GRX - GRX: There Are Better Alternatives In The Healthcare CEF Sector

2023-11-03 07:23:32 ET

Summary

- The Gabelli Healthcare & WellnessRx Trust is an underperforming equity closed-end fund (CEF) focused on healthcare stocks.

- GRX has a -19% discount to net asset value, but has traded at very substantial discounts for the past five years.

- The fund employs a 27% leverage ratio, which has hampered its performance in 2023.

- Retail investors are better off investing in ETFs like XLV or CEFs such as THQ for exposure to the healthcare equity space.

Thesis

The Gabelli Healthcare & WellnessRx Trust (GRX) is an equities closed-end diversified management investment company. The fund focuses on the healthcare space and seeks long-term growth of capital:

Under normal market conditions, the Fund will invest at least 80% of its net assets in equity securities and income producing securities of domestic and foreign companies in the healthcare and wellness industries. Companies in the healthcare and wellness industries are defined as those companies which are primarily engaged in providing products, services and/or equipment related to healthcare, medical, or lifestyle needs (i.e., nutrition, weight management, and food and beverage companies primarily engaged in healthcare and wellness).

Source: Semi-Annual Report

The CEF has an astounding -19% discount to net asset value, but the discount exists for a good reason:

When comparing GRX with the Health Care Select Sector SPDR ETF ( XLV ) and the Tekla Healthcare Opportunities Fund ( THQ ), the CEF underperforms quite significantly. On a five year lookback GRX is almost flat from a total return perspective, whereas XLV is up 51% and THQ is up 24%. Instead of being up 50% by investing in a plain vanilla healthcare ETF, an investor has the same amount after five years, not even factoring for inflation after buying GRX.

A CEF serves a number of purposes:

- introduction of leverage in a portfolio of securities

- active management with the goal of outperformance versus passive sectoral ETFs

- extraction of dividends from the underlying securities' returns (equity in our case)

When a CEF fails at several of its purposes as stated above, then it does not make sense to use the structure. GRX has failed to produce an outperformance versus a passive cheap ETF, and its usage of leverage has actually hampered performance via a higher expense ratio and magnification of negative returns. The CEF's historic underperformance is responsible for a high return of capital currently, which exceeds 90% as of the August distribution date.

There is not much to like about GRX at the moment. Its performance has been lagging, magnified by its leverage, and its large discount is fully justified. At this juncture a retail investor looking at the healthcare space is better served by XLV in the ETF space or THQ in the CEF arena.

Holdings and Performance

Its poor historic performance has been driven by its individual name selection, which has failed to capitalize on the stocks which have provided growth in the market in the past year. Let us have a look:

Top Holdings (Author / Seeking Alpha)

This year Eli Lilly ( LLY ) has been an outstanding stock, not only in the healthcare sector, but the market overall. LLY has been a large positive contributor towards XLV's performance, but is not present at all in the GRX portfolio. In fact, if we look at the top 5 names in each fund we can visually identify the culprits for the difference in performance. Four out of the five top names in GRX are deep in the red for 2023, whereas the top two names in XLV are in the green, with the discussed LLY an outperformer.

UnitedHealth (UNH) is present in the GRX portfolio, but it has a 0.25% weighting, versus more than 10% in XLV. Individual name selection matters, especially in a tough market like today's. When looking at the overall valuation metrics for the healthcare sector we can see a flat fair value, meaning the sector overall has not been in a bubble that subsequently deflated.

Analytics

- AUM: $0.13 billion.

- Sharpe Ratio: -0.08 (3Y).

- Std. Deviation: 19 (3Y).

- Yield: 7.4%.

- Premium/Discount to NAV: -19%.

- Z-Stat: -1.47.

- Leverage Ratio: 27%.

