GGAL - Grupo Galicia: Synergy Between Traditional Banking And Digital Transformation

2023-09-11 12:56:53 ET

Summary

- Digital banking is simultaneously a challenge and an opportunity for traditional banks. Brazil is the leader in digital banking in LATAM, but Argentina is advancing quickly.

- Grupo Galicia is the second-largest bank in Argentina. The company offers a wide range of services. Among them is Naranja X, the third most popular digital banking app in Argentina.

- Grupo Galicia`s balance sheet is well diversified on both sides. The bank efficiently manages maturity transformation between loans and deposits.

- I give a buy rating despite the company being overvalued compared to its peers and measured with Excess Returns due to its strong performance and macro tailwinds.

Thesis

Grupo Financiero Galicia (GGAL) is one of the largest traditional banks in Argentina. Besides that, it is the best positioned among its peers to capitalize on the ongoing digital banking transformation. The company covers all banking aspects through its subsidiaries, including digital banking. Naranja X is the third to Mercado Pago and BNA+ banking apps.

Mercado Pago is owned by Mercado Libre ( MELI ) and Banco de la Nacion owns BNA+. The former is LATAM's leading e-commerce platform, while the latter is the biggest bank in Argentina. As the name suggests, Banco de la Nacion is a state enterprise. Gruppo Galicia is the sole traditional bank with a strong presence in digital services. Banco Macro ( BMA ) lags significantly behind. However, Banco BBVA Argentina ( BBAR ) is advancing.

Apart from traditional and digital banking, Grupo Galicia manages insurance, securities, and investment subsidiaries. The company has a solid standing due to its neat balance sheet compositions, providing risk mitigation.

I give a buy rating due to my solid digital presence, efficient risk management, and diversified services.

LATAM and digital banking

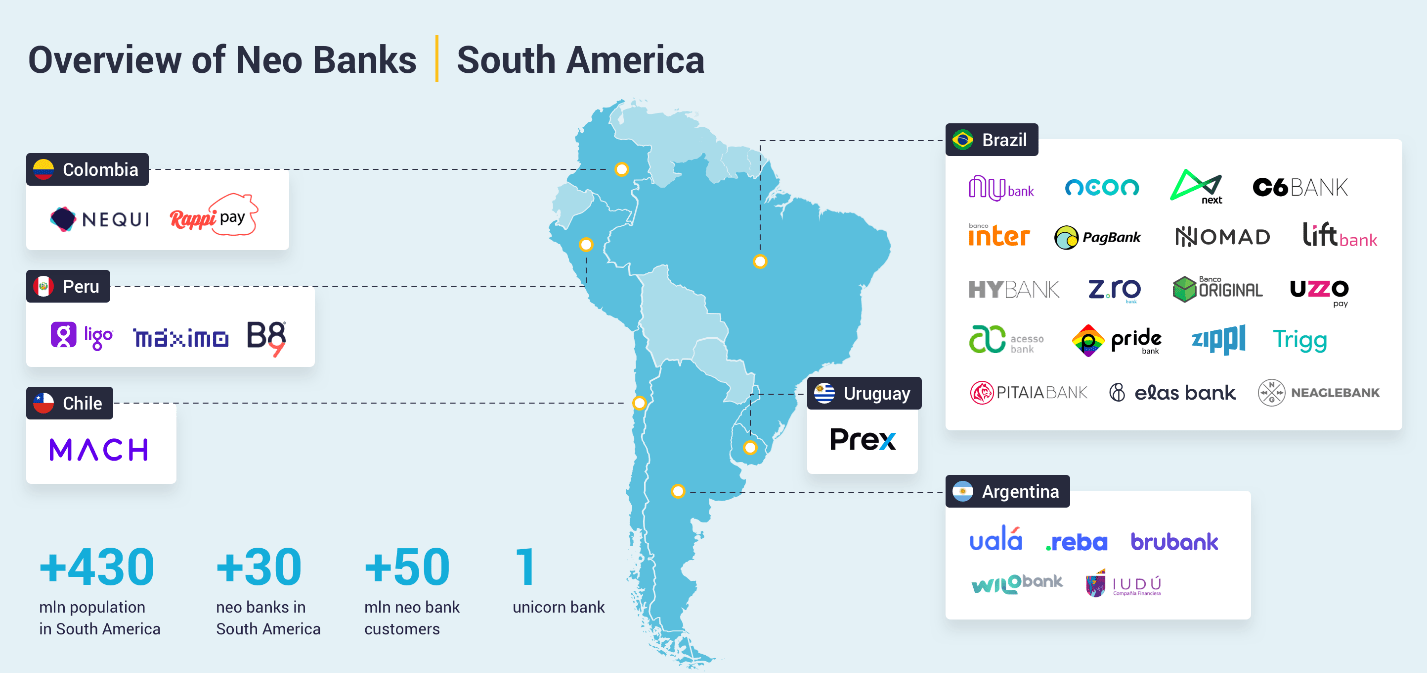

Neonbanks are the bridge between traditional banking and digital services. The largest neobank in the world is NU Holdings ( NU ). The image below shows the major players in the LATAM fintech industry:

{kind=link}

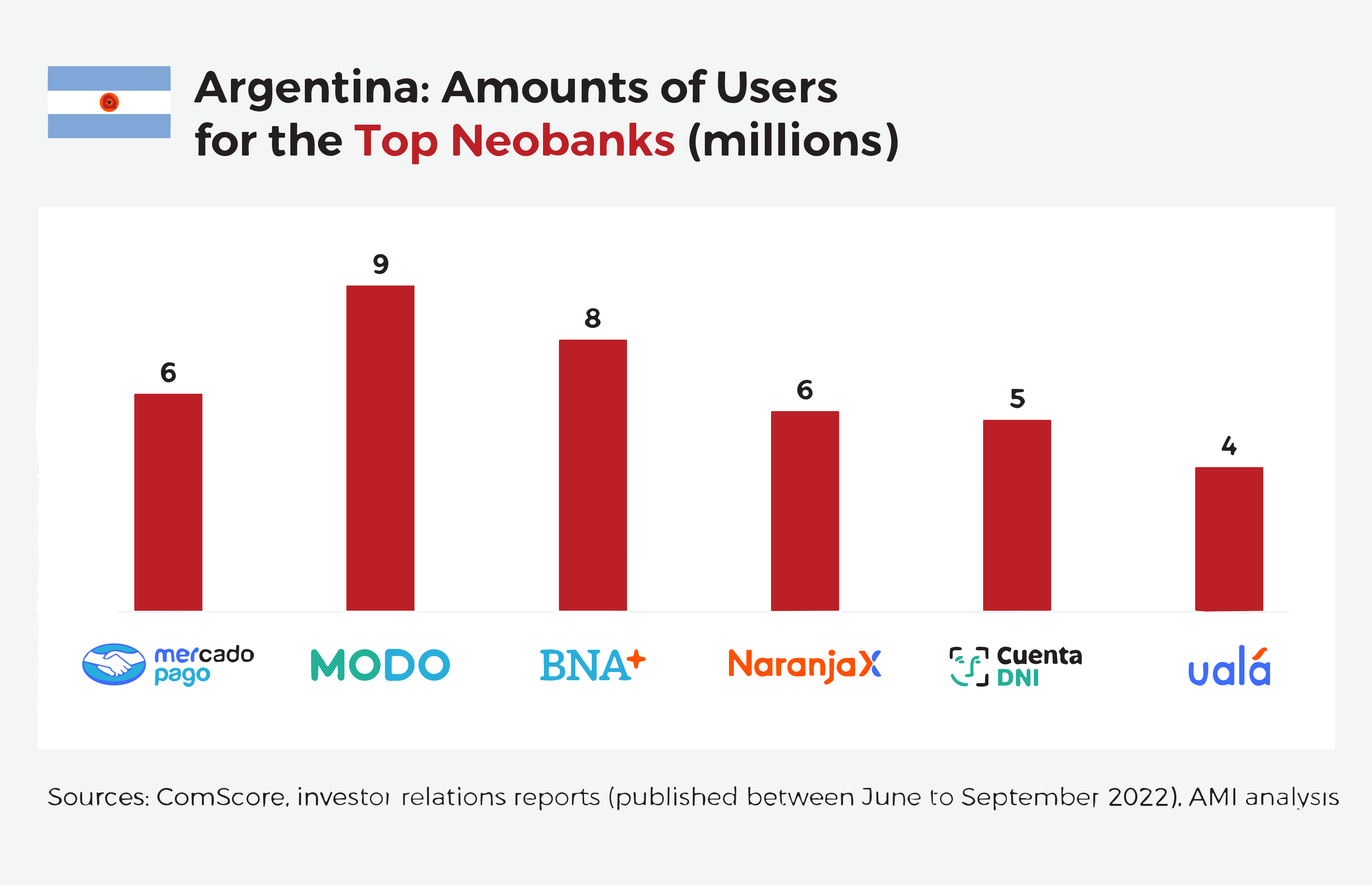

Brazil leads the pack with the highest number of fintech companies in LATAM. All other countries are lagging significantly. From an entrepreneur’s standpoint, this represents unserved demand; from an investor`s view, it means new growth investments. The traditional banks in the region are facing fierce competition in the face of the neobanks. Some of them are more adaptive than others. Argentina has a competitive landscape for digital banking services, as seen in the image below:

