TV - Grupo Televisa: Wait For A Catalyst Before Buying

2023-12-01 12:20:00 ET

Summary

- Grupo Televisa has not been a very good investment over the past few years.

- The company is a fairly complex entity including a core cable business, a majority ownership stake in Sky Mexico, and a large minority interest in TelevisaUnivision.

- TV has recently experienced weakness in its core businesses due to a secular shift away from paid television.

- TV is trading at a a fairly attractive valuation but currently lacks an upside catalyst.

- I am initiating TV with a hold rating and would consider upgrading the stock if an upside catalyst emerges.

Grupo Televisa SAB ( TV ) has proved a very disappointing investment for shareholders over the past few years. Over the past 5 years, TV has delivered a total return of -80.8% compared to total returns of 81.9% and 56.7% delivered by the iShares MSCI ACWI ETF ( ACWI ) and the iShares MSCI Mexico ETF ( EWW ) over the same period of time.

TV has struggled due to secular headwinds related to the disruption of the traditional cable TV and satellite TV business by streaming players. I expect this disruption to continue going forward. TV currently has only modest levels of leverage but leverage could increase if the core business continues to deteriorate. Additionally, the company has a fairly complex operating structure with exposure to a number of different businesses with different growth prospects which makes the stock difficult to value.

For these reasons, despite the recent share price decline and attractive valuation I would wait for a catalyst to emerge before buying TV shares.

Company Overview

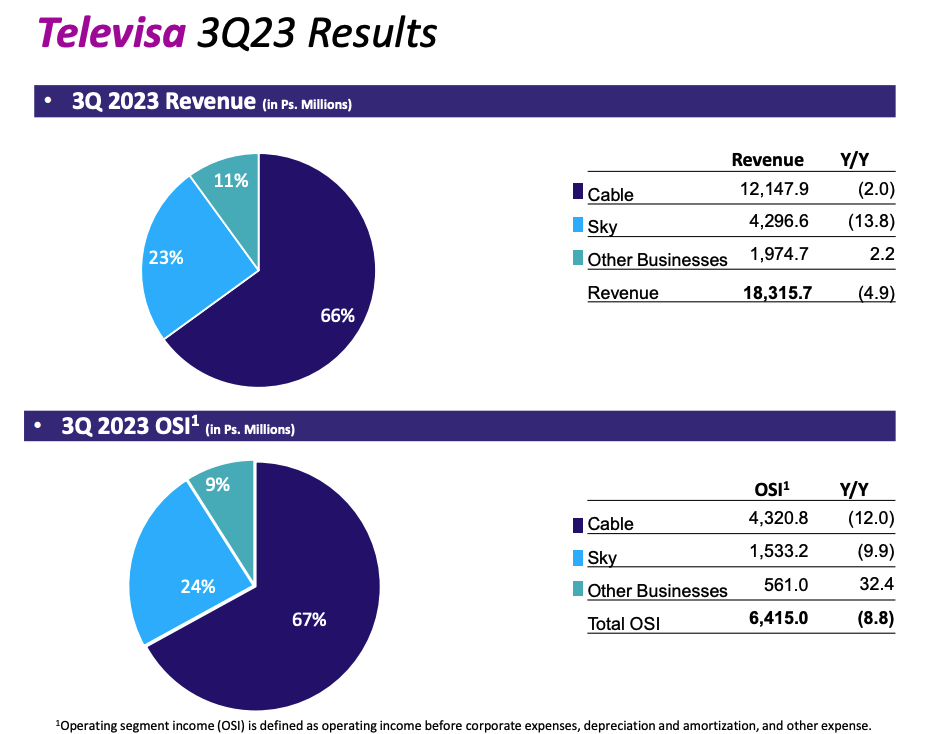

TV is a leading telecommunication company in Mexico. The company owns controlling interests in a number of Mexican cable companies. The company's cable business offers integrated services including video, high speed data, voice and mobile to residential and commercial customers as well as managed services to domestic and international carriers. TV's cable business accounts for ~66% of the company's total revenue and ~67% of total operating segment income ("OSI").

TV also owns a 58.7% interest in Sky, which is a leading DTH satellite pay television and broadband provider in Mexico. Sky also has operations in the Dominican Republic and Central America. Sky accounts for ~23% of the company's total revenue and ~24% of total OSI.

