SFM - Grocery Outlet: Shares Are Getting Close

2023-06-21 05:02:47 ET

Summary

- Grocery Outlet's strong financial performance and declining share price make it a more appealing prospect than it was previously.

- The company's growth has not been enough to justify the market's high premium, which is what has caused a lot of its pain.

- A further upgrade could be possible if shares drop further or profitability expectations rise.

As time goes on, I love seeing a company that continues to generate strong fundamental performance become more appealing because the combination of strong performance and a declining share price brings it to a level that makes it a more reasonable prospect. One company that I have seen move in that direction in recent months is extreme value retailer Grocery Outlet ( GO ). Revenue, profits, and cash flows continue to expand at a nice clip. On an absolute basis, shares of the company look quite affordable, though they are pricey compared to similar firms. It's this relative priciness that turns me off, even after shares of the company have taken a beating over the past few months while the broader market has increased. Having said that, the picture is becoming more appealing with each percentage point that the stock drops. And have shares continue to fall from here, I could very well turn bullish on the firm.

When growth isn’t enough

Buying into companies that achieve attractive growth is often viewed as a great way to make some money. But you also need to be careful about how much you're paying for that growth. This was a sentiment that I had when I last wrote about Grocery Outlet in November of 2022. At the time, I acknowledged how fast the business was growing. But shares looked so pricey, even when factoring in that growth, that I could not be anything other than neutral on the firm. This had represented an upgrade compared to the ‘sell’ rating that I had assigned the stock when I wrote about it in August. It would seem, however, that my upgrade from a ‘sell’ to a ‘hold’ was perhaps a bit premature. Even though the stock had underperformed the S&P 500 by roughly 20% between those two articles, the stock has dropped another 8.8% since I upgraded it. That compares to the 14.3% increase seen by the S&P 500 over the same window of time.