{kind=link}

The leader is Mercado Pago, a subsidiary of Mercado Libre. Among the competitors is Naranja X. It is a subsidiary of Grupo Galicia, one of the largest Argentinean banks. Naranja`s app is second in downloads next to Mercado Pago. This is an excellent example of how traditional banks can succeed in digital transformation. Compared to the other large Argentinean banks, GGAL is the best performer due to Naranja X's performance.

Company Overview

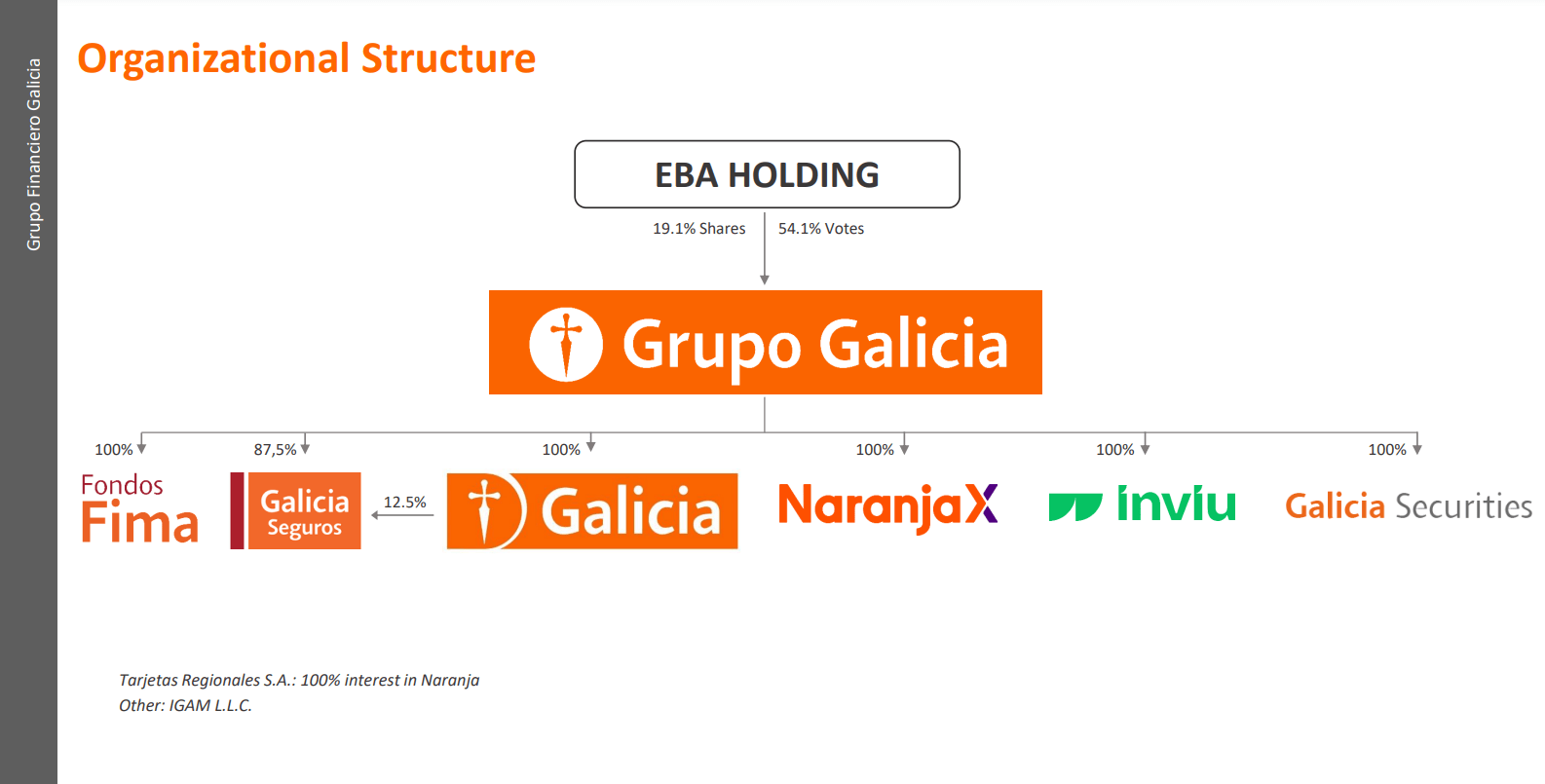

Grupo Galicia is the second-largest traditional bank in Argentina. It offers a wide range of services through its subsidiaries. The image below from the last company presentation illustrates the corporate structure:

{kind=link}

Banco Galicia, Fondos Firma, Galicia Seguros, and Naranja X are the primary revenue generators.

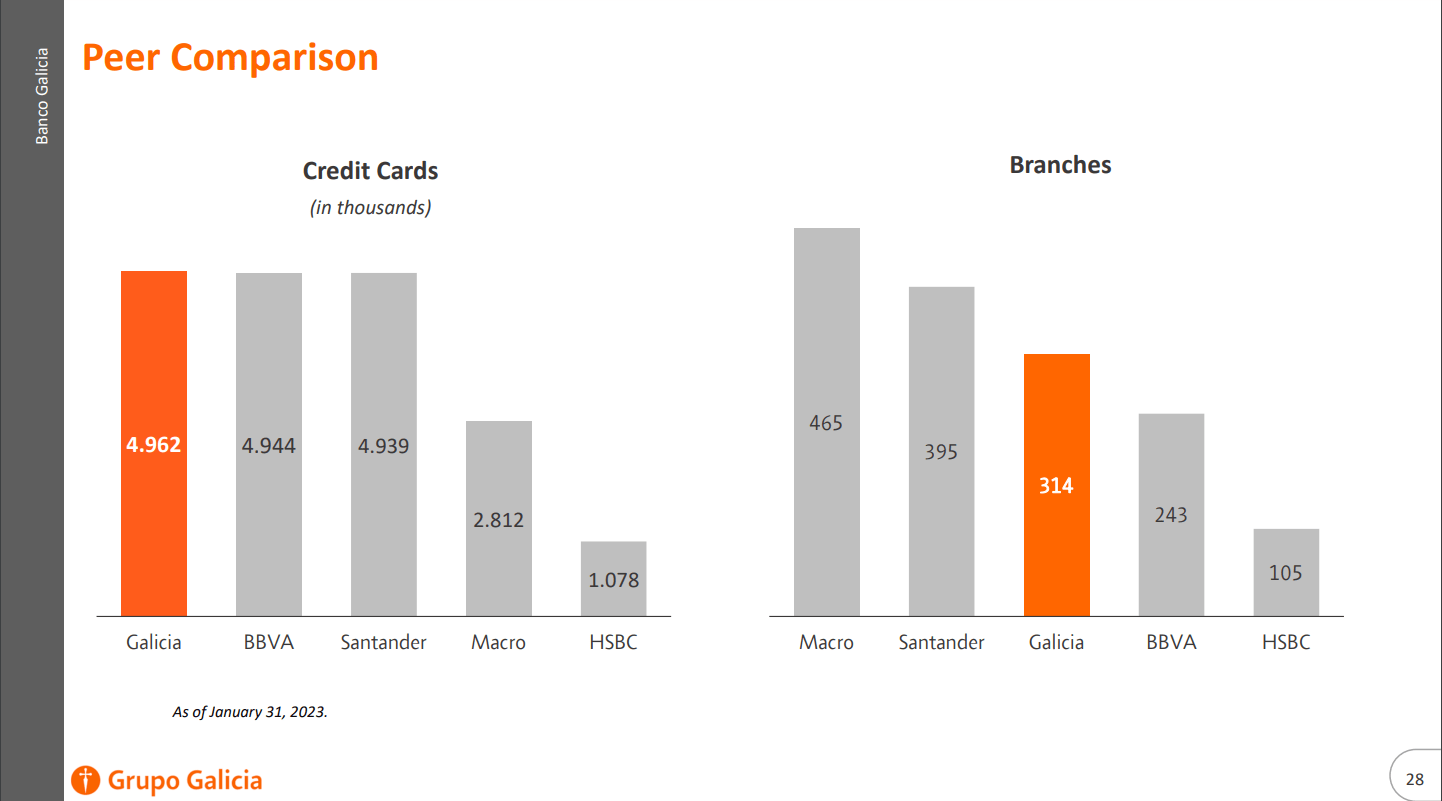

The chart below from the last company presentation shows Grupo Galicia and its peers:

{kind=link}

GGAL is the largest credit card issuer in Argentina. Its physical network has 314 branches, third to Banco Macro ( BMA ) and Santander. Like Banco BBVA, GGAL seeks expansion for its digital services instead of maintaining an extensive branch network. GGAL is the largest bank next to the state enterprise Banco Nacion. It takes a lead to the following bank with more than 10 % on the loans.

In the following paragraphs, I will briefly review GGAL subsidiaries. The first to analyze is Banco Galicia.

Banco Galicia

The balance sheet structure is similar to the other large Argentinean banks. Below is shown Banco Galicia's balance sheet structure.

| Asset ratios: assets structure |

| Cash/Total Assets |

| 15 % |

| Loans (Net Financing)/Total Assets |

| 34 % |

| Central Bank Exposure/Total Assets |

| 28 % |

| Government Exposure/Total Assets |

| 12 % |

| Liability ratios: capital structure |

| Deposits/ Total Liabilities |

| 69 % |

| Other liabilities/ Total Liabilities |

| 6 % |

| Company bonds/ Total Liabilities |

| 2 % |

| Equity/ Total Liabilities + Equity |

| 17 % |

| Solvency ratios: |

| Loans (inc., Credit Cards) /Deposits |

| 49 % |

| Cash/Deposits |

| 18 % |

| Borrowings (inc. bonds)/ Total Assets |

| 8 % |

For every deposited currency unit, the banks own as cash reserves 0.18 units. Such a ratio is very similar to the US. Compared to the other Argentinean banks, it touches the average. The other metrics are close to the country`s average, too.

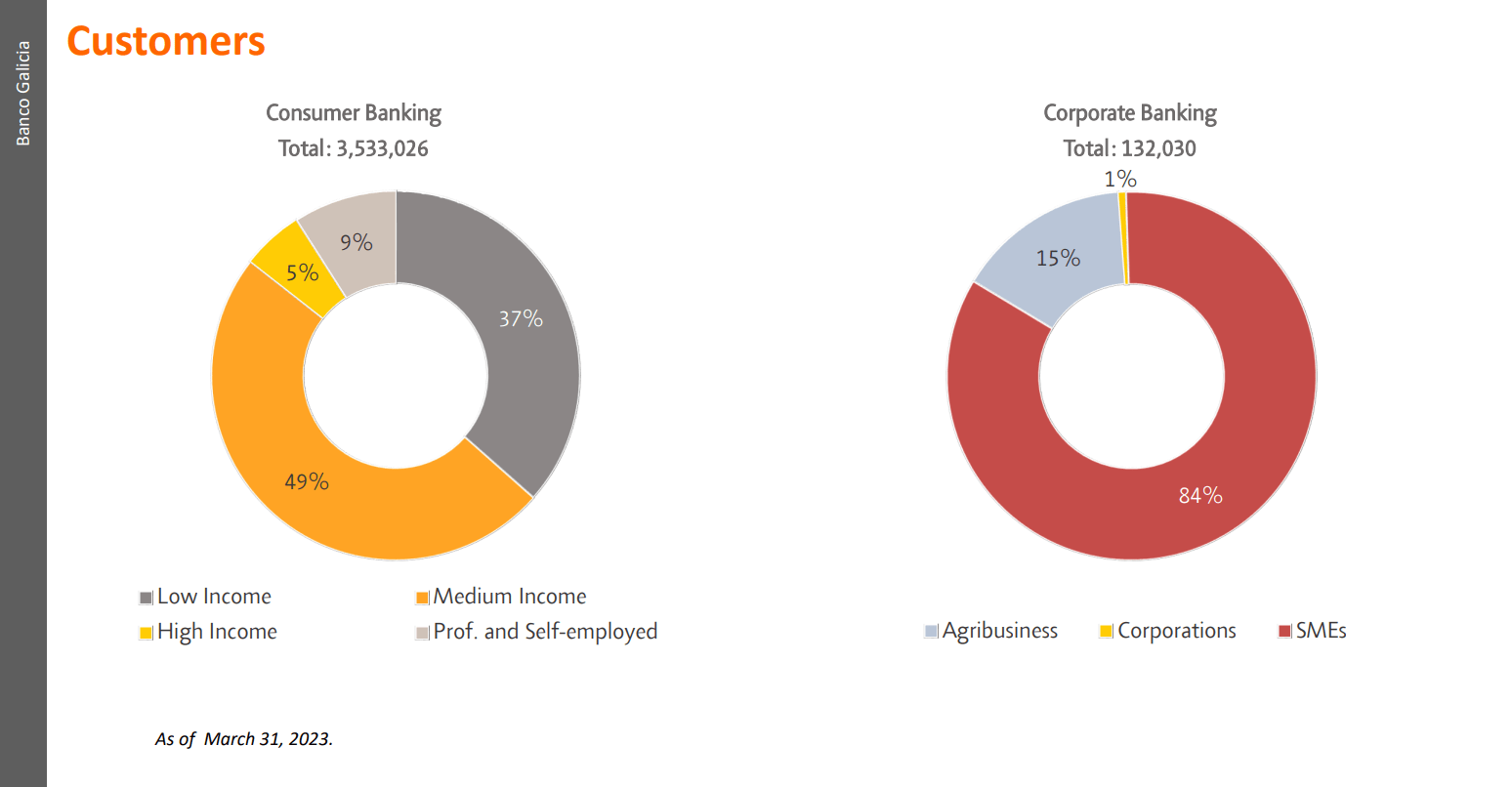

Consumer banking is focused on low- and medium-income consumers. Both represent 86 % of total clients. Business banking is focused on Small to Medium Enterprises ((SME)) at 84 % and agribusiness at 15 %.