TV is the leading provider of paid television in Mexico with a 62.4% market share and is the second largest fixed broadband operator with a 25.9% market share.

In addition to these holdings, TV is also the largest shareholder of TelevisaUnivision, a leading producer of Spanish-language content in Mexico, the U.S., and many other countries. TelevisaUnivision offers its content via television networks, cable, and over-the-top ("OTT") streaming services. TelevisaUnivision is a key earnings driver for the company and would account for ~40% of revenue and EBITDA under the proportionate consolidation method.

TV also owns a number of other businesses including a magazine publishing business, a professional soccer team Club de Fútbol América S.A. de C.V., Azteca Stadium, and a gaming business called "PlayCity." These businesses currently account for ~11% of revenue and ~9% of OSI but are in the process of being spun off into a new entity which will be listed on the Mexican stock exchange.

Cable & Sky Businesses Are Experiencing Secular Headwinds

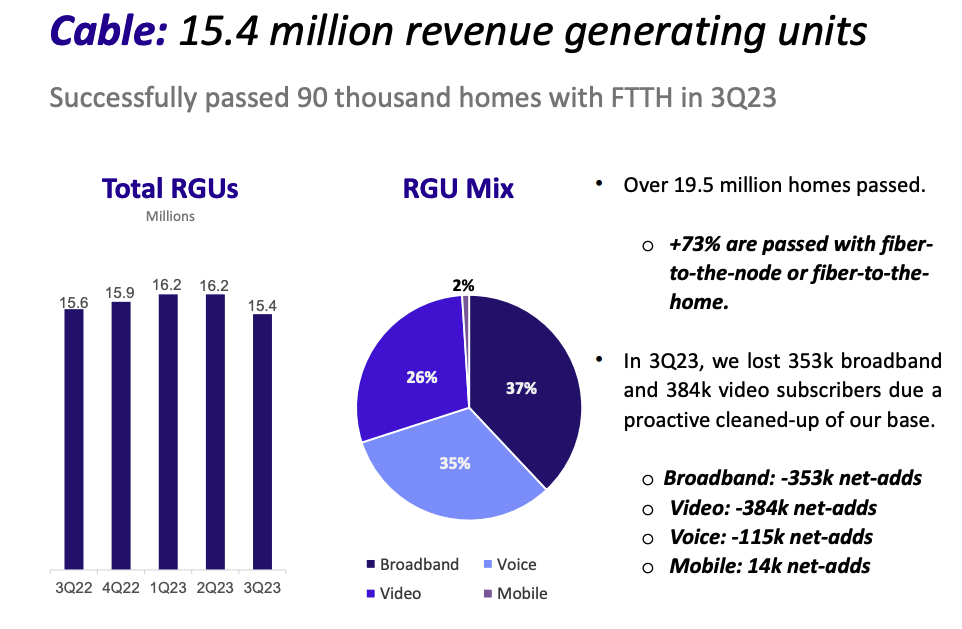

TV is facing significant secular headwinds due to a shift away from paid television in favor of over the top streaming offerings. As shown by the chart below, total revenue generating units ("RSUs") have decreased substantially over the past few quarters. Cable RSUs decreased by ~ 800,000 during 3Q 2023. Of these 800,000 ~ 392,000 were due to clean-up efforts initiated by the company to remove customers who have skipped payments. Thus, even after removing the effects of the clean-up efforts, TV still experienced significant cord cutting in its cable business.