{kind=link}

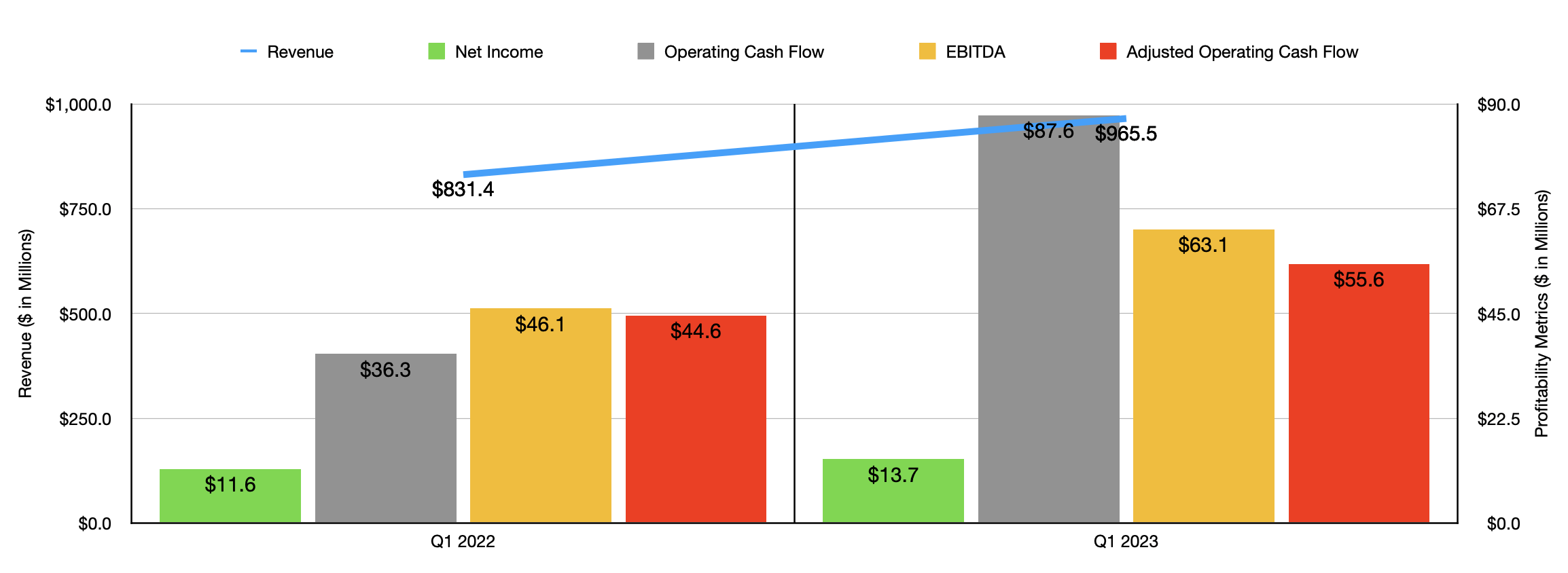

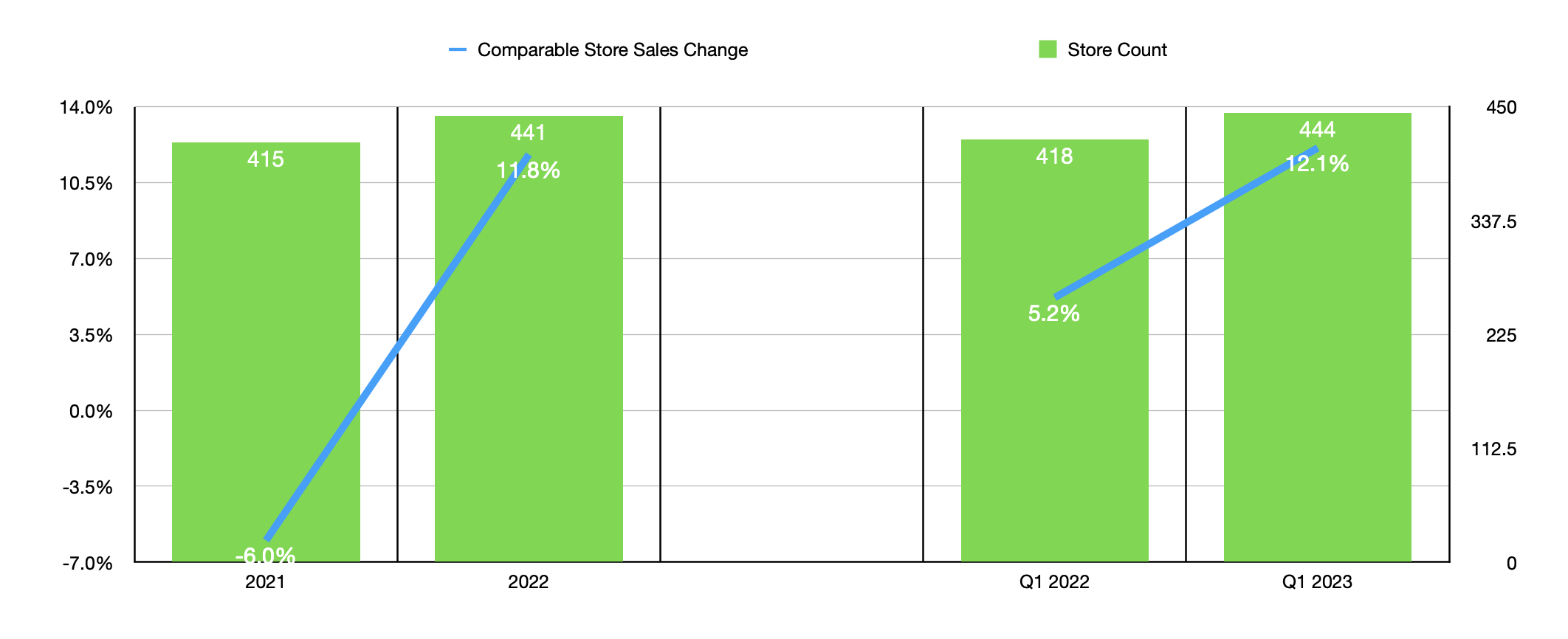

Given these significant declines, it wouldn't be shocking to look at the fundamentals of the business and see weakness. But that's the exact opposite of what we see when we look only at the numbers. During the first quarter of the company's 2023 fiscal year, for instance, sales came in at $965.5 million. That's 16.1% above the $831.4 million the company generated only one year earlier. A good portion of this sales increase was a rise in the number of locations that it had an operation from 418 to 444. But on top of this, the company also saw comparable store sales growth of 12.1%.

{kind=link}

What is really exciting to me is that 7.9% of the sales increase came from a greater number of transactions. By comparison, 3.9% was attributable to an increase in average transaction size. The growth that the company saw in comparable transactions is great, because it means that either more people are visiting its stores, that people were visiting at stores more often, or some combination of the two. Multiple sources, such as this one and this one, support the idea that, faced with inflationary pressures and high interest rates, more Americans are focusing on getting attractive discounts where they can find them. For instance, 77% of Americans will regularly shop clearance sections of stores. And according to one study from Tufts University, dollar stores have become the fastest growing food retailers in the nation.

{kind=link}

This strong financial performance has had a positive impact on the company's bottom line. Net income expanded from $11.6 million in the first quarter of 2022 to $13.7 million in the first quarter of this year. Operating cash flow more than doubled from $36.3 million to $87.6 million. Though if we adjust for changes in working capital, we would have seen a more modest rise from $44.6 million to $55.6 million. Meanwhile, EBITDA also increased, climbing from $46.1 million to $63.1 million over the same window of time. As you can see in the chart above, the first quarter of 2023 is part of a larger trend. By every measure, 2022 was a better year for the company than 20/21 was, with a 26-store increase and an 11.8% rise in comparable store sales fueling growth for the retailer.

