GRPFF - Grupo Televisa: Lots Of Uncertainties As The Turnaround Stalls

2023-08-24 06:17:33 ET

Summary

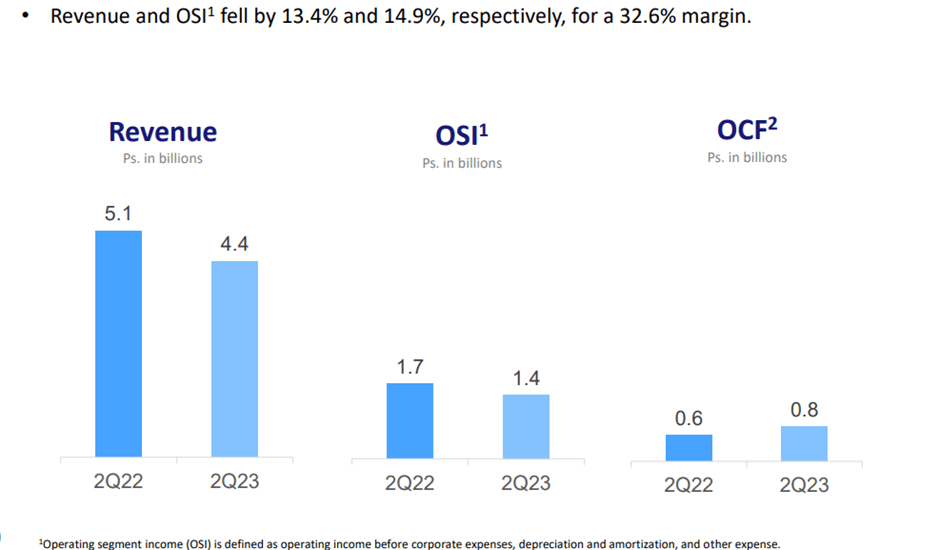

- Televisa's torrid last few months have extended into Q2.

- Churn rates are as high as ever in its core businesses, along with margin pressures.

- TV stock is cheap, but with no positive catalysts anytime soon, it's hard to underwrite much upside from here.

Grupo Televisa ( TV ) continues to underperform this year, with further Q2 churn in its core Cable and Sky (satellite pay-tv) businesses driving valuations lower. The key concern remains the lack of a turnaround at Sky (despite management's upbeat targets last year), while the outsized subscriber reaction to price hikes taken at Cable (vs. its peers that held firm) underscores the lack of pricing power at TV. Higher debt levels (per net debt/EBITDA) also remain an issue, which, combined with the lack of free cash generation, has led to slower progress on the company's buyback program this quarter.

To be clear, I still think TV stock is cheaply priced , particularly relative to its 45% stake in TelevisaUnivision ( worth the vast majority of its current equity value). And there's optionality too - the recent management change at TV's cable business and ongoing turnaround measures at Sky bode well for earnings long-term, while the healthy cash balance presents M&A upside. This needs to be balanced, however, against the prospect of increased competition from Megacable's ( OTCPK:MHSDF ) aggressive mid-term expansion plan and the company sustaining returns well below its cost of capital going forward. Pending concrete measures to unlock sum-of-parts value, I am turning neutral here.

Another Weak Quarter Amid A Challenging Operating Backdrop

Having started off the year with a failed cable merger with key peer Megacable, the industry's competitive intensity has ramped up, as reflected in another quarter of YoY profit declines for TV (reported EBITDA down 2% YoY). TV's cable segment ('Izzi'), which hosts internet, pay TV, and telephony services, led the EBITDA decline, with margins compressing 2.8 percentage points YoY to 39%. Some degree of weakness was expected heading into the print, given TV management's announced price increases in April (its peers held firm), but the cable churn of 5.4k was concerning. While the expiry of several promotions likely added to the headwinds, TV's clear lack of cable pricing power doesn't bode well ahead of Megacable's aggressive revenue/EBITDA expansion plan (double over the 2021 to 2026/2027 period).

