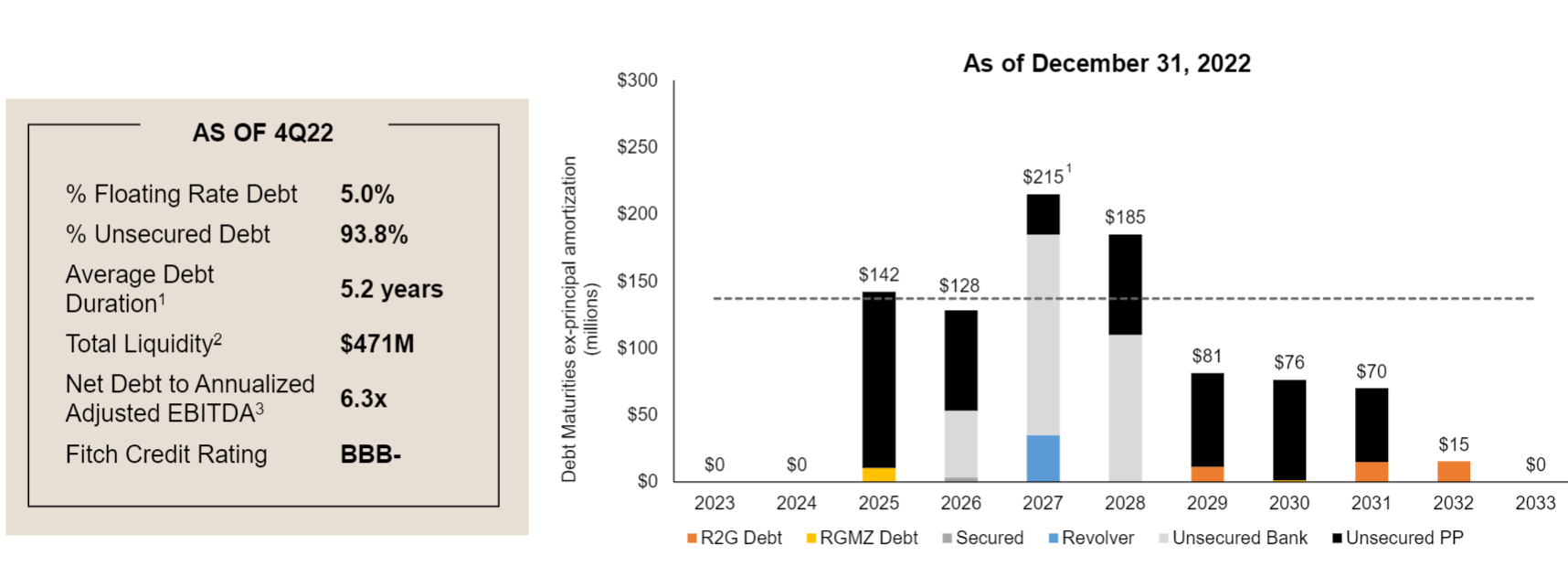

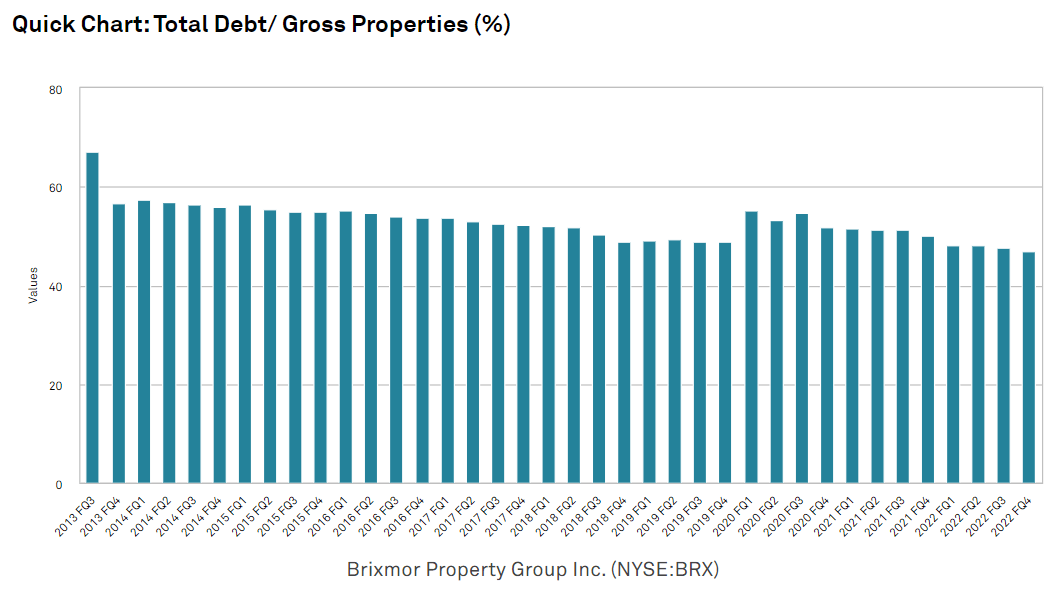

Brixmor has worked hard over the years to bring its leverage down and now sits at a very comfortable level.

{kind=link}

It also has well laddered maturities.

{kind=link}

No major concerns here with a slight edge to BRX for its lower debt levels.

Management and strategy

REITs really like to grow in size. When spreads are favorable such growth is usually accretive to shareholders.

The typical spread is something around 2% or 3% where the REIT can invest at a higher ROIC than its WACC resulting in the cycle of raising capital and deploying it into assets accreting to the bottom line.

These are not normal times. The REITs are trading at close to 9% implied cap rates which makes cost of equity prohibitively