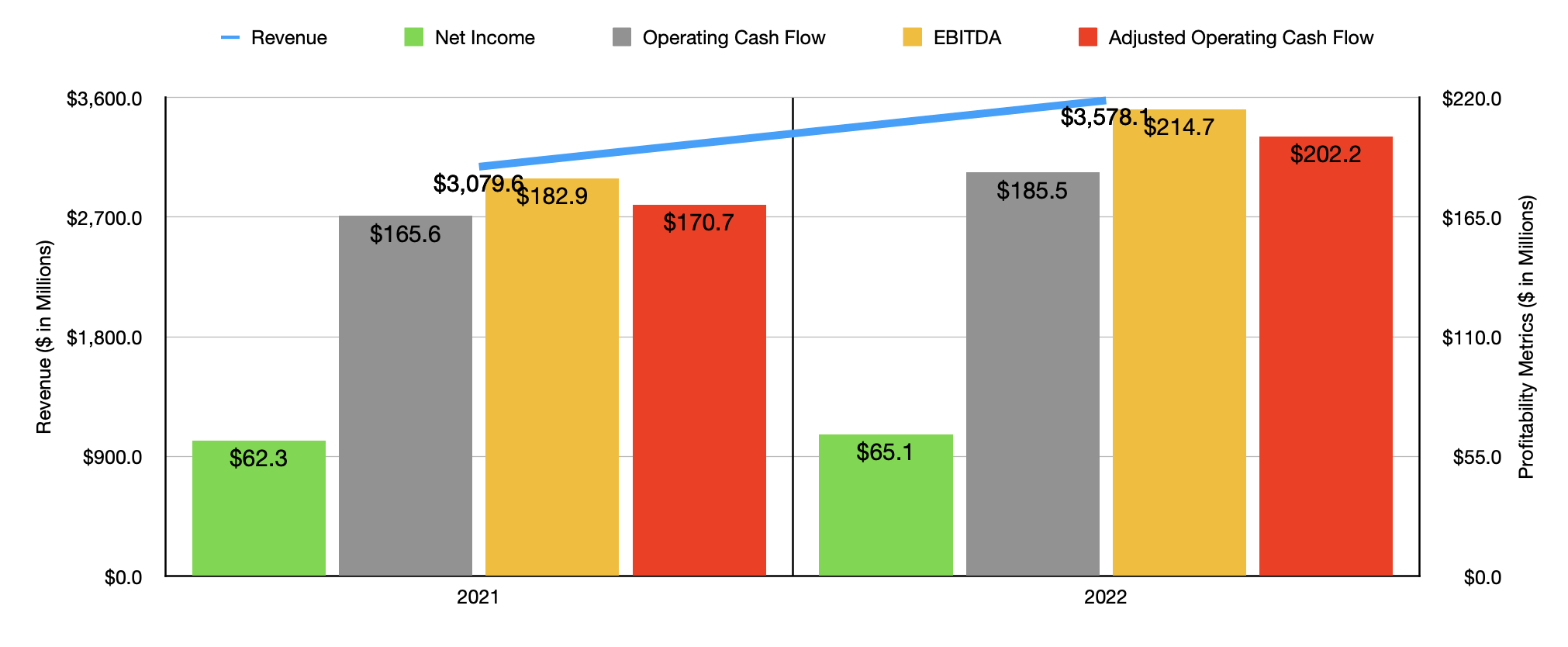

Just because a company is growing rapidly, does not mean that the business makes sense for investors to buy into. On an absolute basis, shares of Grocery Outlet look reasonable. For 2023 as a whole, management expects revenue of $3.90 billion. This would be driven by a 5% to 6% increase in comparable store sales and the opening of between 25 and 28 new stores. That should cause earnings per share to come in at between $0.96 and $1, which would translate, at the midpoint, to net profits of $98.6 million. Also for the year, management is forecasting EBITDA of between $240 million and $246 million. Management did not provide any guidance when it comes to other profitability metrics. But a good approximation for adjusted operating cash flow would be $228.9 million.

