PAC - Grupo Aeroportuario Del Pacifico: A Story Of High ROIC And Growth

Summary

- Grupo Aeroportuario del Pacifico has high NOPAT margins, allowing it to have high returns on invested capital, as well as attractive debt coverage ratios.

- Mexico's proximity to the United States will be beneficial for the industry given the new trend of "regionalization" rather than globalization.

- I believe PAC is undervalued on the basis of a discounted cash flow analysis, a GARP analysis, and a multiple analysis.

Editor's note: Seeking Alpha is proud to welcome Gabriel Romano as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

I currently live in Guadalajara, Mexico; the place where Grupo Aeroportuario del Pacifico ( PAC ) or GAP (Spanish ticker) has its main airport and headquarters. During my last visit, I couldn't help but notice how strong and durable the business model is, because when you think about it airports operate in a monopoly-type industry, with no close competitors.

Chances are that where you currently live there's only one airport, at most two, but usually when that's the case, they are too far apart from each other (like London with Heathrow and Luton airports). This basically means that if an airline would like to open a new route, it either lands at that airport or it doesn't. And for consumers, once they are inside, they must pay a premium for any product or service they purchase, suddenly a simple bottle of water they could get outside the airport for $1 USD jumps to $3 USD. The product is still the same, the only difference is the location.

Airlines' unavailability to have other options where to land coupled with the higher prices charged inside, give airports two important profitability levers:

- Customer Stickiness

- Higher Margins

Among the publicly traded airports, I believe PAC presents a great opportunity for long-term investors, based on the following:

Financials

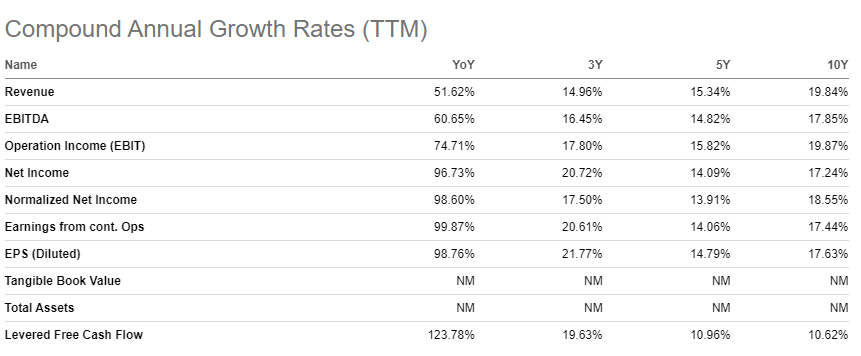

PAC has been able to grow its revenue during the last 3, 5 and 10 year at double digit figures, but more importantly, during the last 3 years, management has been focused on increasing the company´s operational leverage by a factor of 1.19 times (17.80% EBIT growth/14.96% Revenue Growth), demonstrating operational efficiencies and cost management.

{kind=link}

In its latest investor presentation, management reiterated its commitment to reaching a WACC level of 9% and keeping its Net Debt to EBITDA ratio below 3.0x; currently, it seems they´ll reach the goal.