{kind=link}

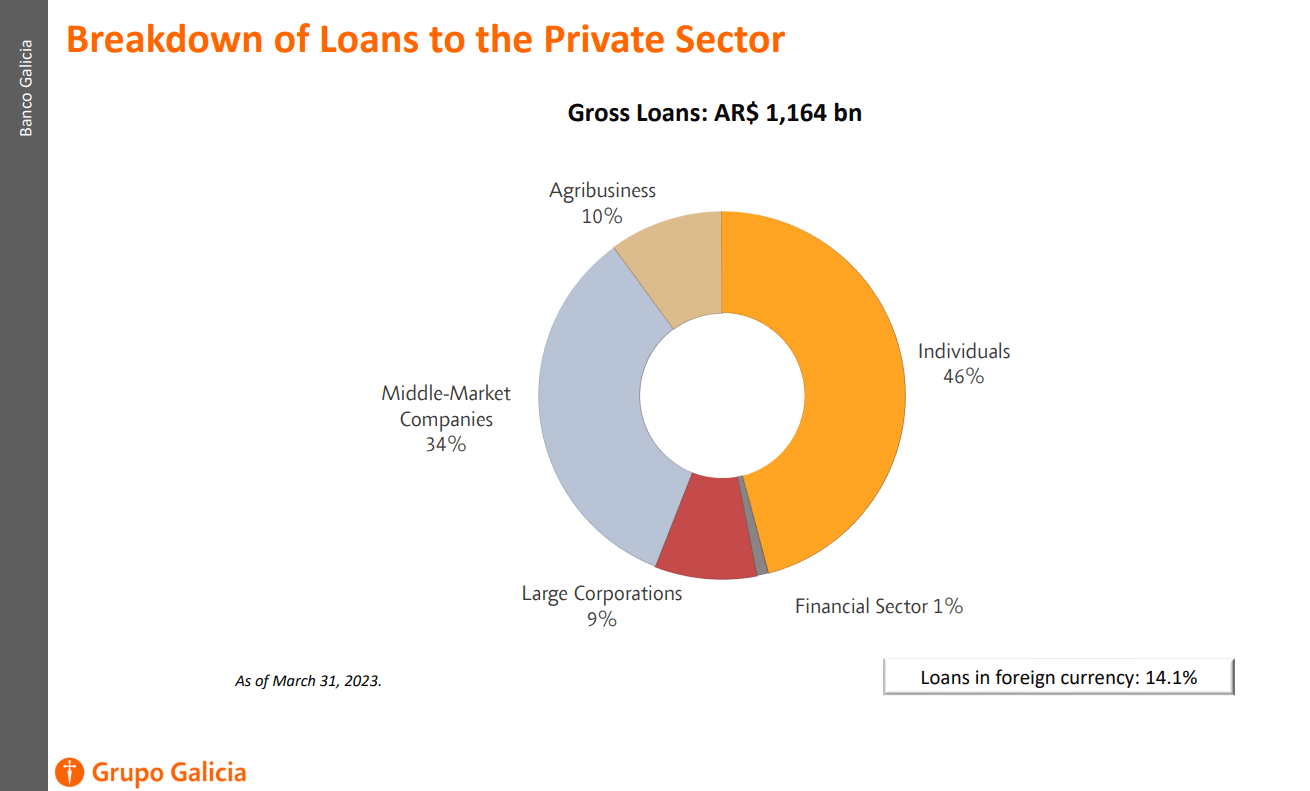

Agriculture is a huge part of the country's GDP. 15 % is a safe exposure to the sector known for its uncertainties. For example, due to severe droughts, soy yield dropped by 50 % last year. Years of poor production expose agribusiness lenders to high liquidity risks, hence, the bank credit risk. Such massive production drops inevitably affect the company`s bottom line and ability to service its debts. Banco Galicia's loan portfolio composition is illustrated below:

{kind=link}

Loans maturity is dominated by 1 to 6 and 6 to 12 months. Loans in USD represent 14.1 % of the total. The agribusiness loans represent 10 % of the total loan portfolio.

Below is shown the structure of Banco Galicia's liabilities.

{kind=link}

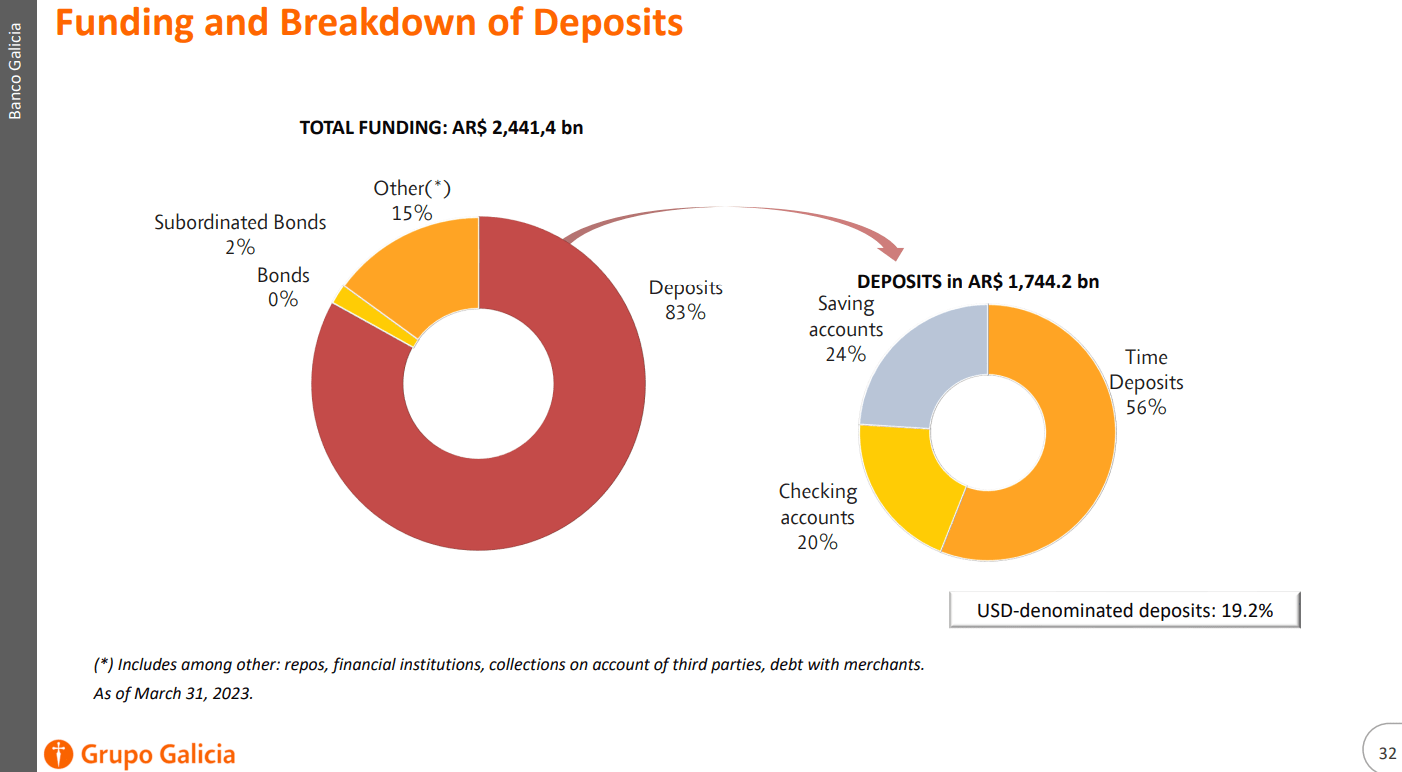

83 % of banks` funding originates from clients` deposits. They are well diversified with an accent on time deposits and saving accounts. The former equates to 56 % of total deposits. That said, Banco Galicia management is doing a great job using maturity transformation. Banks` NPL ratio is below Argentina`s average of 3 %. Since the pandemic's peak, the bank`s NPL has been steady despite the worsening economic conditions.