high and cost of debt is also fairly expensive right now. Thus, external acquisitions are straight up not accretive.

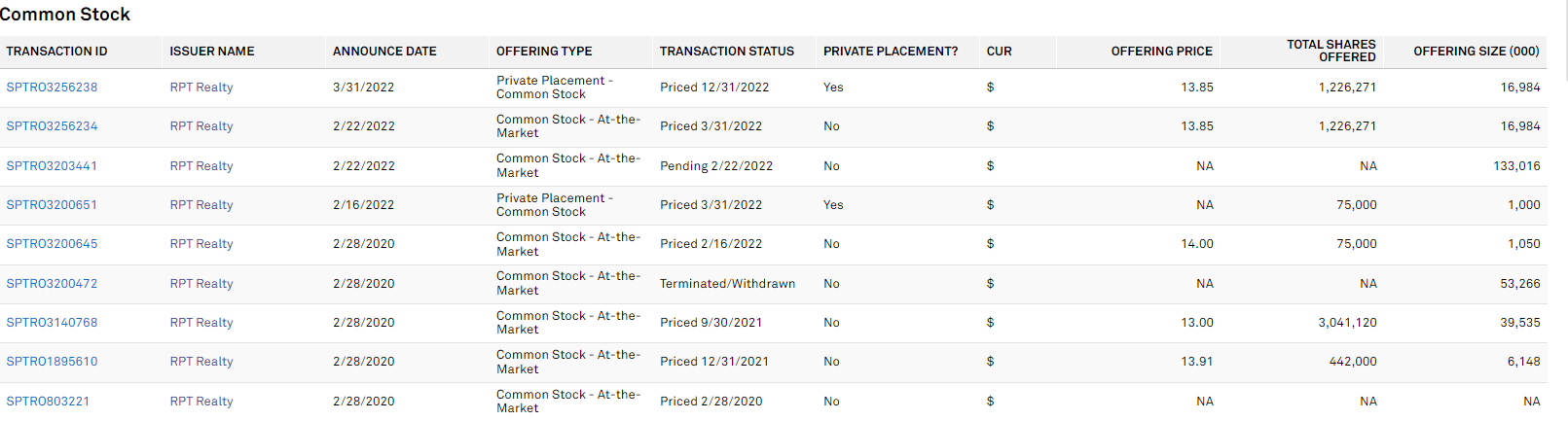

It is a time of separating the wheat from the chaff. The good REIT managers will show capital discipline while the sloppier teams will continue buying. I fear RPT is a bit less disciplined.

They have been major equity issuers over the past few years.

{kind=link}

Fortunately, these were at higher equity prices than today's level, but it was still a time in which spreads were not great.

Most real estate transactions are somewhat private where the REIT will only disclose it after it happens with the public not privy to the negotiating process. Occasionally, however, we get a glimpse of what is happening at the negotiating table.