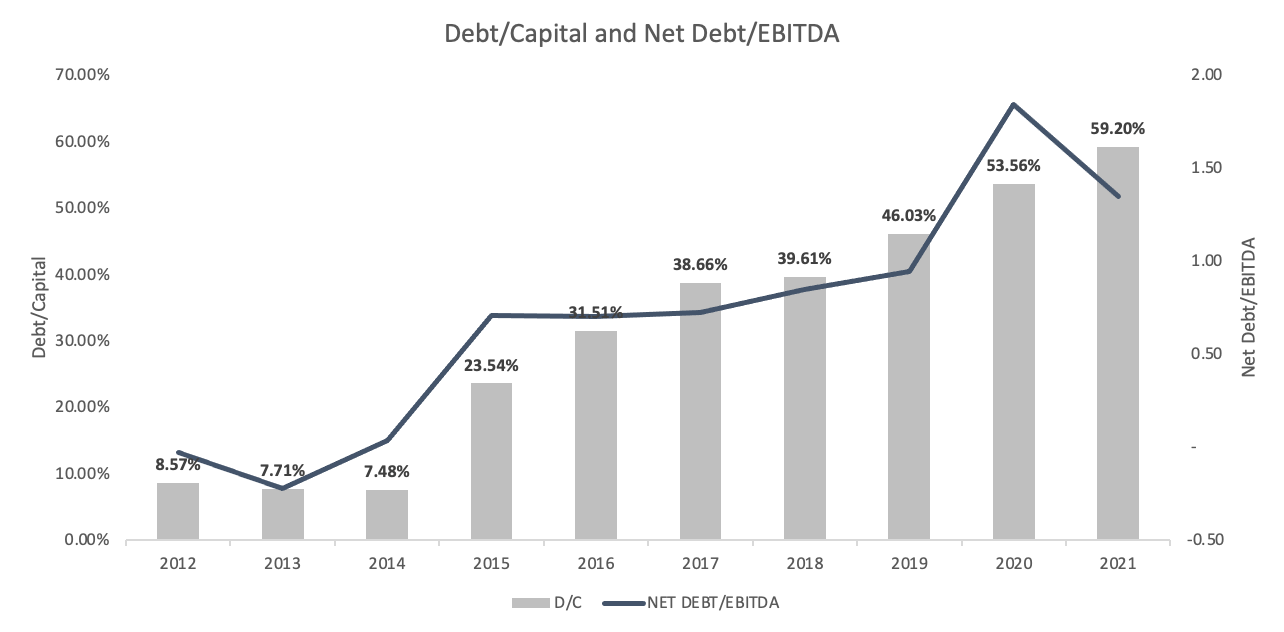

The proportion of debt in the capital structure has been rising steadily over recent years, why? Because debt is a cheaper source of financing than equity, therefore, the most efficient way of lowering the company's cost of capital. But even with greater debt, PAC still has a Net Debt to EBITDA ratio of 1.18x based on TTM data and historically the ratio has never been higher than 2.0x, despite the greater leverage in the capital structure.

Author's creation based on PAC Financial Statements

{kind=link}

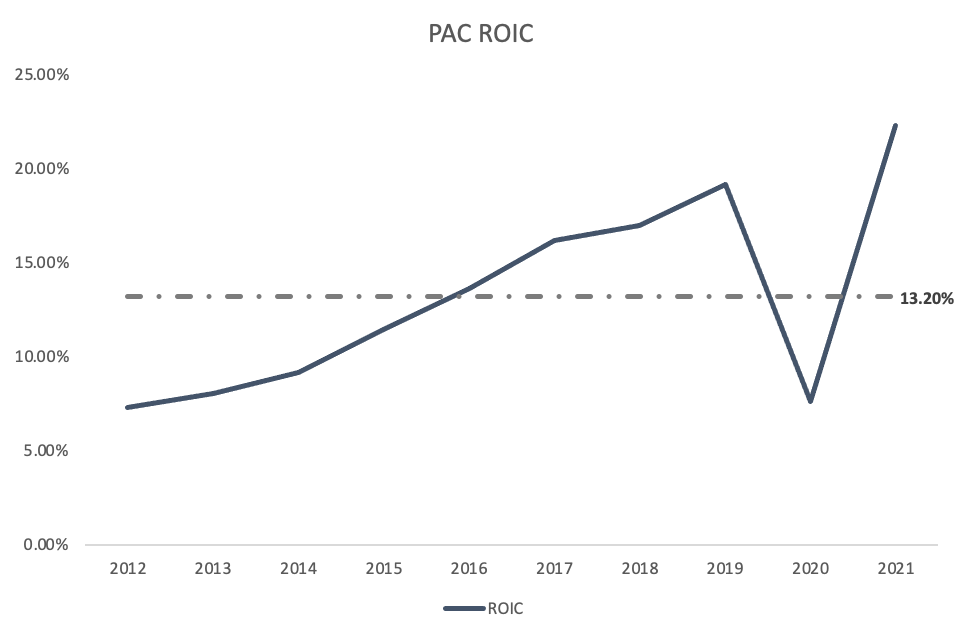

The last thing I want to dive into is PAC's profitability based on its ROIC, which can tell us a lot about the business if we divide the classic formula into two components:

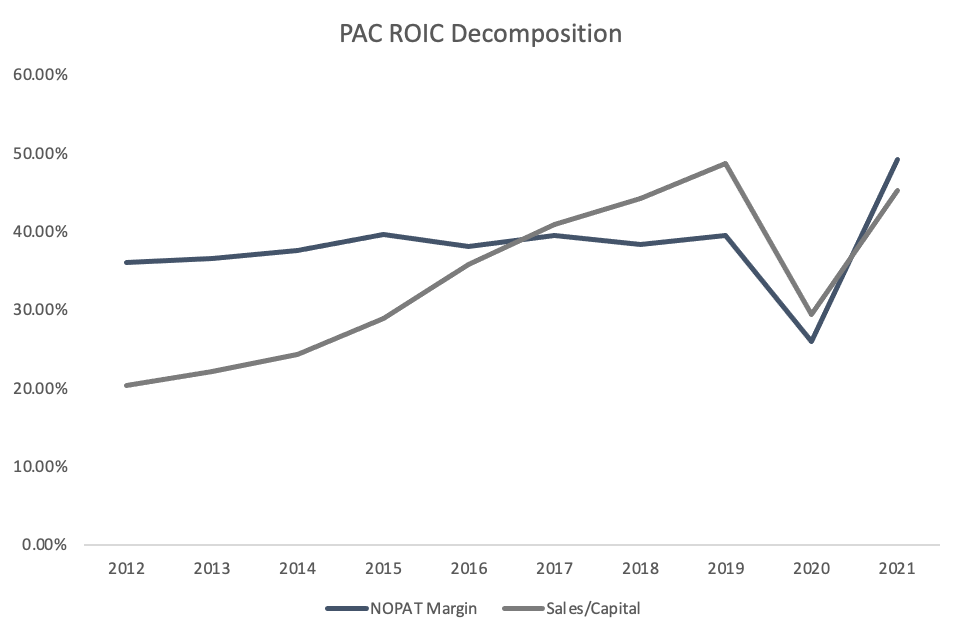

- Nopat Margin: NOPAT/Sales

- Sales to Capital: Sales/Capital

The first measure tells us how much of the sales the company is able to keep as profits, the higher the better. Usually, companies with high margins have a consumer advantage, meaning they are able to charge a premium for their products and services. PAC operates in a monopoly-type business, which has allowed it to have an average Nopat margin of 38% during the last 10 years.

The second measure tells us how much capital the company needs to invest in order to generate revenues. Therefore, it is a measure of capital efficiency. Companies that have economies of scale or a production advantage have high sales to capital ratios, as they are able to deliver products and/or services without investing too much capital. PAC does not have this type of advantage as the ratio shows an average of 0.34 over the last 10 years, but, it´s worth mentioning that the ratio has been on an uptrend, demonstrating better capital efficiencies.

If we multiply both ratios, we get the company's ROIC, and as previously mentioned, PAC's ROIC derives more from its high margin rather than from its capital use.

Over the last 10 years, the company´s ROIC has been on average 13.20% (dashed line on the graph below), but it has been steadily increasing from 7.3% in 2012 to almost 22.29% in 2021. Overall, the trend in ROIC is more important than the absolute level, as it demonstrates management's ability to keep on delivering and improving shareholder's return.

Author's creation based on PAC Financial Statements Author's creation based on PAC Financial Statements

{kind=link}

{kind=link}

Growth

We have already looked into the company's current situation, but just as important is the future outlook , and for PAC the following are expected to be drivers of return:

Passenger growth is expected to continue to be robust in the coming years as Mexican airlines plan to increase their fleet by 38% by 2027.

Most of its revenues (almost 40%) comes from passengers traveling for leisure and around 13,000 new rooms are being created in leisure destinations.