Naranja X

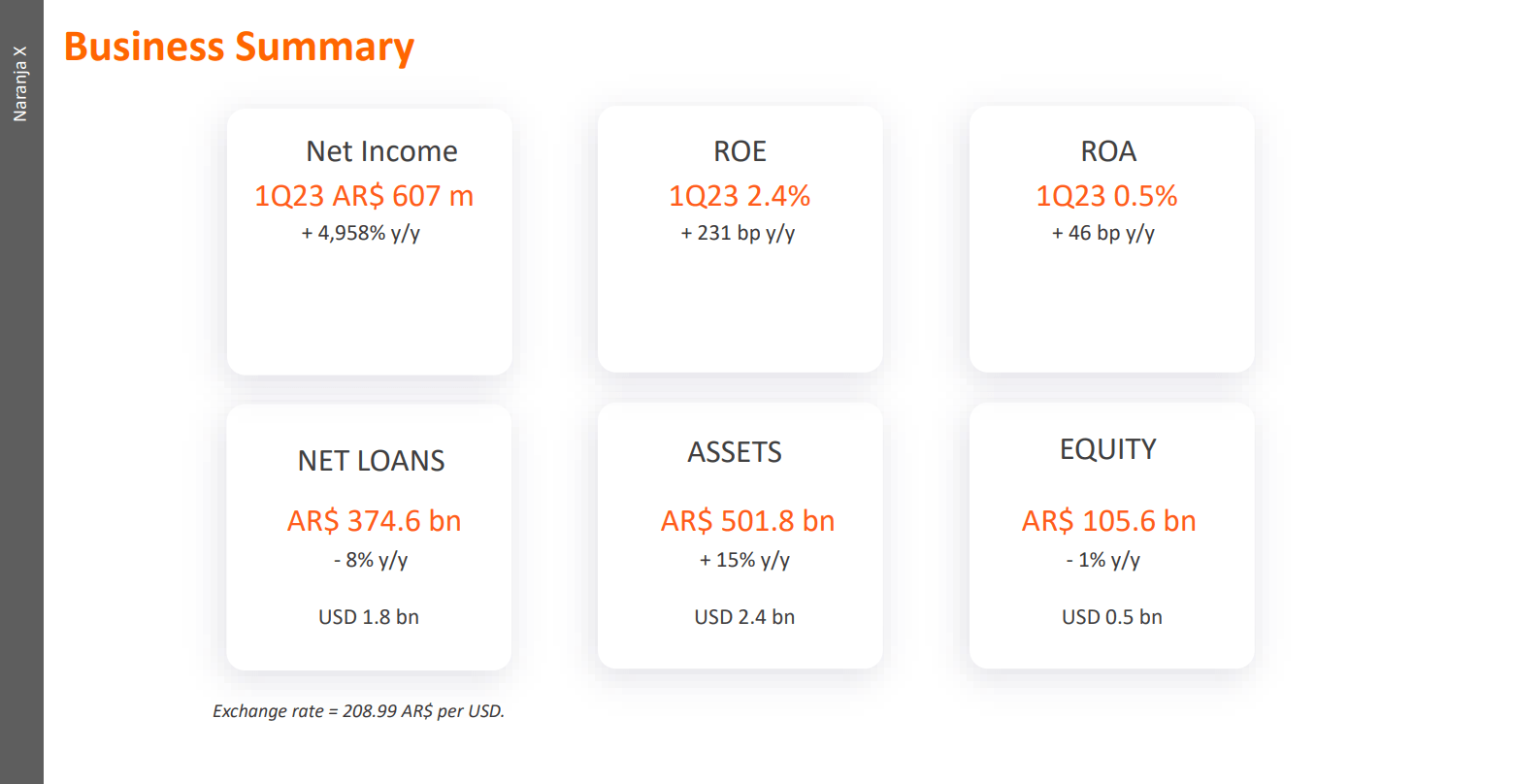

Naranja X is the largest credit card issuer in Argentina. Its performance is shown on the chart below:

{kind=link}

The net income has grown with impressive figures. However, those results are caused by runaway inflation and peso devaluation. A better metric is the ROE because it includes the company`s equity in the denominator. The latter reflects inflation and currency devaluation. A positive sign is asset growth, regardless of the decline in lending activities. In such a case, more people borrow money from the bank, i.e., Naranja attracts more deposits.

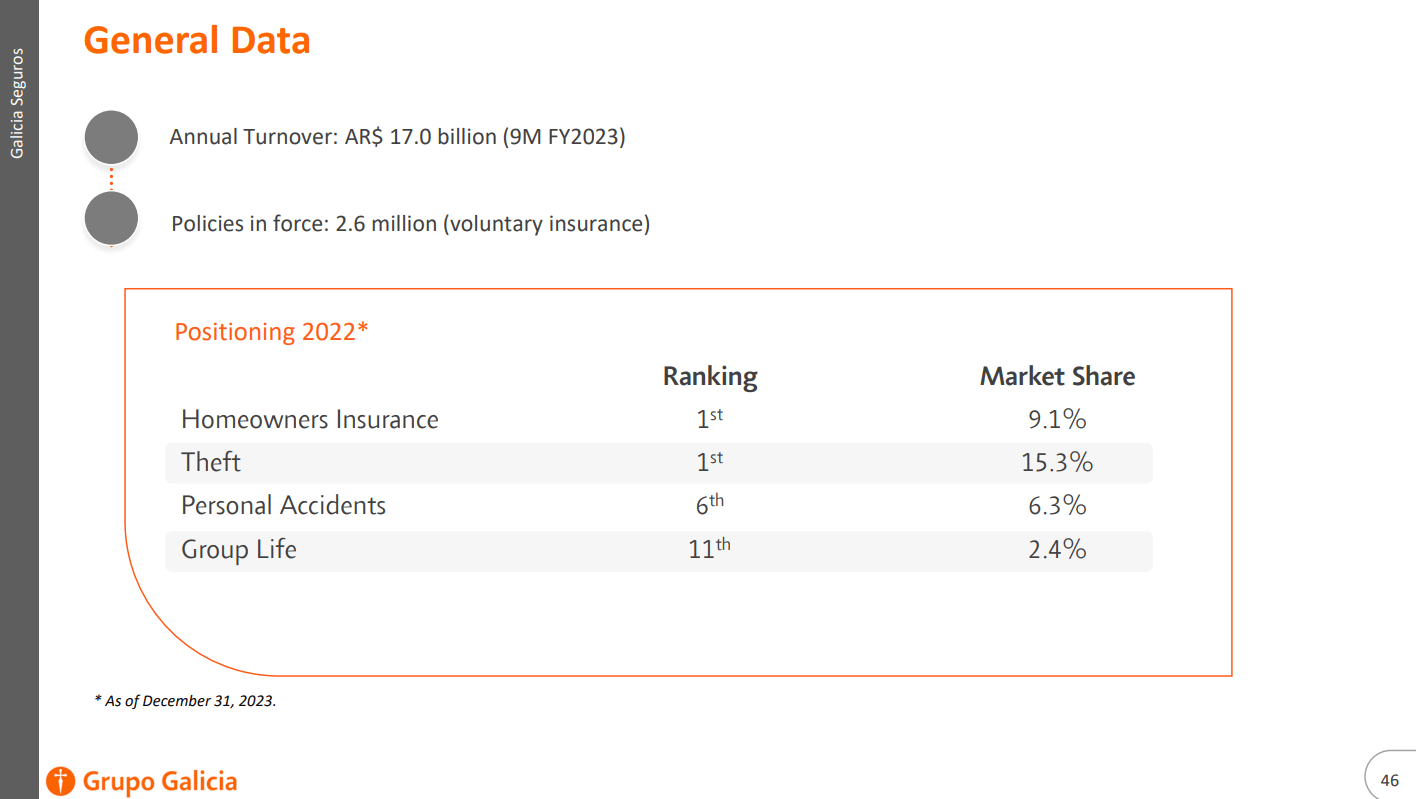

Galicia Seguros

Galicia Seguros is the insurance branch of GGAL. It is among the leaders in the industry in Argentina. The image below shows Galicia Seguro's positioning:

{kind=link}

It is number one in homeowners insurance and theft insurance while sixth in personal accidents.