{kind=link}

The other core business, Sky, which houses the satellite TV operations, hasn't delivered on its transformation goals (i.e., a shift in focus to returns over volumes). Against expectations for an EBITDA improvement in 2023, helped by a favorable YoY comparison (no World Cup amortization costs), segment EBITDA was down low-teens % YoY in Q2. Even after accounting for management's 'sales quality' rationale for the heavy net churn (now at -400k in H1 2023) and revenue decline, the simultaneous EBITDA margin compression (60bps to 33%) indicates a troubled turnaround. The silver lining here is that inflation pressures, a key driver for the profitability erosion over the last year, are easing. So, more opex/capex efficiencies and revenues expanding above a lower inflation rate could eventually boost the P&L. Still, underwriting a successful Sky turnaround remains challenging with little sign of easing churn rates or competitive pressures.

{kind=link}

Izzi Reshuffle Paves The Way For Another Turnaround

TV management issued a press release in June announcing that Francisco Valim, a telecom/media turnaround specialist with successful stints at Nextel Brazil and Oi, would be taking over from ex-CEO Jose Gonzalez as CEO of the cable business, Izzi. Given Mr Valim's focus on profitability (vs growth) in the past, expect a similar playbook at TV focusing on improved cash flow generation going forward.

While Sky's troubled return-focused turnaround shows success here is far from a given, the intent is encouraging given the historically poor cash generation at Cable. In turn, progress here (if it materializes) should boost the current low valuation the market is assigning to TV. That said, it isn't clear how Izzi's new management team can navigate the competitive implications of Megacable's expansion plan or its pricing power erosion anytime soon. So I'm optimistic but wouldn't underwrite a structural solution anytime soon.

Addressing The Capital Allocation Outlook

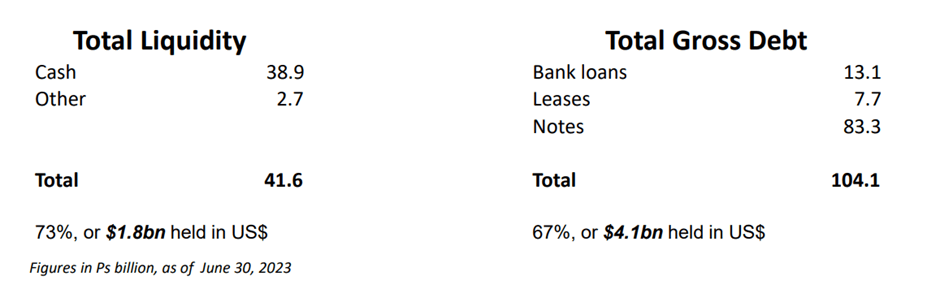

Progress on managing the balance sheet has also been somewhat disappointing, with net debt most recently reaching $3.6bn on working capital swings. Net of cash, this leaves TV's net debt to EBITDA at 2.45x (up from 2.39x in Q1 2023), constraining the pace of buybacks near-term. The ~$5m buyback in Q2, for instance, was well below Q1 levels and has likely left investors questioning if TV can deploy its full ~$0.6bn (or P$9.9bn) remaining authorization.

On the flip side, TV does still have a healthy gross cash balance, which provides optionality for value creation, for instance, via a revived Megacable merger or bolt-ons to strengthen its competitive positioning. Also worth looking out for are potential split-offs of its non-core assets, particularly its 45% stake in TelevisaUnivision, which could well command a significant % of TV's current market cap on a standalone basis.

{kind=link}

Lots Of Uncertainties As The Turnaround Stalls

TV is nowhere near out of the woods yet, as evidenced by its underwhelming Q2 2023 performance. With elevated net disconnections for both Cable and Sky confirming fears that TV is working against a highly elastic demand curve in an increasingly competitive environment, margins could see further downside from here. Even with some reprieve on the horizon from disinflation (vs. inflation over the last year) and cable peers eventually taking pricing action as well, TV still has a long way to go before its ROEs can sufficiently cover its cost of capital.

The balance sheet also needs work if investors are to give TV credit for its capital return plans and 45% stake in TelevisaUnivision (worth a significant chunk of the TV market cap). On the flip side, the management shake-up at Cable could be the start of a positive change - not only from a fundamental perspective but also for corporate action to unlock sum-of-parts value. For now, though, there are probably better ways to allocate capital in Mexico.

For further details see:

Grupo Televisa: Lots Of Uncertainties As The Turnaround Stalls