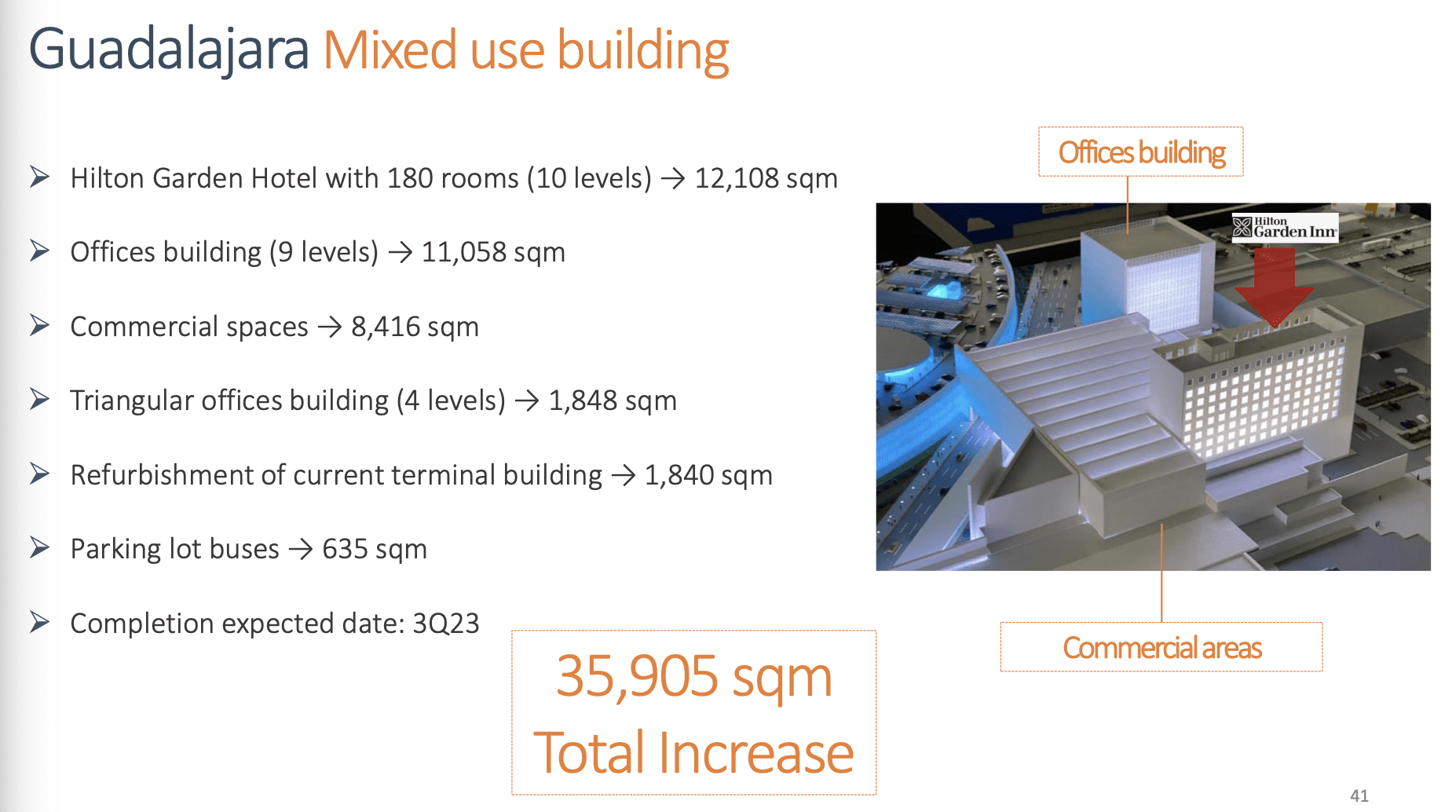

They are increasing capacity by creating a second runway at Guadalajara´s airport, their biggest airport, which served almost 15.6 million passengers in 2022. In addition to this second runaway, they are continuing to increase the size of their other main airports. In 2019, their top 3 airports had 280,000 sqm and by 2026 they are expected to have around 590,000 sqm, which represents a 13% CAGR.

Their Aeronautical revenue has grown over the last 10 years at a CAGR of 13.6%, whereas their Non-aeronautical revenues have grown at a rate of 15.4%, that's why they are committed to developing new commercial spaces, parking lots, corporate offices, hotels and VIP lounges.

Mexico is poised to benefit from the US´s manufacturing nearshoring , which should boost business-related bookings, representing almost 22% of PAC´s passengers.

The annualized number of tourists visiting Mexico has yet to recover to pre-pandemic levels, meaning there is still pent-up demand for vacation-related travels.

Mexico's middle class is estimated to represent almost 79% of the total population by 2030, in comparison to 73% in 2020.

