ASR - Grupo Aeroportuario del Pacífico: No Easy Way Out

2023-10-10 20:49:38 ET

Summary

- Mexican airport regulator's potential change to tariff formula caused shares to plummet.

- The current share price already incorporates a 15% tariff cut.

- Other scenarios offer limited upside potential, making GAP shares a weak risk-reward option.

Summary

Grupo Aeroportuario del Pacífico ( PAC ) shares were hit hard last week at one point down 32% to US$109, on a surprise announcement that the Mexican airport regulator apparently changed the formula by which the three Mexican airport groups charge for services i.e. generate regulated revenue.

The company press release did not offer much information but caused panic. In my view, the company made an error in communication that could have been avoided by simply waiting to meet with the authorities to better understand the consequences and mitigations if any, before making a public statement.

At present, the shares are rebounding on several unconfirmed tariff cut expectations. To better understand the potential impact this may have on the stock, I conducted three sensitivity analyses. The result, in my view, is that PAC may come out the worst of the three Mexican airport stocks.

For more depth on the Mexican Airport business model please refer to my article. Mexican Airports: I Prefer ASR Over OMAB And PAC

Pre-Announcement Estimates and Valuation

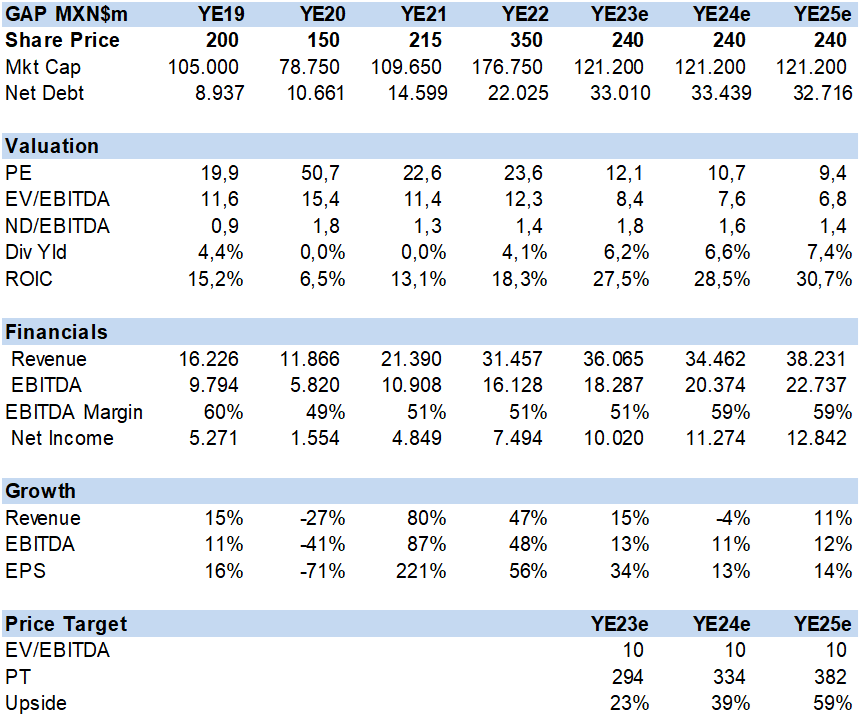

Prior to last week's events, I rated PAC a hold given its higher valuation vs peers and increasing debt levels. The company is during a US$1.5bn capex plan that includes a new runway in Guadalajara.

GAP Financial Summary and Valuation (Created by author with data from GAP)

{kind=link}

Three Scenarios

PAC faces an uncertain tariff cut at best. To better gauge the impact this may have on results and valuation I conducted three scenarios.

1. What tariff cut is priced in?

2. What if tariffs decline 8%?

3. What if GAP is allowed to extend its concession contract for another 50yrs but acquire the abandoned Mexico City airports debt (40% or US$1.9bn)?

Scenario 1: What is priced in

Lower Valuation Multiple: Before applying tariff cuts to regulated service (passenger and airplane landing fees) one should first assume that a unilateral change in the concession rules increases business risk and as such one should use a higher discount rate or lower fair value multiple.

I cut the fair EV/EBITDA multiple to 9x from 10x. This is less than the discount applied to ( OMAB ) due to PAC's lower overall exposure to regulated tariffs. PAC has a higher percentage of commercial revenue thanks in part to innovation such as the pedestrian bridge from Tijuana to USA called the CBX and more importantly due to operations in Jamaica that are not part of this tariff risk and contribute 10% to consolidated EBITDA.

Then I calculated that regulated rates would need to be cut by 15% to produce a 14% decline in EBITDA that at 9x EV/EBITDA would price the shares at the recent level. Note that I do not assume a reduction in capex while traffic growth remains as estimated.

While this level of tariff cut has been mentioned in the media, it seems aggressive to me, at least without some mitigating factors such as lower capex, lower traffic risk, or the extension of the concession for another 50yrs.

GAP Tariff Cut of 15% Price In (Created by author with data from GAP)

Scenario 2: An 8% tariff cut

This 8% tariff cut seems more benign to results with a 7% impact to EBITDA. However, it would damage the upside potential due to a greater valuation discount. An 11% upside estimate to YE24 does not seem sufficient for the risk taken.

GAP 8% Tariff Cut Impact (Created by author with data from GAP)

Scenario 3: Adding US$1.9bn in debt

This third scenario requires more imagination and a bit of conspiracy theory. When AMLO cancelled the New Mexico City Airport, during construction, the Mexican Federal government was left with about US$6bn in debt. I read in media sources that the Govt wanted to have this debt removed and transferred to the three airport groups in exchange for renewing the concession for another 50yrs. This seems somewhat fair, depending on the structure of the debt transfer and I would keep the 10x EV/EBITDA as a target multiple.

Under this scenario, I assume PAC takes about US$1.9bn (40% of the US$4.8bn outstanding) in line with Grupo Aeroportuario del Sureste ( ASR ). The problem is that PAC has about US$1.8bn in debt due to capex execution and healthy dividends. So, doubling this without a material increase in EBITDA drives the price target lower with a 10% upside potential to YE24. Again, in my view, not enough reward for the risk.

GAP Debt Transfer Impact (Created by author with data from GAP)

Conclusion

PAC looks to be the worst risk-reward stocks of the three Mexico Airport Groups given higher starting valuation and significant debt levels. On 8% tariff cut, I see only 11% upside to YE24.

For further details see:

Grupo Aeroportuario del Pacífico: No Easy Way Out