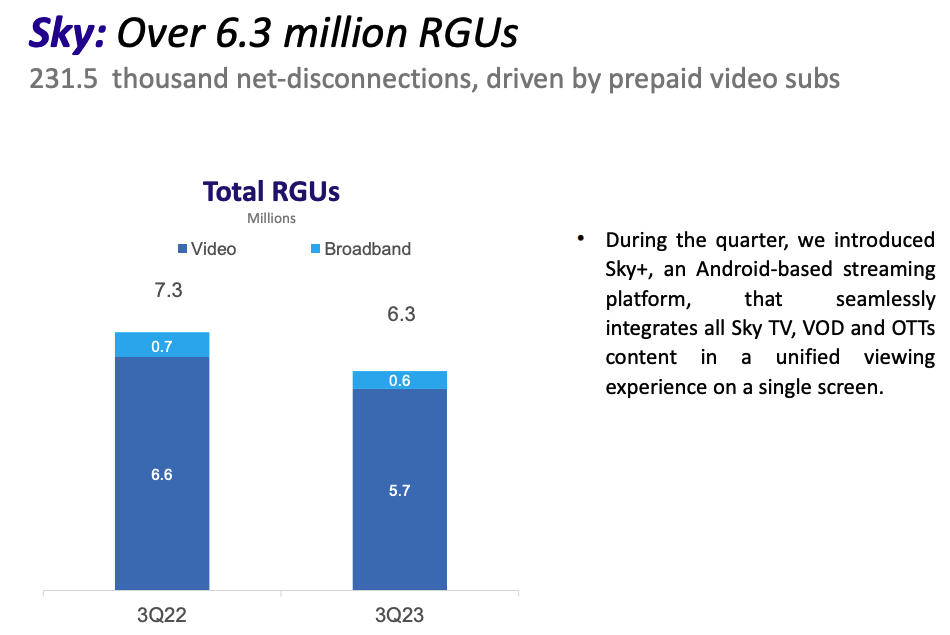

The story is similar in the company's Sky business which experienced a decrease of 213,500 RGUs during 3Q 2023 and a decrease of 1 million RGUs over the past year.

Subscriber declines have led to a significant drop in revenues and OSI. During Q3 2023, the company reported a total revenue decline of 4.9% on a year-over-year basis and a 8.8% decline on OSI on a year-over-year basis.

OSI margin dropped to 34.8% during 3Q 2023 from 36.4% during the same period a year ago. The decline in margins was driven by a 400 basis point decline in operating segment income for the cable business to 35.6% from 39.6%. The decline in margins is attributable to higher labor and content costs due to the impacts of inflation. In response to these factors, the company implemented a headcount reduction program during Q3 2023 which will save ~12% of payroll costs in Q4 2023.

{kind=link}

{kind=link}

{kind=link}

TeleviaUnivision Performance Has Been A Bright Spot

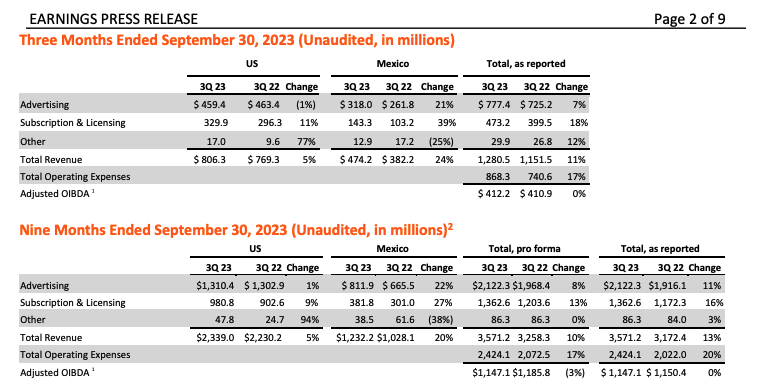

TV's 44% stake in TelevisaUnivision represents a significant part of TV's value and thus is a significant driver of TV stock. During 3Q 2023, TV reported 11% revenue growth on a year-over-year basis which was driven by strength in Mexico. For the nine month period ending 3Q 2023, TelevisaUnivision reported 13% revenue growth compared to the same period a year ago.

Despite strong revenue growth, TelevisaUnivision reported Adjusted OIBDA which was roughly flat vs the same period a year ago. The reason for this is that the company has been aggressively investing in its direct to consumer ("DTC") business, ViX which now has 40 million average monthly unique users. To put that number into context, Netflix ( NFLX ) has a global total of 247.1 million paid subscribers.

TelevisaUnivision has been focused on trying to improve margins in its D2C business and narrowed D2c losses by nearly 60% during the quarter. Wade Davis added the below color on the TV Q3 conference call:

This quarter, we narrowed our D2C losses by nearly 60%, and we continue to have direct line of sight to our target of D2C profitability by the second half of 2024. This is now only nine months away, and when we deliver this, ViX will have had the shortest ramp to profitability of any major streaming service in history.