PAC Corporate Presentation January 2023

{kind=link}

Valuation

I will now conduct a DCF Analysis using the following assumptions:

| Base Year ((TTM)) |

| Next Year |

| Years 2 - 5 |

| Years 6 -10 |

| After Year 10 |

| Revenues |

| $1,052 |

| 11.00% |

| 12.00% |

| 8.30% |

| 5.83% |

| EBIT Margin |

| 60.88% |

| 61.00% |

| 61.35% |

| 61.80% |

| 62.00% |

| Tax Rate |

| 22.30% |

| 23.07% |

| 25.00% |

| 28.46% |

| 30.00% |

| Reinvestment |

| 0.61x |

| 0.40x |

| 0.45x |

| 0.80x |

| 38.87% |

| ROIC |

| 28.79% |

| 26.17% |

| 24.93% |

| 24.92% |

| 15.00% |

| Cost of Capital |

| 11.00% |

| 10.60% |

| 10.30% |

| 9.50% |

| 9.00% |

I explain each variable below:

Revenues: Management´s guidance for the next year estimates revenue growth of 12%-14%, to be a little conservative, I am just 1% below at 11% and then forecast a 12% growth for the next 2-5 years, which is in line with historical averages and CAPEX spending should start to pay off by then. Lastly, I assume revenues will decline linearly to a terminal growth of 5.83%, based on a 10 year T-Bond of 3.5% + 2.33% (Mexico´s Adjusted Default Spread).

EBIT Margin: Going forward I don't see much improvement in margins, as PAC has the highest EBIT margin from all airports in Mexico and all planned expenditures are focused on increasing capacity rather than improving the cost structure. My assumption is that management will reach a 62% target margin by year 10 and stay like that for perpetuity.

Tax Rate: Here I just assume that by year 10 PAC will pay the statutory Mexican tax rate of 30%, therefore, the tax rate increases each year until it reaches the 30% rate.

Reinvestment: Given management's growth ambitions and currently ongoing projects, I assume that for next year the Sales to Capital Ratio falls to 0.40x (average of last 5 years) from 0.68x. For years 2-5 I estimate the ratio increases to 0.45x, as CAPEX expenditures start to be concluded (mainly Guadalajara´s new runway). Lastly, for years 6-10 I assume PAC reaches the Global Air Transport average Sales to Capital of 0.81x. For the terminal value, rather than using a ratio, I used the Sustainable Growth Rate Formula, which is Growth = ROIC* (Reinvestment Rate), I solve for the Reinvestment Rate using the known variables and I get the value of 38.87%.

ROIC: The data shown on the table comes from the model output, except for the terminal ROIC of 15%. Even though PAC has significant barriers to entries and no close substitutes, I'd rather be a little conservative and be proven wrong. Therefore, I assign a 15% value to the perpetuity ROIC, which is in line with the last 5 year average.

Cost of Capital: I estimate current WACC at 11% and then project it reaches management's cost of capital target of 9%.