Both Urban Edge (UE) and RPT attended the Citi Conference and they ended up being interviewed together. The Citi analyst was asking questions of Harper (RPT's CEO) and Olson, UE's CEO.

Craig Allen Mailman

Brian, just curious what markets you're most excited about within your portfolio now where you see the best opportunity to grow externally, but also organically?

Brian L. Harper

Yes. I mean we're -- as I'll steal from -- I'm in a Citi Conference, but I'll steal from Jamie Dimon, who said earlier this week, in Miami, 7.5% of our ABR is coming from here, 4% of that is Brickell. We have phenomenal real estate and repositioning real estate here, where we're literally buying out tenants and 3x'ing rent. It's about an -- Miami represents about a 9% CAGR over the next 3 years. RPT's about 50% of our cash flows are coming from the state of Florida, Boston, Nashville and Atlanta. And we -- I really believe in concentrations of assets to really maximize G&A leverage with tenants, leverage with vendors, leverage with the brokers. So I would say all of Florida is really where we're spending a lot of time, but Boston is another area where we had 0 exposure prior to COVID. And through the GIC partnership, Boston now will soon be our #1 MSA for the company.

Jeffrey S. Olson

You beat me on the property. We were competing, and you won it. It was a good deal.

Ouch! Jeff Olson's comment is absolutely brutal.

This is typical CEO speak where it is phrased as a compliment but clearly disparages the competition. Buying properties is not a competition in which the more skilled buyer wins the bid. It is the buyer who is willing to pay more that wins the bid.

So if we translate this to what he is actually meaning it is that RPT was willing to pay more for the asset than Urban Edge thought was reasonable.

In this sort of environment I want to be invested in companies that are significantly more disciplined with their capital.

Brixmor is a beacon of discipline

Here is how James Taylor (CEO of BRX) views acquisitions:

"Now as it relates to external growth, we don't see the opportunity immediately today, but we are watching very carefully the dislocation in the asset level financing market. And we're watching what that does for private owners who have to rely on asset level financing to recapitalize their assets, to put capital in to backfill tenants, etcetera. And we're cautiously optimistic that, that external growth opportunity, not in the next quarter or so, but over the next few quarters becomes compelling enough to execute upon. But it's going to be opportunity driven."

We recognize that our incremental cost of capital has increased and yet it will be interesting to see how this all settles out from a capital markets perspective for owners of privately held assets. One thing to appreciate about our space is that it's 87% held in private hands. It's been a long time in a cycle since you've seen securitization on any scale from private to public hands. If we do go into an environment where asset level borrowers are disadvantaged because of the lack of availability of bank capital, the conduit maybe not being there, the life companies having finite levels of financing.

For platforms such as ours that have investment-grade balance sheets and the capacity to access the unsecured market, we may find acquisitions penciling. They're not today, right? And the good news is we can be disciplined because we're generating great growth on our internal plan."

When spreads aren't great, that is exactly what I want a REIT to do. Sit back and wait while using free cash flow to grow internally.