And we can do this because of the unique content costs and the powerful marketing advantages we've created with the combined Televisa Univision business. We have a massively scaled, fully vertically integrated business operating across multiple platforms and leading in the largest Spanish speaking markets in the world. And our relentless focus on efficiency manifests on an overall consolidated basis with the highest operating margins in the industry. But this will be further underscored as we continue toward D2C profitability where we believe our margins will also be best-in-class.

{kind=link}

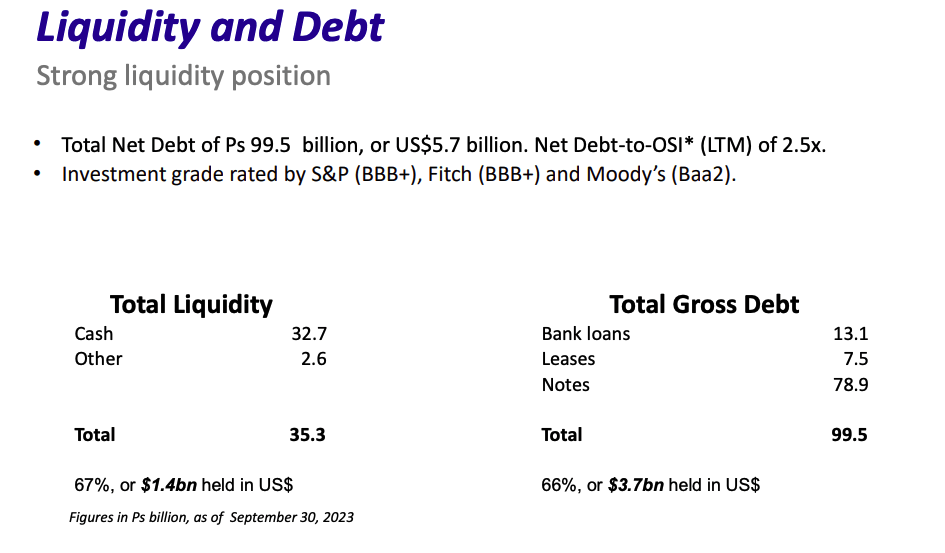

Moderate Leverage & Strong Liquidity

As shown by the table below, TV has a moderately levered balance sheet with Net Debt to OSI of 2.5x on an LTM basis. TV also has a strong total liquidity position of $1.4 billion. TV enjoys investment grade ratings from S&P, Fitch, and Moody's. Moreover, Fitch expects the company to continue reducing debt going forward.

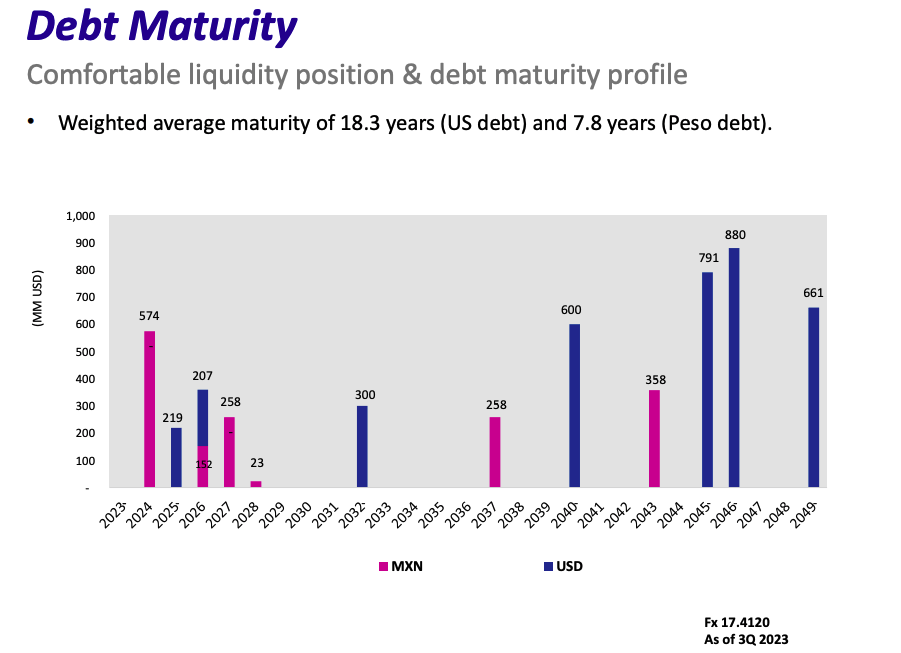

TV has a well laddered debt maturity schedule which is a positive as the company does not face a major maturity wall at one point.