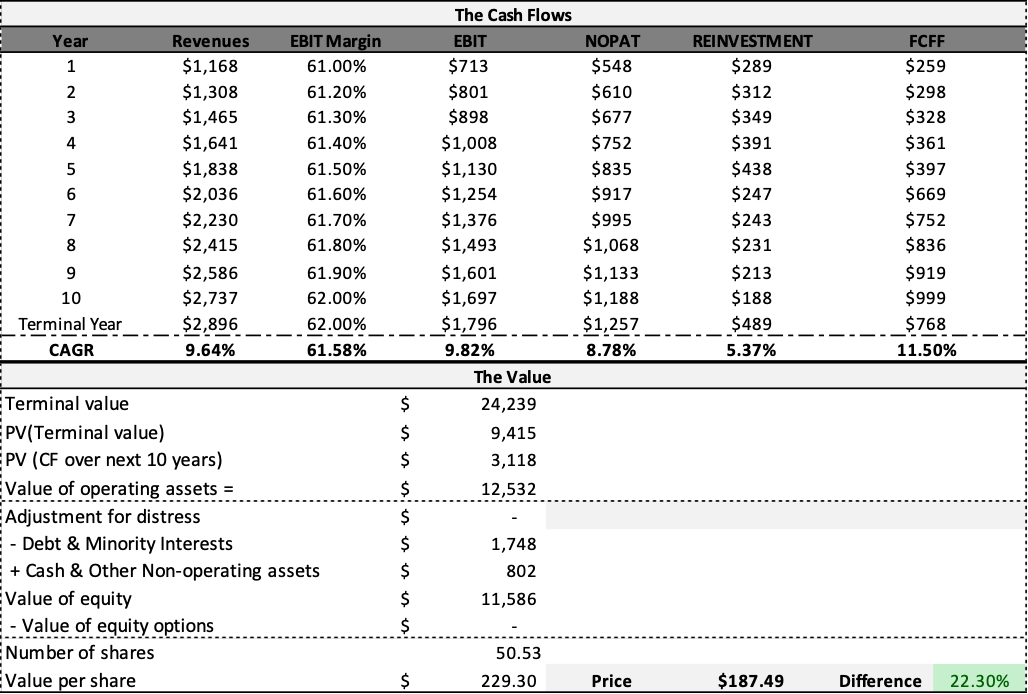

Once these inputs are thrown into the model, I obtain the following result:

{kind=link}

As the results show, at a price of $187.49 and an intrinsic value of $229.30 PAC is undervalued by almost 22%, making it an attractive investment opportunity.

However, what also caught my attention is that if you buy PAC you are getting future growth at an attractive discount, turning it into an even more enticing opportunity.

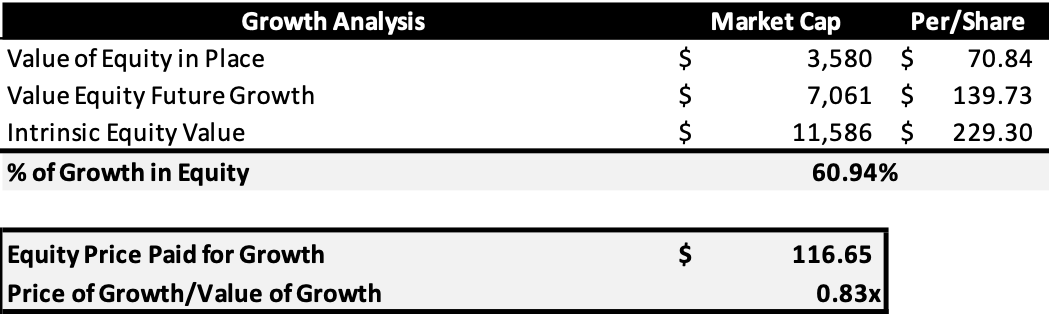

If we assume PAC stay's with its current NOPAT for perpetuity at a WACC of 11%, the value of the current assets in place should be $70.84, thus, the value added by growth should be $139.73 ($229.30 - $70.84) or better said, around 61% of the whole value derives from growth expectations. Now, at the current price of $187.49, if we subtract the value we got of $70.84 from current assets in place, we get that we are actually paying $116.65 for growth, but remember that the intrinsic value of growth we got is $139.73, therefore, if we divide the current price of growth from the actual value of growth we get a ratio of 0.83x, which means that we are just paying 83 cents for each dollar of future growth.

