ASR - Grupo Aeroportuario del Pacífico: It's Time To Buy This Dip

2023-09-08 04:10:44 ET

Summary

- PAC stock has seen a 15% dip from its 52-week highs, presenting a buying opportunity.

- Pacifico's traffic results have shown renewed acceleration after a slowdown earlier this year.

- Profits are at record highs amid both strong top-line growth and rising EBITDA margins.

Mexico has three publicly traded airport operators, and I've been covering all of them here at Seeking Alpha dating back to around 2016. As the global tourism recovery trade has played out, attention has started to shift from hospitality-focused travel stocks back toward ones with more of a business component.

This makes it a great time to update the outlook for Grupo Aeroportuario del Pacifico (PAC), as it has both tourism-focused airports and properties that are primarily tied to the growth of Mexican business and industrial activity.

In particular, I highlight PAC stock today because with its 15% dip from the 52-week highs, this is actually close to the largest pullback the stock has seen since the early days of the pandemic:

Shares jumped from $70 to over $100 in early 2021 as Pacifico returned to robust profitability more quickly than analysts had expected. In late 2021, shares made their next move, rising as industrial growth started to kick in on top of the initial tourism reopening traffic. After puttering along around $150 for most of 2022, PAC stock then surged to $200 to start 2023 as Mexican stocks and financial assets put in a sharp rally across the board.

Zooming in on the past year, the stock price peaked this spring, sitting in a trading range between $170 and $200 since February:

Just over the past week or so, the stock has dropped from $193 to $173 due to a sell-off in Mexican equities more broadly. I see this as a solid buying opportunity, as Pacifico just put up another strong traffic report. Meanwhile, fundamentals are strong, and I expect the stock to move higher out of this trading range in due time. I'm looking for a share price north of $200 plus the generous dividend on top over the next year.

Traffic: A Continuing Strong Uptrend Despite Some Headwinds

As mentioned, there are three publicly traded Mexican airport companies.

Right now, Sureste (Grupo Aeroportuario del Sureste) (ASR) is delivering the weakest results. Sureste is primarily tied to Mexican tourism along with the currently shaky Colombian market. Sureste's key Cancun property also faces competition from a new Tulum airport , though I believe that threat is overblown. In any case, Sureste grew traffic just 4% in August year-over-year.

Centro Norte (Grupo Aeroportuario del Centro Norte) (OMAB), which is primarily tied to Mexican industrialization, showed the best results, with traffic soaring 22% year-over-year for August 2023. Given the rush of new factories opening in key Centro Norte cities such as Monterrey this year, it's not surprising that Centro Norte is leading the charge in benefitting from the reshoring wave.

Pacifico finds itself in the middle of the three Mexican airport groups in traffic results, which makes a lot of sense given its mix of tourism and industrial-focused airports.

To that point, Pacifico's tourism-driven airports are entering a pause after several years of torrid growth. Cabos traffic was up 5% year-over-year in August, and Puerto Vallarta grew less than 1%. I've been expecting a significant deceleration in Mexican tourism and that is starting to play out for both Pacifico and Sureste.

However, Pacifico's more industry and business-focused airports continue to show strong growth . Tijuana jumped 12% year-over-year, and Guadalajara traffic soared 18%. As Guadalajara is Pacifico's largest and most important airport, the outperformance there was more than enough to offset the slowing figures at the tourism-focused properties.

There was an additional positive sign in the August numbers. That was that load factors on flights using Pacifico airports jumped from 79% in August 2022 to 81% for this past month. Load factors had been generally weakening in 2023 as it appeared that airlines were adding capacity at a rate faster than the market could absorb it. However, the upward turn in load factors suggests that things are balancing out and could incentivize airlines to consider another round of additional capacity expansion.

In conjunction with the rise in load factors, we've also seen Pacifico's y-o-y growth rate reaccelerate. Consider the past four months of traffic growth:

- May 2023: +10.4%

- June 2023: +12.5%

- July 2023: +11.5%

- August 2023: +14.1%

Mexican airport stocks have been generally rangebound in 2023, perhaps due to the decelerating year-over-year traffic growth rates observed earlier this year. This August figure, however, suggests that the traffic growth is more of a secular story. That's in contrast to the bearish narrative that airports were simply a pandemic reopening trade that was now drawing to a close.

To add more context to that, I'd note that Volaris (VLRS), by far the fastest-growing carrier within Mexico, has seen its stock price lose altitude since 2021 with another downturn kicking in over the past few months:

Weaker load factors and profitability are a negative incentive to airlines like Volaris in terms of adding new routes and frequencies at Pacifico airports. Hopefully the improvement in operations in August will signal an inflection point -- especially at the industrial airports -- and pave the way for further capacity expansion.