While the company's financial position appears fairly strong right now, it should be noted that the leverage picture could change quickly if the core business continues to deteriorate.

{kind=link}

{kind=link}

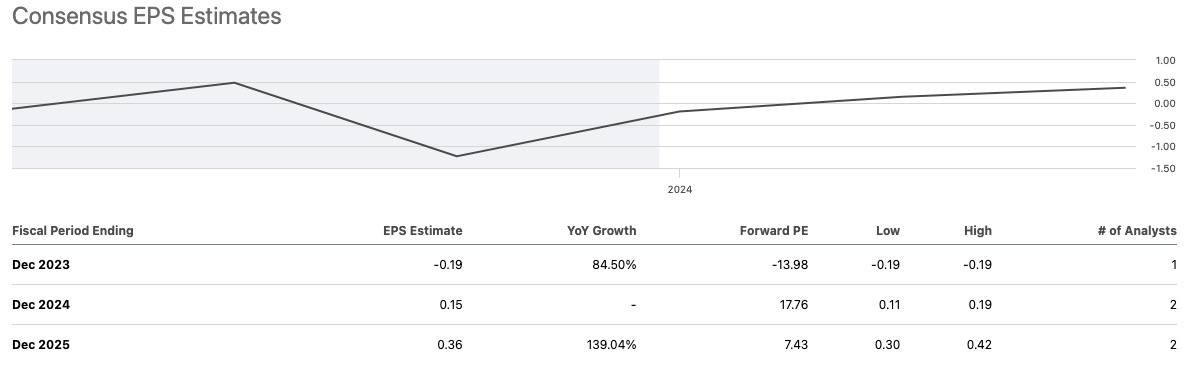

Growth Estimates

As shown by the table below, consensus estimates call for TV to achieve low single digit revenue increases over the next two years. However, consensus estimates call for significant EPS growth with EPS expected to be $0.15 for FY 2024 and $0.36 for FY 2025. These estimates strike me as reasonable given the company's recent financial performance. I believe the 2025 EPS target is aggressive and is highly dependent on a positive impact related to increased net income from TelevisaUnivision as B2C profitability improves. TV accounts for TelevisiaUnivision using the equity method and thus income or lesses from TelevisiaUnivision are included in TV's net income.

{kind=link}

{kind=link}

Dividend & Buyback

As shown by the chart below, TV currently pays a quarterly dividend of $0.10 and thus at current levels the stock carries a yield of ~3.7%. The dividend has been adjusted historically based on the strength of operating performance. Currently, TV receives a dividend safety score of D- from Seeking Alpha quant scores. While I do not expect the dividend to get cut in the near-term, I am not confident that the company will be able to sustain the current dividend if the core cable and sky businesses continue to weaken.

TV has been a modest repurchaser of its own stock over the past few years. The share count has been reduced by ~3.7% over the past five years. Given the company's relatively high debt load, I expect excess cash to be used to reduce debt given the current high interest rate environment. Thus, I do not anticipate the company to repurchase a significant amount of shares going forward over the near-term.