{kind=link}

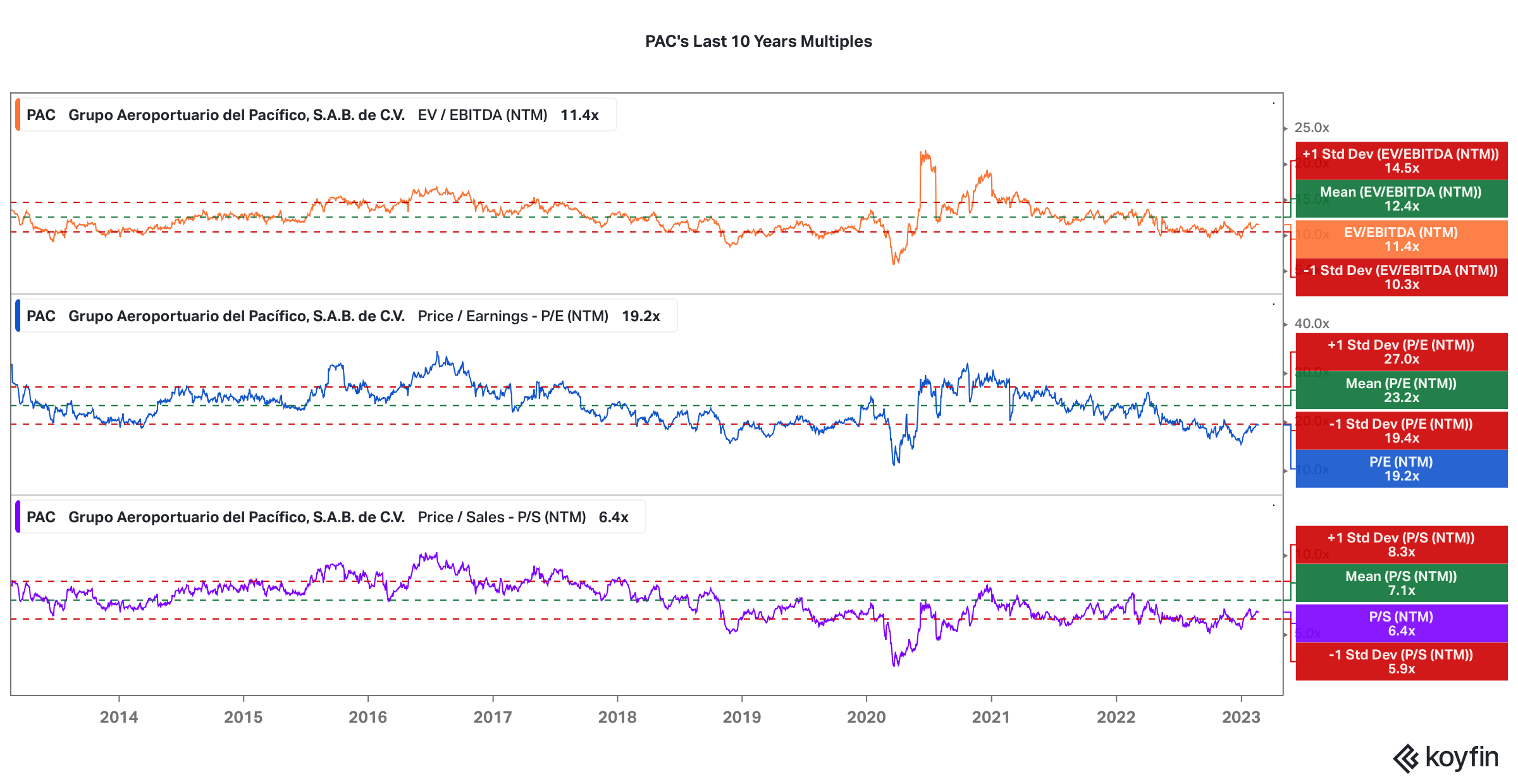

Lastly, to confirm my last valuations, I wanted to conduct a simple multiple analysis by looking at the 10 year average of the EV/EBITDA, P/E and P/S ratios on a NTM basis and see how they compare with the current value of the multiple. The results show that for all metrics, the current multiple is below its 10 year average (dotted green line) and both the P/E and P/S ratios are close to 1 standard deviation below that average. This further confirms that PAC is indeed an attractive opportunity

{kind=link}

Risks

Although PAC looks like an attractive opportunity, the following risks may prevent it from reaching its full value:

Customer Concentration: 43% of its revenue comes from Volaris airline, should something happen to the carrier, PAC's profitability could be impaired.

Political Risk: Mexico will hold presidential elections in 2024 and should the market see the future candidate as a danger to Mexico's stability, the stock could have some volatility.

Remote Work Policies: Almost 22% of PAC's revenues come from business-related travels, should the tendency to work online increase, revenues could suffer.

Economic Contraction: Traveling is a disposable expense, when money is tight people and businesses postpone all kinds of travel. The current macro environment forecasts a slight recession, however, if it turns out to be worse than expected, profits could slow down drastically.

Conclusion

PAC is an attractive investment opportunity for investors that value managers that focus on improving returns on invested capital and maximizing the value of the shares by smart capital allocation. But not only is PAC a well-managed firm, it operates in an industry that provides a natural shield against competitors, allowing it to charge premium prices.

Lastly, Mexico looks like a clear winner from the new trend of "regionalization" thanks to its proximity to the United States, stable fiscal policy and balance of payment, young and cheap workforce, natural resources and a growing middle class, all of which should benefit PAC and the airport industry as a whole.

For further details see:

Grupo Aeroportuario Del Pacifico: A Story Of High ROIC And Growth