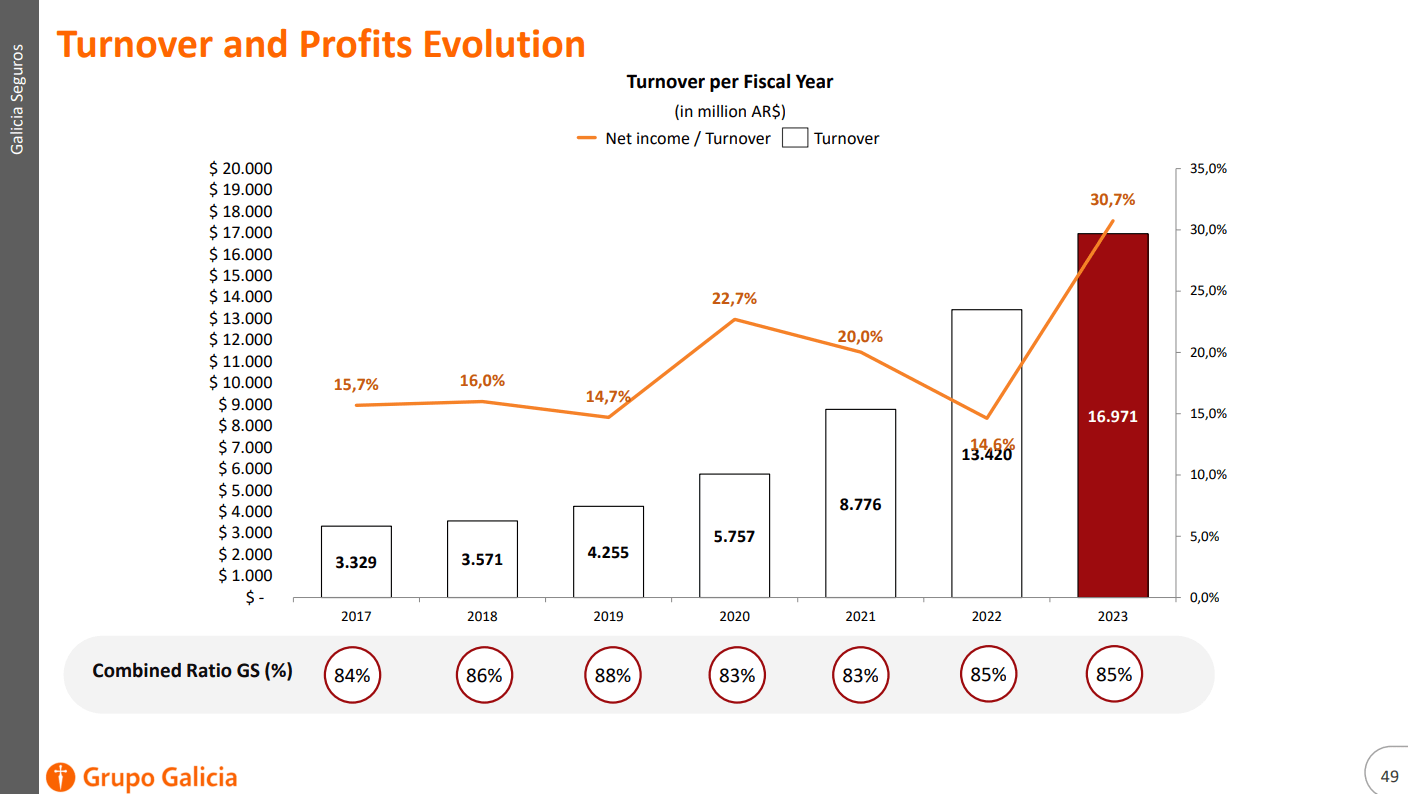

As an insurance company, Galicia Seguros underwrites policies with the expectation that a minor part of the claims will be paid in the future. In other words, the insurance company is put option seller who collects option premiums but periodically experiences significant losses. The latter represents payments on customers' claims. We use the Combined Ratio to measure an insurance company's profitability. In the nominator, we have incurred losses and expenses; in the denominator, we have earned premiums.

The image below shows Grupo Seguro's performance:

{kind=link}

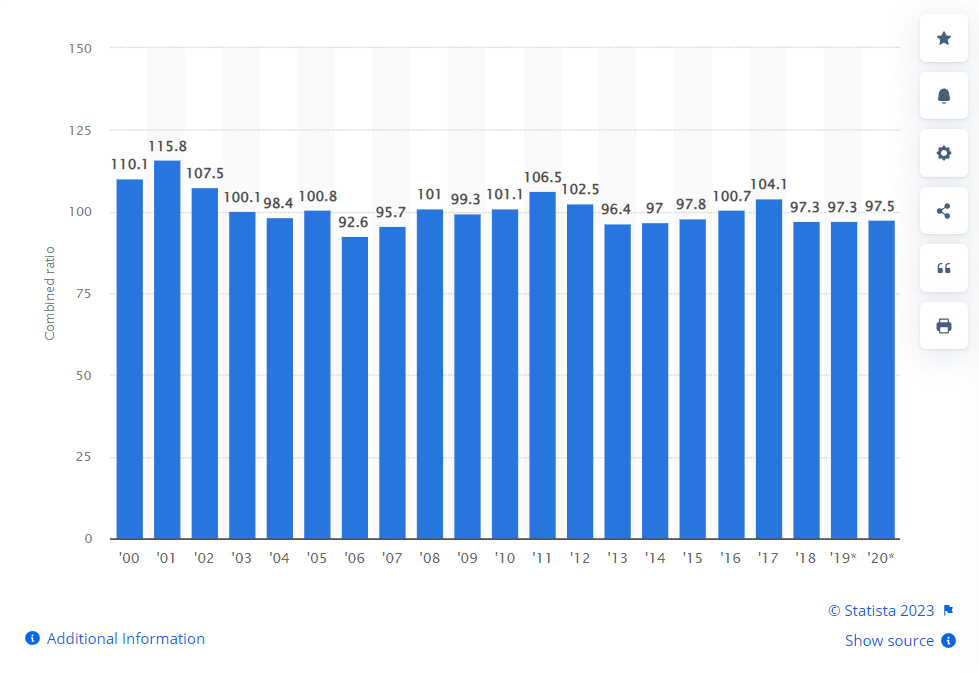

If the ratio is lower than 100 %, the company is profitable, and vice versa; if it exceeds 100 %, the business loses money. Being below 90 % for the last five years is a remarkable achievement. To understand why, I will compare those numbers with US insurance data. I share a table from Statista .

{kind=link}

The chart represents the combined ratio for property and casualty insurance industry in the United States from 2000 to 2022. The combined ratio has been well above 90 % and occasionally exceeded 100 %.

Grupo Seguros operates in segments with high demand, such as theft and personal accidents. I expect the company's policies' customer base to grow due to the vast branch network shared with Naranja X and Banco Galicia.

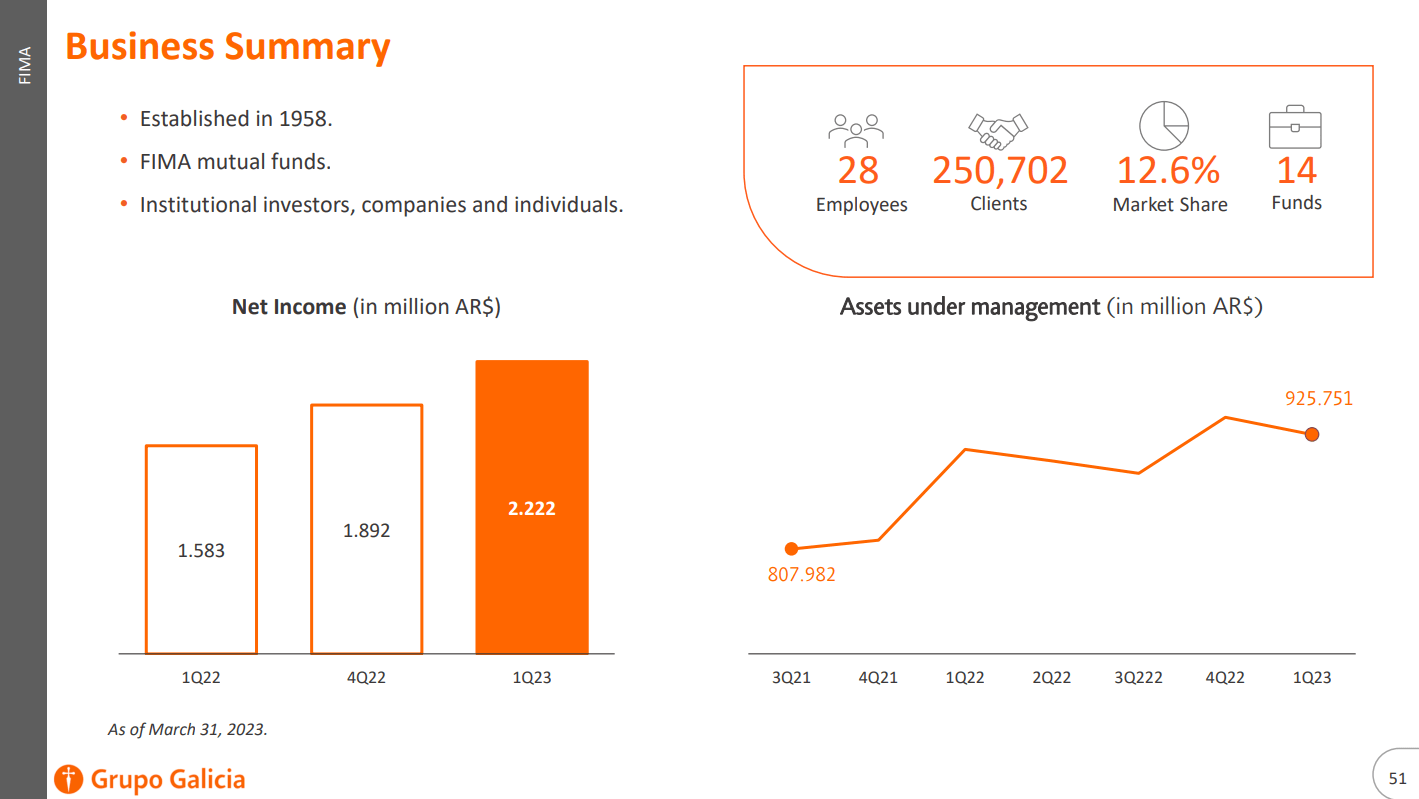

Fondos Firma

Fondos Firma is the investment management branch of Grupo Galicia. The company serves institutional, corporate, and individual clients. The chart below gives a quick overview of the company:

{kind=link}

The most important metric for every mutual fund is AUM growth because the fund`s revenue derives from AUM-based fees. The latter grow proportionally with AUM. Fondos Firma has 12.6 % of the market share and has increased its AUM by 14 % over the last two years. As mentioned, that reflects higher revenues and net income.