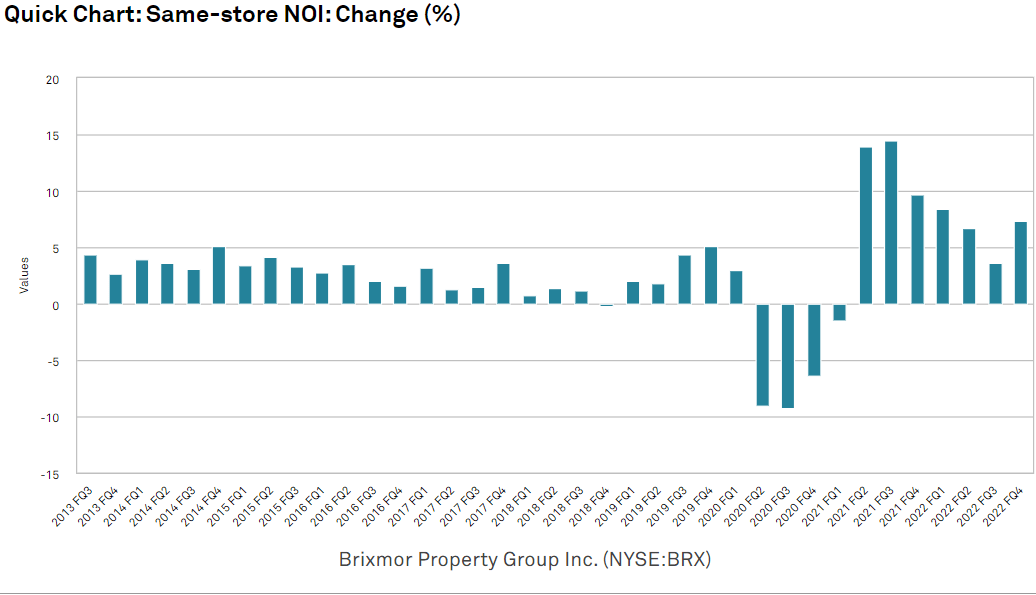

Brixmor doesn't need to be in a hurry because they are growing organically. Aside from the pandemic which hurt shopping centers, organic growth has been consistently strong.