Seeking Alpha

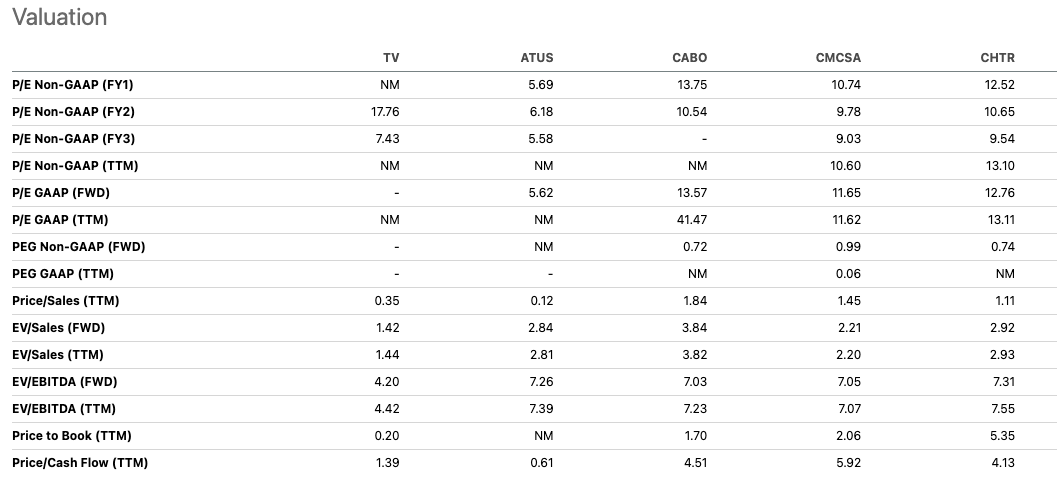

Valuation

Currently, TV receives a valuation score of "A" from Seeking Alpha quant ratings. I agree that TV's current valuation is relatively attractive though I am not sure it is an "A".

The two year forward P/E ratio of ~7.4x is attractive but that level of EPS is far from a sure thing as it requires significant improvement from current levels.

TV trades at just a forward EV/ EBITDA of just 4.2x. Comparably, U.S. peers such as ATUS, CABO, CMCSA, and CHTR trade closer to 7x forward EV/ EBITDA. Despite being a much larger company, CMCSA may represent the most appropriate comp given its ownership of NBC Universal.

In addition to trading at an attractive valuation relative to peers, TV is trading at the lower end of its historical valuation range during the period since the TelevisionUnivision transaction closed. This transaction marked a significantly shift in business mix for the company and thus I believe valuation relative to historical norm should be based off of this time period.

Seeking Alpha

{kind=link}

Potential Upside Catalysts

I believe one potential upside catalyst driver would be a simplification of TV's business. In its current form, TV is a highly complex entity to analyze given the mix of businesses which includes cable, a majority ownership interest in Sky, sports teams, publishing, a large but non majority stake in TelevisiaUnivision, among other holdings.

I believe further simplification of the company's structure will make the company easier for investors to analyze and thus more investible. TV's previously announced plan to spin-off its other businesses is a positive but that part of the business is relatively small. Even after the spin-off is accomplished, TV will remain a fairly complex company given its cable, Sky, and TelevisionUnivision businesses. One potential driver of value may be the IPO of TelevisionUnivision.

TelevisionUnivision is currently privately held and thus is not publicly traded. An IPO of that business would allow investors to put a value on TV's stake. Additionally, an IPO of Sky Mexico would also allow investors to put a market valuation on TV's 58.7% stake.

Another potential upside driver for TV is growth related to the ViX streaming platform which already has 40 million users and is poised to become profitable next year. Further growth and monetization of this business has potential to be a long-term value driver for TV given its large stake in TelevisiaUnivision.

Finally, another potential upside catalyst would be a stabilization of TV's core cable and satellite TV businesses. However, given the secular headwinds I believe this is unlikely in the near-term and the company may continue to lose subscribers over the next few quarters.

Conclusion

TV has proved a disappointing investment over the past few years as the company has experienced secular headwinds related to a move away from traditional paid television services.

TV is a fairly complex company currently with cable being the biggest driver followed by the company's significant equity investment in TelevisionUnivision. TV also own other businesses in the sports and gaming industries which account for a fairly small portion of revenue and earnings.

Currently TV is characterized by a fairly strong balance sheet. However, this could change in the event that the core business continues to experience weakness which has accelerated over the most recent quarter.

TV is trading at a fairly attractive valuation relative to peers and its own history. However, the stock lacks a catalyst.

I am initiating TV with a hold rating and would consider upgrading my rating if an upside catalyst emerges. I believe potential upside catalysts include a simplification of the company, growth in income from TelevisaUnivsion related to improved profitability of ViX, or a stabilization of the core business.

For further details see:

Grupo Televisa: Wait For A Catalyst Before Buying