To summarize, I like GGAL's fully diverse portfolio of services. The company`s is among the top performers in every activity. On top of that, it efficiently cross-sell its products between its subsidiaries. The largest branch network gives an undisputable advantage.

Company Financials

Grupo Galicia's balance sheet is very healthy considering Argentinean economic peculiarities. The table below shows consolidated balance sheet metrics for Grupo Galicia. The data is from the last company report, Q2 2023 .

| Asset ratios: assets structure |

| Cash/Total Assets |

| 11.2 % |

| Credit Cards/Total Assets |

| 14 % |

| Loans (ex., Credit cards)/Total Assets |

| 24 % |

| Bonds/Total Assets |

| 30 % |

| Liability ratios: capital structure |

| Deposits/ Total Liabilities |

| 83 % |

| Other liabilities/ Total Liabilities |

| 15 % |

| Company bonds/ Total Liabilities |

| 2 % |

| Equity/ Total Liabilities + Equity |

| 18 % |

| Solvency ratios: |

| Credit Cards Receivables /Deposits |

| 21 % |

| Loans (inc., Credit Cards) /Deposits |

| 61 % |

| Cash/Deposits |

| 18 % |

| Borrowings (inc. bonds)/ Total Assets |

| 4.2 % |

The data below shows Grupo Galicia Basel III ratios. The inputs are taken from the last financial report .

| Capital (in millions AR pesos): |

| Regulatory Capital |

| 587,380 |

| Tier 1 capital |

| 442,495 |

| Common equity tier 1 ((CET1)) |

| 411,495 |

| Risk-Weighted Assets |

| 1,870,089 |

| Basel III Ratios: |

| Regulatory capital ratio (Capital adequacy ratio) |

| 31 % |

| Tier 1 ratio |

| 23 % |

| CET1 ratio |

| 21.9 % |

GGAL and the other traditional banks in Argentina perform well on all risk metrics. Considering the dire economic conditions, adequate liquidity is paramount for a bank`s survival.

The profitability, too, is average. In the long term, I expect GGAL to convert its rising customer base into profit growth. Naranja X is a strong contender to lift the company`s performance in the future. The table below illustrates GGAL's profitability. The data is from GGAL's last financial report .

| ROE |

| 15.5 % |

| RoTE |

| 17.7 % |

| RoCET 1 |

| 19.0 % |

| ROA |

| 3.9 % |

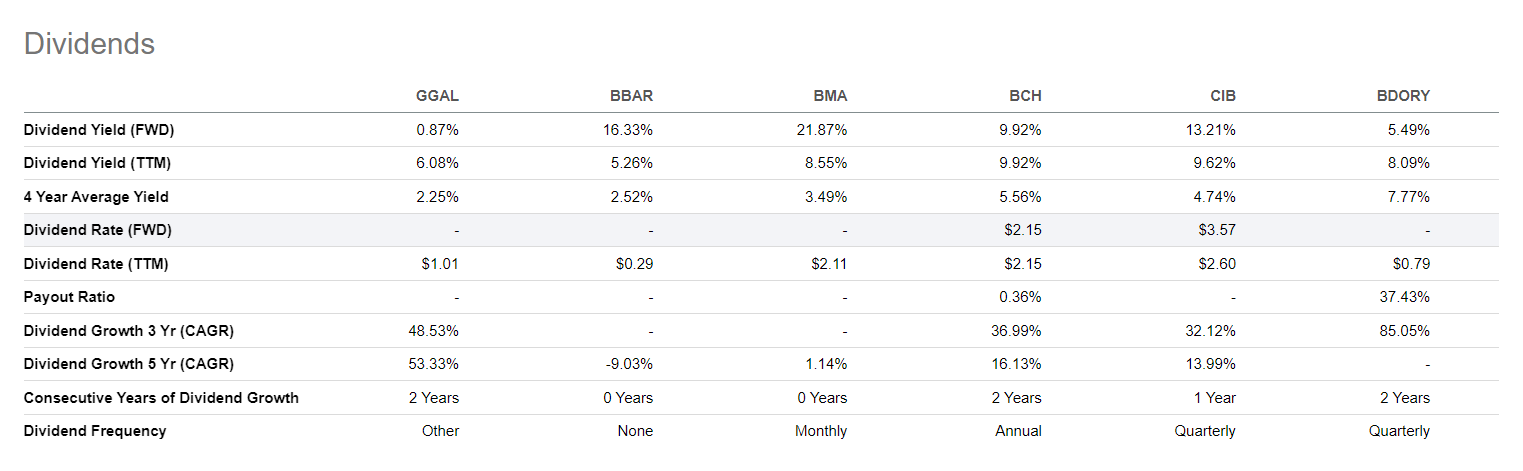

GGAL distributes dividends. The yields are slightly below the average for the region. The image below compares GGAL's dividend policy against its similar type banks in Argentina and LATAM.

{kind=link}

Company Valuation

For the valuation of GGAL, I use the Excess Return Model. I do follow Professor Damodaran's framework and its database .

Assumptions and inputs:

- Risk-free rate equals the 5Y average of USA long-term Government bond Rate, 2.2%.

- Growth rate, g, equals the 5Y average of the USA long-term Government bond Rate, 2.2%.

- Argentina's equity risk premium is 23.21 %.

- GGAL's book value per share is $ 2.36 (Sept 10, 2023).

- Banks' unlevered Beta 0.41.

- GGAL Debt/Equity ratio 23 %.

- Argentina's effective tax rate is 35 %.

- GGAL ROE ((TTM)) 16.89 %

1. Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E).

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk-Free Rate + (Levered Beta * Equity Risk Premium).

3. Calculate Excess Returns using GGAL's ROE, Book Value, and Cost of Equity:

Excess equity return = = (Stable Return on equity - Cost of equity) x (Book Value of Equity per share).

4. Calculate Excess Returns Terminal Value assuming perpetual constant growth and stable cost of equity:

Excess Returns Terminal Value = = Excess Returns / (Cost of Equity - Expected Growth Rate).

6. Calculate the Value of Equity.

Value of Equity = Book Value per share + Terminal Value of Excess Returns.

For GGAL, I get the following results:

Terminal Value of Excess Returns Per Share = $ 2.24

Intrinsic value per share = $ 4.6

Current market price = $ 15.86 (Sept 10, 2023)