On a related note, Mexico's aviation industry was downgraded to FAA category 2 safety status several years ago. Industry experts suggest this has caused more than $1 billion in harm to the sector. This downgrade has prevented Mexican carriers such as Volaris from opening new routes to the United States. As a result, for international flights into Mexico, new routes have had to be opened by foreign carriers, with the Mexican players locked out of the marketplace.

From my talks with industry insiders, the expectation had been that Mexico was unlikely to regain FAA level 1 status until the current Mexican president left office at the end of 2024. However, there is now speculation that Mexico could regain its safety classification by the end of 2023, which would be a positive surprise for the industry.

I believe that Volaris and other Mexican airlines have seen stagnating load factors in part because planes that were originally supposed to be deployed in the U.S.-Mexico international market have instead had to operate on domestic Mexican routes in the interim. As such, we could see a significant bump in results for Mexican aviation if and when FAA compliance is regained hopefully this year but perhaps more likely toward the end of 2024.

Pacifico's Record Profitability

Pacifico's Q2 results showed record numbers across the board. Passenger growth jumped 12.7% year-over-year. The real magic kicks in when seeing how that passenger growth is reflected in financial results. From that 12.7% increase in passengers, Pacifico grew top-line revenues a tremendous 26.5%.

That's more than twice as much additional revenues as passengers. It speaks to the strength of the airport business model. Global aviation has historically grown much faster than global GDP, and that's especially true in emerging markets. And then from that favorable starting position, Pacifico can generate a huge amount of incremental revenues from that passenger growth as it monetizes non-aeronautical opportunities such as retail, car parking, advertising, hotels and industrial facilities, and so on.

Pacifico also has maintained a razor-sharp focus on costs. The company grew its EBITDA margin from an already excellent 70.4% to 72.4% this quarter. The company's overall EBITDA has blasted off over the past five years, making the 2020-era dip a distant memory:

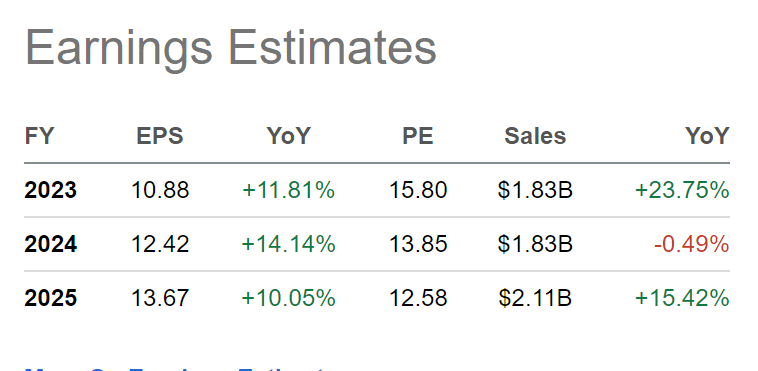

What price do we have to pay for Pacifico with its 26% top-line growth and sky-high profit margins? Currently, it is at a forward P/E of just 15.8:

{kind=link}

And, adding to that, I believe these earnings estimates are too low. In particular, I struggle to see how revenues will be flat-to-slightly-down in 2024 given that traffic is still growing everywhere and is outright booming at the firm's more industry-focused properties. On top of that, Pacifico's concessions have an adjustment for inflation built in and thus will see higher revenues simply from that even if passenger traffic growth inexplicably disappeared next year.

Pacifico pays close to 100% of its free cash flow out as dividends annually. This leads to a variable but rapidly increasing rate of dividend payments. I expect about $8/share of dividends for 2024, which would be a 4.6% dividend yield on the current price. I expect that dividend to grow at a compounded low double-digits rate over the next decade, making this a phenomenal growth and income stock going forward.

PAC Stock Verdict

Mexican stocks (EWW) have dipped over the past two weeks, perhaps tied to concerns around a slowdown in the Chinese economy which could spark global economic worries:

Many emerging market currencies, including the Mexican Peso, have slipped as this global slowdown narrative filters through the system. I'm of the view, however, that Mexico is an alternative for a significant chunk of Asian manufacturing, at least as it pertains to the North American consumer market. Mexico did just overtake China as the United States's #1 trade partner this year, after all. As such, it doesn't make sense to have a kneejerk sell-off in Mexican stocks every time we get weak economic data out of China.

The latest traffic report from Pacifico, released earlier this week, highlights that point. Even with the concerns around global growth, Mexican passenger traffic continues to grow at a double-digit clip with the business-focused properties showing the biggest increases of all. I believe we're still in the early innings of the North American industrialization/reshoring story and that companies that provide transportation and logistics will benefit greatly as this plays out. And the airport industry in particular enjoys uniquely strong economics and a tremendous moat around the business, making Pacifico a great long-term investment.

With the recent dip in Mexican equities and Pacifico stock in particular, there is an opportunity to take advantage of the current correction.

For further details see:

Grupo Aeroportuario del Pacífico: It's Time To Buy This Dip