{kind=link}

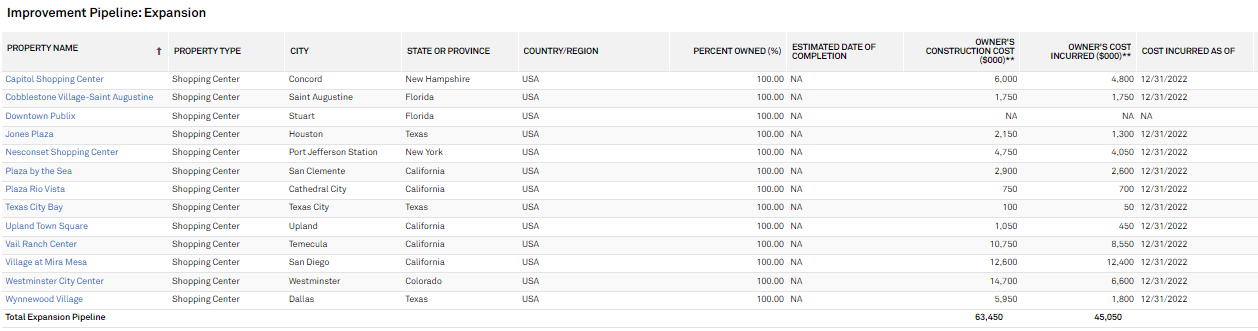

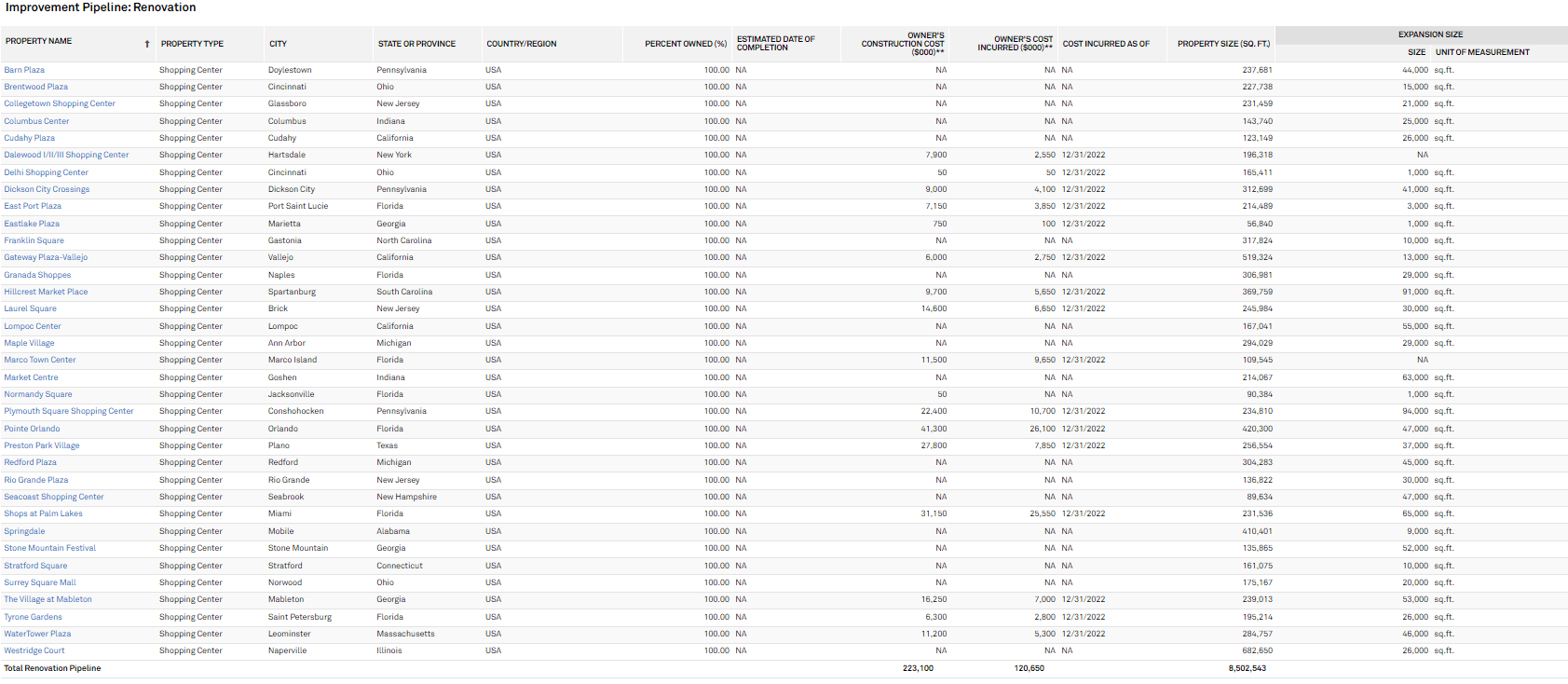

Presently Brixmor's dividend payout ratio is quite low which leaves a fair bit of free cash flow. That cash is being put into expansions and improvements at 9%-11% cap rates.

{kind=link}

{kind=link}

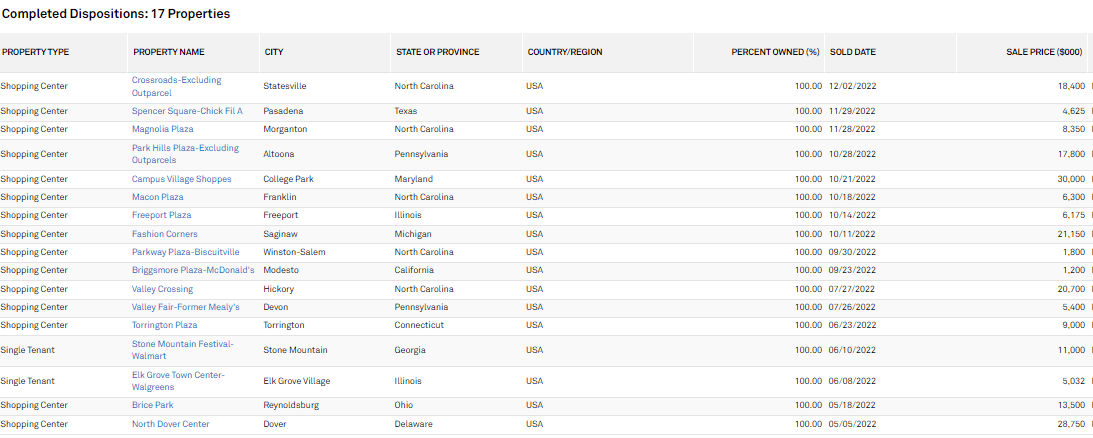

The rest of the funding for the myriad of redevelopments comes from dispositions at low cap rates.

{kind=link}

Brixmor is essentially taking advantage of the low cap rate at which grocery-anchored shopping centers are sold. They can sell in the 6s and redevelop in the 9%-11% range.

That is a great spread and a great way to keep growing even as cost of equity capital is prohibitively high.

The bottom line

Grocery-anchored shopping center REITs are trading at huge discounts to the value of their underlying assets. Brixmor appears to be one of the best in the space with disciplined management and organic growth coming from a combination of mark-to-market, SNO leases commencing and high ROIC redevelopments. At this level of growth, BRX should trade at a significantly higher multiple.

For further details see:

Grocery-Anchored Real Estate: Brixmor's Discipline Surpasses RPT's Value