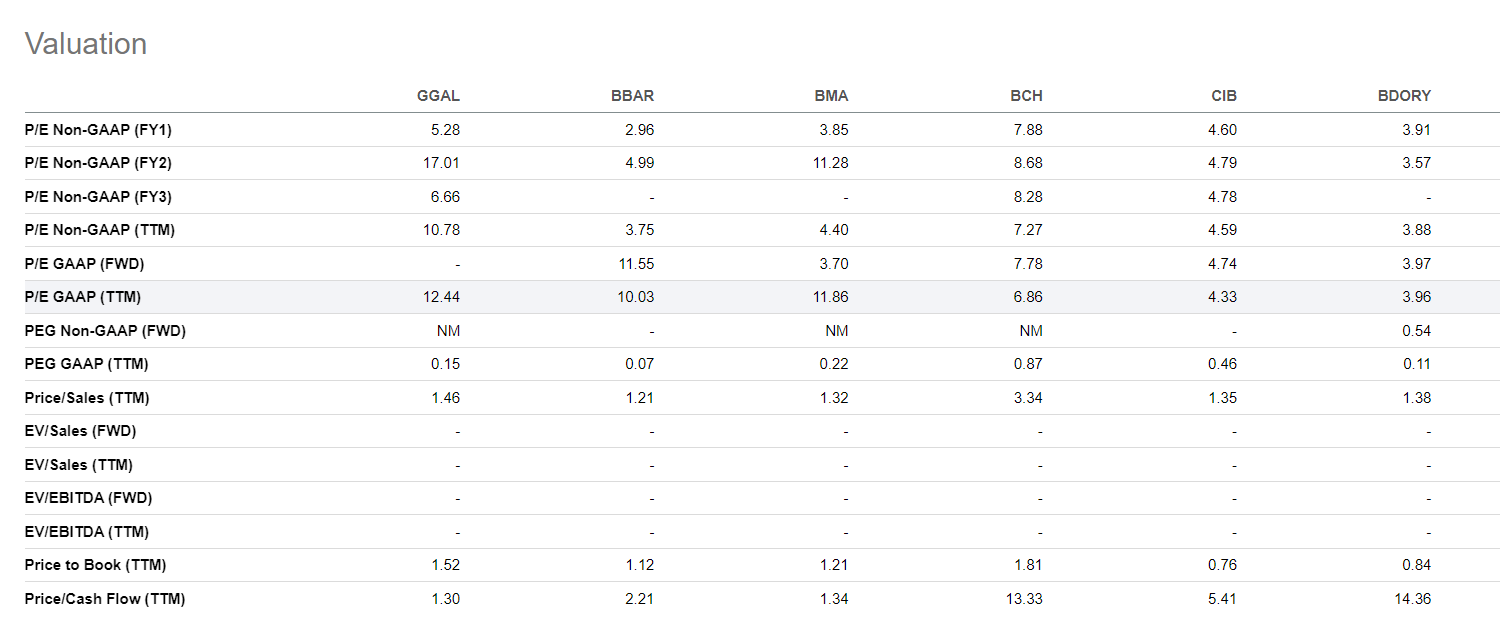

The chart below compares GGAL with other large banks in LATAM.

{kind=link}

Grupo Galicia is more expensive than its country peers, BMA and BBAR, based on price to sales and price to book. However, the company is cheaper than Banco de Chile ( BCH ) and Banco do Brazil (BDORY). The tendency to hold higher prices than the other Argentinean banks is due to its better standing. As mentioned earlier, GGAL is the most progressive traditional bank.

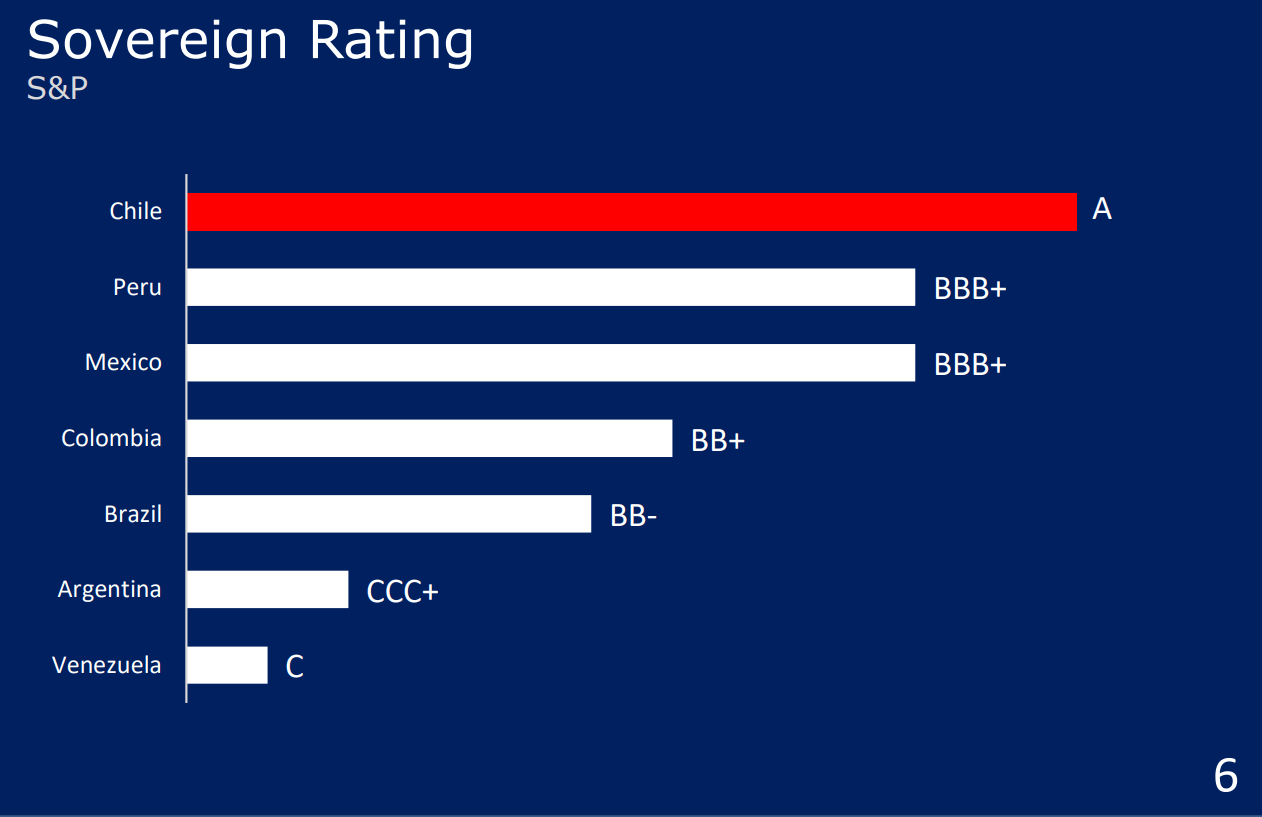

However, Banco de Chile is more expensive due to its safer jurisdiction. Chile has the highest credit rating among LATAM countries. The table below from the last Banco de Chile presentation compares Latin American country's S&P credit ratings:

{kind=link}

That explains the higher valuation for BDORY, too. However, the scary rating keeps the mispricing longer and makes the opportunity exist. That is true for all Argentinean stocks.

Risks

The mantra says you do not invest in Argentina. This is true for most investors. Investing in any emerging market, especially Argentina, comes with safety precautions. Many emerging economies are major exporters of commodities. Argentina is a key exporter of crops, livestock, oil, gas, and lithium. Its economy is a function of its prices; it is very cyclical.

On top of that, Argentina follows a pronounced political cycle. The political pendulum swings from left to right and right to left, and the equity markets follow accordingly. We might see another shift to the right in the October elections. Milei`s won PASO and now is the strongest contender for presidential office.

Investing in Argentina is a game of narratives, i.e., expect what the others expect. The expectations can create strong tailwinds moving all boats. The importance here is to protect your downside. This is the reason stock picking is crucial in macro investing, too. Even if everything is lined up for a parabolic move, an unexpected event can adversely affect the company or the industry. If the business does not have sufficient liquidity and solvency, it might not survive until sunrise.

Grupo Galicia manages the liquidity, credit, market, and operational risks well. The time deposits dominate on the liabilities side, and the loans have an average maturity of 6-18 months. Such maturity composition provides the bank with sufficient liquidity. The credit risk is diversified between individuals, SMEs, and agribusiness. The idiosyncratic operation risk is difficult to measure. It depends on quality factors such as business processes, leadership skills, and corporate culture.

In conclusion, the major risk for GGAL is the country risk. Argentina has a long history of poor political decisions, leaving the country's economy in ruins. The distinct cyclicality helps to determine where we are now. We just left the bottom, and the downside risk is relatively limited compared to the upside potential. In other words, Grupo Galicia is a safe bet by Argentinean standards, offering significant asymmetry in investors' favor.

Conclusion

Grupo Galicia is a traditional bank offering a wide range of services. The company has a few distinct advantages. The first is NaranjaX, the third most popular digital banking app. The second is the vital insurance segment, and the third is the company`s mutual funds. Despite being more expensive than its peers and excess value calculations, I give Grupo Galicia a buy rating due to its strong performance and macro tailwinds.

For further details see:

Grupo Galicia: Synergy Between Traditional Banking And Digital Transformation