- Effective Duration: n/a

- Composition: Healthcare Equities

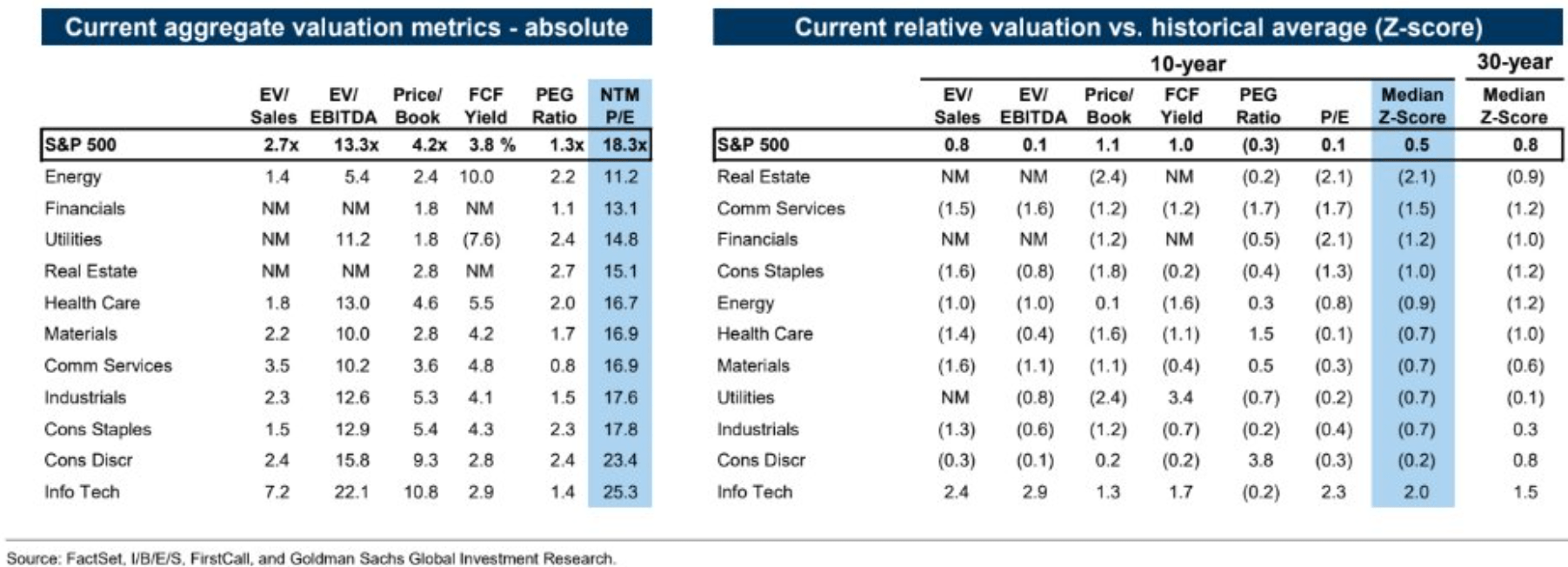

Healthcare Sector Valuation Metrics

The healthcare equity sector is currently trading at a 16.7x P/E ratio:

{kind=link}

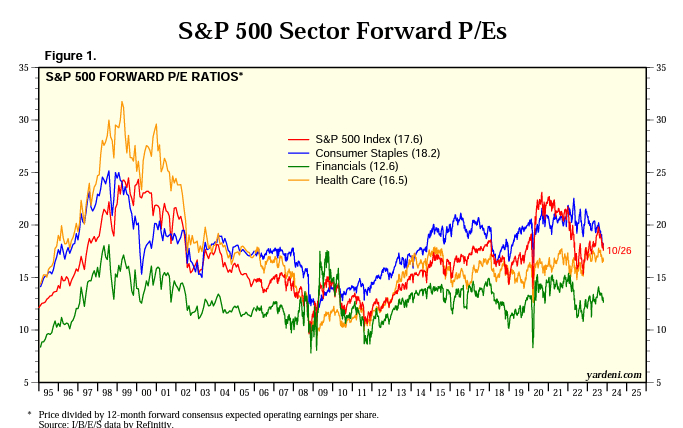

The metric is in line with its historic levels, as shown in the low median z-score. A more graphic representation of the same story can be found below from Yardeni:

{kind=link}

The orange line in the above graph represents the historic P/E ratio for the healthcare sector. Currently the line is fairly flat versus its levels in the past decade, which tells the same story of sectoral fair value. From an optics standpoint please compare the orange line with the red line, which is the S&P 500 valuation. Notice the large 'pop' in the S&P 500 P/E ratio during the zero rates environment in 2020/2021. The index is now de-rating, with only the "Magnificent 7' propping up the bubble level P/E ratios.

Premium/Discount to NAV

GRX is currently trading with a very large -19% discount to net asset value:

Despite the large figure, do note that GRX has historically traded with a -16% discount, thus today's figure, while large on an absolute basis, represents just a slight deviation from the fund's usual numbers.

We are comparing GRX with another healthcare CEF we covered, namely THQ. We can see that THQ's discount actually narrowed to flat in 2021/2022, while GRX's stayed at the same levels. There is an ongoing merger which has pushed THQ's discount wider, but historically if a retail investor is playing for a narrowing of a discount, THQ looks much more attractive than GRX.

Distribution Coverage

Given its large drawdown in the past year, the CEF is currently using a very significant amount of return of capital:

Based on the accounting records of the Fund currently available, each of the distributions paid to common shareholders in 2023 would include approximately 2% from net investment income, 5% from net capital gains and 93% would be deemed a return of capital on a book basis.

ROC utilization for equity CEFs is not unusual, especially during periods when the underlying names are not performing. A retail investor needs to keep in mind that a CEF structure simply sells equities and crystalizes capital gains in order to generate dividends. When there are no capital gains to be had, the fund needs to use the return of capital feature.

Long term underperformance translated into continuous ROC utilization is long term destructive since it shrinks the NAV and the capability of the fund to recover long term, but it is not the case here:

On a ten year basis we can see the CEF having a very stable NAV, meaning the portfolio managers are doing a good job of not overdistributing. So although the ROC is high currently, it should not be a concern in itself given the historic track record here.

Conclusion

GRX is an equity CEF. The vehicle focuses on healthcare stocks, but has severely underperformed in the past years. The market has punished the fund by trading it at a very large discount to net asset value, discount which is -19% currently. We think this figure is justified since GRX is flat from a total return perspective on a five year lookback, while a simple passive ETF such as XLV is up 51%. Do not expect GRX's discount to narrow any time soon, and moreover the CEF usually trades with a -16% discount historically, thus making any narrowing marginal at best. Retail investors looking for exposure in the healthcare equity space are best served by looking at XLV or THQ.

For further details see:

GRX: There Are Better Alternatives In The Healthcare CEF Sector