{kind=link}

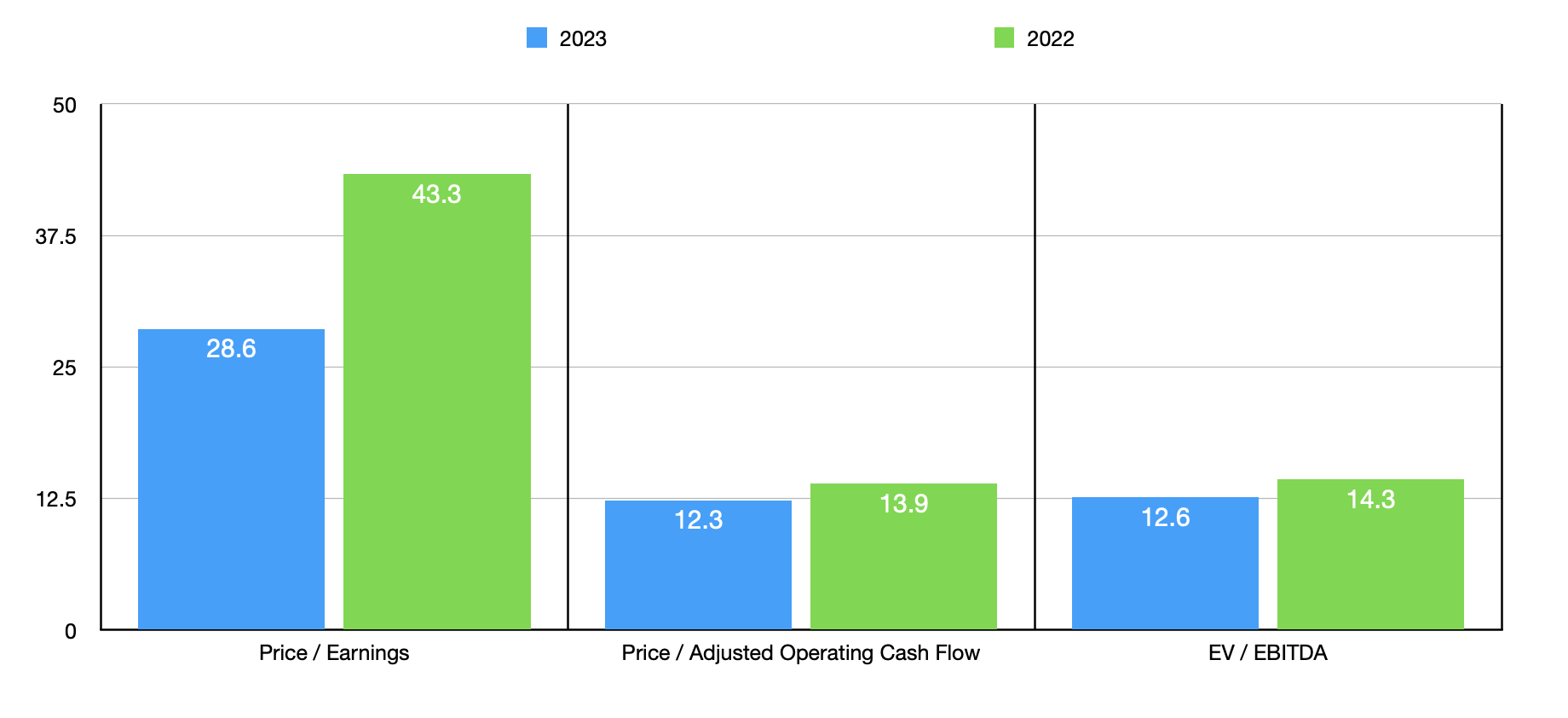

As you can see in the chart above, shares of Grocery Outlet look pricey on a forward basis when it comes to the price to earnings multiple. But when it comes to the price to adjusted operating cash flow multiple and the EV to EBITDA multiple, the stock looks much more reasonable. These numbers are also cheaper than if we were to use the results from 2022. However, one problem is that shares are still very pricey relative to similar firms. In the table below, you can see how five similar enterprises are priced relative to the forward pricing for Grocery Outlet. Even if we are generous in using the aforementioned forward pricing, shares of our prospect are still more expensive than any of the peers I compared it to.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Grocery Outlet |

| 28.6 |

| 12.3 |

| 12.6 |

| Sprouts Farmers Market ( SFM ) |

| 14.5 |

| 9.1 |

| 5.8 |

| Natural Grocers By Vitamin Cottage ( NGVC ) |

| 16.6 |

| 5.7 |

| 5.0 |

| The Kroger Co ( KR ) |

| 13.2 |

| 5.3 |

| 5.7 |

| Albertsons Companies ( ACI ) |

| 9.8 |

| 4.2 |

| 4.2 |

| Casey's General Stores ( CASY ) |

| 18.4 |

| 9.3 |

| 9.9 |

Takeaway

In the long run, I fully expect Grocery Outlet to do quite well for itself. I believe that the overall risk of investing in the company is quite low. Having said that, the rapid growth that the company has achieved has not been enough to justify the lofty premium that the market demands. I do think that the company is getting closer to the point where a further upgrade could very well be on the table. But in order for that to happen, I would need to see shares drop a bit further or for profitability expectations to rise. Until then, I believe that the ‘hold’ rating I assigned the stock is still appropriate at this time.

For further details see:

Grocery Outlet: Shares Are Getting Close